India Juice Market Report: Trends, Growth and Forecast (2026-2032)

By Category (100% Juice (Not from Concentrate, Reconstituted), Juice Drinks (up to 24% Juice), Nectars (High Concentration (40% to 50% fruit content), Medium Concentration (30% to 39% fruit content), Low Concentration (25% to 29% fruit content)), Vegetable Juice, Fruit and Vegetable Blends), By Nature (Conventional, Organic), By Packaging Material (Plastic, Glass, Metal, Others), By Packaging Type (PET Bottles, Aseptic Packages (Cartons), Glass Bottles, Metal Cans, Disposable Cups & Pouches), By Sales Channel (Off-Trade (Hypermarkets/ Supermarkets, Retail Outlets, Convenience Stores, Online Platforms), On-Trade), By Region (North, East, West, South) ... Read more

|

Major Players

|

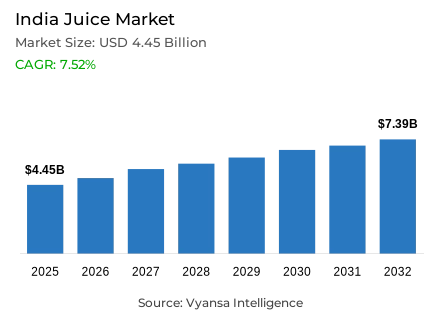

India Juice Market Statistics and Insights, 2026

- Market Size Statistics

- Juice market size in India was estimated at USD 4.45 billion in 2025.

- The market size is expected to grow to USD 7.39 billion by 2032.

- Market to register a CAGR of around 7.52% during 2026-32.

- Category Shares

- Juice drinks (up to 24% juice) grabbed market share of 60%.

- Competition

- More than 5 companies are actively engaged in producing juice in India.

- Top 5 companies acquired around 65% of the market share.

- ITC Foods Ltd, Tunip Agro Pvt Ltd, Rakyan Beverages Pvt Ltd, Coca-Cola India Pvt Ltd, PepsiCo India Holdings Pvt Ltd etc., are few of the top companies.

- Sales Channel

- Off-trade grabbed 65% of the market.

India Juice Market Outlook

The India juice market is at a stage of active growth, as the country has a high number of young people and an increasing focus on healthy consumption. The market is projected to grow to US 4.45 billion in 2025 and to US 7.39 billion in 2032, with a remarkable CAGR of about 7.52% in the 2026–32 period. This fast expansion is enabled by an abundant supply of local fruits and a per-capita consumption rate that is still far below the global average, which leaves much room to penetrate the market among Gen Z and Millennial generations.

In order to cope with the high inflation and increasing production prices, manufacturers are turning to low-unit packs as a pivot. The approach includes the launch of smaller and cheaper SKUs, including 65 ml or 200 ml at INR 5–20. These affordable price points are critical in attracting rural and urban end user who are more concerned with low-disbursement deals. Juice drinks (up to 24% juice) have been the backbone of the category in this competitive environment, with a market share of 60%.

The blurring of category lines is also becoming a source of innovation, as juice is becoming more and more a part of sports drinks, flavoured waters, and even carbonates. Whereas nectars are competing with a price war in the carbonate segment, 100% juice is successful with mini-cans and bottles that focus on natural immunity. The bottling partners of leading players like Dabur and Coca-Cola are actively increasing their production and distribution capacities to satisfy this growing demand in the country.

Juice distribution is mainly home and on-the-go consumption with off-trade channels taking 65% of the market. Traditional general trade stores to high-growth e-commerce platforms, brands are guaranteeing a high level of visibility to their smaller, low-cost formats. With the growth of disposable incomes and the empowerment of end user to make informed decisions by health-related labelling regulations, the Indian juice market will continue to be one of the most dynamic beverage segments up to 2032.

India Juice Market Growth Driver

Heat-Driven Hydration Needs Sustaining Demand for Single-Serve and Portable Juice Formats

The increasing temperature conditions maintain strong demand of quick, portable drinks, thus supporting the habitual intake of juice beverages. According to the India Meteorological Department, the average land-surface air temperature of India in 2025 is 0.28°C. According to the same release, the highest monthly mean temperature was recorded in February 2025 with an anomaly of 1.36°C and the highest temperature in the country.

This weather scenario increases the necessity of convenient hydration in heat waves, which is the shift of your portfolio towards smaller and more cost-effective packs. Low-unit-price formats are more conveniently available in distribution channels and occasions of use when end user are interested in instant refreshment and are price conscious. As a result, juice drinks remain relevant in the off-trade and on-trade contexts despite the increasing input prices and inflationary pressures that affect the buying behavior.

