Global Automotive Brake Components Market Report: Trends, Growth and Forecast (2026-2032)

By Vehicle Type (Medium and Heavy Commercial Vehicles, Light Commercial Vehicles, Passenger Cars, Others), By Sales Channel (OEMs, Aftermarket), By Product Type (Brake Caliper, Floating Caliper, Fixed Caliper, Brake Pad, Metal, Ceramic, Organic, Brake Rotor, Brake Shoe, Brake Line), By Region (North America, South America, Europe, Middle East & Africa, Asia Pacific) ... Read more

|

Major Players

|

Global Automotive Brake Components Market Statistics and Insights, 2026

- Market Size Statistics

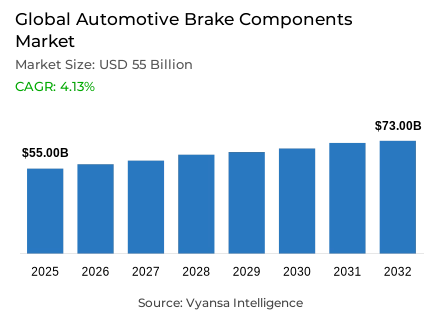

- Automotive brake components market size in Global was valued at USD 55 billion in 2025 and is estimated at USD 57.27 billion in 2026.

- The market size is expected to grow to USD 73 billion by 2032.

- Market to register a CAGR of around 4.13% during 2026-32.

- Product Type Shares

- Brake pad grabbed market share of 30%.

- Competition

- More than 10 companies are actively engaged in producing automotive brake components.

- Top 5 companies acquired the maximum share of the market.

- Robert Bosch GmbH, Aisin Seiko Co. Ltd., Valeo SA, Nisshinbo Holdings, Hitachi Automotive Systems Limited etc., are few of the top companies.

- Vehicle Type

- Passenger cars grabbed 55% of the market.

- Region

- Asia Pacific leads with a 50% share of the global market.

Global Automotive Brake Components Market Outlook

The Global automotive brake components market was valued at USD 55 billion in 2025 and is projected to advance from USD 57.27 billion in 2026 to USD 73 billion by 2032, registering a CAGR of 4.13% across the forecast period. This steady and safety-system-anchored expansion reflects a commercially dependable growth environment within the Global automotive brake components market, where rising vehicle assembly output, growing regulatory emphasis on active safety architecture, and the continuing centrality of braking performance across both original equipment fitment and aftermarket replacement channels are collectively sustaining consistent and broadly distributed demand for brake pad market, brake caliper market, disc, drum, shoe, cylinder, hose, booster, and fluid-management components across every major vehicle class and production geography worldwide. As per data published by OICA, global vehicle production increased from 92.7 million units in 2024 to 96.4 million units in 2025, while global vehicle sales rose from 95.3 million to 99.8 million units, confirming that the production base sustaining automotive brake components market consumption is both large and commercially expanding.

Brake Pad formats command the leading product type share at approximately 30% within the automotive brake components market, reflecting the consistent and broadly distributed OEM and aftermarket preference for friction brake components that sit at the primary contact point in disc braking systems and deliver stopping performance, wear-cycle management, and friction control across the highest-volume passenger car, SUV, and light commercial vehicle platforms globally. As vehicle safety content requirements intensify and brake dust emission compliance obligations elevate formulation and validation investment across the supplier base, the brake pad segment's centrality to both original equipment supply and aftermarket brake components replacement demand is structurally reinforcing its commercial leadership position across the full vehicle lifecycle.

Passenger Cars hold approximately 55% share within the vehicle type segment of the automotive braking system market, anchored in the structural reality that sedans, hatchbacks, SUVs, crossovers, and electric passenger vehicles represent the highest-volume production and service category requiring complete disc brake components and drum brake components assemblies including pads or shoes, rotors or drums, calipers or cylinders, lines, and support hardware across both new vehicle fitment and recurring maintenance replacement cycles. The electric vehicle dimension of this segment is deepening as regenerative braking strategies alter wear patterns and system layout requirements, progressively elevating demand for corrosion-resistant brake components, low-dust brake materials, and brake-by-wire compatible caliper and actuation architectures across next-generation passenger car platforms.

