India Electric Motorcycle Market Report: Trends, Growth and Forecast (2026-2032)

By Battery Type (Lithium-Ion Battery, Lead Acid Battery, Solid-State Battery, Others), By Battery Capacity (Upto 2 kWh, 2–4 kWh, 4–6 kWh, Above 6 kWh), By Range (Upto 100 km, 101–150 km, 151–200 km, Above 200 km), By Speed (Upto 50 km/h, 51–80 km/h, 81–120 km/h, Above 120 km/h), By Power Output (Upto 3 kW, 3–6 kW, 6–10 kW, Above 10 kW), By Charging Type (Normal Charging, Fast Charging, Battery Swapping), By End User (Personal Users, Commercial Users), By Application (Daily Commuting, Sports & Performance Riding, Last-Mile Delivery, Fleet Mobility, Adventure & Off-Road Riding), By Region (North, East, West, South) ... Read more

|

Major Players

|

India Electric Motorcycle Market Statistics and Insights, 2026

- Market Size Statistics

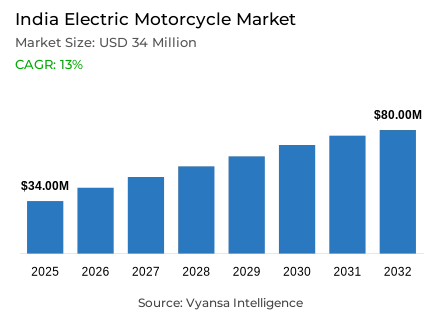

- Electric motorcycle market size in India was valued at USD 34 million in 2025 and is estimated at USD 38 million in 2026.

- The market size is expected to grow to USD 80 million by 2032.

- Market to register a CAGR of around 13% during 2026-32.

- Battery Type Shares

- Lithium-ion battery grabbed market share of 90%.

- Competition

- More than 10 companies are actively engaged in producing electric motorcycle in India.

- Top 5 companies acquired around 70% of the market share.

- Ola Electric, Komaki Electric, Joy e-bike, Revolt Motors, Ultraviolette Automotive etc., are few of the top companies.

- Application

- Daily commuting grabbed 55% of the market.

India Electric Motorcycle Market Outlook

The India electric motorcycle market was valued at USD 34 million in 2025 and is projected to advance from USD 38 million in 2026 to USD 80 million by 2032, registering a CAGR of 13% across the forecast period. This sustained and policy-reinforced expansion reflects a commercially deepening growth environment within the India electric motorcycle market, where rising fuel-cost sensitivity, urban commuting necessity, battery technology improvement, and a nationally coordinated electric mobility incentive framework are collectively elevating electric motorcycles from a small early-adoption segment toward a more commercially visible and consumer-accessible sub-category within India's vast two-wheeler ecosystem. Growth is anchored not in speculative enthusiasm but in the demonstrated and accelerating adoption of electric commuter bikes across daily-use rider segments whose economic calculus increasingly favours lower running costs over the familiarity of petrol alternatives.

India's broader two-wheeler electrification momentum provides the market with a structurally supportive demand foundation. As per data published by the Press Information Bureau, electric two-wheeler sales reached 11,49,334 units in FY2024-25, rising 21% from 9,48,561 units in FY2023-24, confirming that consumer acceptance of electric mobility across the two-wheeler category is expanding at a commercially meaningful pace that progressively normalises lithium-ion battery ownership, charging behaviour, and low-maintenance electric drivetrains across the rider population most likely to consider electric motorcycles for daily commuting as a practical next step beyond scooter adoption.

Lithium-ion battery electric motorcycles command approximately 90% of the battery type segment within the India electric motorcycle market, anchored in the technical requirements of motorcycle performance where higher energy density, lower pack weight, stronger discharge capability, faster charging compatibility, and superior thermal management are non-negotiable baseline specifications for delivering the acceleration, top speed, and usable daily range that competitive motorcycle buyers expect. The PM E-DRIVE Scheme reinforces this technology concentration by restricting demand incentives exclusively to electric two-wheelers equipped with advanced batteries, creating a structurally clear commercial advantage for lithium-ion platform investment across every manufacturer seeking subsidy-eligible product positioning within India's national electric mobility programme.

electric motorcycles for daily commuting lead the application segment with approximately 55% share, reflecting the practical and recurring nature of India's urban two-wheeler usage culture where office travel, college mobility, local errands, and short-distance city riding represent the most scalable and volume-generating adoption pathway for the India electric motorcycle market. As per data published by NITI Aayog via the Press Information Bureau, India's EV sales reached 2.08 million in 2024 with total EV stock at 5.45 million, while India's stated ambition of achieving a 30% EV share in total vehicle sales by 2030 confirms that electric motorcycles are expanding within a nationally mandated electrification trajectory that provides sustained commercial tailwind through the forecast period.

