Japan Dermatologicals Market Report: Trends, Growth and Forecast (2026-2032)

By Category (Medicated Shampoos, Topical Antifungals, Vaginal Antifungals, Hair Loss Treatments, Nappy (Diaper) Rash Treatments, Antiparasitics/Lice (Head and Body) Treatments, Antipruritics, Cold Sore Treatments, Haemorrhoid Treatments, Paediatric Dermatologicals, Topical Allergy Remedies/Antihistamines, Topical Germicidals/Antiseptics), By Dispensing Status (Prescription-based Drugs, Over-the-counter Drugs), By Route of Administration (Topical Administration, Oral Administration, Parenteral Administration), By Drug Type (Branded, Generics), By Skin Condition (Acne, Dermatitis, Psoriasis, Skin Cancer, Rosacea, Alopecia, Fungal Infections, Others), By End User (Hospitals, Cosmetic Centers, Dermatology Clinics, Homecare, Others), By Sales Channel (Retail Offline, Retail Online) ... Read more

|

Major Players

|

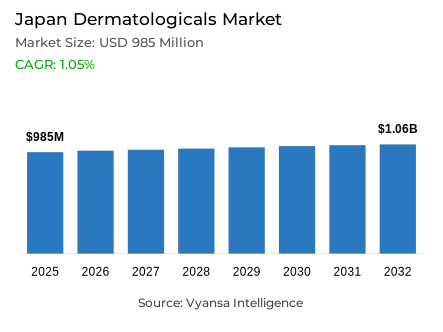

Japan Dermatologicals Market Statistics and Insights, 2026

- Market Size Statistics

- Dermatologicals in Japan is estimated at USD 985 million.

- The market size is expected to grow to USD 1.06 billion by 2032.

- Market to register a cagr of around 1.05% during 2026-32.

- Category Shares

- Antipruritics grabbed market share of 25%.

- Competition

- More than 20 companies are actively engaged in producing dermatologicals in Japan.

- Top 5 companies acquired around 35% of the market share.

- Kobayashi Pharmaceutical Co Ltd; Sato Pharmaceutical Co Ltd; Zeria Pharmaceutical Co Ltd; Taisho Pharmaceutical Co Ltd; Amato Pharmaceutical Products Ltd etc., are few of the top companies.

- Sales Channel

- Retail offline grabbed 85% of the market.

Japan Dermatologicals Market Outlook

The Japan Dermatologicals Market is expected to grow steadily through 2026–32, supported by rising unit prices and increasing demand for high-value formulations. In 2025, the market is valued at USD 985 million, with expectations to reach USD 1.06 billion by 2032 at a 1.05% CAGR. Premiumisation remains a key driver as enduser prioritize effective, trustworthy solutions, particularly in allergy and dermatitis care, for which steroid–antibacterial combinations are well established. Antipruritics, holding 25% share, continue to do well as users look for targeted relief. While 85% of sales still come from retail offline channels, e-commerce is growing for privacy-sensitive categories like hair regrowth and haemorrhoid care.

Digital is fast becoming the core of brand competitiveness. As enduser increasingly go online for product understanding and discreet purchasing, clear communication, ease of use, and educational content have become a given. Expanding its Borraginol line digitally to include stool-monitoring tools and preventive guidance, Amato Pharmaceutical epitomizes dermatological brands moving from pure treatment positioning to lifestyle-supportive care, through which it increases trust and ensures long-term engagement.

In the 2026–32 period, growth will stabilise, as Japan faces demographic pressures, including ageing and population decline. Competition from cosmetics and dermatology clinics will influence purchasing behavior. However, increasing interest in prevention routines—such as moisturising, acne care, low-irritant paediatric products, and femcare—will continue to support demand. These areas benefit from greater awareness, policy support, and expanding product ranges.