The Asia-Pacific automotive brake components market anchors global demand with approximately 50% of total market share, supported by a vehicle manufacturing base that OICA confirms rose 7.6% to approximately 59.2 million vehicles in 2025, accounting for more than 61% of global production output. This regional concentration makes Asia Pacific the most commercially significant geography for brake pad, rotor, caliper, drum, shoe, and actuation component procurement and supply, with China, India, Japan, South Korea, and Southeast Asia collectively sustaining the production volumes, OEM relationships, and supplier ecosystem depth that define the automotive brake components market's geographic centre of gravity through the forecast period.

Global Automotive Brake Components Market Growth Driver

Rising Global Vehicle Production and Safety Content Integration

Rising global vehicle output establishes sustained demand for automotive brake components throughout vehicle manufacturing systems. Statistics from OICA confirm global vehicle production reaches 96.4 million units in 2025, up from 92.7 million in 2024, with global sales rising to 99.8 million units. This production expansion directly translates into heightened market relevance for brake components supporting diverse vehicle applications. Growing vehicle output ensures persistent demand for professional brake component infrastructure supporting disc, drum, pad, shoe, caliper, cylinder, hose, and fluid-management parts throughout extended forecast period.

Safety regulation evolution and automated emergency braking requirements strengthen commercial foundation for expanded brake component deployment. Published evidence from European Commission indicates General Safety Regulation phase two implementation in July 2024 requires automated emergency braking features for all new vehicles, expanding braking system scope beyond stopping power. This regulatory expansion creates market opportunity for brake component suppliers developing integrated systems supporting broader safety architecture. Safety regulation momentum ensures sustained component demand supporting enhanced vehicle protection capabilities throughout global automotive systems.

Global Automotive Brake Components Market Challenge

Brake Dust Emission Compliance and Non-Exhaust Particulate Matter Control

Global automotive brake components market faces substantial challenge from tightening non-exhaust emission regulations affecting brake-part design and material formulation. Official records from European Environment Agency indicate overall particulate matter emissions from transport activity fall 53% from 1990 to 2023, while non-exhaust emissions from road transport rise 63.1% establishing increased brake-wear emission focus. This emission concern creates practical operational constraints for brake component manufacturers. Service providers must develop compliant friction-material solutions managing particulate matter emissions.

Regulatory compliance burden and material reformulation pressure intensify operating complexity for brake component manufacturers. Evidence from UNECE's 2026 brake-emissions text reveals PM10 brake-particle limits of 3 mg/km for pure electric light vehicles and 7 mg/km for other passenger-vehicle powertrains while European Commission's 2025 automotive review includes brake and tire emission limits under Euro 7. This regulatory complexity raises compliance cost for pads, discs, coatings, and validation programs. Component manufacturers must develop solutions incorporating low-dust friction materials and emissions-compliant designs supporting regulatory alignment throughout global automotive brake components market.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Global Automotive Brake Components Market Trend

Electrification-Driven Brake System Redesign and Low-Dust Component Development

Global automotive brake components market demonstrates pronounced shift toward electrification-driven brake system redesign emphasizing regenerative braking integration and low-dust friction materials. Market data from International Energy Agency reveals global electric car sales exceed 17 million in 2024 accounting for more than 20% of new car sales, with China selling more than 11 million electric vehicles. This EV momentum directly supports market expansion for braking systems designed for quiet operation, corrosion resistance, and regenerative braking compatibility. Published evidence establishes industry shift toward EV-specific braking hardware and soft-wear friction materials addressing electric vehicle operational characteristics.