India Juice Market Challenge

Heightened Labelling and Claim Scrutiny Increasing Compliance and Consumer Trust Risks

Greater scrutiny of product claims poses an obvious challenge to juice manufacturers, especially those who are marketing themselves on the basis of health. In May 2025, the Food Safety and Standards Authority of India released an advisory that instructed food business operators not to use the term 100% on labels and promotional material because of the risk of misleading end user. This creates an increased compliance pressure in the packaging, advertising and portfolio communication particularly in reconstituted and sweetened versions.

The demand to be transparent is heightened by the fact that end user are increasingly sensitive to the risks associated with sugar. According to the World Health Organization, 2.5 billion adults were overweight and 890 million were obese in 2022, which explains why regulators and end user are paying closer attention to the messages of healthy beverages. Brands should invest in more transparent labelling and stricter claim management, or risk reputational harm and loss of shelf credibility.

Unlock Market Intelligence

Explore the market potential with our data-driven report

India Juice Market Trend

Affordability-First Purchasing Reshaping Pack-Size Mix Toward Lower Unit-Price Formats

Affordability is kept at the centre and the purchasing behaviour is changed to smaller packs which minimise cash out-lay per purchase. The trend is supported by the current cost-of-living pressures on basic goods. The Ministry of Statistics and Programme Implementation recorded year-on-year inflation of 3.60% in health, 3.38% in education and 2.95% in housing in November 2025. end user are more likely to demand lower unit prices in discretionary goods like packaged beverages when the normal household expenditures increase.

Consequently, brands are increasingly focusing on mini packs that can work in general trade, modern trade, and e-commerce without committing end user to greater expenditure obligations. This trend favors increased trial and broader penetration, and holds the category pegged to value-based formats in which margin management and packaging efficiency are paramount to profitability.

India Juice Market Opportunity

Expanding Digital and Quick-Commerce Reach Unlocking Omnichannel Scale for Juice Brands

India’s fast-rising digital access strengthens the route for juice brands to build scale through e-commerce and quick commerce, matching the channel expansion highlighted in the market dynamics. The Telecom Regulatory Authority of India reports that total broadband subscribers reach 1,003.65 million at the end of November 2025, rising from 999.81 million a month earlier. It also reports wireless subscribers at 1,187.48 million at the end of November 2025.

This connectivity enables grocery platforms to push wider assortments, targeted promotions, and faster replenishment for small packs that end user prefer under inflation pressure. Brands that design online-friendly packs and bundle strategies can improve availability beyond metros, while using digital channels to trial newer hybrids such as juice-based hydration drinks that sit between juice, flavoured water, and functional refreshment.

Unlock Market Intelligence

Explore the market potential with our data-driven report

India Juice Market Segmentation Analysis

By Category

- 100% Juice

- Not from Concentrate

- Reconstituted

- Juice Drinks (up to 24% Juice)

- Nectars

- High Concentration (40% to 50% fruit content)

- Medium Concentration (30% to 39% fruit content)

- Low Concentration (25% to 29% fruit content)

- Vegetable Juice

- Fruit and Vegetable Blends

The segment has the highest share around the category in the Indian juice market, where Juice Drinks (up to 24% Juice) grabbed a market share of 60%. This dominance is driven by the category’s superior affordability and the strategic move by manufacturers toward micro-packaging. By offering SKUs priced as low as INR 5 to INR 10, brands like Frooti have made juice drinks accessible to a vast population of price-sensitive end user in both rural and urban areas. This segment effectively bridges the gap between basic refreshment and the perceived health benefits of fruit.

While 100% juice and nectars are positioned as more premium options, juice drinks thrive due to their high penetration and popularity as a convenient, everyday beverage. The category is also benefiting from cross-category innovation, where juice is being blended into other soft drink formats to create flavorful, hydrating experiences. As the youthful demographic continues to enter the workforce, the accessibility and mass appeal of juice drinks are expected to sustain their leading market position through 2032.

By Sales Channel

- Off-Trade

- Hypermarkets/ Supermarkets

- Retail Outlets

- Convenience Stores

- Online Platforms

- On-Trade

The segment has the highest share around the Sales Channel is Off-Trade, which grabbed 65% of the market. This significant share is a result of juice being a staple for household consumption and a primary choice for on-the-go refreshment purchased through retail outlets. The general trade—composed of millions of small local grocers—remains the heartbeat of this channel, providing the hyper-local reach necessary for small, affordable pack sizes. Modern trade and e-commerce are also gaining ground by offering bulk deals and a wider variety of premium 100% juice options.