As the OTC landscape matures, brands will increasingly differentiate themselves through improved formulations, digital education, and personalized guidance. Success will depend on offering discreet online pathways, a stronger user experience, and credible information. As enduser increasingly demand reliability and convenience, companies that can integrate self-care tools and engage users constantly will be the best-positioned for growth within Japan's developing and increasingly value-conscious dermatologicals market.

Japan Dermatologicals Market Growth Driver

Premiumisation Supported by High Health Expenditure

The transition in the marketplace from being volume-driven to being value-driven is very strong right now. Endusers are now more interested in high value multifunctional products rather than going for the cheapest option available. There is also significant growth in the Allergy/Dermatitis segment for premium steroid/antibacterial combinations marketed toward both clinical effectiveness as well as providing safety for those with sensitive skin. Certain adjacent categories, specifically hair regrowth treatments, antifungal treatments, and the pediatric dermatological category have also begun moving toward more sophisticated products that are focused on comfort and without irritation. Rooting for a higher psuedo-science price point regardless of continuing to have flat unit volume totals.

The premiumisation trend in Japan reflects the fact that total health expenditure at around 10.6% of GDP exceeds the OECD average of 9.3%, as well as Japan's significant level of investment in both medical and quasi-medical products at a value of USD 5,790 per capita in terms of purchasing power parity. This macro-economy also provides endusers support for purchasing OTC products which may be marketed based on clinical efficacy, safety, and long term management of skin conditions, rather than solely for symptom relief.

Japan Dermatologicals Market Challenge

Population Decline Constraining Volume Growth

The decreasing population in Japan presents a significant structural challenge for the Japan dermatologicals market. A declining population will limit volume growth potential for the long-term, even if the per capita dermatological needs remain stable or increase. The demographic shift toward a smaller total population, decreased household sizes and reduced relevance of large family-format products will restrict unit sales from being based on population growth; therefore, brands must respond to a shrinking number of users, despite ongoing need, as a consequence of ageing, stress exposure, and chronic skin conditions.

The scope of this constraint can be confirmed from official demographic data. The total population of Japan on October 1st, 2024, was approximately 123.8 million, representing a continual decline of approximately 550,000 individuals -0.44% compared to the previous year and marking the 14th consecutive year of population decline. Given this context, future growth within the dermatologicals category will increasingly must come from strategies that take advantage of Premiumisation, improve Value Per enduser and expand use occasions that are either Preventive or Lifestyle-oriented since there will Structurally not be volume growth from Population Growth.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Japan Dermatologicals Market Trend

Constraints on Growth Shift Strategies Toward Structural Improvement

A key emerging trend in Japan’s dermatologicals landscape is the shift from short-term line expansion toward deeper structural enhancements in formulation design, user experience, and behaviour-support features, reflecting stabilising demand and increasingly pronounced demographic pressures. Companies are focusing more on scientific credibility, clearer claims, better textures and formats, and guidance that embeds products into daily routines, rather than chasing incremental volume through new variants alone.

This evolution is reinforced by Japan high level of digital readiness recent data indicate that around 88.2% of the population roughly 109 million people uses the internet, creating a strong base for information‑rich engagement and self‑education around skin health. As endusers increasingly research symptoms, compare safety claims, and scrutinise ingredient transparency online, brands are pushed to strengthen evidence, refine communication, and integrate digital tools such as trackers and educational content, reshaping value creation from more SKUs toward deeper structural quality and trust.

Japan Dermatologicals Market Opportunity

Evolving Online Strategy Through Expanded Convenience

A major opportunity emerges in building digital‑first dermatological strategies that provide discretion, personalised guidance, and frictionless access, especially in privacy‑sensitive areas such as hair loss, haemorrhoids, vaginal health, and antifungal treatments. By extending existing digital assets—apps, symptom checkers, self‑monitoring tools, reminders, and adaptive product suggestions—OTC brands can shift from episodic problem‑solving toward becoming embedded companions in everyday wellness behaviour.