India Electric Motorcycle Market Growth Driver

Policy-Backed Incentives and Domestic Manufacturing Investment Are Creating a Structurally Reinforced Demand Foundation

Government incentive architecture is the most commercially significant demand driver within the India electric motorcycle market, directly reducing the purchase-price barrier that has historically constrained conversion from petrol to electric platforms across India's cost-sensitive commuter motorcycle buyer base. As per data published by the Press Information Bureau, the PM E-DRIVE Scheme carries a financial outlay of INR 10,900 crore effective from October 2024 to March 2026, targeting incentivisation of approximately 24.79 lakh electric two-wheelers equipped with advanced batteries, while the PLI-Auto Scheme with a budgetary outlay of INR 25,938 crore had achieved cumulative investment of INR 35,657 crore and determined sales of INR 32,879 crore by September 2025, collectively building both consumer affordability and domestic manufacturing depth for advanced battery electric motorcycles simultaneously.

Charging infrastructure limitations and battery cost sensitivity are simultaneously creating the most commercially consequential adoption challenge within the India electric motorcycle market, as the 29,151 EV charging stations installed across India by December 2025 including 8,805 fast chargers remain insufficient to support the flexible long-distance riding expectations that distinguish motorcycle buyers from scooter-oriented consumers. The most durable commercial opportunity within this environment lies in electric motorcycles for last-mile delivery and urban commuter fleet electrification, where predictable daily routes, depot-based charging access, and measurable fuel-cost savings collectively create the most commercially self-sustaining adoption path, supported by the PM E-DRIVE framework's INR 2,000 crore allocation for pan-India EV charging infrastructure that is progressively expanding the deployable addressable market throughout the forecast period.

India Electric Motorcycle Market Challenge

Charging Infrastructure Gaps and Battery Cost Sensitivity Constrain Broader Market Penetration

The most commercially consequential structural challenge within the India electric motorcycle market is the persistent inadequacy of public charging infrastructure relative to the flexible travel expectations of motorcycle buyers who compare electric ownership against the near-instant refuelling convenience of petrol alternatives. Based on data from the Press Information Bureau, India had 29,151 EV charging stations installed across states and union territories by December 2025, comprising 8,805 fast chargers and 20,346 slow chargers, a base that reflects meaningful progress under FAME-I, FAME-II, and PM E-DRIVE but remains insufficient to eliminate range anxiety concerns among performance-oriented and long-distance motorcycle riders whose adoption decisions are more sensitive to charging convenience than those of typical urban scooter commuters with predictable short daily routes.

Battery replacement cost, thermal safety concerns, warranty coverage adequacy, and real-world range performance under Indian high-temperature and high-traffic conditions compound this infrastructure challenge by raising the total-cost-of-ownership scrutiny that electric motorcycle purchases attract from commuter buyers accustomed to the lower upfront cost and wider service availability of petrol alternatives. As indicated by authoritative sources at NITI Aayog, India targets a 30% EV share in total vehicle sales by 2030 even as EV stock reached only 5.45 million against a vastly larger overall vehicle base in 2024, confirming that battery warranty issues, service network limitations, and high upfront cost of electric motorcycles remain structurally significant adoption barriers that manufacturers must resolve through stronger warranty programmes, certified service networks, and locally optimised battery thermal management before the India electric motorcycle market can scale meaningfully beyond its current early-adopter and daily-commuter core.

Unlock Market Intelligence

Explore the market potential with our data-driven report

India Electric Motorcycle Market Trend

Advanced Battery Platforms and Performance-Oriented Architectures Are Reshaping electric motorcycle Product Standards

A well-defined and commercially consequential structural trend is reshaping product development priorities across the India electric motorcycle market, as the combination of PM E-DRIVE's advanced battery eligibility requirements and the ACC PLI scheme's 50 GWh domestic advanced chemistry cell manufacturing target progressively elevates the technical specification standard for electric motorcycle battery systems beyond basic electrification toward integrated platform architectures combining permanent magnet motor systems, regenerative braking, digital instrument clusters, ride modes, mobile connectivity, and battery management system diagnostics. As per data published by the Press Information Bureau, the ACC PLI scheme had awarded 40 GWh of its 50 GWh target to four beneficiary firms with cumulative investment of INR 3,237 crore and 1,118 jobs achieved by December 2025, directly strengthening the domestic cell and pack ecosystem that reduces import dependence and supports battery system customisation for Indian road, heat, and charging conditions.

