Europe Electric Two Wheeler Market Report: Trends, Growth and Forecast (2026-2032)

By Type (Electric Motorcycles, Electric Scooters), By Battery Type (Nickel Metal Hybrid Batteries, Sealed Lead Acid Batteries, Lithium-Ion Batteries), By Drive Type (Hub Drive Motor, Mid Drive Motor), By Voltage (<48V, 48-60V, 61-72V, 73-96V, 96V), By Peak Power (<3 kW, 3–6 kW, 7–10 kW, 10 kW), By Battery Technology (Removable, Non-Removable), By Motor Placement (Hub Type, Chassis Mounted), By Country (UK, Germany, France, Italy, Netherlands, Austria, Spain, Rest of Europe) ... Read more

|

Major Players

|

Europe Electric Two Wheeler Market Statistics and Insights, 2026

- Market Size Statistics

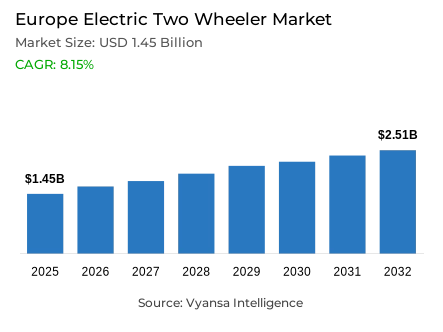

- Electric two wheeler market size in Europe was valued at USD 1.45 billion in 2025 and is estimated at USD 1.57 billion in 2026.

- The market size is expected to grow to USD 2.51 billion by 2032.

- Market to register a CAGR of around 8.15% during 2026-32.

- Type Shares

- Electric scooters grabbed market share of 65%.

- Competition

- More than 15 companies are actively engaged in producing electric two wheeler in Europe.

- Top 5 companies acquired around 20% of the market share.

- Askoll EVA, Silence/ACCIONA, Zero Motorcycles, NIU Technologies, Yadea Group etc., are few of the top companies.

- Battery Type

- Lithium-Ion Batteries grabbed 90% of the market.

- Country

- Germany leads with a 25% share of the Europe market.

Europe Electric Two Wheeler Market Outlook

Europe electric two wheeler market was valued at USD 1.45 billion in 2025 and is projected to advance from USD 1.57 billion in 2026 to USD 2.51 billion by 2032, registering a CAGR of 8.15% across the forecast period. This sustained and policy-reinforced expansion reflects a commercially dependable growth environment within the Europe electric two wheeler market, where rising urban mobility pressure, growing consumer preference for low-emission urban mobility alternatives, expanding delivery fleet electrification, and the increasing practicality of compact battery-powered personal transport are collectively sustaining consistent and broadly distributed demand across electric scooter and motorcycle categories simultaneously. Growth is anchored not in speculative adoption but in the demonstrated practical utility of electric two wheelers across daily commuting, last-mile logistics, shared mobility, and short-distance urban travel where their cost, size, and emission profile advantages over petrol alternatives are measurable and commercially self-reinforcing.

Electric scooters Europe command approximately 65% of the type segment within the Europe electric two wheeler market, reflecting the consistent and broadly distributed consumer and fleet preference for lighter, easier-to-operate, and more space-efficient two-wheeler formats that align naturally with the density, parking constraints, and short-trip dominance of European urban mobility environments. As per data published by the European Commission citing Eurostat, approximately 39% of new mopeds registered in 2024 were zero-emission vehicles, confirming that electrification in the small two-wheeler category is already commercially visible and advancing at a pace that validates scooters' structural leadership within the broader market.

Lithium-ion batteries dominate the battery type segment with approximately 90% share, anchored in their superior energy density, lower weight, longer cycle life, and strong compatibility with the removable battery electric scooters and compact battery designs that urban scooter and motorcycle platforms increasingly depend on for practical everyday usability. Evidence drawn from public data released by the IEA confirms that two- and three-wheelers remained the most electrified road transport segment globally in 2024, with more than 9% of the global fleet already electric and global electric model sales reaching 10 million units, confirming that the technology foundation sustaining lithium-ion battery electric two wheelers demand is globally robust and commercially deepening.

