Indonesia Juice Market Report: Trends, Growth and Forecast (2026-2032)

By Category (100% Juice (Not from Concentrate, Reconstituted), Juice Drinks (up to 24% Juice), Nectars (High Concentration (40% to 50% fruit content), Medium Concentration (30% to 39% fruit content), Low Concentration (25% to 29% fruit content)), Vegetable Juice, Fruit and Vegetable Blends), By Nature (Conventional, Organic), By Packaging Material (Plastic, Glass, Metal, Others), By Packaging Type (PET Bottles, Aseptic Packages (Cartons), Glass Bottles, Metal Cans, Disposable Cups & Pouches), By Sales Channel (Off-Trade (Hypermarkets/ Supermarkets, Retail Outlets, Convenience Stores, Online Platforms), On-Trade), By Region (Sumatra, Java, Kalimantan, Sulawesi, Others) ... Read more

|

Major Players

|

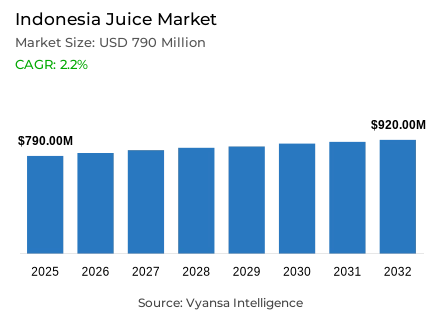

Indonesia Juice Market Statistics and Insights, 2026

- Market Size Statistics

- Juice market size in Indonesia was estimated at USD 790 million in 2025.

- The market size is expected to grow to USD 920 million by 2032.

- Market to register a CAGR of around 2.2% during 2026-32.

- Category Shares

- Juice drinks (up to 24% juice) grabbed market share of 75%.

- Competition

- More than 10 companies are actively engaged in producing juice in Indonesia.

- Top 5 companies acquired around 85% of the market share.

- Djojonegoro C-1000 PT, Sappe Plc Co Ltd, Heinz ABC Indonesia PT, Tirta Alam Segar PT, Coca-Cola Indonesia PT etc., are few of the top companies.

- Sales Channel

- Off-trade grabbed 85% of the market.

Indonesia Juice Market Outlook

The Indonesia juice market is a stable segment of the larger beverage market, with a distinct emphasis on extreme price-sensitivity and portable packaging. The market is estimated to reach USD 790 million in 2025 and USD 920 million in 2032 with a consistent CAGR of about 2.2% in the 2026–32 period. Although the market is experiencing headwinds due to a declining purchasing power and geopolitical boycotts on on-trade destinations, the category is supported by its wide appeal across all age groups and income brackets.

The strategic use of cup packaging is a characteristic of the Indonesian landscape that has allowed brands like Ale Ale to offer a highly competitive price of IDR 1,000. The market is dominated by juice drinks (up to 24% juice) with a 75% share, which enjoy the advantage of being available everywhere in the traditional outlets. On the other hand, 100% juice is becoming more niche, mostly confined to high-end supermarkets in high-income neighborhoods because of its higher prices and larger pack sizes.

Innovation is divided into volume-based affordability and value-based health trends. In the mid-to-high-income segments, the brands are oriented on lower sugar content, vitamin enrichment (C and D), and fashionable flavour profiles endorsed by international brand ambassadors like K-pop stars. In the meantime, the low-end segment is still concerned with cost-effectiveness. The convenience stores are likely to have a bigger role to play in the coming years by launching single-serve, aesthetically appealing formats that will support the fast-paced, on-the-go lifestyle of the country.

The distribution environment is skewed towards home and impulse consumption, with off-trade outlets taking 85% of the market. The main point of sale is still small local grocers, including warungs, as they are close and offer individual cup packs. Nevertheless, e-commerce is the most vibrant expanding channel, which has surmounted the past cold-chain logistics challenges to emerge as a destination of choice when it comes to bulk buying and imported niche juices via multi-pack offers and free shipping.

Indonesia Juice Market Growth Driver

Affordable Single-Serve Pack Strategies Sustaining Everyday Juice Accessibility

Packaged juice is not obsolete as brands are based on affordability and small and convenient sizes that fit daily budgets. This is important in a price sensitive environment where household spending is still wary. In February 2025, the year-on-year deflation in Statistics Indonesia was 0.09%, which reflects weak demand in the wider economy.

Meanwhile, prices remain volatile enough to keep end user concerned with value. In September 2025, Statistics Indonesia indicated that the year-on-year headline inflation stood at 2.65%, which supports the significance of low out-of-pocket choices and convenient pack designs in making regular purchases of juice.

