Europe Advanced Energy Storage Systems Market Report: Trends, Growth and Forecast (2026-2032)

By Technology (Batteries, Thermal Energy Storage, Pumped Hydro Storage, Compressed Air Energy Storage, Flywheel Energy Storage, Other Advanced Energy Storage Technologies), By Application (Grid Storage, Transportation, Renewable Energy Integration, Backup Power, Microgrids, Others), By End Use (Residential, Commercial, Industrial, Utility), By Storage Duration (Short-Duration Storage, Medium-Duration Storage, Long-Duration Storage), By Sales Channel (Retail Online (Company-Owned Websites, E-Commerce Platforms, Online Energy Equipment Stores, Online Electrical Supply Portals, B2B Procurement Platforms), Retail Offline (Direct Sales, Energy Equipment Distributors, Electrical Equipment Dealers, System Integrators, EPC Contractors, Utility Procurement Contracts, Authorized Dealers, Others)), By Country (Germany, The UK, France, Spain, Italy, Benelux, Nordic, Russia, Rest of Europe) ... Read more

|

Major Players

|

Europe Advanced Energy Storage Systems Market Size, Share & Forecast (2026–2032)

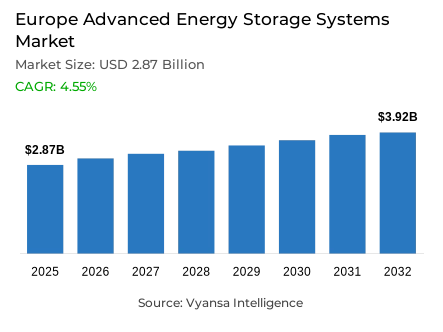

Advanced energy storage systems are critical technologies used to store and manage electrical energy, enabling grid stability, renewable energy integration, and reliable power supply across utility, commercial, and industrial applications. The Europe advanced energy storage systems market is projected to witness steady growth at a CAGR of 4.55% over 2026–2032. The region’s accelerating transition toward renewable energy sources is a key factor supporting market expansion. Increasing deployment of wind and solar power has heightened the need for flexible storage solutions that can balance intermittent generation and strengthen grid resilience. Additionally, supportive energy transition policies, decarbonization targets, and growing investments in modernizing electricity infrastructure are reinforcing demand for advanced energy storage technologies across Europe.

Key highlights of the Europe Advanced Energy Storage Systems Market:

- The market was valued at USD 2.87 Billion in 2025, is projected at USD 2.99 Billion in 2026, and is expected to reach USD 3.92 Billion by 2032.

- The market is forecast to grow at a CAGR of 4.55% during 2026-2032.

- Batteries segment led with a market share of approximately 56% in 2025, Pumped Hydro Storage are fastest growing segment with around 17% of the market.

- Short-Duration Storage led Storage Duration with 50% share in 2025, while Long-Duration Storage is the fastest-growing storage duration at 11.07% CAGR.

- Germany remained the leading country with 29% market share, Spain is the fastest growing country with CAGR 6.44%.

- The top-five companies held 26% share, indicating a competitive but not tightly concentrated structure.

- The strategic direction is shifting toward policy-compliant, software-optimised, containerised storage that can monetise flexibility, reduce curtailment, and support multi-hour dispatch.

Advanced Energy Storage Systems Market are strategically important because of their versatility. A single storage installation can stabilize grid frequency, absorb excess renewable generation, provide backup power during supply disruptions, and defer costly network upgrades. That breadth transforms energy storage from a specialized grid-balancing tool into a core infrastructure asset. As a result, utilities, transmission operators, and renewable energy developers are increasingly deploying storage across entire portfolios rather than limiting it to individual projects. The technology’s ability to address multiple operational challenges simultaneously makes it a recurring investment priority rather than a niche addition to the power system.

Grid resilience and energy security have quietly become the market’s strongest growth drivers. According to SolarPower Europe’s EU Battery Storage Market Review 2025, the European Union added 27.1 GWh of battery storage capacity in 2025, representing 45% year-on-year growth and marking the twelfth consecutive year of record deployment. Total installed battery storage capacity reached 77.3 GWh, reflecting the rapid scaling of storage assets needed to support increasingly renewable-heavy electricity systems. The report also highlights a growing shift toward utility-scale projects, reinforcing the view that storage is becoming a fundamental component of grid infrastructure market rather than a niche flexibility solution.

Additionally, deployment trends continue to strengthen the market outlook. According to the European Association for Storage of Energy (EASE), Europe surpassed 100 GW of installed energy storage capacity in 2025, with storage capacity exceeding the region’s nuclear generation capacity for the first time. Growing investments across battery, pumped hydro, thermal, and long-duration storage technologies underscore the sector’s expanding role in maintaining grid reliability and supporting renewable integration.

