Israel Room Air Conditioners Market Report: Trends, Growth and Forecast (2026-2032)

By Product Type (Split Air Conditioners (Up to 9,000 BTU/h, 9,001-12,000 BTU/h, 12,001-18,000 BTU/h, 18,001-24,000 BTU/h, Above 24,000 BTU/h), Window Air Conditioners (Up to 9,000 BTU/h, 9,001-12,000 BTU/h, 12,001-18,000 BTU/h, 18,001-24,000 BTU/h, Above 24,000 BTU/h), Others), By Technology (Inverter, Non-Inverter), By Price (Up to USD 300, USD 301 to USD 600, USD 601 to USD 1,000, Above USD 1,000), By End User (Residential (Individual Households, Apartments/Condominiums, Vacation/Secondary Homes), Commercial (Offices, Retail Stores/Showrooms, Hospitality, Healthcare Facilities, Educational Institutions, Small Commercial Establishments, Others)), By Sales Channel (Retail Online (Brand-Owned Websites/D2C, E-Commerce Marketplaces), Retail Offline (Exclusive Brand Stores, Multi-Brand Electronics & Appliance Stores, Specialty Stores, Hypermarkets/Supermarkets, Home Improvement Stores, Dealer/Distributor Network, Direct Sales/Institutional Sales, Local Independent Retailers)), By Refrigerant Type (R-32, R-410A, R-290, R-454B, Others), By Connectivity (Smart/Connected, Conventional/Non-Smart), By Energy Efficiency (1 Star, 2 Star, 3 Star, 4 Star, 5 Star) ... Read more

|

Major Players

|

Israel Room Air Conditioners Market Statistics and Insights, 2026

- Market Size Statistics

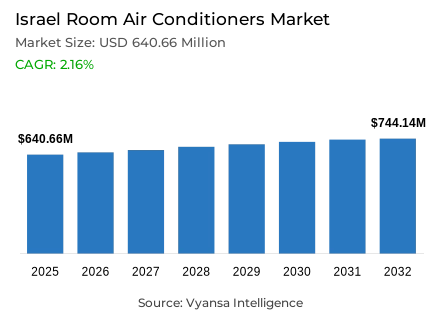

- Room air conditioners market size in Israel was valued at USD 640.66 million in 2025 and is estimated at USD 651.7 million in 2026.

- The market size is expected to grow to USD 744.14 million by 2032.

- Market to register a CAGR of around 2.16% during 2026-32.

- Product Type Shares

- Split air conditioners grabbed market share of 90%.

- Competition

- More than 5 companies are actively engaged in producing room air conditioners in Israel.

- Top 5 companies acquired around 95% of the market share.

- Haier Group, Tornado RA Consumer Products (1992) Ltd, Samsung Corp, Elco Holdings Ltd, Tadiran Holdings Ltd etc., are few of the top companies.

- Sales Channel

- Retail offline grabbed 70% of the market.

Israel Room Air Conditioners Market Outlook

The Israel room air conditioners market was valued at USD 640.66 million in 2025, establishing a commercially mature and structurally stable foundation within one of the Middle East's most advanced residential cooling appliance ecosystems. Projected to advance from USD 651.70 million in 2026 to USD 744.14 million by 2032, the sector registers a compound annual growth rate of 2.16% across the forecast horizon a measured expansion trajectory that reflects the characteristics of a high penetration, replacement cycle driven market rather than a category still in primary adoption acceleration. This steady value progression is underpinned by recurring climatic cooling imperatives, a densely urbanized residential base, and the progressive normalization of room air conditioners as standard household infrastructure across Israel's apartment dominated housing stock. The Israel Meteorological Service's documentation of 2024 as the second warmest year on record since 1950 with average temperatures approximately 1°C above the 1991-2020 baseline and summer temperatures 2°C above normal confirms that the climatic demand foundation sustaining this market is not only persistent but intensifying.

The product architecture of this market is defined by exceptional format concentration, with split air conditioners commanding approximately 90% of total product type share. This near total dominance reflects decades of consumer and installer familiarity with split system technology within Israel's predominantly apartment based residential typology a housing context in which split systems' room level precision, installation practicality, and operational reliability align more naturally with residential cooling requirements than alternative formats. The market's high maturity level means that competitive differentiation is increasingly constructed on dimensions beyond cooling performance with energy efficiency compliance, European regulatory standard alignment, and after sales service quality becoming the primary axes along which brand selection and channel preference are determined by both consumers and institutional building managers.