Regulation alignment and technology integration strengthen industry-wide adoption of electrification-compatible brake solutions. Published data from UNECE indicates UN Regulation No. 179 explicitly accounts for electrified powertrains establishing first global brake-emission rule supporting EV requirements. This regulatory clarity supports market expansion for low-dust friction materials, coated rotors, optimized calipers, and system layouts supporting software-controlled blended braking. Service providers developing EV-compatible brake components incorporating low-dust formulations and corrosion-resistant materials position themselves advantageously capturing growth opportunities throughout global automotive brake components market.

Global Automotive Brake Components Market Opportunity

Asia-Based Localization and Electric Vehicle Component Manufacturing

Strong opportunities emerge in Asia-based localization supporting automotive brake component manufacturing closer to assembly plants and dealer networks. Official records from OICA reveal China adds roughly 3.25 million vehicles in 2025 reaching 34.53 million units produced with new-energy vehicle production reaching 16.626 million, up 29%. This substantial regional production creates commercial opportunity for localized manufacturing of pads, discs, drums, calipers, boosters, and replacement kits reducing delivery times and freight costs. Asia-based localization directly enables accelerated component adoption supporting regional supply chain efficiency.

Regional production concentration and EV manufacturing expansion strengthen commercial foundation for automotive brake components deployment. Evidence from OICA indicates India rising to 6.49 million vehicles produced while Japan remains at 8.41 million units, establishing substantial regional production base. This production scale creates market opportunity for suppliers developing localized manufacturing supporting faster model change response and competitive cost positioning. Asia's concentration of passenger-car and new-energy vehicle volumes ensures sustained demand for brake component localization supporting improved supply chain efficiency throughout extended forecast period.

Global Automotive Brake Components Market Regional Analysis

By Region

- North America

- South America

- Europe

- Middle East & Africa

- Asia Pacific

Asia Pacific emerges as leading regional market with 50% share within global automotive brake components market, reflecting region's dominant vehicle production base and component manufacturing ecosystem. Official records from OICA reveal production in Asia-Pacific rises 7.6% to approximately 59.2 million vehicles in 2025 accounting for more than 61% of global output, with sales across Asia, Oceania and Middle East increasing to 55.02 million units lifting region's share above 55%. This substantial production concentration directly supports heightened market relevance for brake components throughout region. Asia Pacific's vehicle production dominance ensures continued regional market leadership.

Regional manufacturing ecosystem and EV concentration strengthen commercial foundation for Asia Pacific brake components market dominance. Published evidence from OICA establishes region combines mass passenger-car production, strong component ecosystems, and fast-moving EV manufacturing supporting substantial brake component demand. This regional concentration creates sustained market opportunity for global brake component suppliers serving established and emerging vehicle platforms. Service providers developing Asia Pacific localization strategies supporting cost control and next-generation friction-material development position themselves advantageously capturing regional leadership throughout global automotive brake components market.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Global Automotive Brake Components Market Segmentation Analysis

By Product Type

- Brake Caliper

- Floating Caliper

- Fixed Caliper

- Brake Pad

- Metal

- Ceramic

- Organic

- Brake Rotor

- Brake Shoe

- Brake Line

Brake Pad commands the highest share within the product type category at approximately 30%, reflecting the consistent and structurally embedded demand for automotive friction brake components that sit at the primary contact point in disc braking systems and sustain stopping performance, wear-cycle management, and friction control across the highest-volume passenger car, SUV, and commercial vehicle platforms within the Global automotive brake components market. OEMs and aftermarket buyers consistently prioritise brake pad procurement because pads represent the most frequently replaced brake component across the vehicle lifecycle, creating a recurring and high-frequency demand pattern across both OEM brake components fitment programmes and aftermarket brake replacement parts distribution channels that no other brake component category currently matches in volume or replacement regularity.