Through 2032, expect the market to tilt further toward scale, reliability, and system integration. As renewable energy deployment accelerates and electricity networks become more complex, storage will play an increasingly central role in balancing supply and demand. In short, the basis of competition is shifting from capacity additions to performance and reliability, a transition that structurally favors advanced energy storage solutions capable of delivering long-term grid stability and energy security.

Government Regulations Shaping the Europe Advanced Energy Storage Systems Market

Three major policy initiatives have accelerated investment in Europe advanced energy storage systems market. The European Green Deal, launched in December 2019, established the EU’s roadmap to achieve climate neutrality by 2050 and continues to drive investment in clean energy, grid modernization, and storage infrastructure. The Fit for 55 Package, introduced in July 2021, translated these ambitions into binding legislation by targeting a 55% reduction in greenhouse gas emissions by 2030, strengthening long-term demand for grid flexibility and balancing technologies. Meanwhile, the REPowerEU Plan, unveiled in May 2022, was designed to strengthen energy security and accelerate clean energy deployment. By the end of 2025, the EU had exceeded its REPowerEU solar target with 406 GW of installed solar capacity, while solar energy supplied approximately 13% of Europe’s electricity, creating additional requirements for energy storage systems. Together, these initiatives have expanded opportunities for battery energy storage systems, thermal storage, and other advanced storage technologies by supporting decarbonization, renewable integration, and resilient energy infrastructure across Europe. As solar and wind generation continue to expand under these initiatives, utilities and grid operators are increasingly investing in battery energy storage systems, thermal storage, and other advanced storage technologies to maintain grid stability, manage intermittency, and ensure reliable power supply.

Competitive Analysis")

Europe Advanced Energy Storage Systems Market Drivers

Accelerating Renewable Energy Integration

The rapid expansion of energy generation market across Europe is driving the need for advanced energy storage systems market. According to Eurostat, 47.5% of the European Union's gross electricity consumption came from renewable energy sources in 2024, up from 45.4% in 2023. The increasing share of intermittent renewable sources such as solar and wind creates a growing requirement for energy storage systems to balance supply and demand and maintain grid stability.

As renewable penetration continues to rise, energy storage technologies are becoming essential for managing fluctuations in power generation and reducing curtailment. Storage systems enable excess renewable electricity to be stored and deployed during periods of high demand, supporting the efficient integration of clean energy into the power network.

Restraints

Grid Expansion Bottlenecks

The rapid deployment of renewable energy and storage projects is increasing pressure on electricity networks across Europe Advanced Energy Storage Systems Market. According to the International Energy Agency (IEA), at least 3,000 GW of renewable power projects worldwide are waiting in grid connection queues, including 1,500 GW in advanced stages of development. Grid congestion and lengthy connection procedures are becoming major barriers to integrating new energy infrastructure, including advanced energy storage systems.

The effectiveness of energy storage deployment depends on the availability of modern and flexible grid infrastructure. Delays in transmission upgrades, interconnection projects, and grid expansion can slow the integration of storage assets, limiting their ability to support renewable energy deployment and improve system reliability across Europe.

Recent Trends

Growing Deployment of Utility-Scale Storage Projects

The increasing deployment of large-scale energy storage projects is emerging as a major trend across Europe Advanced Energy Storage Systems Market. According to the European Commission, 4.9 GW (12.1 GWh) of utility-scale energy storage capacity was deployed in Europe during 2024, bringing total utility-scale storage capacity to more than 13 GW. This reflects the growing role of storage technologies in supporting grid flexibility and renewable energy integration.

Utilities and grid operators are increasingly investing in battery storage, thermal energy storage, and other advanced technologies to enhance system reliability. The expansion of utility-scale installations demonstrates the transition of energy storage from a supporting technology to a critical component of Europe's evolving energy infrastructure.

Advanced LFP Storage Platforms

The technical direction is toward containerised, liquid-cooled, software-controlled systems that are easier to standardise across markets. LFP chemistry is gaining share because it suits frequent cycling and cost-sensitive grid applications, while digital controls are improving dispatch, monitoring, and asset availability. That makes performance repeatable across utility, industrial, and microgrid use cases in Advanced Energy Storage Systems Market.

Tesla’s Megapack, Sungrow’s PowerTitan, Hitachi Energy’s PCS platform, and LG Energy Solution’s next-generation LFP ESS all show the same pattern: tighter system integration, better thermal management, and faster installation. These features improve project economics and strengthen premium positioning for vendors with strong engineering support.