The regulatory transformation underway in Israel's air conditioner supply chain represents the most structurally significant near term market shaping force. The Ministry of Energy and Infrastructure's mandate that air conditioners sold by importers and manufacturers after 24 June 2025 must comply with European legal import requirements establishes a formal compliance threshold that is simultaneously raising supplier operational pressure and creating a structured product upgrade opportunity for the installed residential base. This regulatory transition aligns with the broader energy efficiency architecture established through Israeli Standard 5282, which evaluates energy consumption for climate conditioning within residential buildings embedding room air conditioner performance within a comprehensive building level energy rating framework that progressively elevates consumer and developer expectations around product compliance and efficiency visibility.

The forward outlook through 2032 is shaped by the simultaneous operation of four structural market forces: Israel's sustained warming temperature trend with 2025 documented at 1.1°C above the long term average by the Israel Meteorological Service continuous population growth reaching 10.178 million at the end of 2025 as confirmed by the Israel Central Bureau of Statistics, European compliance standard implementation across the product supply chain, and the steady replacement cycle dynamics of a mature, high penetration residential market. These converging forces collectively define a demand environment characterized by reliability, regulatory driven product renewal, and progressive efficiency premiumisation that rewards compliance capable suppliers with resilient commercial positioning through 2032.

Israel Room Air Conditioners Market Growth DriverSustained Thermal Intensity Embeds Cooling as Structural Residential Necessity

Israel's sustained and measurably intensifying warming temperature trend represents the foundational structural driver of room air conditioner demand, functioning as a climatic imperative that transforms residential cooling from a seasonal comfort preference into a year round household health and livability necessity across the country's densely urbanized residential base. The progressive upward displacement of Israel's temperature baseline documented across consecutive years by the Israel Meteorological Service ensures that cooling demand operates as a near inelastic residential expenditure priority rather than a discretionary appliance investment subject to economic cycle sensitivity. This structural climatic demand anchor creates exceptional commercial stability for market participants, insulating category revenue from the purchasing cycle volatility that affects more discretionary consumer electronics segments.

The meteorological evidence validating this driver's structural intensity is documented with authoritative precision by the Israel Meteorological Service. The year 2024 registered as the second warmest year on record in Israel since 1950, with average annual temperatures approximately 1°C above the 1991-2020 baseline and summer temperatures running 2°C above seasonal norms a thermal deviation that translates directly into extended high intensity cooling demand periods across Israel's residential and commercial building stock. Confirming the trend's continuity rather than its episodic nature, 2025 is documented at 1.1°C warmer than the long term average, with a single summer heatwave reaching 49.7°C at Gilgal representing a thermal extreme that underscores the non negotiable cooling necessity that structurally anchors Israel's room air conditioner demand base through 2032.

Israel Room Air Conditioners Market ChallengeEuropean Compliance Transition Imposes Structural Supplier Pressure

The mandatory transition to European legal import requirements for air conditioners sold by importers and manufacturers after 24 June 2025 constitutes a critical structural challenge for Israel's room air conditioner supply chain, creating a compliance transformation imperative that demands substantial product portfolio, documentation, and sourcing reconfiguration across all market participants operating under the previous regulatory framework. The challenge is compounded by the Ministry of Energy and Infrastructure's active market inspection program, which creates an enforcement accountability environment in which compliance failures carry direct commercial consequences including product withdrawal, market access restrictions, and reputational damage among an increasingly compliance aware Israeli retail and consumer community. For suppliers that built market positions under the previous standards framework, this transition represents both a significant operational investment obligation and a competitive repositioning risk.

The structural specificity of this compliance challenge is documented with regulatory precision by the Ministry of Energy and Infrastructure. Import and production of air conditioners under the old energy regulation framework were permitted only until 24 June 2024, while sales or marketing under the old framework by importers and manufacturers were permissible only until 24 June 2025 after which European legal import requirement compliance became mandatory across the channel. The phased implementation timeline created a compressed operational window within which suppliers were required to complete product line updates, certification processes, documentation upgrades, and inventory transitions simultaneously. For brands navigating this transition successfully, compliance achievement represents a structural competitive barrier that protects their market position against non compliant challengers. For those unable to meet the deadline, the Ministry's active market inspection program creates an ongoing commercial vulnerability that will define competitive positioning through 2032.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Israel Room Air Conditioners Market TrendEnergy Efficiency Compliance Emerges as the Primary Consumer Purchase Signal

The progressive elevation of energy efficiency compliance and formal performance certification from background specification parameter to primary consumer purchase evaluation criterion represents a defining structural trend in Israel's room air conditioners market, reshaping the competitive differentiation framework within which brands must construct their value propositions and communication strategies. This trend reflects the convergence of regulatory mandate, building energy rating integration, and a consumer base that is becoming systematically more sophisticated in its ability to evaluate and compare air conditioner energy performance driven by rising electricity cost awareness, European label familiarity, and the embedding of cooling equipment performance within Israel's residential building energy certification framework.