The segment's commercial durability is further reinforced by the regulatory visibility that brake pad formulation is attracting across major markets. Evidence drawn from public data released by the European Environment Agency confirms that standardised brake-emissions measurement now supports direct comparison of replacement brake components, while UNECE's 2026 framework specifically covers laboratory emission measurement from non-original replacement pads and drums, elevating ceramic brake pad adoption, dust control, and wear behaviour to the centre of supplier competition and structurally rewarding manufacturers with validated low-dust brake materials portfolios and OEM-certified testing capabilities throughout the forecast period.

By Vehicle Type

- Medium and Heavy Commercial Vehicles

- Light Commercial Vehicles

- Passenger Cars

- Others

Passenger Cars command the highest share within the vehicle type category at approximately 55%, establishing sedans, hatchbacks, SUVs, crossovers, and electric passenger vehicles as the most commercially significant and volume-generating demand context within the Global automotive brake components market. Contractors across passenger car OEM and service channels consistently require full disc brake system and drum brake assemblies including pads, rotors, calipers, cylinders, lines, and hardware across both new vehicle build and recurring maintenance replacement cycles, creating a broad and phase-recurring demand pattern that sustains the passenger car segment's commercial leadership across both original equipment and aftermarket brake components supply simultaneously.

The segment's structural depth within the automotive brake components market is reinforced by the scale of passenger car production and sales across Asia Pacific's most commercially active vehicle markets. Validated reports from OICA confirm that China sold 30.1 million passenger cars in 2025, India sold 4.49 million, and Japan sold 3.84 million, collectively confirming that the passenger car end-user base generating recurring brake components for passenger cars procurement demand is both exceptionally large and geographically concentrated in precisely the regions where supplier localisation, component ecosystem depth, and EV transition momentum are simultaneously creating the most commercially dynamic and competitively demanding operating environment throughout the forecast period.

Market Players in Global Automotive Brake Components Market

These market players maintain a significant presence in the Global automotive brake components market sector and contribute to its ongoing evolution.

- Robert Bosch GmbH

- Aisin Seiko Co. Ltd.

- Valeo SA

- Nisshinbo Holdings

- Hitachi Automotive Systems Limited

- Akebono Brake Industry Co., Ltd.

- Continental AG

- Wabco Holdings Inc.

- Delphi Automotive Plc

- Federal Mogul Holdings Corporations

Market News & Updates

- Delphi, 2026:

Delphi released Professional+ brake pads for light commercial vehicles in February 2026. The range is designed for high-stop and high-load fleet use, with 58 SKUs planned through 2026 for models such as Mercedes-Benz Sprinter, Ford Transit, Volkswagen Transporter, Fiat Ducato, and Iveco Daily. The launch expands Delphi’s brake pad coverage for LCV aftermarket applications.

- Nisshinbo Holdings/TMD Friction, 2026:

TMD Friction’s Textar brand introduced 153 new products in 2025, with the update published in February 2026. The additions included 49 passenger car brake pads, 5 commercial vehicle brake pads, 28 brake discs, 2 brake drums, 1 drum brake lining, and 4 brake shoes. The update expands Textar’s aftermarket braking components portfolio for passenger and commercial vehicles.

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- Global Automotive Brake Components Market Policies, Regulations, and Standards

- Global Automotive Brake Components Market Production (Units) Trend 2022-2032

- Global Automotive Brake Components (Units) Trend By Vehicle Type

- Medium and Heavy Commercial Vehicles

- Light Commercial Vehicles

- Passenger Cars

- Company Wise Production Plants and Statistics

- Installed Production Capacity

- Actual Production

- Planned Production Target

- Global Automotive Brake Components Pricing Analysis 2022-2032

- Global Automotive Brake Components Pricing Trend (USD/Units) 2022-2032

- Global Automotive Brake Components Pricing Trend (USD/Units) By Regions 2022-2032

