India Biofungicides Market Report: Trends, Growth and Forecast (2026-2032)

By Source (Microbial, Botanical), By Species (Bacillus, Trichoderma, Pseudomonas, Streptomyces, Saccharomyces, Aureobasidium, Coniothyrium, Others), By Form (Wettable Powder, Aqueous Solution, Granules, Powder, Liquid), By Mode of Application (Foliar Spray, Soil Treatment, Seed Treatment, Post-Harvest Treatment, Root Dipping, Drip Irrigation, Sprinkler Irrigation, Others), By Crop Type (Fruits and Vegetables, Cereals and Grains, Oilseeds and Pulses, Turf and Ornamentals, Plantation Crops, Nursery Crops, Others), By Region (North, East, West, South) ... Read more

|

Major Players

|

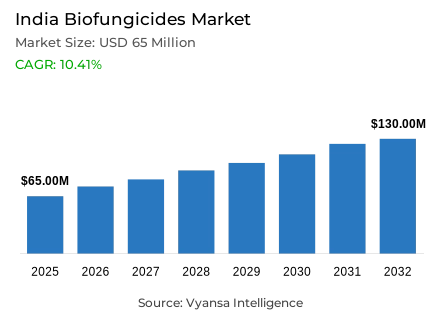

India Biofungicides Market Statistics and Insights, 2026

- Market Size Statistics

- Biofungicides market size in India was valued at USD 65 million in 2025 and is estimated at USD 70 million in 2026.

- The market size is expected to grow to USD 130 million by 2032.

- Market to register a CAGR of around 10.41% during 2026-32.

- Source Shares

- Microbial grabbed market share of 85%.

- Competition

- More than 10 companies are actively engaged in producing biofungicides in India.

- Top 5 companies acquired around 40% of the market share.

- Multiplex Bio-Tech Pvt. Ltd., Ajay Bio-Tech (I) Ltd.(Biofix), Varsha Bioscience and Technology India Pvt. Ltd., IPL Biologicals Limited, T. Stanes and Company Limited etc., are few of the top companies.

- Species

- Trichoderma grabbed 40% of the market.

India Biofungicides Market Outlook

India Biofungicides Market is valued at USD 65 Million in 2025 and is projected to reach USD 130 Million by 2032, growing at a CAGR of 10.41% during 2026-2032. The market covers microbial and naturally derived fungicidal solutions used for crop disease control, seed treatment, soil application, foliar protection, and integrated pest management across field crops, horticulture, plantations, and organic production systems. The biological fungicide industry supports lower-residue agriculture by connecting biological formulation suppliers with growers seeking alternatives to synthetic disease-control inputs and export-sensitive crop assurance.

Organic farming, residue compliance, and natural farming policies are strengthening the demand base for India Biofungicides Market. APEDA states that India had 7.3 million hectares under organic cultivation in FY24, including 4.5 million hectares of farm area and 2.8 million hectares of wild collection area. This acreage expands the addressable base for microbial fungicides, especially where certification, export acceptance, and input restrictions shape procurement preferences among organized growers and aggregators.

The economic impact of India Biofungicides Market is linked to input substitution, localized formulation supply, disease-loss reduction, and compliance-led crop marketing. India Biofungicides Industry benefits from certified organic value chains that require traceable inputs and documented residue controls. APEDA reported 3.6 million MT of certified organic products in FY24, indicating a sizeable production ecosystem where bio-based crop protection can improve grower access to premium and regulated channels nationwide.

The 2026 trajectory favors registered microbial products, quality compliance, field-extension support, and distribution models aligned with natural farming clusters. India Biofungicides Market is positioned for stronger adoption as farmers, input suppliers, and public extension networks move toward chemical-free crop systems. India Biofungicides Industry is likely to prioritize formulation stability, local bio-input availability, Trichoderma-led solutions, and compatibility with IPM programs as procurement shifts from pilot demand toward repeat commercial use across priority crop belts and certification-linked channels.

India Biofungicides Market Growth Driver

Chemical-Free Farming Programs Strengthen Biological Input Demand

Chemical-free cultivation programs are converting biological crop protection from an optional input into a structured procurement and extension-led adoption need. India Biofungicides Market benefits as natural farming clusters require disease-control products that fit residue-sensitive, soil-health-oriented, and locally adaptable production systems. This demand is strongest where growers need microbial fungicides for seed treatment, root-zone disease suppression, nursery protection, and integrated crop management without disrupting certification pathways or reducing buyer confidence across high-value and export-oriented crop categories.

Ministry of Agriculture & Farmers Welfare reported that, under NMNF, 18,786 clusters covering 8.80 lakh hectares and 18.19 lakh farmers had been enrolled as of 05.03.2026. The same update noted bio-input resource centres and trained village-level resource persons, improving last-mile guidance. This directly supports India Biofungicides Industry by expanding organized farmer outreach, increasing repeat use of bio-based disease-control crop inputs, and improving procurement visibility for microbial formulation suppliers steadily serving decentralized rural demand networks nationwide.