Indonesia Juice Market Challenge

Limited Foodservice Penetration and Channel Concentration Constraining Out-of-Home Sales

Packaged juice faces an obvious obstacle in the foodservice merket due to the lack of availability and the preference of fresh juice by many outlets, making the presence of packaged juice less noticeable during away-from-home events. In the case where the channel relies on a few large limited-service chains, external shocks like consumer boycotts can easily upset the demand, as shown in the given material.

This threat is increased because end user are increasingly picky when it comes to discretionary expenditure. According to the consumer survey of Bank Indonesia, the Consumer Confidence Index stands at 118.1 in July 2025 and 115.0 in September 2025, which means that the confidence is still optimistic but still changes enough to affect non-essential purchases in on-trade environments.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Indonesia Juice Market Trend

Rapid Expansion of Cashless Payments Reinforcing Digital and E-Commerce Purchasing Behaviour

Evident structural change is the fast growth of online payments, which enables online discovery, promotions, and repeat buying of beverage shoppers. According to Bank Indonesia, in July 2025, the value of digital transactions increased 45.30% annually with 4.44 billion digital transactions, which shows how fast cashless usage is expanding in the daily business. In this context, the rate of QRIS adoption increases rapidly, and the volume of QRIS transactions increases by 162.77% annually in July 2025.

The volume of mobile banking transactions also rose 26.07% year-on-year, which favors the price reductions, free-shipping, and multi-pack promotions as e-commerce gains momentum in purchasing juices.

Indonesia Juice Market Opportunity

Scalable E-Commerce and Digital Payment Infrastructure Enabling Multi-Pack and Bulk Juice Growth

The e-commerce momentum of price reductions, free shipping, and multi-pack deals, which creates a potential growth opportunity of larger packs and bulk juice orders. The financial foundation of this opportunity is already building up. Bank Indonesia demonstrates 4.44 billion digital transactions in July 2025, and the QRIS volume increases by 162.77% annually, which makes low-friction checkout more widespread across platforms and merchants. With the expansion of faster rails, brands can advertise intended replenishment patterns like multi-pack offers and recurrent deals that can fit bulk purchasers.

Bank Indonesia records BI Fast transaction volume growth of 37.56% year-on-year in July 2025, which facilitates smoother transactions that minimize checkout drop-offs and enable e-commerce to compete with regular beverage stock-ups.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Indonesia Juice Market Segmentation Analysis

By Category

- 100% Juice

- Not from Concentrate

- Reconstituted

- Juice Drinks (up to 24% Juice)

- Nectars

- High Concentration (40% to 50% fruit content)

- Medium Concentration (30% to 39% fruit content)

- Low Concentration (25% to 29% fruit content)

- Vegetable Juice

- Fruit and Vegetable Blends

The segment has the highest share around the category for the Indonesian juice market, where Juice Drinks (up to 24% Juice) grabbed a market share of 75%. This overwhelming dominance is rooted in the cup packaging phenomenon, which provides an entry-level price point that is virtually immune to inflationary pressures. Brands like Tirta Alam Segar’s Ale Ale and Floridina have successfully captured the mass market by ensuring their products are available in almost every local warung, making them a staple for children and price-sensitive adults alike.

In addition to affordability, this segment thrives on its unparalleled diversity, offering the widest range of flavors and brands that target every income demographic. While 100% juices and nectars struggle with limited availability and high costs, juice drinks have achieved 100% penetration across all off-trade channels. This versatility allows the segment to act as a resilient hedge against fluctuating consumer spending power, ensuring it remains the primary driver of volume growth for the merket through 2032.

By Sales Channel

- Off-Trade

- Hypermarkets/ Supermarkets

- Retail Outlets

- Convenience Stores

- Online Platforms

- On-Trade

The segment has the highest share around the Sales Channel is Off-Trade, which grabbed 85% of the market. This high concentration is driven by the cultural importance of small local grocers (warungs and toko kelontong), which serve as the primary source for juice across the archipelago. These outlets are uniquely positioned to sell individual cup packs at prices that rival modern retail promotions. Furthermore, the convenience of neighborhood proximity allows end user to make frequent, small-scale purchases without the added costs of travel or parking associated with hypermarkets.

While the on-trade channel has faced recent declines due to limited product availability and social boycotts of certain international restaurant chains, the off-trade channel has modernized rapidly. E-commerce platforms like Tokopedia and Lazada have transformed the retail landscape by partnering with specialized logistics services to handle refrigerated deliveries. This evolution has made it easier for end user to access bulk 1-liter packs and premium imported products at home, further cementing the off-trade channel’s dominance in the Indonesian market.

List of Companies Covered in Indonesia Juice Market

The companies listed below are highly influential in the Indonesia juice market, with a significant market share and a strong impact on industry developments.