Japan digital maturity strongly supports this direction surveys by the Ministry of Internal Affairs and Communications show that about 90.5% of households own a smartphone and more than four‑fifths of individuals use one, making mobile-based health interaction broadly accessible across age groups. High device and internet penetration provide fertile ground for expanding personalised digital journeys, integrating preventive education, and differentiating on convenience and privacy, positioning brands that excel in mobile‑centric personalisation to lead the next phase of dermatologicals growth.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Japan Dermatologicals Market Segmentation Analysis

By Category

- Medicated Shampoos

- Topical Antifungals

- Vaginal Antifungals

- Hair Loss Treatments

- Nappy (Diaper) Rash Treatments

- Antiparasitics/Lice (Head and Body) Treatments

- Antipruritics

- Cold Sore Treatments

- Haemorrhoid Treatments

- Paediatric Dermatologicals

- Topical Allergy Remedies/Antihistamines

- Topical Germicidals/Antiseptics

The segment with highest market share under Category is Antipruritics with share around 25% of the Japan dermatologicals market. This segment benefits from robust demand for products delivering rapid itch relief while providing antibacterial and skin-repair benefits—attributes highly valued by end users. Premium formulations combining steroids with antibacterial agents have achieved strong market establishment, reflecting Japan enduser preferences for multifunctional, safe, and reliable dermatological solutions. These products demonstrate particular appeal across both adult and paediatric demographics supporting stable long-term demand.

Antipruritics are projected to maintain category leadership through 2026-2032 as endusers increasingly prioritise preventive care and daily skin maintenance protocols. Low-irritant formulations for paediatric applications and high-efficacy options for adult endusers will continue to drive product innovation. As household sizes contract and enduser expectations rise, brands offering rapid relief, long-lasting efficacy, and enhanced user experience will drive sustained segment growth.

By Sales Channel

- Retail Offline

- Retail Online

The segment with highest market share under sales Channel is retail offline channels with share around 85% of the Japan dermatologicals market. Health and personal care stores and pharmacies remain the most trusted offline destinations, supported by knowledgeable staff, comprehensive product assortments, and convenient access to both mass-market and premium dermatological products. These channels prove especially critical for categories where endusers seek reassurance regarding product efficacy and safety, including antipruritics, antifungals, and paediatric treatments.

Offline retail dominance is further reinforced by Japan's established culture of in-store consultation and enduser preference for purchasing daily health products through familiar, conveniently located pharmacy outlets. While e-commerce demonstrates growth—particularly in discreet categories such as hair regrowth treatments—offline channels maintain market dominance attributable to trust factors, purchase immediacy, and enduser comfort with traditional store-based purchasing behaviours.

List of Companies Covered in Japan Dermatologicals Market

The companies listed below are highly influential in the Japan dermatologicals market, with a significant market share and a strong impact on industry developments.

- Kobayashi Pharmaceutical Co Ltd

- Sato Pharmaceutical Co Ltd

- Zeria Pharmaceutical Co Ltd

- Taisho Pharmaceutical Co Ltd

- Amato Pharmaceutical Products Ltd

- Rohto Pharmaceutical Co Ltd

- Daiichi Sankyo Healthcare Co Ltd

- Kowa Co Ltd

- Ikeda Mohando Co Ltd

- Taiho Pharmaceutical Co Ltd

Competitive Landscape

Japan dermatologicals competitive landscape in 2025 is shaped by rising unit prices, premium formulations, and a rapid shift toward digital engagement. Amato Pharmaceutical strengthens leadership in haemorrhoid care through Borraginol, expanding into prevention with its Smooth Laxative and Unlog app-based stool monitoring tools that support lifestyle change and deepen user engagement. In hair loss treatments, Sunstar’s MAGMAS and Taisho’s RiUP drive growth through high-value formulations and strong online demand, while online-exclusive private labels intensify competition in antifungals with discreet packaging. Femcare players expand through self-check tools and science-based products, and antiseptic brands evolve formats to match heightened hygiene needs. Overall, diversification, digitalisation, and preventive positioning define the market’s competitive direction.

