Germany Neurodegenerative Disease Devices Market Report: Trends, Growth and Forecast (2026-2032)

Device Type (Neurostimulation Devices, Diagnostic & Imaging Devices, Interventional Neurology Devices, Surgical Navigation & Support Systems, CSF Management Devices, Monitoring & Wearable Devices, Assistive & Rehabilitation Devices), Indication (Parkinsons Disease, Alzheimers Disease, Multiple Sclerosis, Amyotrophic Lateral Sclerosis, Huntingtons Disease, Epilepsy, Stroke, Others), Technology Platform (Implantable Devices, External / Non-Invasive Devices, Wearable & Portable Technology, AI-Integrated & Closed-Loop Systems, Sensor-Based Technology, Robotic & Automated Systems), End User (Hospitals & Specialty Neurology Centers, Ambulatory Surgery Centers, Neurology & Movement Disorder Clinics, Rehabilitation Centers, Home Care & Remote Monitoring Settings, Long-Term Care Facilities, Research & Academic Institutions), Sales Channel (Offline, Online), Price Range (Premium Devices, Mid-Range Devices, Budget Devices) ... Read more

|

Major Players

|

Germany Neurodegenerative Disease Devices Market Statistics and Insights, 2026

- Market Size Statistics

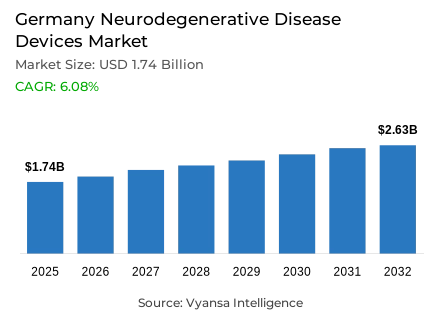

- Neurodegenerative disease devices in Germany is estimated at USD 1.74 billion.

- The market size is expected to grow to USD 2.63 billion by 2032.

- Market to register a cagr of around 6.08% during 2026-32.

- Device Type Shares

- Neurostimulation devices grabbed market share of 50%.

- Competition

- More than 10 companies are actively engaged in producing neurodegenerative disease devices in Germany.

- Top 5 companies acquired around 80% of the market share.

- Stryker; Integra LifeSciences; Nevro Corp.; Medtronic; Boston Scientific etc., are few of the top companies.

- Indication

- Parkinsons disease grabbed 40% of the market.

Germany Neurodegenerative Disease Devices Market Outlook

Germany neurodegenerative disease devices market is expected to witness stable growth from an estimated USD 1.74 billion in 2025 to approximately USD 2.63 billion by 2032, at a CAGR of about 6.08% during 2026-2032. An increasing incidence of neurological disorders like dementia, Parkinson's disease, and multiple sclerosis-mainly due to the aging population in the country-is expected to drive strong demand for advanced diagnostic and therapeutic solutions. Almost 1.8 million people suffer from dementia, while over 378,000 live with Parkinson's disease, which further increases the demand for efficient medical devices that improve disease management and patient outcomes in hospitals and neurological centers.

Growing healthcare burdens, estimated at over €60 billion annually for brain-related conditions, increase the pressure on both public and private sectors to invest more in device-based innovations. Backed by favorable government initiatives, such as the National Dementia Strategy, along with comprehensive health insurance coverage that extends to approved technologies, advanced neurostimulation and imaging systems see their adoption rate increasing. This provides sustained funding for better diagnosis, accuracy in treatment, and effective long-term care management in the neurological care continuum.

Neurostimulation devices hold approximately 50% of the total revenue in the market, due to proven efficacy and established reimbursement support. Deep brain stimulation, spinal cord stimulation, and transcranial magnetic stimulation systems are generally utilized in the management of movement disorders, especially Parkinson's disease, which accounts for about 40% of the total utilization of devices. Continuous integration of AI, remote monitoring, and miniaturization is improving treatment accuracy and patient comfort.

Overall, strong clinical infrastructure, an aging population, and policy-driven health support will continue to fuel growth in Germany. With advancements in neurostimulation and diagnostic technologies, the country is perfectly positioned to retain a lead in European neurodegenerative disease management through 2032.

