Malaysia Bags and Luggage Market Report: Trends, Growth and Forecast (2026-2032)

By Category (Bags (Cross Body Bags, Bags and Backpacks, Business Bags, Duffle Bags, Clutches, Others), Luggage (Soft Luggage, Hard Luggage, Wheeled Luggage, Non-Wheeled Luggage)), By Sales Channel (Retail Offline, Retail Online), By Material Type (Soft Case (Nylon, Polyester, Ballistic Nylon), Hard Case (Polycarbonate, ABS (Acrylonitrile Butadiene Styrene), Polypropylene)), By Price Category (Luxury, Mass/Economy, Premium), By Application (Travel, Business) ... Read more

|

Major Players

|

Malaysia Bags and Luggage Market Statistics and Insights, 2026

- Market Size Statistics

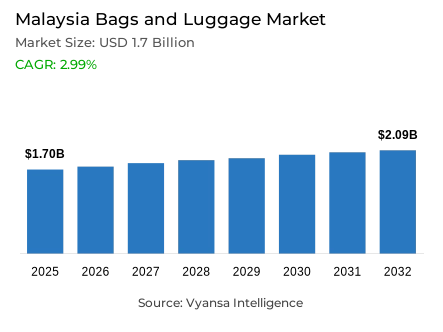

- Bags and luggage in Malaysia is estimated at USD 1.7 billion in 2025.

- The market size is expected to grow to USD 2.09 billion by 2032.

- Market to register a cagr of around 2.99% during 2026-32.

- Category Shares

- Bags grabbed market share of 80%.

- Competition

- More than 20 companies are actively engaged in producing bags and luggage in Malaysia.

- Top 5 companies acquired around 25% of the market share.

- Prada Retail (M) Sdn Bhd; Hermes Retail (M) Sdn Bhd; Chanel (Kuala Lumpur) Sdn Bhd; Louis Vuitton Malaysia Sdn Bhd; Coach Malaysia Sdn Bhd etc., are few of the top companies.

- Sales Channel

- Retail offline grabbed 90% of the market.

Malaysia Bags and Luggage Market Outlook

The Malaysia bags and luggage market is estimated at USD 1.7 billion in 2025 and is expected to grow to USD 2.09 billion by 2032, registering a CAGR of around 2.99% during 2026–32. Market expansion will be supported by lifestyle-driven demand, recovery in travel activity, and the continued evolution of retail formats across major urban centres.

Younger end user are playing a key role in shaping demand, particularly through rising interest in casual bags such as tote and canvas designs. Practical yet stylish formats, often enhanced through personalisation and collaborations, have gained strong traction. Denim and canvas tote bags have re-emerged as everyday accessories, appealing to cost-conscious shoppers who still prioritise aesthetics. At the same time, slowed economic growth has encouraged a shift towards non-luxury and entry-level luxury brands, with frequent promotions helping brands sustain volumes.

The development of new high-end shopping malls and refurbished retail spaces is further strengthening the category. Luxury brands are expanding their physical presence through flagship stores and focused launches, supported by recovering inbound tourism and renewed domestic travel. Luggage demand, in particular, is benefiting from increased travel activity and new product introductions targeted at frequent travellers.

Over the forecast period, growth will also be supported by personalisation, sustainability initiatives, and immersive shopping experiences. Brands are increasingly investing in customisation services, eco-friendly materials, and experiential pop-ups to engage younger shoppers. While retail e-commerce is expected to gain share, physical retail will remain central to category performance, underpinning steady growth in Malaysia’s bags and luggage market

Malaysia Bags and Luggage Market Growth Driver

Youth-led lifestyle shifts and retail recovery supporting demand

Youth-driven lifestyle changes are a core structural driver of demand in the Malaysia bags and luggage market. Younger end users increasingly prefer casual, versatile, and multi-purpose bags that can transition across work, leisure, and short-distance travel, reflecting more fluid daily routines. This behaviour aligns with the broader recovery in mobility and social activity following the pandemic, reinforcing regular replacement and upgrade cycles for everyday carry products.

