Netherlands Menstrual Care Market Report: Trends, Growth and Forecast (2026-2032)

By Product Type (Pantyliners, Tampons (Applicator Tampons, Digital Tampons), Towels (Standard Towels (Standard Towels with Wings, Standard Towels Without Wings), Slim/Thin/Ultra-Thin Towels (Slim/Thin/Ultra-Thin Towels with Wings, Slim/Thin/Ultra-Thin Towels Without Wings)), Intimate Wipes, Menstrual Cups, Period Underwear), By Nature (Disposable, Reusable), By Age Group (Up to 18 Years, 19-30 Years, 31-40 Years, 40 Years and Above), By Sales Channel (Retail Offline, Retail Online) ... Read more

|

Major Players

|

Netherlands Menstrual Care Market Statistics and Insights, 2026

- Market Size Statistics

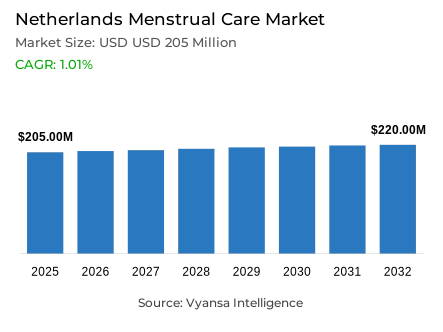

- Menstrual care in Netherlands is estimated at USD 205 million in 2025.

- The market size is expected to grow to USD 220 million by 2032.

- Market to register a cagr of around 1.01% during 2026-32.

- Product Type Shares

- Towels grabbed market share of 40%.

- Competition

- More than 10 companies are actively engaged in producing menstrual care in Netherlands.

- Top 5 companies acquired around 80% of the market share.

- Kimberly-Clark BV; Etos BV; FIP Organic BV; Procter & Gamble Nederland BV; Essity Nederland BV etc., are few of the top companies.

- Sales Channel

- Retail offline grabbed 80% of the market.

Netherlands Menstrual Care Market Outlook

he Netherlands menstrual care market is expected to record a modest growth, which is projected to increase to an estimated USD 205 million in 2025 to an estimated USD 220 million in 2032, with a compound annual growth rate (CAGR) of about 1.01% over the forecast period 2026-2032. The growth trends are predicted to be stable and slowing compared to the previous times, with the overall demand trends being influenced by the softening of inflationary pressures and the uptake of reusable options. Towels, with a market share of about 40%, will remain the top performers in sales because of their convenience and effectiveness, but competition is expected to increase with the rise of sustainability and affordability factors among the end-user groups.

Pantyliners will continue to be the most vibrant product category, with increasing usage among women on oral contraceptives and an ageing demographic group with mild incontinence conditions. Their multifunctional nature is not limited to the conventional use of menstrual care, which further reinforces their practical use as a daily hygiene product. On the other hand, tampons and towels can have moderate growth rates because reusable products will gain popularity in the market due to the continuous educational programs and marketing campaigns that will emphasize the positive environmental effects and cost-saving in the long run.

The current distribution infrastructure is dominated by retail offline channels, which currently contribute to almost 80% of the volume of menstrual care sales. The health-and-beauty store formats, supermarket operations, and drugstore establishments remain popular among the end-users due to their extensive assortments and regular promotional events. Nevertheless, the e-commerce platforms are growing at an alarming rate due to the competitive pricing systems, non-obtrusive delivery systems, and the ease of subscription-based systems. The role of platforms like bol.com and deonlinedrogist.nl in the future of purchasing behaviour is likely to become more important.

During the forecast period, innovation efforts will be more directed at the creation of reusable menstrual solutions. Large brand organizations are strategically placed to expand their product lines to include menstrual cups, washable pads, and period underwear to respond to the sustainability issues. Although the disposable product alternatives will continue to have a market presence, the next stage of the Netherlands menstrual care market will be characterized by strategic investment in the eco-friendly and reusable design architectures.

Netherlands Menstrual Care Market Growth Driver

Rising Hygiene Awareness and Innovation in Menstrual Products Boost Market Growth

The growing consciousness of personal hygiene and comfort is a trend that is still growing in the Netherlands Menstrual Care Market. Women are increasingly demanding new product solutions that will offer reliability and convenience during menstrual periods. According to Eurostat and World Bank statistics, women constitute about 50.32% of the Dutch population in 2024, thus creating a stable and large user demographic base. This increased hygiene awareness, combined with the need to have effective, ultra-thin, absorbent and dermatologically safe product formulations, is what is driving the rate of product adoption and the rate of innovation.

