Japan Juice Market Report: Trends, Growth and Forecast (2026-2032)

By Category (100% Juice (Not from Concentrate, Reconstituted), Juice Drinks (up to 24% Juice), Nectars (High Concentration (40% to 50% fruit content), Medium Concentration (30% to 39% fruit content), Low Concentration (25% to 29% fruit content)), Vegetable Juice, Fruit and Vegetable Blends), By Nature (Conventional, Organic), By Packaging Material (Plastic, Glass, Metal, Others), By Packaging Type (PET Bottles, Aseptic Packages (Cartons), Glass Bottles, Metal Cans, Disposable Cups & Pouches), By Sales Channel (Off-Trade (Hypermarkets/ Supermarkets, Retail Outlets, Convenience Stores, Online Platforms), On-Trade) ... Read more

|

Major Players

|

Japan Juice Market Statistics and Insights, 2026

- Market Size Statistics

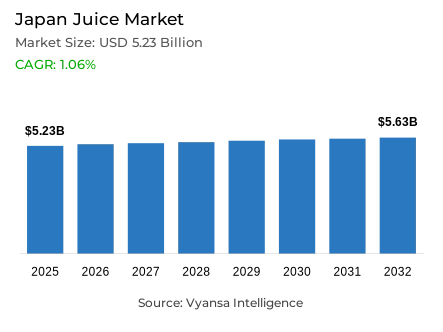

- Juice market size in Japan was estimated at USD 5.23 billion in 2025.

- The market size is expected to grow to USD 5.63 billion by 2032.

- Market to register a CAGR of around 1.06% during 2026-32.

- Category Shares

- 100% juice grabbed market share of 65%.

- Competition

- More than 15 companies are actively engaged in producing juice in Japan.

- Top 5 companies acquired around 55% of the market share.

- Megmilk Snow Brand Co Ltd, Asahi Soft Drinks Co Ltd, Ehime Inryou Co Ltd, Kagome Co Ltd, Coca-Cola (Japan) Co Ltd etc., are few of the top companies.

- Sales Channel

- Off-trade grabbed 85% of the market.

Japan Juice Market Outlook

The Japan juice market is undergoing a structural transformation defined by demographic shifts and a departure from deflationary pricing strategies. Estimated at $5.23 billion in 2025, the market is expected to grow marginally to $5.63 billion by 2032, registering a CAGR of around 1.06% during the 2026–32 period. Historically hesitant to raise prices, major players like Coca-Cola and Kagome are now implementing price hikes to offset rising costs for raw materials and energy. While this has pressured volume sales, value is being sustained through a pivot toward health-functional products, with 100% Juice holding a dominant 65% market share.

Demographics are reshaping product development. With birth rates at record lows, manufacturers are shifting their focus from children to adults and seniors. This has led to the introduction of "medium" pack sizes (e.g., 700 ml) for smaller households and functional claims targeting blood pressure and cholesterol. Trends are also cyclical; while tomato juice remains a staple for health-conscious shoppers, ingredients like acai and high beta-carotene carrots are seeing renewed interest as "drinkable salads" for busy urbanites.

Climate change is further influencing innovation, with juice now marketed as a tool for heatstroke prevention during Japan’s intensifying summers.

New "ice slurry" beverages and frozen smoothies are being positioned for daily hydration and workplace safety. Sales channel remains centered on home consumption, with Off-Trade channels grabbing 85% of the market. Supermarkets continue to drive engagement through in-store sampling events, while e-commerce is rapidly gaining ground due to its convenience for bulk purchasing, contrasting with the decline of vending machines due to higher unit prices.

Japan Juice Market Growth DriverRapid Population Ageing Sustaining Demand for Convenient and Functional Nutritional Beverages

The aging population in Japan still maintains a strong demand in the juice products that offer convenient daily nutrition especially those that include vegetables and functional ingredients that are in line with the health-conscious routines. According to the estimates of the Statistics Bureau of Japan, 36.19 million people aged 65 and above, 29.4% of the population, are aged 65 and above as of 15 September 2025. This age group supports the focus of health maintenance in a large number of shoppers. As a result, there arises a long-term demand of nutritionally fortified drinks that can help in preventing health behaviours and maintaining wellness among older end user groups.

The elderly end users are still active in the economy, and they buy packaged and shelf-stable beverages on a regular basis. According to the 2024 report by the Statistics Bureau, there were 9.3 million employed people aged 65 and above, which translates to an employment rate of 25.7% among this age group. A large number of end users juggle their work and wellness needs, and they like fast ways to consume fruits and vegetables. This behaviour promotes repeat buying of smaller packs and convenient to carry multi-packs, which is usually done on a weekly basis when shopping at the supermarket. The combination of demographic size, economic activity, and health awareness creates favourable structural conditions of functional juice categories targeting active older end users in search of nutritional convenience.

Japan Juice Market ChallengeFood-Led Inflation and Price Revisions Constraining Everyday Juice Affordability

Constant inflation makes juice susceptible to budget cuts and maintains volume pressure in cases where manufacturers make price adjustments. According to the Statistics Bureau of Japan, the end user price index of all items increased by 3.2% in 2025 compared to the year before, and the food index increased by 6.8%, which significantly strained the purchasing power and heightened the sensitivity to non-essential beverages. This inflation differentiation creates severe affordability stress on discretionary beverage products, such as packaged juice.