Frequently Asked Questions

Related Report

1. Market Segmentation

1.1. Research Scope

1.2. Research Methodology

1.3. Definitions and Assumptions

2. Executive Summary

3. Japan Dermatologicals Market Policies, Regulations, and Standards

4. Japan Dermatologicals Market Dynamics

4.1. Growth Factors

4.2. Challenges

4.3. Trends

4.4. Opportunities

5. Japan Dermatologicals Market Statistics, 2022-2032F

5.1. Market Size & Growth Outlook

5.1.1.By Revenues in USD Million

5.2. Market Segmentation & Growth Outlook

5.2.1.By Category

5.2.1.1. Medicated Shampoos- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2. Topical Antifungals- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3. Vaginal Antifungals- Market Insights and Forecast 2022-2032, USD Million

5.2.1.4. Hair Loss Treatments- Market Insights and Forecast 2022-2032, USD Million

5.2.1.5. Nappy (Diaper) Rash Treatments- Market Insights and Forecast 2022-2032, USD Million

5.2.1.6. Antiparasitics/Lice (Head and Body) Treatments- Market Insights and Forecast 2022-2032, USD Million

5.2.1.7. Antipruritics- Market Insights and Forecast 2022-2032, USD Million

5.2.1.8. Cold Sore Treatments- Market Insights and Forecast 2022-2032, USD Million

5.2.1.9. Haemorrhoid Treatments- Market Insights and Forecast 2022-2032, USD Million

5.2.1.10. Paediatric Dermatologicals- Market Insights and Forecast 2022-2032, USD Million

5.2.1.11. Topical Allergy Remedies/Antihistamines- Market Insights and Forecast 2022-2032, USD Million

5.2.1.12. Topical Germicidals/Antiseptics- Market Insights and Forecast 2022-2032, USD Million

5.2.2.By Dispensing Status

5.2.2.1. Prescription-based Drugs- Market Insights and Forecast 2022-2032, USD Million

5.2.2.2. Over-the-counter Drugs- Market Insights and Forecast 2022-2032, USD Million

5.2.3.By Route of Administration

5.2.3.1. Topical Administration- Market Insights and Forecast 2022-2032, USD Million

5.2.3.2. Oral Administration- Market Insights and Forecast 2022-2032, USD Million

5.2.3.3. Parenteral Administration- Market Insights and Forecast 2022-2032, USD Million

5.2.4.By Drug Type

5.2.4.1. Branded- Market Insights and Forecast 2022-2032, USD Million

5.2.4.2. Generics- Market Insights and Forecast 2022-2032, USD Million

5.2.5.By Skin Condition

5.2.5.1. Acne- Market Insights and Forecast 2022-2032, USD Million

5.2.5.2. Dermatitis- Market Insights and Forecast 2022-2032, USD Million

5.2.5.3. Psoriasis- Market Insights and Forecast 2022-2032, USD Million

5.2.5.4. Skin Cancer- Market Insights and Forecast 2022-2032, USD Million

5.2.5.5. Rosacea- Market Insights and Forecast 2022-2032, USD Million

5.2.5.6. Alopecia- Market Insights and Forecast 2022-2032, USD Million

5.2.5.7. Fungal Infections- Market Insights and Forecast 2022-2032, USD Million

5.2.5.8. Others- Market Insights and Forecast 2022-2032, USD Million