Future Opportunities

Expanding Renewable Energy Targets

Europe's ambitious renewable energy goals are creating significant opportunities for Europe Advanced Energy Storage Systems Market. According to the European Environment Agency (EEA), renewable energy accounted for 25.2% of final energy consumption in the European Union in 2024. At the same time, the revised Renewable Energy Directive establishes a binding target of 42.5% renewable energy by 2030, requiring greater flexibility and balancing capabilities across the power system.

As governments and utilities work toward higher renewable energy penetration, demand for grid-scale, long-duration, and distributed storage solutions is increasing. This creates opportunities for energy storage developers, technology providers, and infrastructure investors to support Europe's transition toward a more resilient and low-carbon energy system.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Europe Advanced Energy Storage Systems Market Segmentation Analysis

By Technology

- Batteries

- Thermal Energy Storage

- Pumped Hydro Storage

- Compressed Air Energy Storage

- Flywheel Energy Storage

- Other Advanced Energy Storage Technologies

Batteries Segment Leads, Pumped Hydro Storage are Fastest Growing

The Batteries segment led the Europe Advanced Energy Storage Systems Market with a market share of approximately 56%. The segment’s dominance is supported by increasing deployment of battery energy storage systems alongside renewable power projects, particularly wind and solar installations. Batteries offer rapid response capabilities, modular deployment, and improving cost efficiency, making them suitable for grid balancing and energy management applications. Growing investments in utility-scale storage facilities and supportive government policies promoting clean energy integration have further accelerated battery adoption across Europe. Their flexibility and scalability continue to position batteries as the preferred technology for modern energy storage requirements.

By comparison, Pumped Hydro Storage accounted for around 17% of the market. Although it remains an important technology for large-scale energy storage, its growth is constrained by high capital costs, long development timelines, and geographical limitations. Batteries maintain a significant advantage due to easier installation and wider application across commercial, industrial, and utility sectors. However, pumped hydro systems provide longer-duration storage and substantial capacity for grid reliability. Together, these technologies create a balanced storage ecosystem, with batteries leading deployment volumes and pumped hydro supporting long-term energy balancing needs.

Segmentation Overview")

By Storage Duration

- Short-Duration Storage

- Medium-Duration Storage

- Long-Duration Storage

Short-Duration Storage Holds Scale; Long-Duration Storage Drives Growth

Short-Duration Storage held the largest share of the Europe Advanced Energy Storage Systems Market, accounting for approximately 50% of the market in 2025. Its leadership is driven by widespread deployment of lithium-ion battery energy storage systems for frequency regulation, peak shaving, renewable energy integration, and grid-balancing applications. As Europe expands solar and wind capacity, utilities increasingly rely on short-duration storage due to its fast response time, high efficiency, and improving cost competitiveness. Compared with long-duration solutions, these systems are more commercially mature and require lower upfront investment, supporting broader adoption across utility, commercial, and industrial projects.

Long-Duration Storage, holding around 19% of the market, is the fastest-growing segment. While its current adoption remains lower than short-duration storage, increasing renewable penetration is creating demand for technologies capable of storing energy for several hours or days. Flow batteries, thermal energy storage, compressed air energy storage, and advanced pumped hydro systems offer greater energy-shifting capability than short-duration systems, making them essential for grid resilience, seasonal balancing, and long-term decarbonization goals. As Europe pursues deeper renewable integration, investment in long-duration storage is expected to accelerate significantly.

Europe Advanced Energy Storage Systems Market Country Analysis

Germany Leads on Scale, Spain Accelerates on Growth

Germany led the Europe Advanced Energy Storage Systems Market with a 29% market share in 2025, supported by strong regulatory frameworks and long-term energy transition policies. The country’s Energiewende strategy has encouraged large-scale deployment of renewable energy and energy storage solutions through funding programs, grid modernization initiatives, and incentives for battery installations. Germany’s established renewable energy sector, combined with supportive regulations for grid flexibility and decarbonization, has created a mature market environment for advanced energy storage technologies. These policies have enabled widespread adoption of battery storage systems to improve grid reliability and renewable energy integration.