India Biofungicides Market Challenge

Field Efficacy Variability Raises Adoption Friction

Field-level performance variability constrains supplier scale-up because microbial fungicides strongly depend on strain quality, moisture, temperature, crop stage, soil biology, and application discipline and timing. India Biofungicides Market faces adoption friction when farmers expect chemical-like consistency but handle living formulations through fragmented storage, transport, and advisory channels. This increases the burden on manufacturers to improve shelf life, farmer instructions, compatibility data, and local demonstrations before distributors can convert trial usage into repeat seasonal procurement.

Ministry of Agriculture & Farmers Welfare stated in March 2026 that ICAR’s All India Network on Natural Farming operates through 20 cooperation centres across 16 states, involving 11 State Agricultural Universities, 8 ICAR institutes or centres, and 1 deemed university. The same update noted that natural-farming performance remains context specific. This affects India Biofungicides Industry by raising validation costs, slowing generalized claims, and making region-specific efficacy evidence essential for regulatory confidence, distributor acceptance, and commercial participation.

Unlock Market Intelligence

Explore the market potential with our data-driven report

India Biofungicides Market Trend

Streamlined Biopesticide Registration Improves Product Formalization

Regulatory streamlining is shifting biological crop protection toward faster product formalization and broader microbial portfolio development in India. India Biofungicides Market gains from clearer biopesticide pathways because manufacturers can commercialize eligible biological crop products with lower procedural friction than conventional chemical pesticides. This supports innovation in Trichoderma, Bacillus, Pseudomonas, and consortium formulations while giving distributors more confidence to build category-specific technical teams, demonstration protocols, and farmer education programs across intensive cropping systems.

Press Information Bureau reported in December 2024 that CIB&RC simplified guidelines for registering biopesticides and that provisional registration under the Insecticides Act, 1968 allows biopesticide commercialization. The same source identified Trichoderma, Pseudomonas, Bacillus, Metarhizium, and Beauveria among biopesticides used in sustainable crop protection, with around 20 microorganisms commercially registered in India. This strengthens India Biofungicides Industry by improving product-entry clarity, widening active-microbe options, and supporting competitive differentiation around registered disease-control claims for seed, soil, and foliar applications.

India Biofungicides Market Opportunity

Bio-Input Centres Open Localized Distribution Pathways

Bio-input resource centres create a channel expansion opportunity for localized manufacturing, decentralized distribution, and advisory-led uptake of microbial disease-control crop products. India Biofungicides Market can capture demand where farmers need ready-to-use biological input products but lack on-farm preparation capacity, technical quality checks, or storage infrastructure. Suppliers that align formulations with cluster-level extension, farmer collectives, and seasonal crop calendars can improve availability while reducing last-mile adoption risk across remote farming districts and organized producer groups.

Press Information Bureau stated in August 2025 that NMNF targets 10,000 Bio-input Resource Centres and has deployed over 70,000 trained Krishi Sakhis to support input delivery and farmer guidance. This infrastructure can strengthen India Biofungicides Industry by creating repeat procurement nodes, enabling smaller pack-size distribution, and improving demonstration-led conversion for Trichoderma and other microbial fungicides. The opportunity is strongest for companies offering stable formulations, field protocols, and localized technical support during critical disease windows.

Unlock Market Intelligence

Explore the market potential with our data-driven report

India Biofungicides Market Segmentation Analysis

By Source

- Microbial

- Botanical

Microbial source biofungicide products hold 85% share, reflecting their operational fit with organic farming, IPM programs, seed treatment, and soil-borne disease suppression. India Biofungicides Market depends heavily on microorganisms because bacterial and fungal actives can be rapidly deployed through wettable powders, liquid formulations, compost enrichment, nursery dips, and root-zone applications. Their strong compatibility with farmer advisory programs also makes microbial products easier to demonstrate than many botanical alternatives in cluster-based adoption and training settings.

ICAR’s 2026 list of biologicals developed by its institutes includes biofertilizers, biopesticides, and biostimulants, with entries indicating commercialization status for multiple technologies. This supports microbial-source dominance by showing that public research institutions are converting organism-based crop solutions into usable product pipelines. The segment strengthens demand planning because suppliers can align strain selection, carrier systems, shelf-life improvement, and extension messaging with disease-control use cases already familiar to agricultural universities, cooperatives, KVKs, input distributors, and farmer-training networks.

By Species

- Bacillus

- Trichoderma

- Pseudomonas

- Streptomyces

- Saccharomyces

- Aureobasidium

- Coniothyrium

- Others

Trichoderma holds 40% share because it is embedded in seed and seedling treatment, soil application, nursery management, and root-zone disease suppression across cropping systems. The organism’s commercial strength comes from its fit with fungal pathogen control, compatibility with organic and biological inputs, and practical use in powder or liquid commercial bioformulations. This gives India Biofungicides Industry a recognizable anchor species for farmer education, distributor stocking, procurement planning, and formulation differentiation.