Germany Neurodegenerative Disease Devices Market Growth DriverEscalating Healthcare Burden Fuels Market Growth

With an aging population structure, neurodegenerative diseases are on a steep rise in Germany. In 2023, it is estimated that almost 1.8 million people in the country were suffering from dementia, and this number may increase to 2.7 million by 2050. In addition, more than 378,000 patients suffer from Parkinson’s disease, while multiple sclerosis affects between 100,000 and 140,000 individuals, mostly females. The main driver for this rising demand is the expanding patient pool in need of better diagnostic and therapeutic devices to offer improvement in management and quality of life for end users at all stages of neurological care.

The financial toll of neurodegenerative diseases is high, with brain-related disorders costing the German economy over €60 billion annually-nearly 20% of the country's total healthcare expenditure. The growing direct and indirect economic burden, such as long-term care and productivity loss, has driven investments by both public and private healthcare providers in novel neurostimulation and imaging technologies. Increasing government contributions to neurological and mental health services ensure that funding toward device-driven solutions for neurodegenerative disease management is consistent.

Germany Neurodegenerative Disease Devices Market ChallengeRegulatory Barriers Impede Market Progress

Complexities related to compliance under the EU MDR 2017/745 have acted as a key bottleneck for market growth in Germany. The average time of product approval for neurostimulation and diagnostic devices has increased, and this can generally take 12-18 months for Class IIa and IIb devices to get certification through Notified Bodies. There are just 10 such entities in Germany as of early 2024, leading to bottlenecking and delays in the certification process, which has held innovation and product availability back within the neurodegenerative disease device landscape.

Extended transition periods through 2027-2028 and strict post-market surveillance mandates further raised operational costs, especially for small and medium-sized manufacturers. For these companies, timely approvals are difficult to come by, which means slower market entry and less competition. In turn, healthcare providers and patients also face delays in accessing next-generation neurostimulation and diagnostic technologies that are already available in other international markets. Therfore, this ultimately holds Germany back in terms of the pace of technological advancement in neurological care devices , hence hinering market growth.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Germany Neurodegenerative Disease Devices Market TrendIntegration of AI Technology Reshapes Clinical Practices

Artificial intelligence in neurostimulation and diagnostic devices is transforming clinical workflow efficiency across Germany. Leading examples of such devices include Nevro's HFX iQ and Medtronic's adaptive deep brain stimulation system, BrainSense, which feature AI-driven learning algorithms that automatically adjust therapy settings in real time according to the patient's specific neural patterns. These innovations minimize clinical visits and enhance therapeutic precision, thus helping to address workforce constraints related to the limited availability of neurologists in the German healthcare system.

Further, strong imaging infrastructure in Germany will support the adoption of AI-based devices, as the country has around 178 operational PET scanners as of 2023, and imaging volume increased by 48% between the period 2017 to 2021. The growing usage of technologies such as PET, MRI, and EEG for neurological diagnosis at an early stage supports the adoption of AI-enabled devices, while the recent adoption of telemedicine and home monitoring solutions is supportive of next-generation neurodiagnostic and therapeutic technologies within established care pathways.

Germany Neurodegenerative Disease Devices Market OpportunityGovernment Initiatives Create Favorable Market Outlook

Germany's National Dementia Strategy, initiated in July 2020 in collaboration with the German Alzheimer Society, focuses on holistic patient care and innovative methodologies of care delivery. This has opened new frontiers for developers of diagnostic imaging systems, biomarker-based detection devices, and neurostimulation technologies for early intervention. Emphasis on early and timely diagnosis, interdisciplinary treatment, and long-term optimization of care corresponds with the growing demand within the value chain for medically advanced devices that enhance disease staging and management outcomes for the end user.

The aging demographic further sustains the market potential of the country, given that people aged 65 and above form an increasing share in the population. With more than 80% of Germans being covered by statutory health insurance, reimbursement support is well established for approved neurodegenerative devices. National funding commitments targeting neurological and mental health innovation have positioned neurodegenerative diseases as the fastest-growing category within the broader central nervous system therapeutic segment, thereby securing ongoing commercial momentum for device manufacturers.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Germany Neurodegenerative Disease Devices Market Segmentation Analysis

By Device Type

- Neurostimulation Devices

- Diagnostic & Imaging Devices

- Interventional Neurology Devices

- Surgical Navigation & Support Systems

- CSF Management Devices

- Monitoring & Wearable Devices

- Assistive & Rehabilitation Devices

Neurostimulation devices have the largest share of around 50% in the Germany Neurodegenerative Disease Devices Market. These include deep brain stimulation, spinal cord stimulation, and transcranial magnetic stimulation systems-technologies widely adopted for treating movement disorders such as Parkinson’s disease. Their dominance reflects proven clinical efficacy, robust safety data, and established reimbursement pathways that facilitate widespread clinical use across hospitals and specialized neurology centers.