When food prices increase faster than the general prices, end users focus on essential items and reduce non-essential ones, including packaged drinks. This is a challenge to juice that competes with water, tea, and cheaper alternatives that quench thirst at lower prices. The brands react by emphasizing health and wellness assertions to support pricing; however, the affordability barrier is an inherent limitation. The increased shelf prices discourage impulse buying and promote fewer and less frequent visits to the store. The structural headwinds that are caused by economic pressures restrict volume growth, despite the existence of robust demographic forces and health positioning benefits in the Japanese mature beverage market.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Japan Juice Market TrendDeclining Birth Rates Redirecting Category Focus Toward Adult-Oriented Functional Formats

The decreasing birth rates in Japan essentially change the demographics of the target end users, forcing the brands to pay less attention to children and more to adults who need convenient nutrition. The Ministry of Health, Labour and Welfare records 686,173 births in 2024, down 41,115 on the year before, and a total fertility rate of 1.15, record lows, signifying significantly smaller pipelines of young end users. This population change requires a strategic repositioning of the traditional child-oriented juice marketing to the adult wellness segments.

As household formations have reduced numbers of children, manufacturers focus on benefits that are more adult-oriented, including vegetable intake, beauty, and cardiovascular health, and change the pack sizes to fit smaller household habits. Single-serving and mid-size cartons are more convenient than large family packs, and marketing emphasizes obvious functional indicators like tomato-based lycopene or carrots rich in beta-carotene. This favors flavor and ingredient innovation as firms seek health-oriented product ideas. The shift in the demographic of child to adult consumption patterns is the root cause of fundamental category development, necessitating reformulated products, downsizing packaging, and repositioned marketing efforts that respond to the functional nutrition concerns of mature end users.

Japan Juice Market OpportunityEscalating Heatstroke Risk and Workplace Safety Mandates Unlocking Functional Hydration Demand

The increase in heat risk is a significant opportunity to juice, smoothies, and plant-based blends that are placed in the hydration and mineral replacement category in the face of increasingly hot summers. According to the Fire and Disaster Management Agency of Japan, 100,510 individuals were taken to ambulance due to heatstroke between May and September 2025, the most significant number since the survey began, proving that there is a significant and noticeable demand of practical hydration solutions. This is a health issue in the community that presents an urgent need of functional drinks that can be used to counter the health risks associated with heat.

This opportunity is enhanced by workplace safety regulations that make prevention a daily employer responsibility. According to the Ministry of Health, Labour and Welfare of Japan, the amended Industrial Safety and Health Ordinance, which will be in effect 1 June 2025, will make employers implement procedures that will help to recognize the risk of heatstroke and take timely action. The FDMA report identifies 10,559 heatstroke transports in the workplace, which can be used to justify workplace contracts on chilled juice and frozen smoothie packs. Low-sugar recipes and cooling-pack formats are electrolyte-based and address summer hydration needs. This regulatory-induced workplace need, coupled with end user heat-safety consciousness, provides a long-term seasonal chance of functionally positioned hydration drinks.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Japan Juice Market Segmentation Analysis

By Category

- 100% Juice

- Not from Concentrate

- Reconstituted

- Juice Drinks (up to 24% Juice)

- Nectars

- High Concentration (40% to 50% fruit content)

- Medium Concentration (30% to 39% fruit content)

- Low Concentration (25% to 29% fruit content)

- Vegetable Juice

- Fruit and Vegetable Blends

The segment has the highest share around the category in the Japan juice market, where 100% Juice grabbed a market share of 65%. This dominance is largely driven by the specific health demands of japan's aging population. Manufacturers are successfully marketing these products not just as refreshments, but as functional health tools. For instance, tomato juice has seen sustained success due to claims regarding lycopene’s ability to lower blood pressure and manage cholesterol, resonating strongly with end users over 50.

To combat end user "fickleness," companies are innovating within this segment to create the next "hit" ingredient. Strategies like Kagome’s "carrot hero" campaign highlight the nutritional value of 100% vegetable blends, while products mixing tomato with fruits like peach and lemon aim to make vegetable intake more palatable. By positioning these juices as convenient, nutrient-dense solutions—such as "drinkable salads" the 100% juice segment continues to capture the majority of value despite broader inflationary pressures.

By Sales Channel

- Off-Trade

- Hypermarkets/ Supermarkets

- Retail Outlets

- Convenience Stores

- Online Platforms

- On-Trade

The segment has the highest share around the Sales Channel is Off-Trade, which grabbed 85% of the market. This channel is anchored by supermarkets, which remain the primary touchpoint for end users despite a dip in volume caused by inflation. Brands like Kagome actively utilize this space for "experience-based" marketing, such as sampling events featuring fresh, premium tomato juice, to justify price points and maintain end user loyalty in a budget-conscious environment.