Germany anchors the Europe electric scooter market with approximately 25% of regional demand, supported by structured regulatory clarity, strong EV consumer awareness, mature urban mobility infrastructure, and an established automotive and mobility ecosystem that supports dealer networks, insurance frameworks, battery service providers, and fleet management capabilities. As per data published by the IEA, Europe's public charging points grew by more than 35% in 2024 to just over 1 million, with 11 EU countries expanding public charging stock by more than 50%, collectively reinforcing the broader electric mobility confidence environment that sustains electric two wheeler demand for urban commuting across the continent through the forecast period.

Europe Electric Two Wheeler Market Growth Driver

Urban Emission Policy and Practical Mobility Economics Are Building a Structurally Durable Growth Foundation

Europe's accelerating push toward lower-emission urban transport is the most commercially significant demand driver within the Europe electric two wheeler market, sustaining adoption across consumer, delivery, and shared mobility segments by making compact zero-emission two wheeler market Europe solutions increasingly practical and economically advantageous relative to petrol alternatives. As per data published by the European Environment Agency, transport is responsible for approximately one quarter of the EU's total greenhouse gas emissions and contributes to air pollution, noise, and habitat fragmentation, while the simultaneous expansion of low-emission zones, speed-calmed areas, parking controls, and shared mobility frameworks across major European cities is progressively elevating the urban utility advantage of electric scooters and motorcycles over larger and higher-emission personal transport alternatives.

Battery compliance obligations and safety regulatory fragmentation are simultaneously creating the most demanding structural challenge within the Europe electric two wheeler market, as the EU Sustainable Batteries Regulation establishes lithium battery recycling efficiency targets of 65% by end of 2025 alongside material recovery obligations requiring 90% recovery of cobalt, copper, lead, and nickel by 2027 and 80% lithium recovery by 2031, raising battery design, documentation, supplier verification, and end-of-life collection complexity for every market participant. The strongest commercial opportunity within this environment lies in fleet electrification and delivery mobility, where operators seeking lower running costs, simpler maintenance, and low-emission zone access are creating durable high-utilisation demand that well-positioned suppliers offering battery swapping electric scooters, telematics integration, battery leasing, and certified after-sales service can capture across an expanding addressable base throughout the forecast period.

Europe Electric Two Wheeler Market Challenge

Battery Compliance Obligations and Regulatory Fragmentation Are Raising Market-Entry Complexity

The most commercially consequential structural challenge within the Europe e-scooter market is the rising compliance burden across battery lifecycle management, road-use regulation, and cross-border market-entry requirements that collectively raise the operational and documentation investment that manufacturers and fleet operators must absorb before achieving commercially sustainable scale. Based on data from the European Commission, material recovery targets require 90% recovery of cobalt, copper, lead, and nickel by 31 December 2027 and 80% lithium recovery by 31 December 2031, with lithium battery recycling efficiency targets set at 65% by end of 2025, confirming that battery pack design, traceability, end-of-life collection infrastructure, and recycling partnership agreements are becoming non-negotiable compliance requirements rather than optional sustainability investments for every supplier operating across the European market.

Road-safety regulation adds a separately significant and commercially relevant layer of compliance complexity. Validated reports from the European Commission's ERSO confirm that age restrictions apply for e-scooter use in 14 of 22 reported European countries with minimum ages ranging from 10 to 16 years, while maximum speed limits are consistently set at either 20 km/h or 25 km/h across reporting countries, creating a fragmented national regulatory environment that requires vehicle-level software speed limitation, insurance compatibility, lighting specification, and safety documentation to be managed on a country-by-country basis, raising market-entry costs and operational overhead most severely for low-voltage electric scooters suppliers and smaller importers with limited compliance infrastructure.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Europe Electric Two Wheeler Market Trend

Lithium-Ion Battery Innovation and Connected Mobility Models Are Reshaping Product and Deployment Standards

A well-defined and commercially consequential structural trend is reshaping product development and adoption economics across the Europe electric motorcycle market, as continued improvement in lithium-ion battery platform performance, pack engineering, thermal management, and battery management system sophistication progressively closes the usability and confidence gap between electric and petrol two-wheeler ownership across both consumer and fleet buyer segments. As per data published by the IEA citing Green Li-ion, the global lithium-ion battery market exceeded USD 150 billion in 2025 reflecting more than 20% growth from 2024, confirming that the cell availability, pack engineering depth, supply-chain maturity, and cost-competitiveness improvements flowing from this industrial-scale expansion are directly benefiting lightweight electric scooters and high-performance electric motorcycles platforms across the European market.