- North America

- South America

- Europe

- Middle East & Africa

- Asia Pacific

- Global Automotive Brake Components Pricing Trend (USD/Units) By Vehicle Type 2022-2032

- Medium and Heavy Commercial Vehicles

- Light Commercial Vehicles

- Passenger Cars

- Global Automotive Brake Components Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- Global Automotive Brake Components Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Unit Sold (Thousand Units)

- Market Segmentation & Growth Outlook

- By Vehicle Type

- Medium and Heavy Commercial Vehicles- Market Insights and Forecast 2022-2032, USD Million

- Light Commercial Vehicles- Market Insights and Forecast 2022-2032, USD Million

- Passenger Cars- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel

- OEMs- Market Insights and Forecast 2022-2032, USD Million

- Aftermarket- Market Insights and Forecast 2022-2032, USD Million

- By Product Type

- Brake Caliper- Market Insights and Forecast 2022-2032, USD Million

- Floating Caliper- Market Insights and Forecast 2022-2032, USD Million

- Fixed Caliper- Market Insights and Forecast 2022-2032, USD Million

- Brake Pad- Market Insights and Forecast 2022-2032, USD Million

- Metal- Market Insights and Forecast 2022-2032, USD Million

- Ceramic- Market Insights and Forecast 2022-2032, USD Million

- Organic- Market Insights and Forecast 2022-2032, USD Million

- Brake Rotor- Market Insights and Forecast 2022-2032, USD Million

- Brake Shoe- Market Insights and Forecast 2022-2032, USD Million

- Brake Line- Market Insights and Forecast 2022-2032, USD Million

- By Region

- North America

- South America

- Europe

- Middle East & Africa

- Asia Pacific

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Vehicle Type

- Market Size & Growth Outlook

- North America Automotive Brake Components Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Unit Sold (Thousand Units)

- Market Segmentation & Growth Outlook

- By Vehicle Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Product Type- Market Insights and Forecast 2022-2032, USD Million

- By Country

- US

- Canada

- Mexico

- Rest of North America

- US Automotive Brake Components Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Unit Sold (Thousand Units)

- Market Segmentation & Growth Outlook

- By Vehicle Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Product Type- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Canada Automotive Brake Components Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Unit Sold (Thousand Units)

- Market Segmentation & Growth Outlook

- By Vehicle Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Product Type- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Mexico Automotive Brake Components Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Unit Sold (Thousand Units)

- Market Segmentation & Growth Outlook

- By Vehicle Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Product Type- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Market Size & Growth Outlook

- South America Automotive Brake Components Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Unit Sold (Thousand Units)

- Market Segmentation & Growth Outlook

- By Vehicle Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Product Type- Market Insights and Forecast 2022-2032, USD Million

- By Country

- Brazil

- Argentina

- Colombia

- Chile

- Rest of South America

- Brazil Automotive Brake Components Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Unit Sold (Thousand Units)

- Market Segmentation & Growth Outlook

- By Vehicle Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Product Type- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Argentina Automotive Brake Components Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Unit Sold (Thousand Units)

- Market Segmentation & Growth Outlook

- By Vehicle Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Product Type- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Colombia Automotive Brake Components Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Unit Sold (Thousand Units)

- Market Segmentation & Growth Outlook

- By Vehicle Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Product Type- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Chile Automotive Brake Components Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Unit Sold (Thousand Units)

- Market Segmentation & Growth Outlook

- By Vehicle Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Product Type- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Market Size & Growth Outlook

- Europe Automotive Brake Components Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Unit Sold (Thousand Units)

- Market Segmentation & Growth Outlook

- By Vehicle Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Product Type- Market Insights and Forecast 2022-2032, USD Million

- By Country

- Germany

- UK

- France

- Spain

- Italy

- Netherlands

- Rest of Europe

- Germany Automotive Brake Components Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Unit Sold (Thousand Units)