The regulatory and standards architecture driving this trend is documented with authority by the Ministry of Energy and Infrastructure. Israeli Standard 5282 evaluates energy consumption for climate conditioning and lighting in residential buildings embedding air conditioner performance within a comprehensive building level energy rating system that influences both consumer perception and property transaction dynamics. The complementary mandate requiring European legal import requirement compliance for all importer and manufacturer sales after 24 June 2025 reinforces this efficiency focused framework by establishing a formal minimum performance threshold below which products cannot legally be sold through compliant channels. Together, these regulatory instruments are systematically elevating consumer energy efficiency awareness, making certified performance ratings an increasingly decisive purchase filter, and establishing energy compliance as the foundational competitive prerequisite for market participation through 2032.

Israel Room Air Conditioners Market OpportunityPopulation Growth Generates Continuous Residential Installation Headroom

Israel's consistent and demographically diverse population growth trajectory creates a structurally reliable and continuously regenerating commercial opportunity for room air conditioner market participants, generating a steady flow of new household formations, residential unit occupations, and family size expansions that translate directly into new installation demand, additional room unit requirements, and replacement purchase activity across the country's predominantly urban, apartment intensive housing stock. In a market characterized by near universal air conditioner penetration within the established urban residential base, population driven household formation represents the primary organic demand expansion mechanism providing market participants with a predictable, census validated growth foundation that operates independently of consumer preference cycles or macroeconomic fluctuations.

The demographic foundation of this opportunity is quantified with precision by the Israel Central Bureau of Statistics. Israel's population reached approximately 10.178 million at the end of 2025, reflecting 1.1% year on year growth a rate that, sustained across a base exceeding 10 million, generates approximately 112,000 net population additions annually, translating into consistent new household formation activity that creates recurring first installation and additional unit demand for room air conditioners. This population growth dynamic operates within a climatic context confirmed by the Israel Meteorological Service's documentation of sustained above baseline temperature profiles across consecutive years that ensures newly formed households experience immediate and recurring cooling necessity, compressing the timeline between household formation and first air conditioner acquisition. The combination of steady demographic expansion, near universal residential electricity connectivity, established consumer familiarity with split system technology, and European compliance driven product renewal creates a multi dimensional opportunity landscape that supports sustained commercial growth through 2032.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Israel Room Air Conditioners Market Segmentation Analysis

By Product Type

- Split Air Conditioners

- Up to 9,000 BTU/h

- 9,001-12,000 BTU/h

- 12,001-18,000 BTU/h

- 18,001-24,000 BTU/h

- Above 24,000 BTU/h

- Window Air Conditioners

- Up to 9,000 BTU/h

- 9,001-12,000 BTU/h

- 12,001-18,000 BTU/h

- 18,001-24,000 BTU/h

- Above 24,000 BTU/h

- Others

The segment with highest market share under the product type is split air conditioners, accounting for approximately 90% of the total market. This near total dominance reflects the deep structural alignment between split system technology and the specific residential cooling requirements of Israel's urban apartment intensive housing stock a built environment in which the combination of room level precision cooling, wall mounted installation convenience, operational quietness, and aesthetic residential integration make split systems the unambiguous product of choice for both new installations and replacement purchases. With nine tenths of total market value concentrated within a single product format, split air conditioners define the entire competitive, commercial, and regulatory agenda of the Israel room air conditioners market establishing the performance benchmarks, compliance specifications, and service expectations that all market participants must address in their strategic and operational planning.

The structural leadership of split air conditioners is being actively reinforced by Israel's transition to European legal import requirements, which took full effect for importer and manufacturer sales after 24 June 2025 as confirmed by the Ministry of Energy and Infrastructure. This regulatory transition creates a product renewal imperative within the dominant split system segment, as non compliant legacy inventory exits the market and consumers upgrading to European standard compliant models drive replacement purchase activity. The integration of air conditioner energy performance within Israeli Standard 5282's residential building energy rating framework further deepens split systems' centrality to Israel's built environment management agenda embedding cooling equipment compliance within the broader residential property valuation and transaction context. The segment's commanding position as the market's primary revenue contributor and competitive focal point is expected to remain structurally intact through 2032.

