Egypt Juice Market Report: Trends, Growth and Forecast (2026-2032)

By Category (100% Juice (Not from Concentrate, Reconstituted), Juice Drinks (up to 24% Juice), Nectars (High Concentration (40% to 50% fruit content), Medium Concentration (30% to 39% fruit content), Low Concentration (25% to 29% fruit content)), Vegetable Juice, Fruit and Vegetable Blends), By Nature (Conventional, Organic), By Packaging Material (Plastic, Glass, Metal, Others), By Packaging Type (PET Bottles, Aseptic Packages (Cartons), Glass Bottles, Metal Cans, Disposable Cups & Pouches), By Sales Channel (Off-Trade (Hypermarkets/ Supermarkets, Retail Outlets, Convenience Stores, Online Platforms), On-Trade), By Region (Cairo, Alexandria, Others) ... Read more

|

Major Players

|

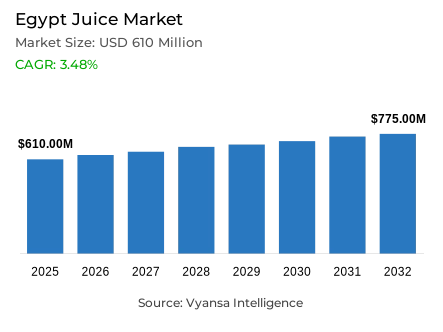

Egypt Juice Market Statistics and Insights, 2026

- Market Size Statistics

- Juice market size in Egypt was estimated at USD 610 million in 2025.

- The market size is expected to grow to USD 775 million by 2032.

- Market to register a CAGR of around 3.48% during 2026-32.

- Category Shares

- Juice drinks (up to 24% juice) grabbed market share of 75%.

- Competition

- More than 20 companies are actively engaged in producing juice in Egypt.

- Top 5 companies acquired around 75% of the market share.

- Faragalla Group, Aujan Soft Drinks Industries, Egyptian Canning Co Best SAE, Juhayna Food Industries, International Co for Agro Industrial Projects (Beyti) SAE etc., are few of the top companies.

- Sales Channel

- Off-trade grabbed 90% of the market.

Egypt Juice Market Outlook

The Egypt juice market is going through a phase of polarization, which is fuelled by the high inflationary forces and increased health consciousness. Although the high retail prices have compelled most households to focus on affordability, there is also an increase in the demand of high quality and premium juice experiences among those with greater purchasing power. The market is projected to be 610 million in 2025 and 775 million in 2032 with a CAGR of approximately 3.48% in the 2026-2032.

The main force of volume is budget-friendly, with end user trading down to cope with the increasing cost of living. Small pack sizes like 200ml and 235ml with prices as low as EGP5 have become necessary to ensure accessibility to the entire population. Juice Drinks (up to 24% Juice) are the staple of this category, capturing 75% of the market share. On the other hand, nectars are undergoing a downturn because they are caught between the price of juice drinks and the better health image of 100% fruit juices.

The future of the category will be determined by digital innovation and strategic retail partnerships. The major players such as Juhayna Food Industries are using social media and other applications such as Talabat to access the young population of Egypt especially in high-end products such as Pure. Greater partnerships between brands and contemporary retailers, including the partnership between Juhayna and Gourmet Egypt, are increasingly essential to emphasize natural, not from concentrate (NFC) products and cold-pressed blends that focus on clean labels.

The distribution environment is still very concentrated in the home-consumption segment with the Off-Trade channels taking 90% of the market. Small local grocers remain the leaders because of their significance in impulse buying and extensive geographic coverage. On-trade sales will not perform well, but e-commerce is becoming a vibrant trend in such big cities as Cairo. With the evolution of delivery networks, online platforms are simplifying the process of niche local brands reaching health-conscious end user who want additive-free options

Egypt Juice Market Growth Driver

Inflation-Driven Value Seeking Sustaining Everyday Demand for Affordable Juice Drinks

Egypt end user remain value-conscious due to high inflation, and thus, low-cost juice beverages remain a low-risk, low-frequency purchase in their daily lives. Central Bank of Egypt records annual urban headline inflation of 24.0% in January 2025, which indicates that the household budgets are still under pressure and trading down in packaged beverages is strengthened.