- Djojonegoro C-1000 PT

- Sappe Plc Co Ltd

- Heinz ABC Indonesia PT

- Tirta Alam Segar PT

- Coca-Cola Indonesia PT

- Unilever Indonesia Tbk PT

- Aneka Semesta Nutrisindo CV

- Kalbe Farma Tbk PT

- Diamond Cold Storage PT

- Tipco Foods Co Ltd

Competitive Landscape

Indonesia juice market in 2025 is dominated by Tirta Alam Segar, which leads off-trade volumes through ultra-affordable juice drinks such as Ale Ale and Floridina, leveraging IDR1,000 cup pricing and deep penetration in warungs to capture low- and mid-income consumers. Mogu Mogu, owned by Sappe, represents the most dynamic challenger, positioned at a premium-to-mid tier with strong branding, K-Pop endorsements, and aggressive promotions targeting higher-income teens and young adults. Indirect competition comes from RTD tea and bottled water, which compete strongly on price and availability, particularly in on-trade settings. Key differentiation gaps exist in affordable health-oriented innovations, smaller premium pack sizes, and broader availability of 100% juice beyond affluent retail locations.

Frequently Asked Questions

Related Report

1. Market Segmentation

1.1. Research Scope

1.2. Research Methodology

1.3. Definitions and Assumptions

2. Executive Summary

3. Indonesia Juice Market Policies, Regulations, and Standards

4. Indonesia Juice Market Dynamics

4.1. Growth Factors

4.2. Challenges

4.3. Trends

4.4. Opportunities

5. Indonesia Juice Market Statistics, 2022-2032F

5.1. Market Size & Growth Outlook

5.1.1.By Revenues in USD Million

5.1.2.By Quantity Sold in Million Litres

5.2. Market Segmentation & Growth Outlook

5.2.1.By Category

5.2.1.1. 100% Juice- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.1. Not from Concentrate- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.2. Reconstituted- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2. Juice Drinks (up to 24% Juice)- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3. Nectars- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3.1. High Concentration (40% to 50% fruit content)- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3.2. Medium Concentration (30% to 39% fruit content)- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3.3. Low Concentration (25% to 29% fruit content)- Market Insights and Forecast 2022-2032, USD Million