Spain, projected to grow at a CAGR of 6.44% during 2026-2032, is benefiting from policy reforms aimed at accelerating renewable energy deployment and storage capacity expansion. The country’s National Energy and Climate Plan promotes energy storage as a critical component of its clean energy transition, supported by streamlined project approvals and investment incentives. Compared with Germany’s mature policy landscape, Spain’s emerging regulatory framework is driving faster market expansion. While Germany maintains leadership through established infrastructure and long-standing government support, Spain is experiencing stronger growth momentum due to aggressive renewable energy targets and increasing storage investments.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Europe Advanced Energy Storage Systems Market Competitive Landscape

The Europe Advanced Energy Storage Systems Market is moderately fragmented, with the top five companies accounting for approximately 26% of total revenue, concentrated enough to feature established leaders yet open enough for technology specialists and regional providers to compete. Buyers prioritize system reliability, performance, and long-term operational support as storage becomes increasingly critical to grid stability and renewable integration. Technology expertise, project execution, and software capabilities have become key differentiators. Large players lead through scale and integrated solutions, while smaller competitors expand adoption by serving niche applications and region-specific energy storage requirements.

Key Companies in the Europe Advanced Energy Storage Systems Market

- Siemens Energy AG

- ABB Ltd.

- Saft Groupe S.A. (TotalEnergies SE)

- Fluence Energy Inc.

- VARTA AG

- Leclanche SA

- Alfen N.V.

- EnerSys

- Eaton Corporation plc

- Hitachi Energy Ltd.

- Schneider Electric SE

- TESVOLT AG

Company Profiles

The leading suppliers are profiled below to clarify how each competes on technology, scale, geography, and energy-storage specialization.

Leclanché SA: Leclanché supplies lithium-ion battery energy storage systems for utility-scale, commercial, industrial, and microgrid applications. The company specializes in integrated storage solutions combining battery technology, energy management software, and system engineering capabilities. Its focus on grid stabilization, renewable integration, and hybrid energy projects has made it a recognized participant in Europe's advanced energy storage sector.

Alfen N.V.: Alfen serves the market through its TheBattery energy storage platform, supplying solutions for grid balancing, renewable energy integration, and industrial energy management. The company combines storage systems with smart-grid infrastructure and EV-charging technologies, allowing customers to optimize energy flexibility and network utilization. Alfen has deployed numerous storage projects across European electricity markets and remains a key supplier to utilities and commercial energy users.

EnerSys: Headquartered in Reading, Pennsylvania, United States, EnerSys participates in the European market through advanced battery systems, power conversion technologies, and energy storage solutions for industrial and utility applications. The company operates manufacturing facilities in multiple European countries, including Germany, France, Spain, and Poland, supporting regional demand for energy storage and critical-power infrastructure. Its expertise in battery technology, power systems, and energy management solutions enables deployment across utility, telecommunications, and industrial markets. Supported by an established European production footprint and technical service network, EnerSys remains a notable supplier within the region's advanced energy storage systems market.

Siemens Energy AG: Siemens Energy supplies grid-scale battery energy storage systems, digital grid solutions, and integrated energy infrastructure. The company's storage portfolio spans batteries, thermal storage, and other emerging technologies through its "Future of Storage" initiative. Siemens has also supported large-scale storage projects, including a 100 MW/200 MWh battery storage facility in Germany designed to enhance renewable energy utilization and grid stability. More recently, Siemens participated in the Nurmijärvi Battery Energy Storage System in Finland, providing electrification, energy management software, and lifecycle services.

ABB Ltd.: ABB competes through battery energy storage integration, power conversion technologies, and grid-management solutions. The company specializes in electrification, automation, and digital energy platforms that improve storage efficiency and operational performance. ABB's storage offerings support utilities, industrial facilities, and renewable energy developers seeking greater grid flexibility and energy resilience. Its extensive engineering expertise and broad European customer base position the company as a prominent supplier within the advanced energy storage systems market.

Recent Developments in the Europe Advanced Energy Storage Systems Industry

- 2026-Schneider Electric introduced its DC-Coupled Megawatt Charging Station at Power2Drive Europe 2026, designed to integrate battery energy storage systems, renewable energy sources, and high-power EV charging infrastructure through a native DC architecture. The solution enables fleet operators and commercial vehicle charging hubs to reduce grid dependency while optimizing energy storage utilization and renewable energy consumption. The development supports Europe's growing demand for advanced energy storage and electrification infrastructure across transport and logistics applications.

- 2026-Alfen deployed its 15 MW/30 MWh BESS Apeldoorn battery energy storage system in the Netherlands to enhance grid flexibility and support energy market participation. The company also expanded the availability of its mobile battery storage solutions through a partnership with DLL, enabling broader deployment of battery energy storage assets across European markets. The developments strengthen Europe's grid-balancing capabilities and accelerate the adoption of advanced energy storage systems for renewable energy integration.