While supermarkets lead, the dynamics within off-trade are shifting. E-commerce is the most dynamic sub-channel, favored by end users for the convenience of home delivery and the ability to buy in bulk. Conversely, vending machines—a traditional staple of Japan retail—are losing favor as end users shy away from the higher unit prices charged in these locations. As households shrink and purchasing power tightens, the off-trade sector is adapting by offering diverse pack sizes that cater to both individual consumption and small families.

List of Companies Covered in Japan Juice Market

The companies listed below are highly influential in the Japan juice market, with a significant market share and a strong impact on industry developments.

- Megmilk Snow Brand Co Ltd

- Asahi Soft Drinks Co Ltd

- Ehime Inryou Co Ltd

- Kagome Co Ltd

- Coca-Cola (Japan) Co Ltd

- ITO EN Ltd

- Kirin Beverage Corp

- Suntory Beverage & Food Ltd

- Dydo Drinco Inc

- Morinaga Milk Industry Co

Competitive Landscape

Japan’s juice market in 2025 is led by Kagome, which dominates through health focused tomato juice positioned around lycopene benefits, cholesterol support, and blood pressure management, targeting both ageing consumers and younger demographics via social media. Nippon Del Monte is the most dynamic challenger, expanding tomato based and blended functional juices that emphasise high lycopene and vitamin content while improving taste accessibility. Major beverage groups such as Coca Cola, Kirin with Tropicana, and Asahi compete broadly but face volume pressure from price hikes and intense retail competition. Indirect competition from functional waters, sports drinks, and smoothies is intensifying amid heatstroke prevention demand and hydration trends. Differentiation opportunities lie in functional ingredients, convenient pack resizing for smaller households, premium seasonal sourcing, and workplace hydration solutions.

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- Japan Juice Market Policies, Regulations, and Standards

- Japan Juice Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- Japan Juice Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold in Million Litres

- Market Segmentation & Growth Outlook

- By Category

- 100% Juice- Market Insights and Forecast 2022-2032, USD Million

- Not from Concentrate- Market Insights and Forecast 2022-2032, USD Million

- Reconstituted- Market Insights and Forecast 2022-2032, USD Million

- Juice Drinks (up to 24% Juice)- Market Insights and Forecast 2022-2032, USD Million

- Nectars- Market Insights and Forecast 2022-2032, USD Million

- High Concentration (40% to 50% fruit content)- Market Insights and Forecast 2022-2032, USD Million

- Medium Concentration (30% to 39% fruit content)- Market Insights and Forecast 2022-2032, USD Million

- Low Concentration (25% to 29% fruit content)- Market Insights and Forecast 2022-2032, USD Million

- Vegetable Juice- Market Insights and Forecast 2022-2032, USD Million

- Fruit and Vegetable Blends- Market Insights and Forecast 2022-2032, USD Million

- 100% Juice- Market Insights and Forecast 2022-2032, USD Million

- By Nature

- Conventional- Market Insights and Forecast 2022-2032, USD Million

- Organic- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Material

- Plastic- Market Insights and Forecast 2022-2032, USD Million

- Glass- Market Insights and Forecast 2022-2032, USD Million

- Metal- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Type

- PET Bottles- Market Insights and Forecast 2022-2032, USD Million

- Aseptic Packages (Cartons)- Market Insights and Forecast 2022-2032, USD Million

- Glass Bottles- Market Insights and Forecast 2022-2032, USD Million

- Metal Cans- Market Insights and Forecast 2022-2032, USD Million

- Disposable Cups & Pouches- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel

- Off-Trade- Market Insights and Forecast 2022-2032, USD Million

- Hypermarkets/ Supermarkets - Market Insights and Forecast 2022-2032, USD Million

- Retail Outlets - Market Insights and Forecast 2022-2032, USD Million

- Convenience Stores- Market Insights and Forecast 2022-2032, USD Million

- Online Platforms- Market Insights and Forecast 2022-2032, USD Million

- On-Trade- Market Insights and Forecast 2022-2032, USD Million

- Off-Trade- Market Insights and Forecast 2022-2032, USD Million

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Category

- Market Size & Growth Outlook

- Japan 100% Juice Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold in Million Litres

- Market Segmentation & Growth Outlook

- By Nature- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Japan Juice Drinks (up to 24% Juice) Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold in Million Litres

- Market Segmentation & Growth Outlook

- By Nature- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Japan Nectars Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold in Million Litres

- Market Segmentation & Growth Outlook

- By Nature- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Japan Vegetable Juice Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold in Million Litres

- Market Segmentation & Growth Outlook

- By Nature- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Japan Fruit and Vegetable Blends Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold in Million Litres

- Market Segmentation & Growth Outlook

- By Nature- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- Kagome Co Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Coca-Cola (Japan) Co Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- ITO EN Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Kirin Beverage Corp

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Suntory Beverage & Food Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Megmilk Snow Brand Co Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Asahi Soft Drinks Co Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Ehime Inryou Co Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Dydo Drinco Inc

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Morinaga Milk Industry Co Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Kagome Co Ltd

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Category |

|

| By Nature |

|

| By Packaging Material |

|

| By Packaging Type |

|

| By Sales Channel |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.