5.2.6.By End User

5.2.6.1. Hospitals- Market Insights and Forecast 2022-2032, USD Million

5.2.6.2. Cosmetic Centers- Market Insights and Forecast 2022-2032, USD Million

5.2.6.3. Dermatology Clinics- Market Insights and Forecast 2022-2032, USD Million

5.2.6.4. Homecare- Market Insights and Forecast 2022-2032, USD Million

5.2.6.5. Others- Market Insights and Forecast 2022-2032, USD Million

5.2.7.By Sales Channel

5.2.7.1. Retail Offline- Market Insights and Forecast 2022-2032, USD Million

5.2.7.2. Retail Online- Market Insights and Forecast 2022-2032, USD Million

5.2.8.By Competitors

5.2.8.1. Competition Characteristics

5.2.8.2. Market Share & Analysis

6. Japan Medicated Shampoos Market Statistics, 2022-2032

6.1. Market Size & Growth Outlook

6.1.1.By Revenues in USD Million

6.2. Market Segmentation & Growth Outlook

6.2.1.By Dispensing Status- Market Insights and Forecast 2022-2032, USD Million

6.2.2.By Route of Administration- Market Insights and Forecast 2022-2032, USD Million

6.2.3.By Drug Type- Market Insights and Forecast 2022-2032, USD Million

6.2.4.By Skin Condition- Market Insights and Forecast 2022-2032, USD Million

6.2.5.By End User- Market Insights and Forecast 2022-2032, USD Million

6.2.6.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

7. Japan Topical Antifungals Market Statistics, 2022-2032

7.1. Market Size & Growth Outlook

7.1.1.By Revenues in USD Million

7.2. Market Segmentation & Growth Outlook

7.2.1.By Dispensing Status- Market Insights and Forecast 2022-2032, USD Million

7.2.2.By Route of Administration- Market Insights and Forecast 2022-2032, USD Million

7.2.3.By Drug Type- Market Insights and Forecast 2022-2032, USD Million

7.2.4.By Skin Condition- Market Insights and Forecast 2022-2032, USD Million

7.2.5.By End User- Market Insights and Forecast 2022-2032, USD Million

7.2.6.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

8. Japan Vaginal Antifungals Market Statistics, 2022-2032

8.1. Market Size & Growth Outlook

8.1.1.By Revenues in USD Million

8.2. Market Segmentation & Growth Outlook

8.2.1.By Dispensing Status- Market Insights and Forecast 2022-2032, USD Million

8.2.2.By Route of Administration- Market Insights and Forecast 2022-2032, USD Million

8.2.3.By Drug Type- Market Insights and Forecast 2022-2032, USD Million

8.2.4.By Skin Condition- Market Insights and Forecast 2022-2032, USD Million

8.2.5.By End User- Market Insights and Forecast 2022-2032, USD Million

8.2.6.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

9. Japan Hair Loss Treatments Market Statistics, 2022-2032

9.1. Market Size & Growth Outlook

9.1.1.By Revenues in USD Million

9.2. Market Segmentation & Growth Outlook

9.2.1.By Dispensing Status- Market Insights and Forecast 2022-2032, USD Million

9.2.2.By Route of Administration- Market Insights and Forecast 2022-2032, USD Million

