India Heat Exchangers Market Report: Trends, Growth and Forecast (2026-2032)

By Product Type (Shell & Tube Heat Exchangers, Plate Heat Exchangers, Air Cooled Heat Exchangers, Finned Tube Heat Exchangers, Others), By Industry (Power Generation, Chemical & Petrochemical, Oil & Gas, Automotive & Manufacturing, Food & Beverage/Pharma, HVAC/Building Services, Others), By Application (Process Heating/Cooling, Energy Recovery/Waste Heat Recovery, Refrigeration & Air Conditioning, Steam Condensation/Boiler Systems, Others), By Material Type (Stainless Steel, Carbon Steel, Copper, Aluminum, Others), By Region (North, East, West, South) ... Read more

|

Major Players

|

India Heat Exchangers Market Statistics and Insights, 2026

- Market Size Statistics

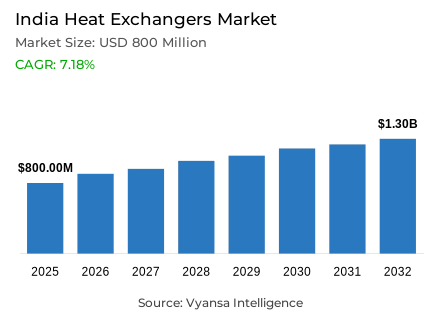

- Heat exchangers market size in India was valued at USD 800 million in 2025 and is estimated at USD 890 million in 2026.

- The market size is expected to grow to USD 1.3 billion by 2032.

- Market to register a CAGR of around 7.18% during 2026-32.

- Product Type Shares

- Shell & tube heat exchangers grabbed market share of 55%.

- Competition

- More than 10 companies are actively engaged in producing heat exchangers in India.

- Top 5 companies acquired around 55% of the market share.

- Heatex Industries Ltd., Kinam Engineering Industries, Universal Heat Exchangers Limited, Thermax Limited, HRS Process Systems Limited etc., are few of the top companies.

- Material Type

- Stainless steel grabbed 40% of the market.

India Heat Exchangers Market Outlook

The India heat exchangers market was valued at USD 800 million in 2025, establishing a commercially stable and industrially well-anchored foundation within one of Asia's most actively expanding process and energy equipment ecosystems. Projected to advance from USD 890 million in 2026 to USD 1.3 billion by 2032, the sector registers a GAGR of 7.18% across the forecast horizon. This measured and structurally supported expansion trajectory reflects the sustained growth of India's power generation capacity, refining throughput, and manufacturing output, all of which generate consistent and compounding demand for reliable thermal management equipment across industrial plant environments. Growth is anchored in operational necessity rather than cyclical capital spending, giving this market a commercial resilience that sustains procurement activity across diverse end-use industries and economic conditions.

The product architecture defining this market's commercial structure is anchored in shell and tube configurations. Shell and Tube heat exchangers command approximately 55% of total product type market share, reflecting the deep and structurally embedded industrial preference for thermal transfer equipment whose design maturity, operational reliability, and broad application compatibility make it the reference product type across power, refining, chemical processing, and manufacturing environments. This concentration confirms that Indian industrial buyers continue to prioritize proven thermal management solutions whose performance credentials are validated across decades of high-volume industrial deployment, sustaining disproportionate procurement share within a product category whose versatility and operational familiarity create natural and durable demand advantages over alternative heat exchanger configurations.

The material architecture reinforces the primacy of stainless steel as the category's dominant fabrication preference. Stainless Steel commands approximately 40% of total material type market share, reflecting the consistent industrial buyer preference for fabrication materials that combine corrosion resistance, structural durability, and reliable long-service performance across the demanding operating conditions of India's process-intensive industrial environments. The Bureau of Indian Standards' issuance of the Stainless Steel Pipes and Tubes Quality Control Order on 10 February 2025, with implementation of welded pipe and tube standards from 1 August 2025, confirms that quality compliance expectations around stainless steel components are tightening in ways that reinforce specification-grade material selection as a procurement standard rather than a discretionary quality preference.

The forward outlook through 2032 is defined by four converging structural forces whose combined commercial impact creates a heat exchangers market of steady and well-grounded expansion momentum. India's installed power capacity reaching 524,009.46 MW as of February 2026, documented by the Central Electricity Authority, sustains institutional demand for thermal management equipment across generation and associated industrial operations. Cumulative crude processing reaching 133,892.41 thousand metric tonnes during April to September 2025, a 1.23% year-on-year increase per the Ministry of Petroleum and Natural Gas, confirms the refining sector throughput that sustains consistent heat exchanger replacement and new installation demand. The Bureau of Energy Efficiency's PAT Cycle VII covering 707 designated consumers with an 8.485 MTOE energy-saving target is progressively focusing industrial buyers on thermal optimization investments. The Ministry of Steel's allocation of USD 49.03 million for green hydrogen pilot projects under the National Green Hydrogen Mission is opening new specialized application demand for heat exchangers in low-carbon industrial processes over the forecast period.