The trend is simultaneously reshaping aftersales and service models across the India electric motorcycle market in ways that are creating durable competitive differentiation between manufacturers capable of delivering full lifecycle battery support and those offering only basic vehicle transactions. In line with findings from the IEA's Global EV Outlook, electric two- and three-wheelers remained the most electrified road transport segment globally in 2024 with more than 9% of the global fleet already electric and total electric model sales reaching 10 million units, confirming that India's smart connected electric motorcycle and software-defined electric motorcycles development trajectory is advancing within a globally validated technology pathway where battery diagnostics, warranty management, thermal monitoring, and over-the-air software updates are becoming standard competitive requirements rather than premium differentiators throughout the forecast period.

India Electric Motorcycle Market Opportunity

Commuter Electrification and Fleet Mobility Create the Largest and Most Scalable Demand Pools

The most commercially significant and structurally recurring growth opportunity within the India electric motorcycle market lies in the daily commuting application segment, which already commands 55% of market share and represents the most volume-generating and economically self-reinforcing adoption pathway available to electric motorcycle manufacturers targeting India's vast urban and semi-urban rider base. As per official figures from the Press Information Bureau, PM E-DRIVE targets incentivisation of approximately 24.79 lakh electric two-wheelers with its INR 10,900 crore outlay, while electric two-wheeler sales grew 21% to 11,49,334 units in FY2024-25, collectively confirming that the commuter rider base generating electric motorcycles for urban mobility demand is both commercially large and actively expanding across the Tier 1 and Tier 2 city corridors where charging access, dealer service depth, and lithium-ion battery familiarity are most reliably available.

The fleet and delivery mobility dimension of this opportunity independently creates a separately significant and high-utilisation demand layer that is structurally insulated from the individual consumer adoption hesitancy driven by battery cost and charging access concerns. Data compiled from internationally recognised public authorities at NITI Aayog confirms that India's total EV stock reached 5.45 million by 2024 within a broader ambition of achieving 30% EV share in total vehicle sales by 2030, while delivery workers, field executives, service technicians, and electric motorcycles for courier services operators represent a commercially distinct buyer segment whose predictable daily routes, depot-charging access, and measurable fuel-saving economics make them structurally more conversion-ready than general consumer buyers, creating a durable and recurring commercial opportunity for manufacturers offering long-range electric motorcycles India with strong battery warranties, fleet telematics integration, and service network depth throughout the forecast period.

Unlock Market Intelligence

Explore the market potential with our data-driven report

India Electric Motorcycle Market Segmentation Analysis

By Battery Type

- Lithium-Ion Battery

- Lead Acid Battery

- Solid-State Battery

- Others

Lithium-Ion Battery commands the highest share within the battery type category at approximately 90%, reflecting the consistent and technically non-negotiable preference among electric motorcycle manufacturers and buyers within the India electric motorcycle market for battery systems that deliver the higher energy density, lower vehicle weight, stronger discharge performance, and superior cycle life that motorcycle-grade acceleration, speed, and daily range requirements demand over sealed lead-acid or older nickel-based alternatives. The segment's overwhelming dominance is further institutionally reinforced by PM E-DRIVE's policy design restricting demand incentives exclusively to advanced battery electric motorcycles, creating a structurally clear and commercially durable advantage for lithium-ion platform investment across every manufacturer seeking subsidy-eligible product qualification within India's national electric mobility programme.

The segment's commercial depth within the India electric motorcycle market is further strengthened by the growing domestic battery manufacturing ecosystem that the ACC PLI scheme is systematically building across the country. Evidence drawn from public data released by the Press Information Bureau confirms that India's ACC PLI scheme has awarded 40 GWh of domestic advanced chemistry cell manufacturing capacity to four firms with INR 3,237 crore investment achieved by December 2025, directly building the local cell supply, thermal management expertise, and pack engineering depth that allows high-capacity electric motorcycles manufacturers to design battery systems specifically optimised for India's high-temperature operating conditions, varied charging behaviours, and cost-sensitive total-ownership economics throughout the forecast period.