The dominance of off-trade sales is further supported by the merket's focus on low volume packs that align with the daily spending habits of local end user. While the on-trade sector in hotels and restaurants is growing, the convenience of purchasing a quick INR 10 pack from a neighborhood store ensures that off-trade remains the primary engine of the market. This robust retail infrastructure is crucial for brands to maintain visibility and compete effectively against other low-cost beverages like carbonates through 2032.

List of Companies Covered in India Juice Market

The companies listed below are highly influential in the India juice market, with a significant market share and a strong impact on industry developments.

- ITC Foods Ltd

- Tunip Agro Pvt Ltd

- Rakyan Beverages Pvt Ltd

- Coca-Cola India Pvt Ltd

- PepsiCo India Holdings Pvt Ltd

- Parle Agro Pvt Ltd

- Dabur India Ltd

Competitive Landscape

India juice market is led by established players such as Dabur, Coca-Cola, and PepsiCo-affiliated bottlers, which dominate through scale, distribution reach, and strong brand recall across juice drinks and nectars. Dabur remains strong in nectars but is strategically reallocating focus toward carbonates and coconut water due to intense price competition. Global soft drink majors indirectly pressure the juice category, as aggressive carbonate pricing—exemplified by Campa Cola’s deep discounts—has diverted budget-conscious consumers away from nectars. Smaller and regional brands compete primarily on affordability via ultra-small pack sizes priced at INR5–20, expanding penetration in both rural and urban markets. Key differentiation opportunities lie in low-sugar compliance-led formulations, hybrid beverages blending juice with hydration formats, and innovative value packs targeting India’s young, fast-growing consumer base.

Frequently Asked Questions

Related Report

1. Market Segmentation

1.1. Research Scope

1.2. Research Methodology

1.3. Definitions and Assumptions

2. Executive Summary

3. India Juice Market Policies, Regulations, and Standards

4. India Juice Market Dynamics

4.1. Growth Factors

4.2. Challenges

4.3. Trends

4.4. Opportunities

5. India Juice Market Statistics, 2022-2032F

5.1. Market Size & Growth Outlook

5.1.1.By Revenues in USD Million

5.1.2.By Quantity Sold in Million Litres

5.2. Market Segmentation & Growth Outlook

5.2.1.By Category

5.2.1.1. 100% Juice- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.1. Not from Concentrate- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.2. Reconstituted- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2. Juice Drinks (up to 24% Juice)- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3. Nectars- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3.1. High Concentration (40% to 50% fruit content)- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3.2. Medium Concentration (30% to 39% fruit content)- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3.3. Low Concentration (25% to 29% fruit content)- Market Insights and Forecast 2022-2032, USD Million