This setting favours high demand of low-juice-content beverages in small packs via neighbourhood grocers, where convenience and cost are paramount. Daily purchases are controlled by traditional grocery stores, and thus brands with extensive distribution are repeat impulse buyers in Cairo, Alexandria, and other major cities. The category is resilient due to wide availability and accessible price points even in times when retail prices increase. Juice drinks are also a reliable, low-cost soft drink substitute, and 100% juice is also targeted at health-conscious end user who are willing to pay more.

Egypt Juice Market Challenge

Prolonged Core Inflation Constraining Premiumisation and Innovation Headroom

Constant price pressure restricts the extent to which end user will shift to high-end juice, despite their willingness to consume healthier products. According to the Central Bank of Egypt, core inflation is 22.6% in January 2025, meaning that the underlying costs remain high and not just a temporary fluctuation but continue to put purchasing power under pressure.

In the case of juice producers, the risk of frequent price resets and heavy selling through promotion increases in the same environment, particularly with 100% juice and not-from-concentrate products, which are more expensive. With shoppers being very price sensitive to minor price adjustments, brands have a limited time to invest in innovation, packaging improvements and increased diversity in weaker subcategories like nectars. This complicates the establishment of stable high-end demand and may drive end user back to less expensive juice beverages.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Egypt Juice Market Trend

Rising Health Risk Awareness Accelerating the Shift Toward Cleaner and Less-Processed Juice

Everyday food and beverage decisions are being more and more associated with long-term health by end user, which boosts the appeal of cleaner juice options. According to the World Health Organization Eastern Mediterranean Regional Office, 82% of all deaths in Egypt are estimated to be caused by noncommunicable diseases, which keeps the risks associated with diet in the limelight.

Shoppers with the means to do so in turn move to 100% juice and not-from-concentrate versions that are more natural and quality, which is the polarisation. No preservatives and no additives labels are more important, and cold-pressed and clean-label positioning are used by niche local brands to gain credibility. Simultaneously, nectars become less relevant since they are frequently viewed as more processed, which puts pressure on brands to renew ingredients and messages.

Egypt Juice Market Opportunity

Widespread Mobile Internet Penetration Expanding Digital Commerce and Direct-to-Consumer Reach

The digital channels are a viable growth driver of juice brands due to high mobile connectivity, which facilitates the transition to social media campaigns and app-based promotions. According to the data provided by the Ministry of Communications and Information Technology based on the data of the National Telecom Regulatory Authority, the%age of mobile internet users is 75.59% of all mobile subscriptions in October 2025.

Such access assists brands to scale online discovery, targeted offers, and delivery partnerships that deliver both value packs and premium 100% juice to end user without depending solely on shelf visibility. The availability of third-party platforms and retailer e-commerce in large cities facilitates the access of niche local products to health-led buyers, and the dominant players can defend entry price points of juice drinks through digital promotions. Enhanced digital presence also reinforces contemporary retail partnerships that showcase products and create equity.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Egypt Juice Market Segmentation Analysis

By Category

- 100% Juice

- Not from Concentrate

- Reconstituted

- Juice Drinks (up to 24% Juice)

- Nectars

- High Concentration (40% to 50% fruit content)

- Medium Concentration (30% to 39% fruit content)

- Low Concentration (25% to 29% fruit content)

- Vegetable Juice

- Fruit and Vegetable Blends

The segment has the highest share around the category in the Egypt juice market, where Juice Drinks (up to 24% Juice) grabbed a market share of 75%. This dominant position is largely due to the extreme price sensitivity caused by high inflation and reduced consumer purchasing power. These products have become the go-to choice for the majority of the population, offering a refreshing and flavorful experience at a fraction of the cost of premium alternatives. Smaller, budget-friendly packs are particularly successful in maintaining high volume sales across all demographic groups.