A 2026 article in The Indian Journal of Agricultural Sciences indexed by ICAR described the use of Trichoderma harzianum, Pseudomonas fluorescens, and neem cake as bio-pesticides in crop research. This type of institutional crop-level usage supports Trichoderma’s segment influence by reinforcing its role in applied disease-management trials and extension validation, agronomy recommendations, and mixed biological input packages. Suppliers benefit when research-backed application practices translate into clearer label positioning, demonstrations, technical selling and seasonal advisory programs across field channels.

List of Companies Covered in India Biofungicides Market

The companies listed below are highly influential in the India biofungicides market, with a significant market share and a strong impact on industry developments.

- Multiplex Bio-Tech Pvt. Ltd.

- Ajay Bio-Tech (I) Ltd.(Biofix)

- Varsha Bioscience and Technology India Pvt. Ltd.

- IPL Biologicals Limited

- T. Stanes and Company Limited

- FMC India Private Limited

- Biotech International Limited

- Sumitomo Chemical India Limited

- Gujarat Agri Processing Company Ltd.(Gujarat State Fertilizers & Chemicals Ltd.)

- Peptech Biosciences Ltd.

Market News & Updates

- IPL Biologicals Limited, 2025:

IPL Biologicals introduced Sporidex as a next-generation biological fungicide under its NXG product line. The product is powered by Pseudomonas fluorescens 5% SP and produces antibiotics, siderophores, and bioactive compounds that suppress harmful fungi. The update expands India-specific biological disease-control options within microbial crop protection portfolios.

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- India Biofungicides Market Policies, Regulations, and Standards

- India Biofungicides Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- India Biofungicides Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Volume in Metric Tonnes

- Market Segmentation & Growth Outlook

- By Source

- Microbial- Market Insights and Forecast 2022-2032, USD Million

- Botanical- Market Insights and Forecast 2022-2032, USD Million

- By Species

- Bacillus- Market Insights and Forecast 2022-2032, USD Million

- Trichoderma- Market Insights and Forecast 2022-2032, USD Million

- Pseudomonas- Market Insights and Forecast 2022-2032, USD Million

- Streptomyces- Market Insights and Forecast 2022-2032, USD Million

- Saccharomyces- Market Insights and Forecast 2022-2032, USD Million

- Aureobasidium- Market Insights and Forecast 2022-2032, USD Million

- Coniothyrium- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By Form

- Wettable Powder- Market Insights and Forecast 2022-2032, USD Million

- Aqueous Solution- Market Insights and Forecast 2022-2032, USD Million

- Granules- Market Insights and Forecast 2022-2032, USD Million

- Powder- Market Insights and Forecast 2022-2032, USD Million

- Liquid- Market Insights and Forecast 2022-2032, USD Million

- By Mode of Application

- Foliar Spray- Market Insights and Forecast 2022-2032, USD Million

- Soil Treatment- Market Insights and Forecast 2022-2032, USD Million

- Seed Treatment- Market Insights and Forecast 2022-2032, USD Million

- Post-Harvest Treatment- Market Insights and Forecast 2022-2032, USD Million

- Root Dipping- Market Insights and Forecast 2022-2032, USD Million

- Drip Irrigation- Market Insights and Forecast 2022-2032, USD Million

- Sprinkler Irrigation- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By Crop Type

- Fruits and Vegetables- Market Insights and Forecast 2022-2032, USD Million

- Cereals and Grains- Market Insights and Forecast 2022-2032, USD Million

- Oilseeds and Pulses- Market Insights and Forecast 2022-2032, USD Million

- Turf and Ornamentals- Market Insights and Forecast 2022-2032, USD Million

- Plantation Crops- Market Insights and Forecast 2022-2032, USD Million

- Nursery Crops- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By Region

- North

- East

- West

- South

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Source

- Market Size & Growth Outlook

- India Microbial Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Volume in Metric Tonnes

- Market Segmentation & Growth Outlook

- By Species- Market Insights and Forecast 2022-2032, USD Million

- By Form- Market Insights and Forecast 2022-2032, USD Million

- By Mode of Application- Market Insights and Forecast 2022-2032, USD Million

- By Crop Type- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- India Botanical Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Volume in Metric Tonnes

- Market Segmentation & Growth Outlook

- By Species- Market Insights and Forecast 2022-2032, USD Million

- By Form- Market Insights and Forecast 2022-2032, USD Million

- By Mode of Application- Market Insights and Forecast 2022-2032, USD Million

- By Crop Type- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- IPL Biologicals Limited

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- T. Stanes and Company Limited

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- FMC India Private Limited

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Biotech International Limited

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Sumitomo Chemical India Limited

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Multiplex Bio-Tech Pvt. Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Ajay Bio-Tech (I) Ltd.(Biofix)

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Varsha Bioscience and Technology India Pvt. Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Gujarat Agri Processing Company Ltd.(Gujarat State Fertilizers & Chemicals Ltd.)

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Peptech Biosciences Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- IPL Biologicals Limited

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Source |

|

| By Species |

|

| By Form |

|

| By Mode of Application |

|

| By Crop Type |

|

| By Region |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.