India Heat Exchangers Market Growth Driver

Industrial Expansion Sustains Core Equipment Demand

The sustained and institutionally documented expansion of India's power generation capacity and petroleum refining throughput represents the primary structural driver of heat exchanger demand, functioning as a persistent procurement imperative that sustains consistent equipment installation, replacement, and maintenance investment across India's most thermally intensive industrial operating environments. This industrial capacity-driven demand dynamic transcends cyclical capital expenditure fluctuations, reflecting a durable operational necessity whose procurement volume generation is structurally anchored in the irreducible thermal management requirements of industrial plants whose continuous process performance depends on reliable and consistently maintained heat transfer equipment across every stage of the production cycle.

The quantitative evidence validating this capacity-driven demand dynamic is documented with precision across official Indian government sources. India's installed power capacity reached 524,009.46 MW as of 28 February 2026 per the Central Electricity Authority, establishing the national generation infrastructure scale that sustains consistent demand for cooling, heat recovery, and thermal transfer equipment across power plants and their industrial support systems. The Ministry of Petroleum and Natural Gas documents cumulative crude processed during April to September 2025 reaching 133,892.41 thousand metric tonnes, a 1.23% increase over the corresponding prior year period, confirming that refining throughput growth is generating expanding heat exchanger procurement requirements across India's most thermally intensive processing operations. These capacity and throughput metrics validate an industrial demand base of sufficient scale and growth momentum to sustain structural heat exchanger market expansion.

India Heat Exchangers Market Challenge

Input Pressures Keep Execution Tight

The structural reliance on imported finished steel inputs combined with the progressively tightening quality compliance obligations surrounding stainless steel components used in industrial heat exchanger fabrication represents the most consequential operational challenge confronting Indian heat exchanger manufacturers, creating systematic procurement cost, sourcing timeline, and certification compliance burdens that elevate production economics and constrain margin management across a competitively price-sensitive industrial equipment market. In a fabrication environment where stainless steel material costs represent a substantial proportion of total manufacturing cost, and where import dependency creates exposure to global steel price volatility and supply chain disruption, procurement planning and cost control discipline function as primary determinants of commercial viability for heat exchanger manufacturers competing on both quality and price.

The structural depth and regulatory specificity of this manufacturing challenge are documented with precision by the Ministry of Steel and the Bureau of Indian Standards. The Ministry of Steel documents that India was a net importer of finished steel during FY 2025, with imports exceeding exports by 46.93 lakh tonnes, confirming the scale of import dependency that exposes heat exchanger manufacturers to global steel supply and pricing dynamics beyond domestic policy control. The Bureau of Indian Standards' issuance of the Stainless Steel Pipes and Tubes Quality Control Order on 10 February 2025, with implementation for stainless steel welded pipes and tubes for general service from 1 August 2025, confirms that certification compliance obligations around key fabrication inputs are advancing toward mandatory standardization. For manufacturers, this combination of import exposure and rising compliance obligations demands simultaneous investment in supply chain diversification, inventory management discipline, and certification readiness infrastructure.

Unlock Market Intelligence

Explore the market potential with our data-driven report

India Heat Exchangers Market Trend

Efficiency-Led Thermal Upgrades Gain Ground

The systematic implementation of energy efficiency performance targets and carbon credit trading obligations across India's most energy-intensive industrial sectors represents the defining structural trend reshaping heat exchanger procurement priorities, specification standards, and investment justification frameworks across the market's most commercially significant buyer segments. This regulatory efficiency and decarbonization trend is moving the procurement conversation around heat exchangers beyond standard equipment replacement decisions into the domain of measurable thermal performance improvement, energy intensity reduction, and emissions management, dimensions that are progressively redefining how industrial buyers evaluate heat exchanger investment value and specify equipment performance requirements.

The regulatory specificity and sectoral scope of this efficiency and decarbonization trend are documented with authority by the Bureau of Energy Efficiency and the Ministry of Power. The Bureau of Energy Efficiency's PAT Cycle VII covers 707 designated consumers with an overall energy-saving target of 8.485 MTOE, creating a structured institutional framework that focuses industrial buyer attention on thermal optimization investments whose documented energy performance improvements deliver both compliance credit value and operational cost reduction. The Ministry of Power notified the Carbon Credit Trading Scheme on 5 February 2026, with greenhouse gas emission intensity targets already notified for seven energy-intensive sectors under the compliance mechanism, confirming that carbon performance obligations are being formalized into the operating accountability frameworks of India's most industrially significant heat exchanger buyer segments. As these regulatory frameworks deepen their operational influence, thermal efficiency improvement becomes a strategic investment priority rather than an optional performance aspiration.