Continuously emerging miniaturization, longer battery life, and integration of biosensors are additive features to enhance device functionality and patient comfort. MRI compatibility, wireless programming, and remote monitoring capabilities further extend the clinical indications and enhance patient compliance. These therapeutic solutions are matched with companion diagnostic solutions in the forms of neuroimaging and electrophysiological systems, among others, that complete the ecosystem to support neurostimulation therapy in the comprehensive management of complex neurodegenerative conditions.

By Indication

- Parkinsons Disease

- Alzheimers Disease

- Multiple Sclerosis

- Amyotrophic Lateral Sclerosis

- Huntingtons Disease

- Epilepsy

- Stroke

- Others

The Parkinson's disease segment has the highest utilization in the Germany Neurodegenerative Disease Devices Market, with share of around 40% of the total device adoption and clinical applications. This is due to the high prevalence of the disease and the fact that deep brain stimulation has long been recognized as a gold-standard intervention for advanced-stage symptom management. The strong clinical evidence base on DBS in improving motor control and reducing medication dependency continues to drive demand across German neurology centers.

Its progressive nature means that the treatments become increasingly intensive as the disease advances, passing patients from pharmacological therapy to device-based interventions. Along with Germany's aging population, expected to grow significantly through 2050, the number of Parkinson's patients eligible for device therapy will only increase. Finally, an increase in clinical evidence supporting various device-based treatments for related disorders, such as essential tremor, epilepsy, and dementia-associated symptoms, shows the diversification of the indication landscape in the future.

List of Companies Covered in Germany Neurodegenerative Disease Devices Market

The companies listed below are highly influential in the Germany neurodegenerative disease devices market, with a significant market share and a strong impact on industry developments.

- Stryker

- Integra LifeSciences

- Nevro Corp.

- Medtronic

- Boston Scientific

- Abbott Laboratories

- LivaNova

- B. Braun Melsungen AG

- Axonics

- IntraPace

Market News & Updates

- Medtronic, 2025:

Partnered with Brainomix to integrate AI-powered Brainomix 360 Stroke platform with its neurovascular solutions across Western Europe for faster stroke diagnosis.

- Stryker, 2025:

Partnered with Siemens Healthineers to develop a robotic system for neurovascular procedures enhancing precision and speed.

Frequently Asked Questions

Related Report

1. Market Segmentation

1.1. Research Scope

1.2. Research Methodology

1.3. Definitions and Assumptions

2. Executive Summary

3. Germany Neurodegenerative Disease Devices Market Policies, Regulations, and Standards

4. Germany Neurodegenerative Disease Devices Market Dynamics

4.1. Growth Factors

4.2. Challenges

4.3. Trends

4.4. Opportunities

5. Germany Neurodegenerative Disease Devices Market Statistics, 2022-2032F

5.1. Market Size & Growth Outlook

5.1.1.By Revenues in USD Million

5.2. Market Segmentation & Growth Outlook

5.2.1.By Device Type

5.2.1.1. Neurostimulation Devices- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2. Diagnostic & Imaging Devices- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3. Interventional Neurology Devices- Market Insights and Forecast 2022-2032, USD Million

