Japan Neurodegenerative Disease Devices Market Report: Trends, Growth and Forecast (2026-2032)

Device Type (Neurostimulation Devices, Diagnostic & Imaging Devices, Interventional Neurology Devices, Surgical Navigation & Support Systems, CSF Management Devices, Monitoring & Wearable Devices, Assistive & Rehabilitation Devices), Indication (Parkinsons Disease, Alzheimers Disease, Multiple Sclerosis, Amyotrophic Lateral Sclerosis, Huntingtons Disease, Epilepsy, Stroke, Others), Technology Platform (Implantable Devices, External / Non-Invasive Devices, Wearable & Portable Technology, AI-Integrated & Closed-Loop Systems, Sensor-Based Technology, Robotic & Automated Systems), End User (Hospitals & Specialty Neurology Centers, Ambulatory Surgery Centers, Neurology & Movement Disorder Clinics, Rehabilitation Centers, Home Care & Remote Monitoring Settings, Long-Term Care Facilities, Research & Academic Institutions), Sales Channel (Offline, Online), Price Range (Premium Devices, Mid-Range Devices, Budget Devices) ... Read more

|

Major Players

|

Japan Neurodegenerative Disease Devices Market Statistics and Insights, 2026

- Market Size Statistics

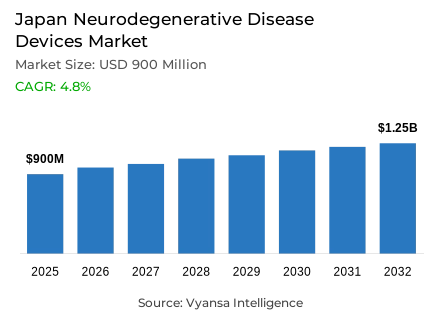

- Neurodegenerative disease devices in Japan is estimated at USD 900 million.

- The market size is expected to grow to USD 1.25 billion by 2032.

- Market to register a cagr of around 4.8% during 2026-32.

- Device Type Shares

- Diagnostic & imaging devices grabbed market share of 40%.

- Competition

- More than 10 companies are actively engaged in producing neurodegenerative disease devices in Japan.

- Top 5 companies acquired around 70% of the market share.

- Stryker; Nihon Kohden Corporation; Smith & Nephew; Medtronic; LivaNova etc., are few of the top companies.

- Indication

- Alzheimers disease grabbed 40% of the market.

Japan Neurodegenerative Disease Devices Market Outlook

Japan neurodegenerative disease device market is expanding, due to the aging population and increasing cases of neurological conditions. It was valued at about USD 900 million in 2025 and is expected to reach approximately USD 1.25 billion by 2032, growing at a CAGR of about 4.8% in the period 2026–2032. With rising prevalence rates of various neurological conditions, such as Alzheimer's disease, Parkinson's disease, and others, this is further changing healthcare priorities and thereby ensuring very strong demand for early diagnostics, monitoring, and therapeutic solutions. Neurological disorders are among the leading causes of death globally, with over 11 million annual deaths. Japan's focus on advanced healthcare infrastructure and early intervention continues to strengthen the outlook for this market.

Diagnostic and imaging devices hold the largest share with approximately 40% of the total revenue. This is because it has been a significant modality for early diagnosis and disease monitoring, especially for Alzheimer's. Imaging techniques such as MRI, CT, and PET-CT have been pivotal in diagnosing neurodegenerative alterations. Next-generation biomarker-based and AI-integrated diagnostic platforms reinforce increased diagnostic accuracy for clinicians. For instance, this enables them to identify the condition in its preclinical stages and optimize the treatment outcome, which reciprocates Japan's interest in modernizing its healthcare system.