India Heat Exchangers Market Opportunity

Green Hydrogen Opens a New Application Lane

The active deployment of green hydrogen pilot projects across India's steel and heavy industry sectors creates a structurally significant and commercially tangible opportunity for heat exchanger manufacturers capable of designing and fabricating thermal management solutions optimized for the specific process conditions of hydrogen-based industrial operations. This green hydrogen opportunity is distinguished from conventional replacement demand by its application novelty, its engineering specialization requirements, and its policy-backed funding certainty, creating procurement conditions where thermal management capability and process engineering expertise carry disproportionate commercial weight relative to price competition alone. For manufacturers with relevant engineering credentials and material science capability, green hydrogen applications represent a high-value demand segment whose growth trajectory is structurally supported by India's National Green Hydrogen Mission investment commitments.

The quantitative scale and operational specificity of this green hydrogen opportunity are documented with precision by the Ministry of Steel. A total of USD 49.03 million has been allocated for pilot projects for the use of green hydrogen in the steel sector under the National Green Hydrogen Mission, confirming the institutional investment commitment behind green hydrogen's industrial deployment trajectory. Two pilot projects have been awarded to produce DRI using 100% hydrogen in vertical shafts, while one pilot project has been awarded to use hydrogen in an existing blast furnace to reduce coal and coke consumption, confirming that active engineering and equipment procurement activity is already underway across hydrogen-linked steel production applications. As these projects progress from pilot phases into broader operational deployment, demand for specialized heat exchanger designs suited to hydrogen process environments including heat recovery, process stabilization, and temperature control applications will expand progressively. Manufacturers that develop engineering capability and material qualification credentials for green hydrogen thermal management applications will capture disproportionate value from this structurally significant and policy-supported market opportunity over the forecast period.

Unlock Market Intelligence

Explore the market potential with our data-driven report

India Heat Exchangers Market Segmentation Analysis

By Product Type

- Shell & Tube Heat Exchangers

- Plate Heat Exchangers

- Air Cooled Heat Exchangers

- Finned Tube Heat Exchangers

- Others

The segment with highest market share under the product type is shell & tube heat exchangers, accounting for approximately 55% of the total market. This commanding position reflects the deep structural alignment between shell and tube design characteristics and the specific thermal management requirements of India's most industrially active sectors, where operational reliability under continuous high-load conditions, broad compatibility with diverse process fluids and temperature ranges, and the availability of established maintenance and servicing infrastructure make this configuration the unambiguous product of choice across energy, refining, chemical, and manufacturing procurement contexts. With more than half of total market value concentrated within a single product category, Shell and Tube heat exchangers define the commercial priorities, fabrication investment frameworks, and competitive strategy of the India heat exchangers market.

The structural leadership of Shell and Tube heat exchangers is further sustained by the industrial familiarity and application breadth that have made this configuration the default thermal management specification across India's most capital-intensive process industries. As plant operators invest in thermal efficiency upgrades under the Bureau of Energy Efficiency's PAT Cycle VII framework and green hydrogen pilot projects advance into active deployment, shell and tube configurations are well positioned to capture disproportionate share of both retrofit and new installation demand given their established engineering credentials and broad compatibility with emerging low-carbon process applications. The segment's structural dominance as the market's primary revenue contributor and competitive focal point is expected to remain comprehensively intact over the forecast period.

By Material Type

- Stainless Steel

- Carbon Steel

- Copper

- Aluminum

- Others

The segment with highest market share under the Material Type is Stainless Steel, accounting for approximately 40% of the total market. This dominant position reflects the industrial procurement reality that corrosion resistance, fabrication consistency, and long service life under chemically aggressive and thermally demanding operating conditions are non-negotiable performance requirements across India's process-intensive industrial environments, where equipment failure consequences include both operational disruption and significant safety risk. With two-fifths of total market value anchored in stainless steel fabricated equipment, this material category defines the quality benchmarks, specification standards, and supplier capability requirements of the India heat exchangers market, establishing the performance credibility threshold against which alternative material options are evaluated across procurement decisions.