5.2.1.4. Surgical Navigation & Support Systems- Market Insights and Forecast 2022-2032, USD Million

5.2.1.5. CSF Management Devices- Market Insights and Forecast 2022-2032, USD Million

5.2.1.6. Monitoring & Wearable Devices- Market Insights and Forecast 2022-2032, USD Million

5.2.1.7. Assistive & Rehabilitation Devices- Market Insights and Forecast 2022-2032, USD Million

5.2.2.By Indication

5.2.2.1. Parkinsons Disease- Market Insights and Forecast 2022-2032, USD Million

5.2.2.2. Alzheimers Disease- Market Insights and Forecast 2022-2032, USD Million

5.2.2.3. Multiple Sclerosis- Market Insights and Forecast 2022-2032, USD Million

5.2.2.4. Amyotrophic Lateral Sclerosis- Market Insights and Forecast 2022-2032, USD Million

5.2.2.5. Huntingtons Disease- Market Insights and Forecast 2022-2032, USD Million

5.2.2.6. Epilepsy- Market Insights and Forecast 2022-2032, USD Million

5.2.2.7. Stroke- Market Insights and Forecast 2022-2032, USD Million

5.2.2.8. Others- Market Insights and Forecast 2022-2032, USD Million

5.2.3.By Technology Platform

5.2.3.1. Implantable Devices- Market Insights and Forecast 2022-2032, USD Million

5.2.3.2. External / Non-Invasive Devices- Market Insights and Forecast 2022-2032, USD Million

5.2.3.3. Wearable & Portable Technology- Market Insights and Forecast 2022-2032, USD Million

5.2.3.4. AI-Integrated & Closed-Loop Systems- Market Insights and Forecast 2022-2032, USD Million

5.2.3.5. Sensor-Based Technology- Market Insights and Forecast 2022-2032, USD Million

5.2.3.6. Robotic & Automated Systems- Market Insights and Forecast 2022-2032, USD Million

5.2.4.By End User

5.2.4.1. Hospitals & Specialty Neurology Centers- Market Insights and Forecast 2022-2032, USD Million

5.2.4.2. Ambulatory Surgery Centers- Market Insights and Forecast 2022-2032, USD Million

5.2.4.3. Neurology & Movement Disorder Clinics- Market Insights and Forecast 2022-2032, USD Million

5.2.4.4. Rehabilitation Centers- Market Insights and Forecast 2022-2032, USD Million

5.2.4.5. Home Care & Remote Monitoring Settings- Market Insights and Forecast 2022-2032, USD Million

5.2.4.6. Long-Term Care Facilities- Market Insights and Forecast 2022-2032, USD Million

5.2.4.7. Research & Academic Institutions- Market Insights and Forecast 2022-2032, USD Million

5.2.5.By Sales Channel

5.2.5.1. Offline- Market Insights and Forecast 2022-2032, USD Million

5.2.5.2. Online- Market Insights and Forecast 2022-2032, USD Million

5.2.6.By Price Range

5.2.6.1. Premium Devices- Market Insights and Forecast 2022-2032, USD Million

5.2.6.2. Mid-Range Devices- Market Insights and Forecast 2022-2032, USD Million

5.2.6.3. Budget Devices- Market Insights and Forecast 2022-2032, USD Million

5.2.7.By Competitors

5.2.7.1. Competition Characteristics

5.2.7.2. Market Share & Analysis

6. Germany Neurostimulation Devices Market Statistics, 2022-2032

6.1. Market Size & Growth Outlook

6.1.1.By Revenues in USD Million

6.2. Market Segmentation & Growth Outlook

6.2.1.By Indication- Market Insights and Forecast 2022-2032, USD Million

6.2.2.By Technology Platform- Market Insights and Forecast 2022-2032, USD Million

6.2.3.By End User- Market Insights and Forecast 2022-2032, USD Million

6.2.4.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

6.2.5.By Price Range- Market Insights and Forecast 2022-2032, USD Million

7. Germany Diagnostic & Imaging Devices Market Statistics, 2022-2032

7.1. Market Size & Growth Outlook

7.1.1.By Revenues in USD Million

7.2. Market Segmentation & Growth Outlook

7.2.1.By Indication- Market Insights and Forecast 2022-2032, USD Million

7.2.2.By Technology Platform- Market Insights and Forecast 2022-2032, USD Million

7.2.3.By End User- Market Insights and Forecast 2022-2032, USD Million

7.2.4.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

7.2.5.By Price Range- Market Insights and Forecast 2022-2032, USD Million

8. Germany Interventional Neurology Devices Market Statistics, 2022-2032

8.1. Market Size & Growth Outlook

8.1.1.By Revenues in USD Million

8.2. Market Segmentation & Growth Outlook

8.2.1.By Indication- Market Insights and Forecast 2022-2032, USD Million

8.2.2.By Technology Platform- Market Insights and Forecast 2022-2032, USD Million

8.2.3.By End User- Market Insights and Forecast 2022-2032, USD Million

8.2.4.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

8.2.5.By Price Range- Market Insights and Forecast 2022-2032, USD Million

9. Germany Surgical Navigation & Support Systems Market Statistics, 2022-2032

9.1. Market Size & Growth Outlook

9.1.1.By Revenues in USD Million

9.2. Market Segmentation & Growth Outlook

9.2.1.By Indication- Market Insights and Forecast 2022-2032, USD Million

9.2.2.By Technology Platform- Market Insights and Forecast 2022-2032, USD Million