Alzheimer's disease still holds the biggest indication with a share of about 40% in the Japan Neurodegenerative Disease Devices Market. Its dominance indicates not only the high prevalence rate-it affects more than 32 million people worldwide-but also the increasing use of devices for early-stage screening, monitoring, and care support. With an increasing focus on early diagnosis and active management of the disease, there is a gradual rise in demand for digital cognitive assessments, biomarker assays, and AI-driven imaging solutions.

With one of the highest elderly populations in the world, Japan will continue to anchor market growth into the future. Increasing investments in early detection infrastructure, supplemented by regulatory support for AI-enabled medical devices, would consequently sustain innovations across diagnostic, imaging, and therapeutic segments. This long-term focus positions Japan as one of the most advanced and resilient markets for neurodegenerative disease devices worldwide.

Japan Neurodegenerative Disease Devices Market Growth DriverRising Neurological Disease Burden Fuels Device Demand

Japan's rapidly growing burden of neurological disease, in accordance with global trends, is transforming the national healthcare agenda and creating demand for devices to monitor and diagnose advanced neurodegenerative disease. According to the World Health Organization, by 2021 more than 3 billion people more than 40% of the world's total population-were experiencing neurological disease, and neurologic diseases accounted for 11 million deaths annually. Alzheimer's disease, for example, increases its disease burden more than two-fold from 2000 - 2021. Consolidated evidence of rising global and national disease burden indicates a growing need for diagnostic and therapeutics innovations to identify Early stage symptoms of disease state. With an estimated 416 million people within the continuum of acuity of Alzheimer's disease, there is immense clinical need for early detection and disease modifying interventions.

Increasing prevalence and rising economic costs of healthcare deliverables provide strong incentives for Japan to position itself to advance its diagnostic and monitoring ecosystem. Increasingly, as early diagnosis of neurodegenerative conditions is the central tenet of treating neurodegenerative disease, it will create additional demand for technologies like imaging systems, biomarker-based tests, and monitoring devices especially in Japan's aging demographic where neurological disease incidence is highest.

Japan Neurodegenerative Disease Devices Market ChallengeShortage of Neurologists and Diagnostic Infrastructure Limits Deployment

Severe disparities in health infrastructure and workforce distribution further act as serious barriers to the proper implementation of neurodegenerative disease devices. While there are, on average, 7.1 neurologists per 100,000 people in high-income countries and 9.2 in Europe, low-income countries have only 0.1, leading to late diagnosis and limited treatment capacity. In most Asian countries, such as India, Nepal, and Bangladesh, there is less than one neurologist per million inhabitants, and in developed regions like Australia, rural communities-housing almost a third of the population-are served by a meager 4.1% of the neurology workforce.

While progress has been made in many dimensions, access to diagnostic imaging remains a critical constraint: only 47% of the global population currently has access to basic imaging services. In low- and middle-income regions, fewer than one CT scanner per million people is available, compared with about 40 per million in high-income countries. This shortage of neurologists and diagnostic infrastructure significantly constrains device adoption in regions with the highest disease burden, with the associated consequence of limiting early intervention and effective care delivery.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Japan Neurodegenerative Disease Devices Market TrendTechnological Shifts Drive Decentralized and AI-Enabled Diagnostics

Digital and biomarker-based diagnostic innovations are rapidly changing the way neurodegenerative diseases are diagnosed by reducing dependence on specialized infrastructures. Blood-based biomarker testing and digital cognitive assessments are now being introduced into primary care, providing scalable and non-invasive diagnostic options. Currently, near-infrared spectroscopy and plasma biomarkers are demonstrating 75–80% sensitivity and specificity for early-stage Alzheimer’s disease identification, thus allowing the detection of preclinical stages. These developments increase the possibility of early screening and monitoring in a range of care settings.

Artificial intelligence integration further improves device performance and regulatory acceptance. The FDA has cleared more than 1,000 AI-enabled medical devices, including emission computed tomography systems and physiologic signal amplifiers for neurological applications. Such technologies extend diagnostic capabilities well beyond neurology departments to support deployment in primary care, pharmacy, optometry, and telemedicine. By reducing dependence on specialized expertise, AI-enabled diagnostics are democratizing access to early neurodegenerative disease detection across both mature and emerging markets.