The structural leadership of Stainless Steel is being actively reinforced by the tightening quality compliance environment surrounding steel components used in industrial heat transfer equipment. The Bureau of Indian Standards' issuance of the Stainless Steel Pipes and Tubes Quality Control Order on 10 February 2025, with implementation for stainless steel welded pipes and tubes for general service from 1 August 2025, confirms that certification and quality compliance obligations around stainless steel components are advancing toward mandatory standardization rather than voluntary quality assurance. This regulatory quality elevation creates procurement conditions that favor heat exchanger manufacturers with established stainless steel fabrication capability and certification-ready supply chains over less-organized competitors. Stainless Steel's structural position as the market's dominant material specification is expected to deepen over the forecast period.

List of Companies Covered in India Heat Exchangers Market

The companies listed below are highly influential in the India heat exchangers market, with a significant market share and a strong impact on industry developments.

- Heatex Industries Ltd.

- Kinam Engineering Industries

- Universal Heat Exchangers Limited

- Thermax Limited

- HRS Process Systems Limited

- Isgec Heavy Engineering Ltd.

- Kirloskar Brothers Limited (KBL)

- BGR Energy Systems Limited

- Artson Engineering Limited

Market News & Updates

- Thermax Limited, 2025:

Thermax said it was intensifying investments in digital transformation and manufacturing capabilities, while its current Cooling and Heating Solutions portfolio highlights 8,300+ installations across 100+ markets and its dry-cooling range includes air-cooled heat exchangers and dry coolers spanning 100 kW to 10 MW, supported by broader system integration that uses high-efficiency heat exchangers to reduce energy use, water consumption, and emissions. For India’s heat exchanger market, this is significant because it shows one of the country’s major thermal engineering players strengthening scale, manufacturing readiness, and water-efficient thermal offerings at a time when industrial users are increasingly prioritizing resource-efficient cooling and energy-transition-aligned equipment.

- BGR Energy Systems Limited, 2025:

In its 2025 official ACHE materials, alongside its Air Fin Cooler division profile, BGR Energy stated that it is the market leader in India for this segment, designs and manufactures air-cooled heat exchangers to ASME and API specifications, and has installations in 29+ countries, with annual finning capacity of 4,118 km, header box capacity of 1,070, and tube bundle capacity of 750. For the Indian heat exchanger market, this is one of the clearest verified operational updates among the named players because it signals substantial domestic manufacturing depth in air-cooled and finned-tube exchangers, reinforcing India’s ability to supply refinery, petrochemical, fertilizer, steel, and process-industry demand through local capacity.

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- India Heat Exchanger Market Policies, Regulations, and Standards

- India Heat Exchanger Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- India Heat Exchanger Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Product Type

- Shell & Tube Heat Exchangers- Market Insights and Forecast 2022-2032, USD Million

- Plate Heat Exchangers- Market Insights and Forecast 2022-2032, USD Million

- Air Cooled Heat Exchangers- Market Insights and Forecast 2022-2032, USD Million

- Finned Tube Heat Exchangers- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By Industry

- Power Generation- Market Insights and Forecast 2022-2032, USD Million

- Chemical & Petrochemical- Market Insights and Forecast 2022-2032, USD Million

- Oil & Gas- Market Insights and Forecast 2022-2032, USD Million

- Automotive & Manufacturing- Market Insights and Forecast 2022-2032, USD Million

- Food & Beverage/Pharma- Market Insights and Forecast 2022-2032, USD Million

- HVAC/Building Services- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By Application

- Process Heating/Cooling- Market Insights and Forecast 2022-2032, USD Million

- Energy Recovery/Waste Heat Recovery- Market Insights and Forecast 2022-2032, USD Million

- Refrigeration & Air Conditioning- Market Insights and Forecast 2022-2032, USD Million

- Steam Condensation/Boiler Systems- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By Material Type

- Stainless Steel- Market Insights and Forecast 2022-2032, USD Million

- Carbon Steel- Market Insights and Forecast 2022-2032, USD Million

- Copper- Market Insights and Forecast 2022-2032, USD Million

- Aluminum- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By Region

- North

- East

- West

- South

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Product Type

- Market Size & Growth Outlook

- India Shell & Tube Heat Exchangers Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Industry- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Material Type- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- India Plate Heat Exchangers Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Industry- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Material Type- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- India Air Cooled Heat Exchangers Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Industry- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Material Type- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- India Finned Tube Heat Exchangers Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Industry- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Material Type- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- Thermax Limited

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- HRS Process Systems Limited

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Isgec Heavy Engineering Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Kirloskar Brothers Limited (KBL)

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- BGR Energy Systems Limited

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Heatex Industries Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Kinam Engineering Industries

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Universal Heat Exchangers Limited

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Artson Engineering Limited

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Others

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Thermax Limited

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Product Type |

|

| By Industry |

|

| By Application |

|

| By Material Type |

|

| By Region |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.