By Application

- Daily Commuting

- Sports & Performance Riding

- Last-Mile Delivery

- Fleet Mobility

- Adventure & Off-Road Riding

Daily Commuting commands the highest share within the application category at approximately 55%, establishing routine urban and semi-urban mobility as the most commercially significant and volume-generating demand context within the India electric motorcycle market. Riders using electric motorcycles for daily office travel, college commuting, local business movement, and household errands consistently generate the most predictable, high-frequency, and charging-compatible usage patterns that make electric motorcycle ownership economically compelling, creating a commercial demand base directly tied to the recurring cost-saving calculus of reduced fuel expenditure and lower maintenance obligations that electric motorcycles for urban mobility deliver over petrol equivalents across India's cost-sensitive commuter rider population.

The segment's structural durability is reinforced by both the scale of India's electric two-wheeler adoption momentum and the expanding policy support environment that is progressively improving commuter-focused product affordability and charging access. As per data published by the Press Information Bureau, electric two-wheeler sales grew 21% to 11,49,334 units in FY2024-25, while NITI Aayog confirms India's EV stock reached 5.45 million with a 30% EV sales share target by 2030, collectively confirming that the commuter rider base driving demand within the India electric motorcycle market is both commercially large and structurally expanding across the urban and semi-urban corridors where fast charging electric motorcycle infrastructure, service network depth, and lithium-ion battery reliability are most reliably available throughout the forecast period.

List of Companies Covered in India Electric Motorcycle Market

The companies listed below are highly influential in the India electric motorcycle market, with a significant market share and a strong impact on industry developments.

- Ola Electric

- Komaki Electric

- Joy e-bike

- Revolt Motors

- Ultraviolette Automotive

- Tork Motors

- Oben Electric

- Matter Motor Works

- Hop Electric Mobility

- Odysse Electric

Market News & Updates

- Ola Electric, 2025:

Ola Electric introduced the Roadster X motorcycle range in 2025 and listed Roadster X and Roadster X+ under its motorcycle portfolio. The Roadster X+ offers up to 500 km IDC range, 125 kmph top speed, 11 kW peak power, and 9.1 kWh or 4.5 kWh battery options. The launch expands Ola’s electric two-wheeler portfolio into motorcycles.

- Revolt Motors, 2025:

Revolt Motors launched the RV BlazeX electric motorcycle in February 2025. The model is listed as “The All New Revolt RV BlazeX electric bike” with pricing from ₹1,19,990 and booking support through Revolt’s official platform. The launch adds a new commuter-focused electric motorcycle to Revolt’s India portfolio.

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- India Electric Motorcycle Market Policies, Regulations, and Standards

- India Electric Motorcycle Production (Unit) Trend 2022-2032

- India Electric Motorcycle Production (Unit) Trend By Battery Type

- Lithium-Ion Battery

- Lead Acid Battery

- Solid-State Battery

- Company Wise Production Plants and Statistics

- Installed Production Capacity

- Actual Production

- Planned Production Target

- India Electric Motorcycle Production (Unit) Trend By Battery Type

- India Electric Motorcycle Pricing Analysis 2022-2032

- India Electric Motorcycle Pricing Trend (USD/Unit) 2022-2032

- India Electric Motorcycle Pricing Trend (USD/Unit) By Regions 2022-2032

- North

- East

- West

- South

- India Electric Motorcycle Pricing Trend (USD/Unit) By Battery Type 2022-2032

- Lithium-Ion Battery

- Lead Acid Battery

- Solid-State Battery

- India Electric Motorcycle Pricing Analysis 2022-2032

- India Electric Motorcycle Pricing Trend (USD/Unit) 2022-2032

- India Electric Motorcycle Pricing Trend (USD/Unit) By Regions 2022-2032

- North

- East

- West

- South

- India Electric Motorcycle Pricing Trend (USD/Unit) By Battery Type 2022-2032

- Lithium-Ion Battery

- Lead Acid Battery

- Solid-State Battery

- India Electric Motorcycle Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- India Electric Motorcycle Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Units Sold (Thousand Units)