The commercial implications of this trend are deepening as shared electric scooters Europe and delivery fleet electrification create high-utilisation recurring demand streams that reward suppliers investing in removable battery electric scooters, depot-charging models, fleet telematics, and subscription-based maintenance rather than selling vehicles as one-time commodity transactions. Evidence drawn from public data released by the IEA confirms that electric car sales in 2025 are expected to exceed 20 million globally and represent more than one quarter of all cars sold worldwide, a trajectory that normalises charging infrastructure, strengthens dealer readiness, and deepens consumer confidence in electric mobility across the broader European market environment that also sustains two-wheeler adoption throughout the forecast period.

Europe Electric Two Wheeler Market Opportunity

Fleet Electrification and Charging Infrastructure Expansion Are Creating High-Value Ecosystem Demand

The most commercially significant and structurally recurring growth opportunity within the Europe electric two wheeler market lies in fleet electrification, delivery mobility, and charging-supported urban deployment, where operators seeking lower running costs, simpler maintenance schedules, and reliable low-emission zone access are creating durable high-utilisation demand that extends well beyond vehicle sales into batteries, chargers, fleet software, diagnostics, spare packs, and maintenance service contracts. As per official figures from the IEA, Europe's public charging points grew by more than 35% in 2024 compared with 2023 to reach just over 1 million, with 11 of 27 EU countries increasing their public charging stock by more than 50%, confirming that the charging visibility infrastructure supporting broader electric mobility confidence is advancing at a pace that progressively reduces adoption friction for electric scooters for last-mile delivery and urban commercial fleet operators across the region.

Battery leasing, subscription-based maintenance, fleet telematics, residual-value support, and service contract models are independently creating a separately significant commercial opportunity layer for manufacturers and distributors capable of positioning electric two wheeler ownership as a lifecycle-managed mobility service rather than a one-time vehicle transaction. Data compiled from internationally recognised public authorities at the IEA confirms that electric car sales in 2025 are expected to represent more than one quarter of global car sales, a mainstream adoption milestone that normalises EV dealer readiness, insurance product availability, and consumer charging confidence across the same European urban environments where electric motorcycles Europe and scooter platforms compete for daily commuter and fleet operator adoption throughout the forecast period.

Europe Electric Two Wheeler Market Country Analysis

By Country

- UK

- Germany

- France

- Italy

- Netherlands

- Austria

- Spain

- Rest of Europe

Germany commands the most commercially influential position within the Europe electric two wheeler market with approximately 25% of regional demand, a concentration that reflects the country's exceptional combination of structured regulatory clarity, high consumer EV awareness, mature urban mobility infrastructure, and a deep automotive and mobility ecosystem that supports dealer networks, insurance frameworks, certified battery service providers, and fleet management operations at a scale no other European national market currently replicates. As per data published by the European Commission's ERSO report, Germany permits electric scooter operation from a minimum age of 14 years, applies a maximum speed limit of 20 km/h, allows up to 500W, and requires mandatory insurance, establishing a defined and commercially navigable operating environment that reduces market-entry uncertainty for vehicle suppliers, fleet operators, and shared electric scooters Europe platforms seeking a credible European scaling base.