This lifestyle shift is reinforced by the recovery of tourism and retail footfall. According to Tourism Malaysia, international tourist arrivals exceeded 20 million in 2023, restoring activity levels across urban retail hubs. In parallel, the expansion and refurbishment of shopping malls in Kuala Lumpur and other major cities have improved brand visibility and discovery-based purchasing, particularly among younger shoppers who engage strongly with lifestyle-oriented retail environments.

Malaysia Bags and Luggage Market Challenge

Cost of living pressure intensifying price sensitivity

Rising price sensitivity remains a structural constraint on value growth in Malaysia’s bags and luggage market. Persistent cost-of-living pressures have shifted purchasing behaviour toward non-luxury and entry-level luxury products, with affordability and functional value prioritised over premium positioning. As bags and luggage remain discretionary purchases, replacement cycles are increasingly influenced by promotional timing rather than spontaneous demand.

Official inflation data underline this constraint. Department of Statistics Malaysia reports that consumer inflation remained elevated through 2023, continuing to pressure household budgets. This environment intensifies competition among brands, increases reliance on discounting, and compresses marginsparticularly for mid- and high-end playerswhile limiting volume expansion beyond value-oriented segments.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Malaysia Bags and Luggage Market Trend

Casualisation and experience-led retail reshaping the market

Casualisation is a defining trend shaping demand patterns in Malaysia’s bags and luggage market. Younger, digitally connected consumers increasingly favour everyday styles such as totes, canvas bags, and practical carry solutions that align with informal dress codes and lifestyle-led consumption. Product narratives centred on functionality, sustainability, and brand values are becoming more influential than traditional status signalling.

Retail strategies are evolving in parallel. Brands are increasingly adopting pop-up stores, capsule launches, and omnichannel engagement to create experiential touchpoints rather than purely transactional sales. These approaches support stronger brand recall and emotional engagement in a crowded market, particularly among younger end users who value immersive physical-digital brand interaction as part of the purchasing journey.

Malaysia Bags and Luggage Market Opportunity

Immersive retail and sustainability unlocking growth avenues

The strongest growth opportunity lies in immersive retail execution combined with sustainable product differentiation. Customisation services, responsible material sourcing, and limited-edition collaborations enable brands to move beyond price-based competition and establish clearer value propositions aligned with consumer expectations of individuality and environmental responsibility.

This opportunity is reinforced by Malaysia’s positioning as a regional shopping and tourism destination. Continued investment in modern retail infrastructure and the rebound in inbound tourism support experiential formats such as flagship stores, pop-ups, and digitally integrated physical retail. Brands that effectively combine sustainability credentials with immersive retail execution are better positioned to attract both domestic youth consumers and international shoppers over the forecast period.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Malaysia Bags and Luggage Market Segmentation Analysis

By Category

- Bags

- Cross Body Bags

- Bags and Backpacks

- Business Bags

- Duffle Bags

- Clutches

- Others

- Luggage

- Soft Luggage

- Hard Luggage

- Wheeled Luggage

- Non-Wheeled Luggage

The segment with highest market share under category is bag, accounting for approximately 80% of total market value. This dominance reflects their daily relevance across work, education, leisure, and social use. Entry-level fashion handbags, tote bags, and casual designs perform strongly, supported by affordability, versatility, and frequent style refresh cycles.

Brand collaborations, customisation, and promotional strategies have helped sustain interest despite economic constraints. Both non-luxury and entry-level luxury brands benefit from wide availability in malls and standalone stores. Over the forecast period, bags are expected to retain their leading position, driven by lifestyle-led demand and ongoing design innovation across income groups.

By Sales Channel

- Retail Offline

- Retail Online

Retail offlinedominates the sales channel structure, accounting for approximately 90% of total market sales. Physical stores remain the preferred purchasing channel for bags and luggage, particularly for fashion-oriented and higher-quality products where fit, material, and brand interaction influence decision-making.

The expansion of premium malls, specialist retailers, flagship stores, and pop-up formats continues to reinforce offline leadership. Department stores also play a key role by offering broad assortments across price tiers. While online channels are gradually expanding, retail offlineis expected to remain the primary channel through 2032, supported by experiential retail strategies and sustained tourism-driven footfall.