Japan Neurodegenerative Disease Devices Market OpportunityAging Demographics Create Long-Term Market Expansion Potential

Japan's rapidly aging population creates a structural foundation for continued growth in the neurodegenerative disease device market. The world will see 1.1 billion people aged 60 and over in 2023 increase to 1.4 billion by 2030 and reach 2.1 billion by 2050, with two-thirds of them in developing regions. In Japan, one of the oldest societies in the world, the demographicconcentration of elderly end users increases demand for diagnostic and monitoring technologies addressing neurological decline related to aging.

The risk of neurodegenerative disease rises sharply with age, and worldwide, the prevalence of dementia among individuals aged 65 years and over has seen a remarkable 160% increase between 1991 and 2021. As populations continue to get older, early detection, cognitive monitoring, and supportive devices are becoming key priorities in managing disease effectively. Such demographic evolution will continue to create expansion opportunities for manufacturers through 2026-2032.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Japan Neurodegenerative Disease Devices Market Segmentation Analysis

By Device Type

- Neurostimulation Devices

- Diagnostic & Imaging Devices

- Interventional Neurology Devices

- Surgical Navigation & Support Systems

- CSF Management Devices

- Monitoring & Wearable Devices

- Assistive & Rehabilitation Devices

Diagnostic and imaging devices account for almost 40% of the Japan Neurodegenerative Disease Devices Market; hence, the category is considered the leading market segment. This segment leads the market because it is essential for the detection of the diseases during the preclinical or prodromal stages of a disease, such as Alzheimer’s, which is quite crucial for therapeutic success. Neurodegenerative changes are usually confirmed by MRI and CT imaging, while functional imaging such as PET-CT allows the in vivo visualization of amyloid and tau accumulation in the brain.

This leadership in the segment has been further solidified with the continuous regulatory approvals and rapid advancement in technology. The FDA approved 3,186 neurological devices between the years 2000 to 2022, with increasing emphasis on neurodiagnostic systems. The diagnostic imaging centers are posting the highest growth rates, supported by AI integration that improves precision and workflow efficiency. This segment will continue anchoring market performance through 2032, owing to expanding healthcare systems' investment in early diagnosis infrastructures.

By Indication

- Parkinsons Disease

- Alzheimers Disease

- Multiple Sclerosis

- Amyotrophic Lateral Sclerosis

- Huntingtons Disease

- Epilepsy

- Stroke

- Others

The Japan Neurodegenerative Disease Devices Market is dominated by Alzheimer's disease and related dementias, which contribute to approximately 40% of the market. This makes the indication the single largest clinical focus of the sector. That can be attributed to the high prevalence of the condition globally, affecting in excess of 32 million worldwide, and also because it is the most studied neurodegenerative disease. Devices targeting this indication span advanced diagnostic platforms, biomarker monitoring systems, and assistive technologies designed to improve patient quality of life and caregiver efficiency.

Since the emergence of disease-modifying therapies, the need for diagnostic tools that detect patients at early stages of the disease, before symptom progression reduces treatment efficacy, has increased. Biomarker assays, AI-driven imaging, and digital cognitive assessments designed for Alzheimer's disease screening and follow-up care are increasingly being adopted by healthcare providers. This consolidated clinical and research focus ensures that the indication of Alzheimer's disease will continue to dominate the innovation pipeline and healthcare investments throughout the 2026-2032 forecast period.

List of Companies Covered in Japan Neurodegenerative Disease Devices Market

The companies listed below are highly influential in the Japan neurodegenerative disease devices market, with a significant market share and a strong impact on industry developments.