Despite the rise in health awareness, juice drinks remain resilient because they fulfill the need for affordable soft drinks. While health-conscious end user are moving toward 100% juice, the sheer volume of the juice drinks segment is sustained by its wide availability in traditional retail. Leading brands like Beyti for Tropicana have secured strong positions here by utilizing massive distribution networks to ensure these affordable options are visible in every corner of the country, from Cairo to smaller regional cities.

By Sales Channel

- Off-Trade

- Hypermarkets/ Supermarkets

- Retail Outlets

- Convenience Stores

- Online Platforms

- On-Trade

The segment has the highest share around the Sales Channel is Off-Trade, which grabbed 90% of the market. This overwhelming majority reflects the fact that juice in Egypt is primarily a retail-driven product, with the vast majority of consumption occurring within the home. Small local grocers are the most influential part of this channel, serving as the primary destination for everyday shopping and impulse purchases. Their ability to reach end user in high-density residential areas makes them the essential link for brands looking to maintain steady volume growth.

While traditional grocery stores lead the way, modern retail and e-commerce are becoming increasingly important sub-channels. Deeper partnerships between brands and high-end retailers are helping to boost the visibility of premium 100% juices, while third-party delivery apps are making online shopping a habitual choice in major urban centers. Despite these modern shifts, the off-trade channel’s dominance is expected to remain unchallenged through 2032, as it continues to offer the most convenient and value-driven shopping experience for Egypt households.

List of Companies Covered in Egypt Juice Market

The companies listed below are highly influential in the Egypt juice market, with a significant market share and a strong impact on industry developments.

- Faragalla Group

- Aujan Soft Drinks Industries

- Egyptian Canning Co Best SAE

- Juhayna Food Industries

- International Co for Agro Industrial Projects (Beyti) SAE

- Alexandria Agriculture Co

- Arabian Food & Dairy Factories Co

- Al Sakr for Food Industries

- Binzagr CO-RO Ltd

- International Dairy & Juice Ltd

Competitive Landscape

Egypt’s juice market in 2025 is highly polarised, dominated by a few large players competing on affordability and distribution, alongside emerging niche brands focused on health. Juhayna Food Industries leads the category, driven by strong nationwide distribution and brand equity in 100% juice through Pure, positioning itself as a premium, health oriented option. Beyti for Tropicana ranks second, holding a strong position in juice drinks up to 24% juice by leveraging competitive pricing, small pack sizes, and extensive reach through traditional grocery retailers. Alexandria Agriculture competes in 100% juice with Lamar, adding pressure in the premium segment. Indirect competition comes from other low cost soft drinks amid inflation. Key differentiation opportunities lie in affordable healthier formulations, not from concentrate offerings, clean label positioning, and stronger digital and e-commerce engagement.

Frequently Asked Questions

Related Report

1. Market Segmentation

1.1. Research Scope

1.2. Research Methodology

1.3. Definitions and Assumptions

2. Executive Summary

3. Egypt Juice Market Policies, Regulations, and Standards

4. Egypt Juice Market Dynamics

4.1. Growth Factors

4.2. Challenges

4.3. Trends

4.4. Opportunities

5. Egypt Juice Market Statistics, 2022-2032F

5.1. Market Size & Growth Outlook

5.1.1.By Revenues in USD Million

5.1.2.By Quantity Sold in Million Litres

5.2. Market Segmentation & Growth Outlook

5.2.1.By Category

5.2.1.1. 100% Juice- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.1. Not from Concentrate- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.2. Reconstituted- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2. Juice Drinks (up to 24% Juice)- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3. Nectars- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3.1. High Concentration (40% to 50% fruit content)- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3.2. Medium Concentration (30% to 39% fruit content)- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3.3. Low Concentration (25% to 29% fruit content)- Market Insights and Forecast 2022-2032, USD Million