List of Companies Covered in Malaysia Bags and Luggage Market

The companies listed below are highly influential in the Malaysia bags and luggage market, with a significant market share and a strong impact on industry developments.

- Prada Retail (M) Sdn Bhd

- Hermes Retail (M) Sdn Bhd

- Chanel (Kuala Lumpur) Sdn Bhd

- Louis Vuitton Malaysia Sdn Bhd

- Coach Malaysia Sdn Bhd

- Michael Kors (M) Sdn Bhd

- Bonia Corp Bhd

- Gucci Malaysia Sdn Bhd

- Delsey SA

- VF Corp

Competitive Landscape

Malaysia bags and luggage market is highly fragmented, with competition shaped by fast-moving local brands, established regional players, and global luxury houses. Non-luxury and entry-level luxury brands such as Charles & Keith, Vincci, and Christy Ng are particularly influential, leveraging frequent promotions, casual designs, and collaborations to attract younger, price-sensitive consumers. Tote and casual bags have become key battlegrounds, with personalisation and licensed collaborations helping brands stand out. At the premium end, luxury players including Louis Vuitton, Dior, Coach, and Bottega Veneta are strengthening their presence through flagship store openings in new high-end malls and travel-linked launches under brands such as Rimowa. Meanwhile, specialist retailers and immersive pop-ups are intensifying competition by combining experiential retail with omnichannel strategies, reinforcing brand engagement across income segments.

Frequently Asked Questions

Related Report

1. Market Segmentation

1.1. Research Scope

1.2. Research Methodology

1.3. Definitions and Assumptions

2. Executive Summary

3. Malaysia Bags and Luggage Market Policies, Regulations, and Standards

4. Malaysia Bags and Luggage Market Dynamics

4.1. Growth Factors

4.2. Challenges

4.3. Trends

4.4. Opportunities

5. Malaysia Bags and Luggage Market Statistics, 2022-2032F

5.1. Market Size & Growth Outlook

5.1.1.By Revenues in USD Million

5.1.2.By Units Sold in Thousand Units

5.2. Market Segmentation & Growth Outlook

5.2.1.By Category

5.2.1.1. Bags- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.1. Cross Body Bags- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.2. Bags and Backpacks- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.3. Business Bags- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.4. Duffle Bags- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.5. Clutches- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.6. Others- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2. Luggage- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2.1. Soft Luggage- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2.2. Hard Luggage- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2.3. Wheeled Luggage- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2.4. Non-Wheeled Luggage- Market Insights and Forecast 2022-2032, USD Million