- Stryker

- Nihon Kohden Corporation

- Smith & Nephew

- Medtronic

- LivaNova

- Boston Scientific

- Abbott Laboratories

- B. Braun Melsungen AG

- Avanos Medical

- Elekta AB

Market News & Updates

- Boston Scientific, 2024:

Gained PMDA approval for FARAPULSE™ Pulsed Field Ablation System to treat paroxysmal atrial fibrillation using non-thermal electrical fields.

- Nihon Kohden Corporation, 2024:

Acquired 71.4% of Ad-Tech Medical Instrument Corporation to strengthen integrated epilepsy diagnostics and neurodiagnostic solutions.

Frequently Asked Questions

Related Report

1. Market Segmentation

1.1. Research Scope

1.2. Research Methodology

1.3. Definitions and Assumptions

2. Executive Summary

3. Japan Neurodegenerative Disease Devices Market Policies, Regulations, and Standards

4. Japan Neurodegenerative Disease Devices Market Dynamics

4.1. Growth Factors

4.2. Challenges

4.3. Trends

4.4. Opportunities

5. Japan Neurodegenerative Disease Devices Market Statistics, 2022-2032F

5.1. Market Size & Growth Outlook

5.1.1.By Revenues in USD Million

5.2. Market Segmentation & Growth Outlook

5.2.1.By Device Type

5.2.1.1. Neurostimulation Devices- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2. Diagnostic & Imaging Devices- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3. Interventional Neurology Devices- Market Insights and Forecast 2022-2032, USD Million