To improve useregence, manufacturers use sustainable material compositions and refined design architectures, and they always focus on comfort optimization, safety assurance, and hygiene efficacy. The World Health Organization (WHO) emphasizes that menstrual hygiene practices can improve the health outcomes and social participation of women, which forms a pillar that supports demand among various demographic groups, such as economically active women and adolescents.

Netherlands Menstrual Care Market Challenge

Economic Pressures and Price Sensitivity Constrain Premium Product Adoption

Economic uncertainty and inflationary pressures have a strong impact on consumer budget allocations and hence on the adoption patterns of premium menstrual products. According to Eurostat, the average inflation rate in the Netherlands was about 3.1% in 2024, which led to a consumer shift to cost-efficient menstrual care products sold under their own-label brand portfolios. This price-sensitivity dynamic puts pressure on premium brand entities to strike a balance between innovation requirements and affordability concerns to retain market share.

According to consumer confidence data provided by Statistics Netherlands (CBS), the level of confidence was lower than the pre-pandemic levels during the entire year 2024, thus, adding to the reserved spending habits. This macroeconomic situation increases the competition between manufacturers and creates a limited market situation of high-value menstrual care products, which favors competitively priced substitutes.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Netherlands Menstrual Care Market Trend

Sustainability and Reusable Alternatives Transform End-User Preferences

The concept of sustainability is one of the key trends that fundamentally transforms the Dutch menstrual care market environment. The European Environment Agency (EEA) reports that almost 68% of the citizens of the European Union are in favor of sustainable consumption programs, such as waste-cutting programs. Eurostat confirms that the Netherlands has one of the highest recycling rates in the EU, which is more than 60%. This environmentally aware social environment creates an increasing consumer demand towards reusable menstrual cups, washable pad substitutes, and biodegradable products.

The existing consumer trend trajectories are supplemented by Dutch policy frameworks that focus on environmental responsibility and the principles of the circular economy. This sustainability orientation promotes brand organizations to be innovative and diversify their product lines, emphasizing durability features, environmentally friendly material structures, and low environmental footprint as important buying factors.

Netherlands Menstrual Care Market Opportunity

Expanding Retail Online and Digital Engagement to Drive Future Growth

The menstrual care market in the Netherlands has critical growth opportunities due to development of digital infrastructure and high internet penetration rates. According to the World Bank, 94% of the Dutch population used internet services in 2024, thus facilitating faster adoption of e-commerce. Online retailing platforms, which are optimized with the help of targeted digital marketing and subscription-based sales models, allow menstruating women to purchase products more conveniently and unobtrusively, which expands the market reach.

According to the OECD Digital Economy Outlook, the Netherlands is ranked among the highest levels of digital adoption in Europe, and e-commerce is growing at a rate of over 10% annually due to consumer demand of convenience, affordability, and customized service delivery. Brand entities that combine omnichannel retailing and data-analytics capabilities are best placed to intensify consumer engagement and maintain market growth over the forecast period.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Netherlands Menstrual Care Market Segmentation Analysis

By Product Type

- Pantyliners

- Tampons

- Towels

- Intimate Wipes

- Menstrual Cups

- Period Underwear

Towels constitute the dominant segment within the produc, commanding approximately 40% of the Netherlands menstrual care market share. Towels maintain their position as the most extensively utilized product attributable to their affordability, comprehensive availability, and operational convenience. Their dominance is further reinforced by robust consumer trust in established brand entities such as Always, alongside private label alternatives delivering reliable quality at reduced price points. Slim/thin and ultra-thin towel variant configurations have experienced increasing popularity driven by their comfort attributes, discreteness characteristics, and superior absorbency performance, aligning with contemporary end-user priorities emphasizing comfort and hygiene optimization.

Despite gradual adoption trajectories for reusable products including menstrual cups and period underwear, disposable towels continue to appeal to younger and economically active female demographics who prioritize convenience and mobile reliability. Manufacturers are additionally introducing eco-friendly towel options formulated from sustainable materials and incorporating recyclable packaging solutions, facilitating sustained strong market positioning while accommodating environmentally conscious preference patterns.

By Sales Channel

- Retail Offline

- Retail Online

Retail offline channels maintain dominant positioning within the sales channel segmentation, accounting for approximately 80% of the Netherlands menstrual care market. Health and beauty store formats, supermarket operations, and drugstore establishments dominate this channel attributable to their substantial physical presence and comprehensive product assortment breadth. end user continue to demonstrate reliance on these retail outlets for convenience, frequent promotional activities, and the capability to conduct physical product comparison evaluations. This dynamic has established retail offline as the preferred purchasing modality, particularly among cost-conscious shopper segments seeking private label or discounted branded product offerings.