5.2.1.4. Vegetable Juice- Market Insights and Forecast 2022-2032, USD Million

5.2.1.5. Fruit and Vegetable Blends- Market Insights and Forecast 2022-2032, USD Million

5.2.2.By Nature

5.2.2.1. Conventional- Market Insights and Forecast 2022-2032, USD Million

5.2.2.2. Organic- Market Insights and Forecast 2022-2032, USD Million

5.2.3.By Packaging Material

5.2.3.1. Plastic- Market Insights and Forecast 2022-2032, USD Million

5.2.3.2. Glass- Market Insights and Forecast 2022-2032, USD Million

5.2.3.3. Metal- Market Insights and Forecast 2022-2032, USD Million

5.2.3.4. Others- Market Insights and Forecast 2022-2032, USD Million

5.2.4.By Packaging Type

5.2.4.1. PET Bottles- Market Insights and Forecast 2022-2032, USD Million

5.2.4.2. Aseptic Packages (Cartons)- Market Insights and Forecast 2022-2032, USD Million

5.2.4.3. Glass Bottles- Market Insights and Forecast 2022-2032, USD Million

5.2.4.4. Metal Cans- Market Insights and Forecast 2022-2032, USD Million

5.2.4.5. Disposable Cups & Pouches- Market Insights and Forecast 2022-2032, USD Million

5.2.5.By Sales Channel

5.2.5.1. Off-Trade- Market Insights and Forecast 2022-2032, USD Million

5.2.5.1.1. Hypermarkets/ Supermarkets - Market Insights and Forecast 2022-2032, USD Million

5.2.5.1.2. Retail Outlets - Market Insights and Forecast 2022-2032, USD Million

5.2.5.1.3. Convenience Stores- Market Insights and Forecast 2022-2032, USD Million

5.2.5.1.4. Online Platforms- Market Insights and Forecast 2022-2032, USD Million

5.2.5.2. On-Trade- Market Insights and Forecast 2022-2032, USD Million

5.2.6.By Region

5.2.6.1. North

5.2.6.2. East

5.2.6.3. West

5.2.6.4. South

5.2.7.By Competitors

5.2.7.1. Competition Characteristics

5.2.7.2. Market Share & Analysis

6. India 100% Juice Market Statistics, 2022-2032

6.1. Market Size & Growth Outlook

6.1.1.By Revenues in USD Million

6.1.2.By Quantity Sold in Million Litres

6.2. Market Segmentation & Growth Outlook

6.2.1.By Nature- Market Insights and Forecast 2022-2032, USD Million

6.2.2.By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

6.2.3.By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

6.2.4.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

6.2.5.By Region- Market Insights and Forecast 2022-2032, USD Million

7. India Juice Drinks (up to 24% Juice) Market Statistics, 2022-2032

7.1. Market Size & Growth Outlook

7.1.1.By Revenues in USD Million

7.1.2.By Quantity Sold in Million Litres

7.2. Market Segmentation & Growth Outlook

7.2.1.By Nature- Market Insights and Forecast 2022-2032, USD Million

7.2.2.By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

7.2.3.By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

7.2.4.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

7.2.5.By Region- Market Insights and Forecast 2022-2032, USD Million

8. India Nectars Market Statistics, 2022-2032

8.1. Market Size & Growth Outlook

8.1.1.By Revenues in USD Million

8.1.2.By Quantity Sold in Million Litres

8.2. Market Segmentation & Growth Outlook

8.2.1.By Nature- Market Insights and Forecast 2022-2032, USD Million

8.2.2.By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

8.2.3.By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

8.2.4.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

8.2.5.By Region- Market Insights and Forecast 2022-2032, USD Million

9. India Vegetable Juice Market Statistics, 2022-2032

9.1. Market Size & Growth Outlook

9.1.1.By Revenues in USD Million

9.1.2.By Quantity Sold in Million Litres

9.2. Market Segmentation & Growth Outlook

9.2.1.By Nature- Market Insights and Forecast 2022-2032, USD Million

9.2.2.By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

9.2.3.By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

9.2.4.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

9.2.5.By Region- Market Insights and Forecast 2022-2032, USD Million

10. India Fruit and Vegetable Blends Market Statistics, 2022-2032

10.1. Market Size & Growth Outlook

10.1.1. By Revenues in USD Million

10.1.2. By Quantity Sold in Million Litres

10.2. Market Segmentation & Growth Outlook

10.2.1. By Nature- Market Insights and Forecast 2022-2032, USD Million

10.2.2. By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

10.2.3. By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

10.2.4. By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

10.2.5. By Region- Market Insights and Forecast 2022-2032, USD Million

11. Competitive Outlook

11.1. Company Profiles

11.1.1. Coca-Cola India Pvt Ltd

11.1.1.1. Business Description

11.1.1.2. Product Portfolio

11.1.1.3. Collaborations & Alliances

11.1.1.4. Recent Developments

11.1.1.5. Financial Details

11.1.1.6. Others

11.1.2. PepsiCo India Holdings Pvt Ltd

11.1.2.1. Business Description

11.1.2.2. Product Portfolio

11.1.2.3. Collaborations & Alliances

11.1.2.4. Recent Developments

11.1.2.5. Financial Details

11.1.2.6. Others

11.1.3. Parle Agro Pvt Ltd

11.1.3.1. Business Description

11.1.3.2. Product Portfolio

11.1.3.3. Collaborations & Alliances

11.1.3.4. Recent Developments

11.1.3.5. Financial Details

11.1.3.6. Others

11.1.4. Dabur India Ltd

11.1.4.1. Business Description

11.1.4.2. Product Portfolio

11.1.4.3. Collaborations & Alliances

11.1.4.4. Recent Developments

11.1.4.5. Financial Details

11.1.4.6. Others

11.1.5. Rakyan Beverages Pvt Ltd

11.1.5.1. Business Description

11.1.5.2. Product Portfolio

11.1.5.3. Collaborations & Alliances

11.1.5.4. Recent Developments

11.1.5.5. Financial Details

11.1.5.6. Others

11.1.6. ITC Foods Ltd

11.1.6.1. Business Description

11.1.6.2. Product Portfolio

11.1.6.3. Collaborations & Alliances

11.1.6.4. Recent Developments

11.1.6.5. Financial Details

11.1.6.6. Others

11.1.7. Tunip Agro Pvt Ltd

11.1.7.1. Business Description

11.1.7.2. Product Portfolio

11.1.7.3. Collaborations & Alliances

11.1.7.4. Recent Developments

11.1.7.5. Financial Details

11.1.7.6. Others

12. Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Category |

|

| By Nature |

|

| By Packaging Material |

|

| By Packaging Type |

|

| By Sales Channel |

|

| By Region |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.