5.2.1.4. Surgical Navigation & Support Systems- Market Insights and Forecast 2022-2032, USD Million

5.2.1.5. CSF Management Devices- Market Insights and Forecast 2022-2032, USD Million

5.2.1.6. Monitoring & Wearable Devices- Market Insights and Forecast 2022-2032, USD Million

5.2.1.7. Assistive & Rehabilitation Devices- Market Insights and Forecast 2022-2032, USD Million

5.2.2.By Indication

5.2.2.1. Parkinsons Disease- Market Insights and Forecast 2022-2032, USD Million

5.2.2.2. Alzheimers Disease- Market Insights and Forecast 2022-2032, USD Million

5.2.2.3. Multiple Sclerosis- Market Insights and Forecast 2022-2032, USD Million

5.2.2.4. Amyotrophic Lateral Sclerosis- Market Insights and Forecast 2022-2032, USD Million

5.2.2.5. Huntingtons Disease- Market Insights and Forecast 2022-2032, USD Million

5.2.2.6. Epilepsy- Market Insights and Forecast 2022-2032, USD Million

5.2.2.7. Stroke- Market Insights and Forecast 2022-2032, USD Million

5.2.2.8. Others- Market Insights and Forecast 2022-2032, USD Million

5.2.3.By Technology Platform

5.2.3.1. Implantable Devices- Market Insights and Forecast 2022-2032, USD Million

5.2.3.2. External / Non-Invasive Devices- Market Insights and Forecast 2022-2032, USD Million

5.2.3.3. Wearable & Portable Technology- Market Insights and Forecast 2022-2032, USD Million

5.2.3.4. AI-Integrated & Closed-Loop Systems- Market Insights and Forecast 2022-2032, USD Million

5.2.3.5. Sensor-Based Technology- Market Insights and Forecast 2022-2032, USD Million

5.2.3.6. Robotic & Automated Systems- Market Insights and Forecast 2022-2032, USD Million

5.2.4.By End User

5.2.4.1. Hospitals & Specialty Neurology Centers- Market Insights and Forecast 2022-2032, USD Million

5.2.4.2. Ambulatory Surgery Centers- Market Insights and Forecast 2022-2032, USD Million

5.2.4.3. Neurology & Movement Disorder Clinics- Market Insights and Forecast 2022-2032, USD Million

5.2.4.4. Rehabilitation Centers- Market Insights and Forecast 2022-2032, USD Million

5.2.4.5. Home Care & Remote Monitoring Settings- Market Insights and Forecast 2022-2032, USD Million

5.2.4.6. Long-Term Care Facilities- Market Insights and Forecast 2022-2032, USD Million

5.2.4.7. Research & Academic Institutions- Market Insights and Forecast 2022-2032, USD Million

5.2.5.By Sales Channel

5.2.5.1. Offline- Market Insights and Forecast 2022-2032, USD Million

5.2.5.2. Online- Market Insights and Forecast 2022-2032, USD Million

5.2.6.By Price Range

5.2.6.1. Premium Devices- Market Insights and Forecast 2022-2032, USD Million

5.2.6.2. Mid-Range Devices- Market Insights and Forecast 2022-2032, USD Million

5.2.6.3. Budget Devices- Market Insights and Forecast 2022-2032, USD Million

5.2.7.By Competitors

5.2.7.1. Competition Characteristics

5.2.7.2. Market Share & Analysis

6. Japan Neurostimulation Devices Market Statistics, 2022-2032

6.1. Market Size & Growth Outlook

6.1.1.By Revenues in USD Million

6.2. Market Segmentation & Growth Outlook

6.2.1.By Indication- Market Insights and Forecast 2022-2032, USD Million

6.2.2.By Technology Platform- Market Insights and Forecast 2022-2032, USD Million

6.2.3.By End User- Market Insights and Forecast 2022-2032, USD Million

6.2.4.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

6.2.5.By Price Range- Market Insights and Forecast 2022-2032, USD Million

7. Japan Diagnostic & Imaging Devices Market Statistics, 2022-2032

7.1. Market Size & Growth Outlook

7.1.1.By Revenues in USD Million

7.2. Market Segmentation & Growth Outlook

7.2.1.By Indication- Market Insights and Forecast 2022-2032, USD Million

7.2.2.By Technology Platform- Market Insights and Forecast 2022-2032, USD Million

7.2.3.By End User- Market Insights and Forecast 2022-2032, USD Million

7.2.4.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

7.2.5.By Price Range- Market Insights and Forecast 2022-2032, USD Million

8. Japan Interventional Neurology Devices Market Statistics, 2022-2032

8.1. Market Size & Growth Outlook

8.1.1.By Revenues in USD Million

8.2. Market Segmentation & Growth Outlook

8.2.1.By Indication- Market Insights and Forecast 2022-2032, USD Million

8.2.2.By Technology Platform- Market Insights and Forecast 2022-2032, USD Million

8.2.3.By End User- Market Insights and Forecast 2022-2032, USD Million

8.2.4.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

8.2.5.By Price Range- Market Insights and Forecast 2022-2032, USD Million

9. Japan Surgical Navigation & Support Systems Market Statistics, 2022-2032

9.1. Market Size & Growth Outlook

9.1.1.By Revenues in USD Million

9.2. Market Segmentation & Growth Outlook

9.2.1.By Indication- Market Insights and Forecast 2022-2032, USD Million

9.2.2.By Technology Platform- Market Insights and Forecast 2022-2032, USD Million