Discount retail formats and drugstore chains such as Kruidvat and Etos further enhance offline sales performance through competitive pricing strategies and accessible geographic locations. These retail outlets have successfully attracted budget-sensitive end-user demographics amid ongoing inflationary pressure conditions. While e-commerce channels are experiencing rapid expansion, retail offline distribution continues to function as the primary distribution infrastructure within the Netherlands, supported by strong in-store visibility, established brand presence, and evolving product assortments that integrate affordability with premium and sustainable menstrual care alternatives.

List of Companies Covered in Netherlands Menstrual Care Market

The companies listed below are highly influential in the Netherlands menstrual care market, with a significant market share and a strong impact on industry developments.

- Kimberly-Clark BV

- Etos BV

- FIP Organic BV

- Procter & Gamble Nederland BV

- Essity Nederland BV

- Johnson & Johnson Consumer BV

- AS Watson (Health & Beauty Benelux)

- Albert Heijn BV

- Jumbo Supermarkten BV

- CIV Superunie BA

Competitive Landscape

The Netherlands Menstrual Care Market in 2024 was led by Procter & Gamble Nederland BV, supported by the strong presence of its Always and Tampax brands. Always benefited from high brand trust, consistent innovation, and strong appeal among older demographics seeking reliability and quality. Despite inflationary pressures, Procter & Gamble maintained leadership through effective pricing and promotional strategies. However, private label ranges from retailers such as Kruidvat and Albert Heijn gained momentum, appealing to price-sensitive consumers with comparable quality at lower prices. This trend reflected growing confidence in private label efficacy across towels and pantyliners. Additionally, e-commerce players like bol.com and deonlinedrogist.nl reshaped competition by leveraging discounts, convenience, and discreet delivery services to capture a larger online consumer base.

Frequently Asked Questions

Related Report

1. Market Segmentation

1.1. Research Scope

1.2. Research Methodology

1.3. Definitions and Assumptions

2. Executive Summary

3. Netherlands Menstrual Care Market Policies, Regulations, and Standards

4. Netherlands Menstrual Care Market Dynamics

4.1. Growth Factors

4.2. Challenges

4.3. Trends

4.4. Opportunities

5. Netherlands Menstrual Care Market Statistics, 2022-2032F

5.1. Market Size & Growth Outlook

5.1.1.By Revenues in USD Million

5.2. Market Segmentation & Growth Outlook

5.2.1.By Product Type

5.2.1.1. Pantyliners- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2. Tampons- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2.1. Applicator Tampons- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2.2. Digital Tampons- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3. Towels- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3.1. Standard Towels- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3.1.1. Standard Towels with Wings- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3.1.2. Standard Towels Without Wings- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3.2. Slim/Thin/Ultra-Thin Towels- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3.2.1. Slim/Thin/Ultra-Thin Towels with Wings- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3.2.2. Slim/Thin/Ultra-Thin Towels Without Wings- Market Insights and Forecast 2022-2032, USD Million