5.2.1.4. Vegetable Juice- Market Insights and Forecast 2022-2032, USD Million

5.2.1.5. Fruit and Vegetable Blends- Market Insights and Forecast 2022-2032, USD Million

5.2.2.By Nature

5.2.2.1. Conventional- Market Insights and Forecast 2022-2032, USD Million

5.2.2.2. Organic- Market Insights and Forecast 2022-2032, USD Million

5.2.3.By Packaging Material

5.2.3.1. Plastic- Market Insights and Forecast 2022-2032, USD Million

5.2.3.2. Glass- Market Insights and Forecast 2022-2032, USD Million

5.2.3.3. Metal- Market Insights and Forecast 2022-2032, USD Million

5.2.3.4. Others- Market Insights and Forecast 2022-2032, USD Million

5.2.4.By Packaging Type

5.2.4.1. PET Bottles- Market Insights and Forecast 2022-2032, USD Million

5.2.4.2. Aseptic Packages (Cartons)- Market Insights and Forecast 2022-2032, USD Million

5.2.4.3. Glass Bottles- Market Insights and Forecast 2022-2032, USD Million

5.2.4.4. Metal Cans- Market Insights and Forecast 2022-2032, USD Million

5.2.4.5. Disposable Cups & Pouches- Market Insights and Forecast 2022-2032, USD Million

5.2.5.By Sales Channel

5.2.5.1. Off-Trade- Market Insights and Forecast 2022-2032, USD Million

5.2.5.1.1. Hypermarkets/ Supermarkets - Market Insights and Forecast 2022-2032, USD Million

5.2.5.1.2. Retail Outlets - Market Insights and Forecast 2022-2032, USD Million

5.2.5.1.3. Convenience Stores- Market Insights and Forecast 2022-2032, USD Million

5.2.5.1.4. Online Platforms- Market Insights and Forecast 2022-2032, USD Million

5.2.5.2. On-Trade- Market Insights and Forecast 2022-2032, USD Million

5.2.6.By Region

5.2.6.1. Cairo

5.2.6.2. Alexandria

5.2.6.3. Others

5.2.7.By Competitors

5.2.7.1. Competition Characteristics

5.2.7.2. Market Share & Analysis

6. Egypt 100% Juice Market Statistics, 2022-2032

6.1. Market Size & Growth Outlook

6.1.1.By Revenues in USD Million

6.1.2.By Quantity Sold in Million Litres

6.2. Market Segmentation & Growth Outlook

6.2.1.By Nature- Market Insights and Forecast 2022-2032, USD Million

6.2.2.By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

6.2.3.By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

6.2.4.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

6.2.5.By Region- Market Insights and Forecast 2022-2032, USD Million

7. Egypt Juice Drinks (up to 24% Juice) Market Statistics, 2022-2032

7.1. Market Size & Growth Outlook

7.1.1.By Revenues in USD Million

7.1.2.By Quantity Sold in Million Litres

7.2. Market Segmentation & Growth Outlook

7.2.1.By Nature- Market Insights and Forecast 2022-2032, USD Million

7.2.2.By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

7.2.3.By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

7.2.4.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

7.2.5.By Region- Market Insights and Forecast 2022-2032, USD Million

8. Egypt Nectars Market Statistics, 2022-2032

8.1. Market Size & Growth Outlook

8.1.1.By Revenues in USD Million

8.1.2.By Quantity Sold in Million Litres

8.2. Market Segmentation & Growth Outlook

8.2.1.By Nature- Market Insights and Forecast 2022-2032, USD Million

8.2.2.By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

8.2.3.By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

8.2.4.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

8.2.5.By Region- Market Insights and Forecast 2022-2032, USD Million

9. Egypt Vegetable Juice Market Statistics, 2022-2032

9.1. Market Size & Growth Outlook