9.2.3.By End User- Market Insights and Forecast 2022-2032, USD Million

9.2.4.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

9.2.5.By Price Range- Market Insights and Forecast 2022-2032, USD Million

10. Japan CSF Management Devices Market Statistics, 2022-2032

10.1. Market Size & Growth Outlook

10.1.1. By Revenues in USD Million

10.2. Market Segmentation & Growth Outlook

10.2.1. By Indication- Market Insights and Forecast 2022-2032, USD Million

10.2.2. By Technology Platform- Market Insights and Forecast 2022-2032, USD Million

10.2.3. By End User- Market Insights and Forecast 2022-2032, USD Million

10.2.4. By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

10.2.5. By Price Range- Market Insights and Forecast 2022-2032, USD Million

11. Japan Monitoring & Wearable Devices Market Statistics, 2022-2032

11.1. Market Size & Growth Outlook

11.1.1. By Revenues in USD Million

11.2. Market Segmentation & Growth Outlook

11.2.1. By Indication- Market Insights and Forecast 2022-2032, USD Million

11.2.2. By Technology Platform- Market Insights and Forecast 2022-2032, USD Million

11.2.3. By End User- Market Insights and Forecast 2022-2032, USD Million

11.2.4. By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

11.2.5. By Price Range- Market Insights and Forecast 2022-2032, USD Million

12. Japan Assistive & Rehabilitation Devices Market Statistics, 2022-2032

12.1. Market Size & Growth Outlook

12.1.1. By Revenues in USD Million

12.2. Market Segmentation & Growth Outlook

12.2.1. By Indication- Market Insights and Forecast 2022-2032, USD Million

12.2.2. By Technology Platform- Market Insights and Forecast 2022-2032, USD Million

12.2.3. By End User- Market Insights and Forecast 2022-2032, USD Million

12.2.4. By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

12.2.5. By Price Range- Market Insights and Forecast 2022-2032, USD Million

13. Competitive Outlook

13.1. Company Profiles

13.1.1. Medtronic

13.1.1.1. Business Description

13.1.1.2. Product Portfolio

13.1.1.3. Collaborations & Alliances

13.1.1.4. Recent Developments

13.1.1.5. Financial Details

13.1.1.6. Others

13.1.2. LivaNova

13.1.2.1. Business Description

13.1.2.2. Product Portfolio

13.1.2.3. Collaborations & Alliances

13.1.2.4. Recent Developments

13.1.2.5. Financial Details

13.1.2.6. Others

13.1.3. Boston Scientific

13.1.3.1. Business Description

13.1.3.2. Product Portfolio

13.1.3.3. Collaborations & Alliances

13.1.3.4. Recent Developments

13.1.3.5. Financial Details

13.1.3.6. Others

13.1.4. Abbott Laboratories

13.1.4.1. Business Description

13.1.4.2. Product Portfolio

13.1.4.3. Collaborations & Alliances

13.1.4.4. Recent Developments

13.1.4.5. Financial Details

13.1.4.6. Others

13.1.5. B. Braun Melsungen AG

13.1.5.1. Business Description

13.1.5.2. Product Portfolio

13.1.5.3. Collaborations & Alliances

13.1.5.4. Recent Developments

13.1.5.5. Financial Details

13.1.5.6. Others

13.1.6. Stryker

13.1.6.1. Business Description

13.1.6.2. Product Portfolio

13.1.6.3. Collaborations & Alliances

13.1.6.4. Recent Developments

13.1.6.5. Financial Details

13.1.6.6. Others

13.1.7. Nihon Kohden Corporation

13.1.7.1. Business Description

13.1.7.2. Product Portfolio

13.1.7.3. Collaborations & Alliances

13.1.7.4. Recent Developments

13.1.7.5. Financial Details

13.1.7.6. Others

13.1.8. Smith & Nephew

13.1.8.1. Business Description

13.1.8.2. Product Portfolio

13.1.8.3. Collaborations & Alliances

13.1.8.4. Recent Developments

13.1.8.5. Financial Details

13.1.8.6. Others

13.1.9. Avanos Medical

13.1.9.1. Business Description

13.1.9.2. Product Portfolio

13.1.9.3. Collaborations & Alliances

13.1.9.4. Recent Developments

13.1.9.5. Financial Details

13.1.9.6. Others

13.1.10. Elekta AB

13.1.10.1.Business Description

13.1.10.2.Product Portfolio

13.1.10.3.Collaborations & Alliances

13.1.10.4.Recent Developments

13.1.10.5.Financial Details

13.1.10.6.Others

14. Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Device Type |

|

| By Indication |

|

| By Technology Platform |

|

| By End User |

|

| By Sales Channel |

|

| By Price Range |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.