9.2.3.By Drug Type- Market Insights and Forecast 2022-2032, USD Million

9.2.4.By Skin Condition- Market Insights and Forecast 2022-2032, USD Million

9.2.5.By End User- Market Insights and Forecast 2022-2032, USD Million

9.2.6.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

10. Japan Nappy (Diaper) Rash Treatments Market Statistics, 2022-2032

10.1. Market Size & Growth Outlook

10.1.1. By Revenues in USD Million

10.2. Market Segmentation & Growth Outlook

10.2.1. By Dispensing Status- Market Insights and Forecast 2022-2032, USD Million

10.2.2. By Route of Administration- Market Insights and Forecast 2022-2032, USD Million

10.2.3. By Drug Type- Market Insights and Forecast 2022-2032, USD Million

10.2.4. By Skin Condition- Market Insights and Forecast 2022-2032, USD Million

10.2.5. By End User- Market Insights and Forecast 2022-2032, USD Million

10.2.6. By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

11. Japan Antiparasitics/Lice (Head and Body) Treatments Market Statistics, 2022-2032

11.1. Market Size & Growth Outlook

11.1.1. By Revenues in USD Million

11.2. Market Segmentation & Growth Outlook

11.2.1. By Dispensing Status- Market Insights and Forecast 2022-2032, USD Million

11.2.2. By Route of Administration- Market Insights and Forecast 2022-2032, USD Million

11.2.3. By Drug Type- Market Insights and Forecast 2022-2032, USD Million

11.2.4. By Skin Condition- Market Insights and Forecast 2022-2032, USD Million

11.2.5. By End User- Market Insights and Forecast 2022-2032, USD Million

11.2.6. By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

12. Japan Antipruritics Market Statistics, 2022-2032

12.1. Market Size & Growth Outlook

12.1.1. By Revenues in USD Million

12.2. Market Segmentation & Growth Outlook

12.2.1. By Dispensing Status- Market Insights and Forecast 2022-2032, USD Million

12.2.2. By Route of Administration- Market Insights and Forecast 2022-2032, USD Million

12.2.3. By Drug Type- Market Insights and Forecast 2022-2032, USD Million

12.2.4. By Skin Condition- Market Insights and Forecast 2022-2032, USD Million

12.2.5. By End User- Market Insights and Forecast 2022-2032, USD Million

12.2.6. By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

13. Japan Cold Sore Treatments Market Statistics, 2022-2032

13.1. Market Size & Growth Outlook

13.1.1. By Revenues in USD Million

13.2. Market Segmentation & Growth Outlook

13.2.1. By Dispensing Status- Market Insights and Forecast 2022-2032, USD Million

13.2.2. By Route of Administration- Market Insights and Forecast 2022-2032, USD Million

13.2.3. By Drug Type- Market Insights and Forecast 2022-2032, USD Million

13.2.4. By Skin Condition- Market Insights and Forecast 2022-2032, USD Million

13.2.5. By End User- Market Insights and Forecast 2022-2032, USD Million

13.2.6. By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

14. Japan Haemorrhoid Treatments Market Statistics, 2022-2032

14.1. Market Size & Growth Outlook

14.1.1. By Revenues in USD Million

14.2. Market Segmentation & Growth Outlook

14.2.1. By Dispensing Status- Market Insights and Forecast 2022-2032, USD Million

14.2.2. By Route of Administration- Market Insights and Forecast 2022-2032, USD Million

14.2.3. By Drug Type- Market Insights and Forecast 2022-2032, USD Million

14.2.4. By Skin Condition- Market Insights and Forecast 2022-2032, USD Million

14.2.5. By End User- Market Insights and Forecast 2022-2032, USD Million

14.2.6. By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

15. Japan Paediatric Dermatologicals Market Statistics, 2022-2032

15.1. Market Size & Growth Outlook

15.1.1. By Revenues in USD Million

15.2. Market Segmentation & Growth Outlook

15.2.1. By Dispensing Status- Market Insights and Forecast 2022-2032, USD Million

15.2.2. By Route of Administration- Market Insights and Forecast 2022-2032, USD Million

15.2.3. By Drug Type- Market Insights and Forecast 2022-2032, USD Million