5.2.1.4. Intimate Wipes- Market Insights and Forecast 2022-2032, USD Million

5.2.1.5. Menstrual Cups- Market Insights and Forecast 2022-2032, USD Million

5.2.1.6. Period Underwear- Market Insights and Forecast 2022-2032, USD Million

5.2.2.By Nature

5.2.2.1. Disposable- Market Insights and Forecast 2022-2032, USD Million

5.2.2.2. Reusable- Market Insights and Forecast 2022-2032, USD Million

5.2.3.By Age Group

5.2.3.1. Up to 18 Years- Market Insights and Forecast 2022-2032, USD Million

5.2.3.2. 19-30 Years- Market Insights and Forecast 2022-2032, USD Million

5.2.3.3. 31-40 Years- Market Insights and Forecast 2022-2032, USD Million

5.2.3.4. 40 Years and Above- Market Insights and Forecast 2022-2032, USD Million

5.2.4.By Sales Channel

5.2.4.1. Retail Offline- Market Insights and Forecast 2022-2032, USD Million

5.2.4.2. Retail Online- Market Insights and Forecast 2022-2032, USD Million

5.2.5.By Competitors

5.2.5.1. Competition Characteristics

5.2.5.2. Market Share & Analysis

6. Netherlands Pantyliners Menstrual Care Market Statistics, 2022-2032

6.1. Market Size & Growth Outlook

6.1.1.By Revenues in USD Million

6.2. Market Segmentation & Growth Outlook

6.2.1.By Nature- Market Insights and Forecast 2022-2032, USD Million

6.2.2.By Age Group- Market Insights and Forecast 2022-2032, USD Million

6.2.3.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

7. Netherlands Tampons Menstrual Care Market Statistics, 2022-2032

7.1. Market Size & Growth Outlook

7.1.1.By Revenues in USD Million

7.2. Market Segmentation & Growth Outlook

7.2.1.By Product Type- Market Insights and Forecast 2022-2032, USD Million

7.2.2.By Nature- Market Insights and Forecast 2022-2032, USD Million

7.2.3.By Age Group- Market Insights and Forecast 2022-2032, USD Million

7.2.4.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

8. Netherlands Towels Menstrual Care Market Statistics, 2022-2032

8.1. Market Size & Growth Outlook

8.1.1.By Revenues in USD Million

8.2. Market Segmentation & Growth Outlook

8.2.1.By Product Type- Market Insights and Forecast 2022-2032, USD Million

8.2.2.By Nature- Market Insights and Forecast 2022-2032, USD Million

8.2.3.By Age Group- Market Insights and Forecast 2022-2032, USD Million

8.2.4.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

9. Netherlands Intimate Wipes Market Statistics, 2022-2032

9.1. Market Size & Growth Outlook

9.1.1.By Revenues in USD Million

9.2. Market Segmentation & Growth Outlook

9.2.1.By Nature- Market Insights and Forecast 2022-2032, USD Million

9.2.2.By Age Group- Market Insights and Forecast 2022-2032, USD Million

9.2.3.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

10. Netherlands Menstrual Cups Menstrual Care Market Statistics, 2022-2032

10.1. Market Size & Growth Outlook

10.1.1. By Revenues in USD Million

10.2. Market Segmentation & Growth Outlook

10.2.1. By Nature- Market Insights and Forecast 2022-2032, USD Million

10.2.2. By Age Group- Market Insights and Forecast 2022-2032, USD Million

10.2.3. By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

11. Netherlands Period Underwear Menstrual Care Market Statistics, 2022-2032

11.1. Market Size & Growth Outlook

11.1.1. By Revenues in USD Million

11.2. Market Segmentation & Growth Outlook

11.2.1. By Nature- Market Insights and Forecast 2022-2032, USD Million

11.2.2. By Age Group- Market Insights and Forecast 2022-2032, USD Million

11.2.3. By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

12. Competitive Outlook

12.1. Company Profiles

12.1.1. Procter & Gamble Nederland BV

12.1.1.1. Business Description

12.1.1.2. Product Portfolio

12.1.1.3. Collaborations & Alliances

12.1.1.4. Recent Developments

12.1.1.5. Financial Details

12.1.1.6. Others

12.1.2. Essity Nederland BV

12.1.2.1. Business Description

12.1.2.2. Product Portfolio

12.1.2.3. Collaborations & Alliances

12.1.2.4. Recent Developments

12.1.2.5. Financial Details

12.1.2.6. Others

12.1.3. Johnson & Johnson Consumer BV

12.1.3.1. Business Description

12.1.3.2. Product Portfolio

12.1.3.3. Collaborations & Alliances

12.1.3.4. Recent Developments

12.1.3.5. Financial Details

12.1.3.6. Others

12.1.4. AS Watson (Health & Beauty Benelux)

12.1.4.1. Business Description

12.1.4.2. Product Portfolio

12.1.4.3. Collaborations & Alliances

12.1.4.4. Recent Developments

12.1.4.5. Financial Details

12.1.4.6. Others

12.1.5. Albert Heijn BV

12.1.5.1. Business Description

12.1.5.2. Product Portfolio

12.1.5.3. Collaborations & Alliances

12.1.5.4. Recent Developments

12.1.5.5. Financial Details

12.1.5.6. Others

12.1.6. Kimberly-Clark BV

12.1.6.1. Business Description

12.1.6.2. Product Portfolio

12.1.6.3. Collaborations & Alliances

12.1.6.4. Recent Developments

12.1.6.5. Financial Details

12.1.6.6. Others

12.1.7. Etos BV

12.1.7.1. Business Description

12.1.7.2. Product Portfolio

12.1.7.3. Collaborations & Alliances

12.1.7.4. Recent Developments

12.1.7.5. Financial Details

12.1.7.6. Others

12.1.8. FIP Organic BV

12.1.8.1. Business Description

12.1.8.2. Product Portfolio

12.1.8.3. Collaborations & Alliances

12.1.8.4. Recent Developments

12.1.8.5. Financial Details

12.1.8.6. Others

12.1.9. Jumbo Supermarkten BV

12.1.9.1. Business Description

12.1.9.2. Product Portfolio

12.1.9.3. Collaborations & Alliances

12.1.9.4. Recent Developments

12.1.9.5. Financial Details

12.1.9.6. Others

12.1.10. CIV Superunie BA

12.1.10.1.Business Description

12.1.10.2.Product Portfolio

12.1.10.3.Collaborations & Alliances

12.1.10.4.Recent Developments

12.1.10.5.Financial Details

12.1.10.6.Others

13. Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Product Type |

|

| By Nature |

|

| By Age Group |

|

| By Sales Channel |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.