9.1.1.By Revenues in USD Million

9.1.2.By Quantity Sold in Million Litres

9.2. Market Segmentation & Growth Outlook

9.2.1.By Nature- Market Insights and Forecast 2022-2032, USD Million

9.2.2.By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

9.2.3.By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

9.2.4.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

9.2.5.By Region- Market Insights and Forecast 2022-2032, USD Million

10. Egypt Fruit and Vegetable Blends Market Statistics, 2022-2032

10.1. Market Size & Growth Outlook

10.1.1. By Revenues in USD Million

10.1.2. By Quantity Sold in Million Litres

10.2. Market Segmentation & Growth Outlook

10.2.1. By Nature- Market Insights and Forecast 2022-2032, USD Million

10.2.2. By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

10.2.3. By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

10.2.4. By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

10.2.5. By Region- Market Insights and Forecast 2022-2032, USD Million

11. Competitive Outlook

11.1. Company Profiles

11.1.1. Juhayna Food Industries

11.1.1.1. Business Description

11.1.1.2. Product Portfolio

11.1.1.3. Collaborations & Alliances

11.1.1.4. Recent Developments

11.1.1.5. Financial Details

11.1.1.6. Others

11.1.2. International Co for Agro Industrial Projects (Beyti) SAE

11.1.2.1. Business Description

11.1.2.2. Product Portfolio

11.1.2.3. Collaborations & Alliances

11.1.2.4. Recent Developments

11.1.2.5. Financial Details

11.1.2.6. Others

11.1.3. Alexandria Agriculture Co

11.1.3.1. Business Description

11.1.3.2. Product Portfolio

11.1.3.3. Collaborations & Alliances

11.1.3.4. Recent Developments

11.1.3.5. Financial Details

11.1.3.6. Others

11.1.4. Arabian Food & Dairy Factories Co

11.1.4.1. Business Description

11.1.4.2. Product Portfolio

11.1.4.3. Collaborations & Alliances

11.1.4.4. Recent Developments

11.1.4.5. Financial Details

11.1.4.6. Others

11.1.5. Al Sakr for Food Industries

11.1.5.1. Business Description

11.1.5.2. Product Portfolio

11.1.5.3. Collaborations & Alliances

11.1.5.4. Recent Developments

11.1.5.5. Financial Details

11.1.5.6. Others

11.1.6. Faragalla Group

11.1.6.1. Business Description

11.1.6.2. Product Portfolio

11.1.6.3. Collaborations & Alliances

11.1.6.4. Recent Developments

11.1.6.5. Financial Details

11.1.6.6. Others

11.1.7. Aujan Soft Drinks Industries

11.1.7.1. Business Description

11.1.7.2. Product Portfolio

11.1.7.3. Collaborations & Alliances

11.1.7.4. Recent Developments

11.1.7.5. Financial Details

11.1.7.6. Others

11.1.8. Egyptian Canning Co Best SAE

11.1.8.1. Business Description

11.1.8.2. Product Portfolio

11.1.8.3. Collaborations & Alliances

11.1.8.4. Recent Developments

11.1.8.5. Financial Details

11.1.8.6. Others

11.1.9. Binzagr CO-RO Ltd

11.1.9.1. Business Description

11.1.9.2. Product Portfolio

11.1.9.3. Collaborations & Alliances

11.1.9.4. Recent Developments

11.1.9.5. Financial Details

11.1.9.6. Others

11.1.10. International Dairy & Juice Ltd

11.1.10.1.Business Description

11.1.10.2.Product Portfolio

11.1.10.3.Collaborations & Alliances

11.1.10.4.Recent Developments

11.1.10.5.Financial Details

11.1.10.6.Others

12. Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Category |

|

| By Nature |

|

| By Packaging Material |

|

| By Packaging Type |

|

| By Sales Channel |

|

| By Region |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.