The broader European regulatory environment reinforces Germany's reference-market role by confirming that its operating rules sit within a structurally converging continental micromobility framework. Validated reports from the European Commission's ERSO confirm that age restrictions apply in 14 of 22 reported European countries with minimum ages ranging from 10 to 16 years, while maximum speed limits across reporting countries are consistently set at either 20 km/h or 25 km/h, confirming that product design standardisation around speed limits, braking systems, lighting, and safety identification is becoming a continental operating baseline rather than a market-specific requirement. For suppliers and fleet operators, Germany's combination of regulatory maturity, charging infrastructure depth, and urban mobility demand makes it the most commercially dependable national entry point within the Europe electric two wheeler market and the strongest credibility platform for subsequent expansion across France, Italy, the Netherlands, Spain, and other major European country markets throughout the forecast period.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Europe Electric Two Wheeler Market Segmentation Analysis

By Type

- Electric Motorcycles

- Electric Scooters

Electric Scooters command the highest share within the type category at approximately 65%, reflecting the consistent and structurally embedded preference among urban consumers, delivery operators, and shared micromobility platforms Europe for lighter, more accessible, and city-optimised two-wheeler formats that deliver lower operating cost, simpler rider requirements, and better alignment with the short-trip, high-frequency mobility patterns that characterise European urban travel. Consumers and fleet buyers consistently select scooter formats because their compact hub drive motor configurations, under-seat battery layouts, and lighter frame designs make them easier to park, more affordable to own, and more practical to charge than larger electric motorcycle alternatives, a preference directly reinforced by the 39% zero-emission share already recorded in new European moped registrations in 2024 as confirmed by Eurostat data.

The segment's commercial durability within the Europe electric two wheeler market is further reinforced by the policy environment that continues to expand urban access advantages for compact low-speed electric scooters across European cities implementing low-emission zones, parking restrictions, and micromobility frameworks. For electric scooters for daily commuting and courier platform operators, the economics are especially compelling because lower energy consumption, simpler powertrain maintenance, and route flexibility across congested city environments collectively sustain stronger operating margins than petrol-equivalent alternatives, creating a structurally recurring commercial demand base that is expected to deepen as European urban mobility regulation intensifies throughout the forecast period.

By Battery Type

- Nickel Metal Hybrid Batteries

- Sealed Lead Acid Batteries

- Lithium-Ion Batteries

Lithium-Ion Batteries command the highest share within the battery type category at approximately 90%, establishing advanced lithium chemistry as the overwhelmingly dominant technology platform across the Europe electric two wheeler market and reflecting the consistent and practically motivated preference among vehicle manufacturers, fleet operators, and individual consumers for battery systems that deliver superior energy density, lower vehicle weight, longer operating cycle life, and strong compatibility with the removable and compact pack configurations that urban scooter usability increasingly demands. Manufacturers across commuter scooter and high-performance electric motorcycles categories consistently specify lithium-ion configurations because they support better vehicle balance, cleaner under-seat packaging, faster charging profiles, and more reliable battery management system integration than sealed lead-acid or older nickel-based alternatives.

The segment's structural dominance within the Europe electric two wheeler market is reinforced by the growing regulatory accountability that battery design must now carry under the EU Sustainable Batteries Regulation, which transforms lithium-ion packs from pure performance components into lifecycle-managed assets requiring traceability, recycling pathway documentation, and certified recovery partnerships. As swappable battery electric two wheelers and removable battery models gain commercial relevance across apartment-dwelling urban consumers and delivery fleet operators who cannot always access dedicated fixed charging points, the ability to combine high lithium-ion performance with regulatory compliance, thermal safety certification, and end-of-life collection capability is becoming a structurally significant competitive differentiator among Europe electric two wheeler market participants throughout the forecast period.

Various Market Players in Europe Electric Two Wheeler Market

The companies mentioned below are highly active in the Europe electric two wheeler market, occupying a considerable portion of the market and shaping industry progress.

- Askoll EVA

- Silence/ACCIONA

- Zero Motorcycles

- NIU Technologies

- Yadea Group

- VMoto/Super Soco

- BMW Motorrad

- Piaggio Group

- HORWIN

- GOVECS

- Energica Motor Company

- PIERER Mobility/KTM

Market News & Updates

- Honda Motor Co., 2025:

Honda introduced the WN7 as its first production full-size electric motorcycle for Europe in November 2025. The 26YM model offers up to 140 km range, 9.3 kWh battery, 50 kW peak power, CCS2 charging, RoadSync connectivity, selectable riding modes, and A1-compatible version. The model expands Honda’s electric two-wheeler lineup beyond urban scooters.