5.2.2.By Sales Channel

5.2.2.1. Retail Offline- Market Insights and Forecast 2022-2032, USD Million

5.2.2.2. Retail Online- Market Insights and Forecast 2022-2032, USD Million

5.2.3.By Material Type

5.2.3.1. Soft Case- Market Insights and Forecast 2022-2032, USD Million

5.2.3.1.1. Nylon- Market Insights and Forecast 2022-2032, USD Million

5.2.3.1.2. Polyester- Market Insights and Forecast 2022-2032, USD Million

5.2.3.1.3. Ballistic Nylon- Market Insights and Forecast 2022-2032, USD Million

5.2.3.2. Hard Case- Market Insights and Forecast 2022-2032, USD Million

5.2.3.2.1. Polycarbonate- Market Insights and Forecast 2022-2032, USD Million

5.2.3.2.2. ABS (Acrylonitrile Butadiene Styrene)- Market Insights and Forecast 2022-2032, USD Million

5.2.3.2.3. Polypropylene- Market Insights and Forecast 2022-2032, USD Million

5.2.4.By Price Category

5.2.4.1. Luxury- Market Insights and Forecast 2022-2032, USD Million

5.2.4.2. Mass/Economy- Market Insights and Forecast 2022-2032, USD Million

5.2.4.3. Premium- Market Insights and Forecast 2022-2032, USD Million

5.2.5.By Application

5.2.5.1. Travel- Market Insights and Forecast 2022-2032, USD Million

5.2.5.2. Business- Market Insights and Forecast 2022-2032, USD Million

5.2.6.By Competitors

5.2.6.1. Competition Characteristics

5.2.6.2. Market Share & Analysis

6. Malaysia Bags Market Statistics, 2022-2032

6.1. Market Size & Growth Outlook

6.1.1.By Revenues in USD Million

6.1.2.By Units Sold in Thousand Units

6.2. Market Segmentation & Growth Outlook

6.2.1.By Category- Market Insights and Forecast 2022-2032, USD Million

6.2.2.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

6.2.3.By Material Type- Market Insights and Forecast 2022-2032, USD Million

6.2.4.By Price Category- Market Insights and Forecast 2022-2032, USD Million

6.2.5.By Application- Market Insights and Forecast 2022-2032, USD Million

7. Malaysia Luggage Market Statistics, 2022-2032

7.1. Market Size & Growth Outlook

7.1.1.By Revenues in USD Million

7.1.2.By Units Sold in Thousand Units

7.2. Market Segmentation & Growth Outlook

7.2.1.By Category- Market Insights and Forecast 2022-2032, USD Million

7.2.2.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

7.2.3.By Material Type- Market Insights and Forecast 2022-2032, USD Million

7.2.4.By Price Category- Market Insights and Forecast 2022-2032, USD Million

7.2.5.By Application- Market Insights and Forecast 2022-2032, USD Million

8. Competitive Outlook

8.1. Company Profiles

8.1.1.Louis Vuitton Malaysia Sdn Bhd

8.1.1.1. Business Description

8.1.1.2. Product Portfolio

8.1.1.3. Collaborations & Alliances

8.1.1.4. Recent Developments

8.1.1.5. Financial Details

8.1.1.6. Others

8.1.2.Coach Malaysia Sdn Bhd

8.1.2.1. Business Description

8.1.2.2. Product Portfolio

8.1.2.3. Collaborations & Alliances

8.1.2.4. Recent Developments

8.1.2.5. Financial Details

8.1.2.6. Others

8.1.3.Michael Kors (M) Sdn Bhd

8.1.3.1. Business Description

8.1.3.2. Product Portfolio

8.1.3.3. Collaborations & Alliances

8.1.3.4. Recent Developments

8.1.3.5. Financial Details

8.1.3.6. Others

8.1.4.Bonia Corp Bhd

8.1.4.1. Business Description

8.1.4.2. Product Portfolio

8.1.4.3. Collaborations & Alliances

8.1.4.4. Recent Developments

8.1.4.5. Financial Details

8.1.4.6. Others

8.1.5.Gucci Malaysia Sdn Bhd

8.1.5.1. Business Description

8.1.5.2. Product Portfolio

8.1.5.3. Collaborations & Alliances

8.1.5.4. Recent Developments

8.1.5.5. Financial Details

8.1.5.6. Others

8.1.6.Prada Retail (M) Sdn Bhd

8.1.6.1. Business Description

8.1.6.2. Product Portfolio

8.1.6.3. Collaborations & Alliances

8.1.6.4. Recent Developments

8.1.6.5. Financial Details

8.1.6.6. Others

8.1.7.Hermes Retail (M) Sdn Bhd

8.1.7.1. Business Description

8.1.7.2. Product Portfolio

8.1.7.3. Collaborations & Alliances

8.1.7.4. Recent Developments

8.1.7.5. Financial Details

8.1.7.6. Others

8.1.8.Chanel (Kuala Lumpur) Sdn Bhd

8.1.8.1. Business Description

8.1.8.2. Product Portfolio

8.1.8.3. Collaborations & Alliances

8.1.8.4. Recent Developments

8.1.8.5. Financial Details

8.1.8.6. Others

8.1.9.Delsey SA

8.1.9.1. Business Description

8.1.9.2. Product Portfolio

8.1.9.3. Collaborations & Alliances

8.1.9.4. Recent Developments

8.1.9.5. Financial Details

8.1.9.6. Others

8.1.10. VF Corp

8.1.10.1. Business Description

8.1.10.2. Product Portfolio

8.1.10.3. Collaborations & Alliances

8.1.10.4. Recent Developments

8.1.10.5. Financial Details

8.1.10.6. Others

9. Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Category |

|

| By Sales Channel |

|

| By Material Type |

|

| By Price Category |

|

| By Application |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.