By Sales Channel

- Retail Online

- Brand-Owned Websites/D2C

- E-Commerce Marketplaces

- Retail Offline

- Exclusive Brand Stores

- Multi-Brand Electronics & Appliance Stores

- Specialty Stores

- Hypermarkets/Supermarkets

- Home Improvement Stores

- Dealer/Distributor Network

- Direct Sales/Institutional Sales

- Local Independent Retailers

The segment with highest market share under the sales channel is retail offline, accounting for approximately 70% of the total market. This dominant share reflects the comprehensive purchase journey complexity that characterizes room air conditioner acquisition in Israel's mature market where consumer decisions involve not only product selection but installation logistics coordination, capacity sizing consultation, energy efficiency rating comparison, compliance verification, and after sales service arrangement. Physical retail environments are uniquely equipped to support this multi dimensional decision process, providing the direct product comparison, technical consultation, and service commitment infrastructure that consumers require when investing in a high value, installation dependent residential appliance. The 70% offline share confirms that even in one of the region's most digitally sophisticated consumer economies, the room air conditioner purchase journey resists pure digital displacement.

The structural persistence of offline retail dominance is reinforced by the category's post purchase service dependencies installation, maintenance, warranty management, and replacement coordination that are most effectively initiated and sustained through physical retail relationships. As Israel's regulatory transition to European compliance standards creates a more specification complex consumer evaluation environment, the retail floor's capacity to facilitate direct energy label comparison, compliance certification verification, and informed technical dialogue becomes an increasingly critical purchase conversion asset. The Israel Central Bureau of Statistics' documentation of population growth reaching 10.178 million at end 2025 reflecting 1.1% annual expansion ensures a continuously growing residential consumer base that sustains consistent traffic through physical retail channels. Offline retail's structural dominance as the primary commercial touchpoint for brand consideration, specification evaluation, and purchase finalization is expected to remain the defining channel characteristic of this market through 2032.

List of Companies Covered in Israel Room Air Conditioners Market

The companies listed below are highly influential in the Israel room air conditioners market, with a significant market share and a strong impact on industry developments.

- Haier Group

- Tornado RA Consumer Products (1992) Ltd

- Samsung Corp

- Elco Holdings Ltd

- Tadiran Holdings Ltd

- LG Corp

- Hisense Group

Market News & Updates

- Tadiran Holdings Ltd, 2026:

Tadiran’s official 2026 content and product lineup highlight the ALPHA PRO Inverter wall-mounted series and the newer SILENT SENSE positioning, focusing on smart inverter control, quieter operation, room-by-room comfort, and connected-home compatibility. This is a major Israel room AC market update because Tadiran is one of the country’s key local brands, and these 2026 features reinforce competition in premium residential inverter split ACs where energy savings, smart control, and lower-noise operation are central purchase drivers.

- Samsung Corp, 2025:

Samsung’s official Levant air-conditioner pages in 2025 highlight the Bespoke AI WindFree lineup with AI Fast & Comfort Cooling, AI Energy Mode, Comfort Drying, SmartThings/Map View, and Quick Remote, while Samsung’s Levant support content for air conditioners was updated in June 2025. This is relevant to the Israel room AC market because it shows Samsung actively pushing AI-connected wall-mounted AC features in the regional market, which aligns with demand for smart, energy-aware residential cooling in Israel.

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- Israel Room Air Conditioners Market Policies, Regulations, and Standards

- Israel Room Air Conditioners Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- Israel Room Air Conditioners Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Units Sold in Thousand Units

- Market Segmentation & Growth Outlook

- By Product Type

- Split Air Conditioners- Market Insights and Forecast 2022-2032, USD Million

- Up to 9,000 BTU/h- Market Insights and Forecast 2022-2032, USD Million

- 9,001-12,000 BTU/h- Market Insights and Forecast 2022-2032, USD Million

- 12,001-18,000 BTU/h- Market Insights and Forecast 2022-2032, USD Million

- 18,001-24,000 BTU/h- Market Insights and Forecast 2022-2032, USD Million

- Above 24,000 BTU/h- Market Insights and Forecast 2022-2032, USD Million

- Window Air Conditioners- Market Insights and Forecast 2022-2032, USD Million

- Up to 9,000 BTU/h- Market Insights and Forecast 2022-2032, USD Million

- 9,001-12,000 BTU/h- Market Insights and Forecast 2022-2032, USD Million

- 12,001-18,000 BTU/h- Market Insights and Forecast 2022-2032, USD Million

- 18,001-24,000 BTU/h- Market Insights and Forecast 2022-2032, USD Million

- Above 24,000 BTU/h- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- Split Air Conditioners- Market Insights and Forecast 2022-2032, USD Million