- Ltd., 2025:

ACCIONA renewed the Silence S02 electric scooter in December 2025. The upgraded version is lighter, more stable, and offers more under-seat storage, with the company positioning it for urban mobility and professional use. The update strengthens Silence’s electric scooter portfolio in Europe, especially for city commuting and delivery applications.

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- Europe Electric Two Wheeler Market Policies, Regulations, and Standards

- Europe Electric Two Wheeler Production (Unit) Trend 2022-2032

- Europe Electric Two Wheeler Production (Unit) Trend By Type

- Electric Motorcycles

- Electric Scooters

- Company Wise Production Plants and Statistics

- Installed Production Capacity

- Actual Production

- Planned Production Target

- Europe Electric Two Wheeler Production (Unit) Trend By Type

- Europe Electric Two Wheeler Pricing Analysis 2022-2032

- Europe Electric Two Wheeler Pricing Trend (USD/Unit) 2022-2032

- Europe Electric Two Wheeler Pricing Trend (USD/Unit) By Regions 2022-2032

- UK

- Germany

- France

- Italy

- Netherlands

- Austria

- Spain

- Europe Electric Two Wheeler Pricing Trend (USD/Unit) By Type 2022-2032

- Electric Motorcycles

- Electric Scooters

- Europe Electric Two Wheeler Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- Europe Electric Two Wheeler Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Units Sold (Thousand Units)

- Market Segmentation & Growth Outlook

- By Type

- Electric Motorcycles- Market Insights and Forecast 2022-2032, USD Million

- Electric Scooters- Market Insights and Forecast 2022-2032, USD Million

- By Battery Type

- Nickel Metal Hybrid Batteries- Market Insights and Forecast 2022-2032, USD Million

- Sealed Lead Acid Batteries- Market Insights and Forecast 2022-2032, USD Million

- Lithium-Ion Batteries- Market Insights and Forecast 2022-2032, USD Million

- By Drive Type

- Hub Drive Motor- Market Insights and Forecast 2022-2032, USD Million

- Mid Drive Motor- Market Insights and Forecast 2022-2032, USD Million

- By Voltage

- <48V- Market Insights and Forecast 2022-2032, USD Million

- 48-60V- Market Insights and Forecast 2022-2032, USD Million

- 61-72V- Market Insights and Forecast 2022-2032, USD Million

- 73-96V- Market Insights and Forecast 2022-2032, USD Million

- 96V- Market Insights and Forecast 2022-2032, USD Million

- By Peak Power

- <3 kW- Market Insights and Forecast 2022-2032, USD Million

- 3–6 kW- Market Insights and Forecast 2022-2032, USD Million

- 7–10 kW- Market Insights and Forecast 2022-2032, USD Million

- 10 kW- Market Insights and Forecast 2022-2032, USD Million

- By Battery Technology

- Removable- Market Insights and Forecast 2022-2032, USD Million

- Non-Removable- Market Insights and Forecast 2022-2032, USD Million

- By Motor Placement

- Hub Type- Market Insights and Forecast 2022-2032, USD Million

- Chassis Mounted- Market Insights and Forecast 2022-2032, USD Million

- By Country

- UK

- Germany

- France

- Italy

- Netherlands

- Austria

- Spain

- Rest of Europe

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Type

- Market Size & Growth Outlook

- UK Electric Two Wheeler Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Units Sold (Thousand Units)

- Market Segmentation & Growth Outlook

- By Type- Market Insights and Forecast 2022-2032, USD Million

- By Battery Type- Market Insights and Forecast 2022-2032, USD Million

- By Drive Type- Market Insights and Forecast 2022-2032, USD Million

- By Voltage- Market Insights and Forecast 2022-2032, USD Million

- By Peak Power- Market Insights and Forecast 2022-2032, USD Million

- By Battery Technology- Market Insights and Forecast 2022-2032, USD Million

- By Motor Placement- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Germany Electric Two Wheeler Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Units Sold (Thousand Units)