9.2.3.By End User- Market Insights and Forecast 2022-2032, USD Million

9.2.4.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

9.2.5.By Price Range- Market Insights and Forecast 2022-2032, USD Million

10. Germany CSF Management Devices Market Statistics, 2022-2032

10.1. Market Size & Growth Outlook

10.1.1. By Revenues in USD Million

10.2. Market Segmentation & Growth Outlook

10.2.1. By Indication- Market Insights and Forecast 2022-2032, USD Million

10.2.2. By Technology Platform- Market Insights and Forecast 2022-2032, USD Million

10.2.3. By End User- Market Insights and Forecast 2022-2032, USD Million

10.2.4. By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

10.2.5. By Price Range- Market Insights and Forecast 2022-2032, USD Million

11. Germany Monitoring & Wearable Devices Market Statistics, 2022-2032

11.1. Market Size & Growth Outlook

11.1.1. By Revenues in USD Million

11.2. Market Segmentation & Growth Outlook

11.2.1. By Indication- Market Insights and Forecast 2022-2032, USD Million

11.2.2. By Technology Platform- Market Insights and Forecast 2022-2032, USD Million

11.2.3. By End User- Market Insights and Forecast 2022-2032, USD Million

11.2.4. By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

11.2.5. By Price Range- Market Insights and Forecast 2022-2032, USD Million

12. Germany Assistive & Rehabilitation Devices Market Statistics, 2022-2032

12.1. Market Size & Growth Outlook

12.1.1. By Revenues in USD Million

12.2. Market Segmentation & Growth Outlook

12.2.1. By Indication- Market Insights and Forecast 2022-2032, USD Million

12.2.2. By Technology Platform- Market Insights and Forecast 2022-2032, USD Million

12.2.3. By End User- Market Insights and Forecast 2022-2032, USD Million

12.2.4. By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

12.2.5. By Price Range- Market Insights and Forecast 2022-2032, USD Million

13. Competitive Outlook

13.1. Company Profiles

13.1.1. Medtronic

13.1.1.1. Business Description

13.1.1.2. Product Portfolio

13.1.1.3. Collaborations & Alliances

13.1.1.4. Recent Developments

13.1.1.5. Financial Details

13.1.1.6. Others

13.1.2. Boston Scientific

13.1.2.1. Business Description

13.1.2.2. Product Portfolio

13.1.2.3. Collaborations & Alliances

13.1.2.4. Recent Developments

13.1.2.5. Financial Details

13.1.2.6. Others

13.1.3. Abbott Laboratories

13.1.3.1. Business Description

13.1.3.2. Product Portfolio

13.1.3.3. Collaborations & Alliances

13.1.3.4. Recent Developments

13.1.3.5. Financial Details

13.1.3.6. Others

13.1.4. LivaNova

13.1.4.1. Business Description

13.1.4.2. Product Portfolio

13.1.4.3. Collaborations & Alliances

13.1.4.4. Recent Developments

13.1.4.5. Financial Details

13.1.4.6. Others

13.1.5. B. Braun Melsungen AG

13.1.5.1. Business Description

13.1.5.2. Product Portfolio

13.1.5.3. Collaborations & Alliances

13.1.5.4. Recent Developments

13.1.5.5. Financial Details

13.1.5.6. Others

13.1.6. Stryker

13.1.6.1. Business Description

13.1.6.2. Product Portfolio

13.1.6.3. Collaborations & Alliances

13.1.6.4. Recent Developments

13.1.6.5. Financial Details

13.1.6.6. Others

13.1.7. Integra LifeSciences

13.1.7.1. Business Description

13.1.7.2. Product Portfolio

13.1.7.3. Collaborations & Alliances

13.1.7.4. Recent Developments

13.1.7.5. Financial Details

13.1.7.6. Others

13.1.8. Nevro Corp.

13.1.8.1. Business Description

13.1.8.2. Product Portfolio

13.1.8.3. Collaborations & Alliances

13.1.8.4. Recent Developments

13.1.8.5. Financial Details

13.1.8.6. Others

13.1.9. Axonics

13.1.9.1. Business Description

13.1.9.2. Product Portfolio

13.1.9.3. Collaborations & Alliances

13.1.9.4. Recent Developments

13.1.9.5. Financial Details

13.1.9.6. Others

13.1.10. IntraPace

13.1.10.1.Business Description

13.1.10.2.Product Portfolio

13.1.10.3.Collaborations & Alliances

13.1.10.4.Recent Developments

13.1.10.5.Financial Details

13.1.10.6.Others

14. Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Device Type |

|

| By Indication |

|

| By Technology Platform |

|

| By End User |

|

| By Sales Channel |

|

| By Price Range |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.