15.2.4. By Skin Condition- Market Insights and Forecast 2022-2032, USD Million

15.2.5. By End User- Market Insights and Forecast 2022-2032, USD Million

15.2.6. By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

16. Japan Topical Allergy Remedies/Antihistamines Market Statistics, 2022-2032

16.1. Market Size & Growth Outlook

16.1.1. By Revenues in USD Million

16.2. Market Segmentation & Growth Outlook

16.2.1. By Dispensing Status- Market Insights and Forecast 2022-2032, USD Million

16.2.2. By Route of Administration- Market Insights and Forecast 2022-2032, USD Million

16.2.3. By Drug Type- Market Insights and Forecast 2022-2032, USD Million

16.2.4. By Skin Condition- Market Insights and Forecast 2022-2032, USD Million

16.2.5. By End User- Market Insights and Forecast 2022-2032, USD Million

16.2.6. By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

17. Japan Topical Germicidals/Antiseptics Market Statistics, 2022-2032

17.1. Market Size & Growth Outlook

17.1.1. By Revenues in USD Million

17.2. Market Segmentation & Growth Outlook

17.2.1. By Dispensing Status- Market Insights and Forecast 2022-2032, USD Million

17.2.2. By Route of Administration- Market Insights and Forecast 2022-2032, USD Million

17.2.3. By Drug Type- Market Insights and Forecast 2022-2032, USD Million

17.2.4. By Skin Condition- Market Insights and Forecast 2022-2032, USD Million

17.2.5. By End User- Market Insights and Forecast 2022-2032, USD Million

17.2.6. By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

18. Competitive Outlook

18.1. Company Profiles

18.1.1. Taisho Pharmaceutical Co Ltd

18.1.1.1. Business Description

18.1.1.2. Product Portfolio

18.1.1.3. Collaborations & Alliances

18.1.1.4. Recent Developments

18.1.1.5. Financial Details

18.1.1.6. Others

18.1.2. Amato Pharmaceutical Products Ltd

18.1.2.1. Business Description

18.1.2.2. Product Portfolio

18.1.2.3. Collaborations & Alliances

18.1.2.4. Recent Developments

18.1.2.5. Financial Details

18.1.2.6. Others

18.1.3. Rohto Pharmaceutical Co Ltd

18.1.3.1. Business Description

18.1.3.2. Product Portfolio

18.1.3.3. Collaborations & Alliances

18.1.3.4. Recent Developments

18.1.3.5. Financial Details

18.1.3.6. Others

18.1.4. Daiichi Sankyo Healthcare Co Ltd

18.1.4.1. Business Description

18.1.4.2. Product Portfolio

18.1.4.3. Collaborations & Alliances

18.1.4.4. Recent Developments

18.1.4.5. Financial Details

18.1.4.6. Others

18.1.5. Kowa Co Ltd

18.1.5.1. Business Description

18.1.5.2. Product Portfolio

18.1.5.3. Collaborations & Alliances

18.1.5.4. Recent Developments

18.1.5.5. Financial Details

18.1.5.6. Others

18.1.6. Kobayashi Pharmaceutical Co Ltd

18.1.6.1. Business Description

18.1.6.2. Product Portfolio

18.1.6.3. Collaborations & Alliances

18.1.6.4. Recent Developments

18.1.6.5. Financial Details

18.1.6.6. Others

18.1.7. Sato Pharmaceutical Co Ltd

18.1.7.1. Business Description

18.1.7.2. Product Portfolio

18.1.7.3. Collaborations & Alliances

18.1.7.4. Recent Developments

18.1.7.5. Financial Details

18.1.7.6. Others

18.1.8. Zeria Pharmaceutical Co Ltd

18.1.8.1. Business Description

18.1.8.2. Product Portfolio

18.1.8.3. Collaborations & Alliances

18.1.8.4. Recent Developments

18.1.8.5. Financial Details

18.1.8.6. Others

18.1.9. Ikeda Mohando Co Ltd

18.1.9.1. Business Description

18.1.9.2. Product Portfolio

18.1.9.3. Collaborations & Alliances

18.1.9.4. Recent Developments

18.1.9.5. Financial Details

18.1.9.6. Others

18.1.10. Taiho Pharmaceutical Co Ltd

18.1.10.1.Business Description

18.1.10.2.Product Portfolio

18.1.10.3.Collaborations & Alliances

18.1.10.4.Recent Developments

18.1.10.5.Financial Details

18.1.10.6.Others

19. Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Category |

|

| By Dispensing Status |

|

| By Route of Administration |

|

| By Drug Type |

|

| By Skin Condition |

|

| By End User |

|

| By Sales Channel |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.