- Market Segmentation & Growth Outlook

- By Type- Market Insights and Forecast 2022-2032, USD Million

- By Battery Type- Market Insights and Forecast 2022-2032, USD Million

- By Drive Type- Market Insights and Forecast 2022-2032, USD Million

- By Voltage- Market Insights and Forecast 2022-2032, USD Million

- By Peak Power- Market Insights and Forecast 2022-2032, USD Million

- By Battery Technology- Market Insights and Forecast 2022-2032, USD Million

- By Motor Placement- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- France Electric Two Wheeler Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Units Sold (Thousand Units)

- Market Segmentation & Growth Outlook

- By Type- Market Insights and Forecast 2022-2032, USD Million

- By Battery Type- Market Insights and Forecast 2022-2032, USD Million

- By Drive Type- Market Insights and Forecast 2022-2032, USD Million

- By Voltage- Market Insights and Forecast 2022-2032, USD Million

- By Peak Power- Market Insights and Forecast 2022-2032, USD Million

- By Battery Technology- Market Insights and Forecast 2022-2032, USD Million

- By Motor Placement- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Italy Electric Two Wheeler Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Units Sold (Thousand Units)

- Market Segmentation & Growth Outlook

- By Type- Market Insights and Forecast 2022-2032, USD Million

- By Battery Type- Market Insights and Forecast 2022-2032, USD Million

- By Drive Type- Market Insights and Forecast 2022-2032, USD Million

- By Voltage- Market Insights and Forecast 2022-2032, USD Million

- By Peak Power- Market Insights and Forecast 2022-2032, USD Million

- By Battery Technology- Market Insights and Forecast 2022-2032, USD Million

- By Motor Placement- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Netherlands Electric Two Wheeler Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Units Sold (Thousand Units)

- Market Segmentation & Growth Outlook

- By Type- Market Insights and Forecast 2022-2032, USD Million

- By Battery Type- Market Insights and Forecast 2022-2032, USD Million

- By Drive Type- Market Insights and Forecast 2022-2032, USD Million

- By Voltage- Market Insights and Forecast 2022-2032, USD Million

- By Peak Power- Market Insights and Forecast 2022-2032, USD Million

- By Battery Technology- Market Insights and Forecast 2022-2032, USD Million

- By Motor Placement- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Austria Electric Two Wheeler Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Units Sold (Thousand Units)

- Market Segmentation & Growth Outlook

- By Type- Market Insights and Forecast 2022-2032, USD Million

- By Battery Type- Market Insights and Forecast 2022-2032, USD Million

- By Drive Type- Market Insights and Forecast 2022-2032, USD Million

- By Voltage- Market Insights and Forecast 2022-2032, USD Million

- By Peak Power- Market Insights and Forecast 2022-2032, USD Million

- By Battery Technology- Market Insights and Forecast 2022-2032, USD Million

- By Motor Placement- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Spain Electric Two Wheeler Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Units Sold (Thousand Units)

- Market Segmentation & Growth Outlook

- By Type- Market Insights and Forecast 2022-2032, USD Million

- By Battery Type- Market Insights and Forecast 2022-2032, USD Million

- By Drive Type- Market Insights and Forecast 2022-2032, USD Million

- By Voltage- Market Insights and Forecast 2022-2032, USD Million

- By Peak Power- Market Insights and Forecast 2022-2032, USD Million

- By Battery Technology- Market Insights and Forecast 2022-2032, USD Million

- By Motor Placement- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- NIU Technologies

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Yadea Group

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- VMoto/Super Soco

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- BMW Motorrad

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Piaggio Group

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Askoll EVA

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Silence/ACCIONA

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Zero Motorcycles

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- HORWIN

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- GOVECS

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Energica Motor Company

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- PIERER Mobility/KTM

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Peugeot Motocycles

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Honda Motor Co., Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Yamaha Motor Co., Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- NIU Technologies

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Type |

|

| By Battery Type |

|

| By Drive Type |

|

| By Voltage |

|

| By Peak Power |

|

| By Battery Technology |

|

| By Motor Placement |

|

| By Country |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.