5.2.1.4. Vegetable Juice- Market Insights and Forecast 2022-2032, USD Million

5.2.1.5. Fruit and Vegetable Blends- Market Insights and Forecast 2022-2032, USD Million

5.2.2.By Nature

5.2.2.1. Conventional- Market Insights and Forecast 2022-2032, USD Million

5.2.2.2. Organic- Market Insights and Forecast 2022-2032, USD Million

5.2.3.By Packaging Material

5.2.3.1. Plastic- Market Insights and Forecast 2022-2032, USD Million

5.2.3.2. Glass- Market Insights and Forecast 2022-2032, USD Million

5.2.3.3. Metal- Market Insights and Forecast 2022-2032, USD Million

5.2.3.4. Others- Market Insights and Forecast 2022-2032, USD Million

5.2.4.By Packaging Type

5.2.4.1. PET Bottles- Market Insights and Forecast 2022-2032, USD Million

5.2.4.2. Aseptic Packages (Cartons)- Market Insights and Forecast 2022-2032, USD Million

5.2.4.3. Glass Bottles- Market Insights and Forecast 2022-2032, USD Million

5.2.4.4. Metal Cans- Market Insights and Forecast 2022-2032, USD Million

5.2.4.5. Disposable Cups & Pouches- Market Insights and Forecast 2022-2032, USD Million

5.2.5.By Sales Channel

5.2.5.1. Off-Trade- Market Insights and Forecast 2022-2032, USD Million

5.2.5.1.1. Hypermarkets/ Supermarkets - Market Insights and Forecast 2022-2032, USD Million

5.2.5.1.2. Retail Outlets - Market Insights and Forecast 2022-2032, USD Million

5.2.5.1.3. Convenience Stores- Market Insights and Forecast 2022-2032, USD Million

5.2.5.1.4. Online Platforms- Market Insights and Forecast 2022-2032, USD Million

5.2.5.2. On-Trade- Market Insights and Forecast 2022-2032, USD Million

5.2.6.By Region

5.2.6.1. Sumatra

5.2.6.2. Java

5.2.6.3. Kalimantan

5.2.6.4. Sulawesi

5.2.6.5. Others

5.2.7.By Competitors

5.2.7.1. Competition Characteristics

5.2.7.2. Market Share & Analysis

6. Indonesia 100% Juice Market Statistics, 2022-2032

6.1. Market Size & Growth Outlook

6.1.1.By Revenues in USD Million

6.1.2.By Quantity Sold in Million Litres

6.2. Market Segmentation & Growth Outlook

6.2.1.By Nature- Market Insights and Forecast 2022-2032, USD Million

6.2.2.By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

6.2.3.By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

6.2.4.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

6.2.5.By Region- Market Insights and Forecast 2022-2032, USD Million

7. Indonesia Juice Drinks (up to 24% Juice) Market Statistics, 2022-2032

7.1. Market Size & Growth Outlook

7.1.1.By Revenues in USD Million

7.1.2.By Quantity Sold in Million Litres

7.2. Market Segmentation & Growth Outlook

7.2.1.By Nature- Market Insights and Forecast 2022-2032, USD Million

7.2.2.By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

7.2.3.By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

7.2.4.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

7.2.5.By Region- Market Insights and Forecast 2022-2032, USD Million

8. Indonesia Nectars Market Statistics, 2022-2032

8.1. Market Size & Growth Outlook

8.1.1.By Revenues in USD Million

8.1.2.By Quantity Sold in Million Litres

8.2. Market Segmentation & Growth Outlook

8.2.1.By Nature- Market Insights and Forecast 2022-2032, USD Million

8.2.2.By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

8.2.3.By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

8.2.4.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

8.2.5.By Region- Market Insights and Forecast 2022-2032, USD Million

9. Indonesia Vegetable Juice Market Statistics, 2022-2032

9.1. Market Size & Growth Outlook

9.1.1.By Revenues in USD Million

9.1.2.By Quantity Sold in Million Litres

9.2. Market Segmentation & Growth Outlook

9.2.1.By Nature- Market Insights and Forecast 2022-2032, USD Million

9.2.2.By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

9.2.3.By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

9.2.4.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

9.2.5.By Region- Market Insights and Forecast 2022-2032, USD Million

10. Indonesia Fruit and Vegetable Blends Market Statistics, 2022-2032

10.1. Market Size & Growth Outlook

10.1.1. By Revenues in USD Million

10.1.2. By Quantity Sold in Million Litres

10.2. Market Segmentation & Growth Outlook

10.2.1. By Nature- Market Insights and Forecast 2022-2032, USD Million

10.2.2. By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

10.2.3. By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

10.2.4. By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

10.2.5. By Region- Market Insights and Forecast 2022-2032, USD Million

11. Competitive Outlook

11.1. Company Profiles

11.1.1. Tirta Alam Segar PT

11.1.1.1. Business Description

11.1.1.2. Product Portfolio

11.1.1.3. Collaborations & Alliances

11.1.1.4. Recent Developments

11.1.1.5. Financial Details

11.1.1.6. Others

11.1.2. Coca-Cola Indonesia PT

11.1.2.1. Business Description

11.1.2.2. Product Portfolio

11.1.2.3. Collaborations & Alliances

11.1.2.4. Recent Developments

11.1.2.5. Financial Details

11.1.2.6. Others

11.1.3. Unilever Indonesia Tbk PT

11.1.3.1. Business Description

11.1.3.2. Product Portfolio

11.1.3.3. Collaborations & Alliances

11.1.3.4. Recent Developments

11.1.3.5. Financial Details

11.1.3.6. Others

11.1.4. Aneka Semesta Nutrisindo CV

11.1.4.1. Business Description

11.1.4.2. Product Portfolio

11.1.4.3. Collaborations & Alliances

11.1.4.4. Recent Developments

11.1.4.5. Financial Details

11.1.4.6. Others

11.1.5. Kalbe Farma Tbk PT

11.1.5.1. Business Description

11.1.5.2. Product Portfolio

11.1.5.3. Collaborations & Alliances

11.1.5.4. Recent Developments

11.1.5.5. Financial Details

11.1.5.6. Others

11.1.6. Djojonegoro C-1000 PT

11.1.6.1. Business Description

11.1.6.2. Product Portfolio

11.1.6.3. Collaborations & Alliances

11.1.6.4. Recent Developments

11.1.6.5. Financial Details

11.1.6.6. Others

11.1.7. Sappe Plc Co Ltd

11.1.7.1. Business Description

11.1.7.2. Product Portfolio

11.1.7.3. Collaborations & Alliances

11.1.7.4. Recent Developments

11.1.7.5. Financial Details

11.1.7.6. Others

11.1.8. Heinz ABC Indonesia PT

11.1.8.1. Business Description

11.1.8.2. Product Portfolio

11.1.8.3. Collaborations & Alliances

11.1.8.4. Recent Developments

11.1.8.5. Financial Details

11.1.8.6. Others

11.1.9. Diamond Cold Storage PT

11.1.9.1. Business Description

11.1.9.2. Product Portfolio

11.1.9.3. Collaborations & Alliances

11.1.9.4. Recent Developments

11.1.9.5. Financial Details

11.1.9.6. Others

11.1.10. Tipco Foods Co Ltd

11.1.10.1.Business Description

11.1.10.2.Product Portfolio

11.1.10.3.Collaborations & Alliances

11.1.10.4.Recent Developments

11.1.10.5.Financial Details

11.1.10.6.Others

12. Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Category |

|

| By Nature |

|

| By Packaging Material |

|

| By Packaging Type |

|

| By Sales Channel |

|

| By Region |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.