- Market Segmentation & Growth Outlook

- By Vehicle Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Product Type- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- UK Automotive Brake Components Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Unit Sold (Thousand Units)

- Market Segmentation & Growth Outlook

- By Vehicle Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Product Type- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- France Automotive Brake Components Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Unit Sold (Thousand Units)

- Market Segmentation & Growth Outlook

- By Vehicle Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Product Type- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Spain Automotive Brake Components Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Unit Sold (Thousand Units)

- Market Segmentation & Growth Outlook

- By Vehicle Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Product Type- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Italy Automotive Brake Components Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Unit Sold (Thousand Units)

- Market Segmentation & Growth Outlook

- By Vehicle Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Product Type- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Netherlands Automotive Brake Components Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Unit Sold (Thousand Units)

- Market Segmentation & Growth Outlook

- By Vehicle Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Product Type- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Market Size & Growth Outlook

- Middle East & Africa Automotive Brake Components Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Unit Sold (Thousand Units)

- Market Segmentation & Growth Outlook

- By Vehicle Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Product Type- Market Insights and Forecast 2022-2032, USD Million

- By Country

- Saudi Arabia

- UAE

- South Africa

- Egypt

- Rest of Middle East & Africa

- Saudi Arabia Automotive Brake Components Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Unit Sold (Thousand Units)

- Market Segmentation & Growth Outlook

- By Vehicle Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Product Type- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- UAE Automotive Brake Components Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Unit Sold (Thousand Units)

- Market Segmentation & Growth Outlook

- By Vehicle Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Product Type- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- South Africa Automotive Brake Components Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Unit Sold (Thousand Units)

- Market Segmentation & Growth Outlook

- By Vehicle Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Product Type- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Egypt Automotive Brake Components Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Unit Sold (Thousand Units)

- Market Segmentation & Growth Outlook

- By Vehicle Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Product Type- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Market Size & Growth Outlook

- Asia Pacific Automotive Brake Components Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Unit Sold (Thousand Units)

- Market Segmentation & Growth Outlook

- By Vehicle Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Product Type- Market Insights and Forecast 2022-2032, USD Million

- By Country

- China

- India

- Japan

- Australia

- South Korea

- Thailand

- Indonesia

- Singapore

- Rest of Asia Pacific

- China Automotive Brake Components Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Unit Sold (Thousand Units)

- Market Segmentation & Growth Outlook

- By Vehicle Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Product Type- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- India Automotive Brake Components Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Unit Sold (Thousand Units)

- Market Segmentation & Growth Outlook

- By Vehicle Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Product Type- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Japan Automotive Brake Components Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Unit Sold (Thousand Units)

- Market Segmentation & Growth Outlook

- By Vehicle Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Product Type- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Australia Automotive Brake Components Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Unit Sold (Thousand Units)

- Market Segmentation & Growth Outlook

- By Vehicle Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Product Type- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- South Korea Automotive Brake Components Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Unit Sold (Thousand Units)

- Market Segmentation & Growth Outlook

- By Vehicle Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Product Type- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Thailand Automotive Brake Components Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Unit Sold (Thousand Units)

- Market Segmentation & Growth Outlook

- By Vehicle Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Product Type- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Indonesia Automotive Brake Components Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Unit Sold (Thousand Units)

- Market Segmentation & Growth Outlook

- By Vehicle Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Product Type- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Singapore Automotive Brake Components Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Unit Sold (Thousand Units)

- Market Segmentation & Growth Outlook

- By Vehicle Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Product Type- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- Nisshinbo Holdings

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Hitachi Automotive Systems Limited

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Akebono Brake Industry Co., Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Continental AG

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Wabco Holdings Inc.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Robert Bosch GmbH

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Aisin Seiko Co. Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Valeo SA

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Delphi Automotive Plc

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Federal Mogul Holdings Corporations

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Nisshinbo Holdings

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Vehicle Type |

|

| By Sales Channel |

|

| By Product Type |

|

| By Region |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.