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- Europe Advanced Energy Storage Systems Market Policies, Regulations, and Standards

- Europe Advanced Energy Storage Systems Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- Europe Advanced Energy Storage Systems Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold in Megawatt (MW)

- Market Segmentation & Growth Outlook

- By Technology

- Batteries- Market Insights and Forecast 2022-2032, USD Million

- Thermal Energy Storage- Market Insights and Forecast 2022-2032, USD Million

- Pumped Hydro Storage- Market Insights and Forecast 2022-2032, USD Million

- Compressed Air Energy Storage- Market Insights and Forecast 2022-2032, USD Million

- Flywheel Energy Storage- Market Insights and Forecast 2022-2032, USD Million

- Other Advanced Energy Storage Technologies- Market Insights and Forecast 2022-2032, USD Million

- By Application

- Grid Storage- Market Insights and Forecast 2022-2032, USD Million

- Transportation- Market Insights and Forecast 2022-2032, USD Million

- Renewable Energy Integration- Market Insights and Forecast 2022-2032, USD Million

- Backup Power- Market Insights and Forecast 2022-2032, USD Million

- Microgrids- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By End Use

- Residential- Market Insights and Forecast 2022-2032, USD Million

- Commercial- Market Insights and Forecast 2022-2032, USD Million

- Industrial- Market Insights and Forecast 2022-2032, USD Million

- Utility- Market Insights and Forecast 2022-2032, USD Million

- By Storage Duration

- Short-Duration Storage- Market Insights and Forecast 2022-2032, USD Million

- Medium-Duration Storage- Market Insights and Forecast 2022-2032, USD Million

- Long-Duration Storage- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel

- Retail Online- Market Insights and Forecast 2022-2032, USD Million

- Company-Owned Websites- Market Insights and Forecast 2022-2032, USD Million

- E-Commerce Platforms- Market Insights and Forecast 2022-2032, USD Million

- Online Energy Equipment Stores- Market Insights and Forecast 2022-2032, USD Million

- Online Electrical Supply Portals- Market Insights and Forecast 2022-2032, USD Million

- B2B Procurement Platforms- Market Insights and Forecast 2022-2032, USD Million

- Retail Offline- Market Insights and Forecast 2022-2032, USD Million

- Direct Sales- Market Insights and Forecast 2022-2032, USD Million

- Energy Equipment Distributors- Market Insights and Forecast 2022-2032, USD Million

- Electrical Equipment Dealers- Market Insights and Forecast 2022-2032, USD Million

- System Integrators- Market Insights and Forecast 2022-2032, USD Million

- EPC Contractors- Market Insights and Forecast 2022-2032, USD Million

- Utility Procurement Contracts- Market Insights and Forecast 2022-2032, USD Million

- Authorized Dealers- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- Retail Online- Market Insights and Forecast 2022-2032, USD Million

- By Country

- Germany

- The UK

- France

- Spain

- Italy

- Benelux

- Nordic

- Russia

- Rest of Europe

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Technology

- Market Size & Growth Outlook

- Germany Advanced Energy Storage Systems Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold in Megawatt (MW)

- Market Segmentation & Growth Outlook

- By Technology- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By End Use- Market Insights and Forecast 2022-2032, USD Million

- By Storage Duration- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- The UK Advanced Energy Storage Systems Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold in Megawatt (MW)

- Market Segmentation & Growth Outlook

- By Technology- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By End Use- Market Insights and Forecast 2022-2032, USD Million

- By Storage Duration- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Spain Advanced Energy Storage Systems Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold in Megawatt (MW)

- Market Segmentation & Growth Outlook

- By Technology- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By End Use- Market Insights and Forecast 2022-2032, USD Million

- By Storage Duration- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Italy Advanced Energy Storage Systems Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold in Megawatt (MW)

- Market Segmentation & Growth Outlook

- By Technology- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By End Use- Market Insights and Forecast 2022-2032, USD Million

- By Storage Duration- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Netherlands Advanced Energy Storage Systems Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold in Megawatt (MW)

- Market Segmentation & Growth Outlook

- By Technology- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By End Use- Market Insights and Forecast 2022-2032, USD Million

- By Storage Duration- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- Siemens Energy AG

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- ABB Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Saft Groupe S.A. (TotalEnergies SE)

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Fluence Energy Inc.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- VARTA AG

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Leclanche SA

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Alfen N.V.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- EnerSys

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Eaton Corporation plc

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Hitachi Energy Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Schneider Electric SE

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- TESVOLT AG

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Siemens Energy AG

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Technology |

|

| By Application |

|

| By End Use |

|

| By Storage Duration |

|

| By Sales Channel |

|

| By Country |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.