- By Technology

- Inverter- Market Insights and Forecast 2022-2032, USD Million

- Non-Inverter- Market Insights and Forecast 2022-2032, USD Million

- By Price

- Up to USD 300- Market Insights and Forecast 2022-2032, USD Million

- USD 301 to USD 600- Market Insights and Forecast 2022-2032, USD Million

- USD 601 to USD 1,000- Market Insights and Forecast 2022-2032, USD Million

- Above USD 1,000- Market Insights and Forecast 2022-2032, USD Million

- By End User

- Residential- Market Insights and Forecast 2022-2032, USD Million

- Individual Households- Market Insights and Forecast 2022-2032, USD Million

- Apartments/Condominiums- Market Insights and Forecast 2022-2032, USD Million

- Vacation/Secondary Homes- Market Insights and Forecast 2022-2032, USD Million

- Commercial- Market Insights and Forecast 2022-2032, USD Million

- Offices- Market Insights and Forecast 2022-2032, USD Million

- Retail Stores/Showrooms- Market Insights and Forecast 2022-2032, USD Million

- Hospitality- Market Insights and Forecast 2022-2032, USD Million

- Healthcare Facilities- Market Insights and Forecast 2022-2032, USD Million

- Educational Institutions- Market Insights and Forecast 2022-2032, USD Million

- Small Commercial Establishments- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- Residential- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel

- Retail Online- Market Insights and Forecast 2022-2032, USD Million

- Brand-Owned Websites/D2C- Market Insights and Forecast 2022-2032, USD Million

- E-Commerce Marketplaces- Market Insights and Forecast 2022-2032, USD Million

- Retail Offline- Market Insights and Forecast 2022-2032, USD Million

- Exclusive Brand Stores- Market Insights and Forecast 2022-2032, USD Million

- Multi-Brand Electronics & Appliance Stores- Market Insights and Forecast 2022-2032, USD Million

- Specialty Stores- Market Insights and Forecast 2022-2032, USD Million

- Hypermarkets/Supermarkets- Market Insights and Forecast 2022-2032, USD Million

- Home Improvement Stores- Market Insights and Forecast 2022-2032, USD Million

- Dealer/Distributor Network- Market Insights and Forecast 2022-2032, USD Million

- Direct Sales/Institutional Sales- Market Insights and Forecast 2022-2032, USD Million

- Local Independent Retailers- Market Insights and Forecast 2022-2032, USD Million

- Retail Online- Market Insights and Forecast 2022-2032, USD Million

- By Refrigerant Type

- R-32- Market Insights and Forecast 2022-2032, USD Million

- R-410A- Market Insights and Forecast 2022-2032, USD Million

- R-290- Market Insights and Forecast 2022-2032, USD Million

- R-454B- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By Connectivity

- Smart/Connected- Market Insights and Forecast 2022-2032, USD Million

- Conventional/Non-Smart- Market Insights and Forecast 2022-2032, USD Million

- By Energy Efficiency

- 1 Star- Market Insights and Forecast 2022-2032, USD Million

- 2 Star- Market Insights and Forecast 2022-2032, USD Million

- 3 Star- Market Insights and Forecast 2022-2032, USD Million

- 4 Star- Market Insights and Forecast 2022-2032, USD Million

- 5 Star- Market Insights and Forecast 2022-2032, USD Million

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Product Type

- Market Size & Growth Outlook

- Israel Split Air Conditioners Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Units Sold in Thousand Units

- Market Segmentation & Growth Outlook

- By Technology- Market Insights and Forecast 2022-2032, USD Million

- By Price- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Refrigerant Type- Market Insights and Forecast 2022-2032, USD Million

- By Connectivity- Market Insights and Forecast 2022-2032, USD Million

- By Energy Efficiency- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Israel Window Air Conditioners Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Units Sold in Thousand Units

- Market Segmentation & Growth Outlook

- By Technology- Market Insights and Forecast 2022-2032, USD Million

- By Price- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Refrigerant Type- Market Insights and Forecast 2022-2032, USD Million

- By Connectivity- Market Insights and Forecast 2022-2032, USD Million

- By Energy Efficiency- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- Elco Holdings Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Tadiran Holdings Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Haier Group

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Tornado RA Consumer Products (1992) Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Samsung Corp

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- LG Corp

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Hisense Group

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Others

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Elco Holdings Ltd

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Product Type |

|

| By Technology |

|

| By Price |

|

| By End User |

|

| By Sales Channel |

|

| By Refrigerant Type |

|

| By Connectivity |

|

| By Energy Efficiency |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.