- Market Segmentation & Growth Outlook

- By Battery Type

- Lithium-Ion Battery- Market Insights and Forecast 2022-2032, USD Million

- Lead Acid Battery- Market Insights and Forecast 2022-2032, USD Million

- Solid-State Battery- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By Battery Capacity

- Upto 2 kWh- Market Insights and Forecast 2022-2032, USD Million

- 2–4 kWh- Market Insights and Forecast 2022-2032, USD Million

- 4–6 kWh- Market Insights and Forecast 2022-2032, USD Million

- Above 6 kWh- Market Insights and Forecast 2022-2032, USD Million

- By Range

- Upto 100 km- Market Insights and Forecast 2022-2032, USD Million

- 101–150 km- Market Insights and Forecast 2022-2032, USD Million

- 151–200 km- Market Insights and Forecast 2022-2032, USD Million

- Above 200 km- Market Insights and Forecast 2022-2032, USD Million

- By Speed

- Upto 50 km/h- Market Insights and Forecast 2022-2032, USD Million

- 51–80 km/h- Market Insights and Forecast 2022-2032, USD Million

- 81–120 km/h- Market Insights and Forecast 2022-2032, USD Million

- Above 120 km/h- Market Insights and Forecast 2022-2032, USD Million

- By Power Output

- Upto 3 kW- Market Insights and Forecast 2022-2032, USD Million

- 3–6 kW- Market Insights and Forecast 2022-2032, USD Million

- 6–10 kW- Market Insights and Forecast 2022-2032, USD Million

- Above 10 kW- Market Insights and Forecast 2022-2032, USD Million

- By Charging Type

- Normal Charging- Market Insights and Forecast 2022-2032, USD Million

- Fast Charging- Market Insights and Forecast 2022-2032, USD Million

- Battery Swapping- Market Insights and Forecast 2022-2032, USD Million

- By End User

- Personal Users- Market Insights and Forecast 2022-2032, USD Million

- Commercial Users- Market Insights and Forecast 2022-2032, USD Million

- By Application

- Daily Commuting- Market Insights and Forecast 2022-2032, USD Million

- Sports & Performance Riding- Market Insights and Forecast 2022-2032, USD Million

- Last-Mile Delivery- Market Insights and Forecast 2022-2032, USD Million

- Fleet Mobility- Market Insights and Forecast 2022-2032, USD Million

- Adventure & Off-Road Riding- Market Insights and Forecast 2022-2032, USD Million

- By Region

- North- Market Insights and Forecast 2022-2032, USD Million

- East- Market Insights and Forecast 2022-2032, USD Million

- West- Market Insights and Forecast 2022-2032, USD Million

- South- Market Insights and Forecast 2022-2032, USD Million

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Battery Type

- Market Size & Growth Outlook

- India Lithium-Ion Battery Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Units Sold (Thousand Units)

- Market Segmentation & Growth Outlook

- By Battery Capacity- Market Insights and Forecast 2022-2032, USD Million

- By Range- Market Insights and Forecast 2022-2032, USD Million

- By Speed- Market Insights and Forecast 2022-2032, USD Million

- By Power Output- Market Insights and Forecast 2022-2032, USD Million

- By Charging Type- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- India Lead Acid Battery Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Units Sold (Thousand Units)

- Market Segmentation & Growth Outlook

- By Battery Capacity- Market Insights and Forecast 2022-2032, USD Million

- By Range- Market Insights and Forecast 2022-2032, USD Million

- By Speed- Market Insights and Forecast 2022-2032, USD Million

- By Power Output- Market Insights and Forecast 2022-2032, USD Million

- By Charging Type- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- India Solid-State Battery Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Units Sold (Thousand Units)

- Market Segmentation & Growth Outlook

- By Battery Capacity- Market Insights and Forecast 2022-2032, USD Million

- By Range- Market Insights and Forecast 2022-2032, USD Million

- By Speed- Market Insights and Forecast 2022-2032, USD Million

- By Power Output- Market Insights and Forecast 2022-2032, USD Million

- By Charging Type- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- Revolt Motors

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Ultraviolette Automotive

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Tork Motors

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Oben Electric

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Matter Motor Works

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Ola Electric

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Komaki Electric

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Joy e-bike

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Hop Electric Mobility

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Odysse Electric

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Revolt Motors

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Battery Type |

|

| By Battery Capacity |

|

| By Range |

|

| By Speed |

|

| By Power Output |

|

| By Charging Type |

|

| By End User |

|

| By Application |

|

| By Region |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.