Dominican Republic Juice Market Report: Trends, Growth and Forecast (2026-2032)

By Category (100% Juice (Not from Concentrate, Reconstituted), Juice Drinks (up to 24% Juice), Nectars (High Concentration (40% to 50% fruit content), Medium Concentration (30% to 39% fruit content), Low Concentration (25% to 29% fruit content)), Vegetable Juice, Fruit and Vegetable Blends), By Nature (Conventional, Organic), By Packaging Material (Plastic, Glass, Metal, Others), By Packaging Type (PET Bottles, Aseptic Packages (Cartons), Glass Bottles, Metal Cans, Disposable Cups & Pouches), By Sales Channel (Off-Trade (Hypermarkets/ Supermarkets, Retail Outlets, Convenience Stores, Online Platforms), On-Trade) ... Read more

|

Major Players

|

Dominican Republic Juice Market Statistics and Insights, 2026

- Market Size Statistics

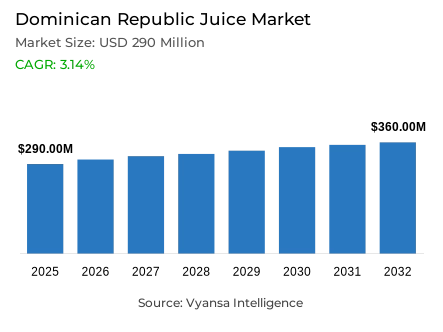

- Juice market size in Dominican Republic was estimated at USD 290 million in 2025.

- The market size is expected to grow to USD 360 million by 2032.

- Market to register a CAGR of around 3.14% during 2026-32.

- Category Shares

- Nectars grabbed market share of 45%.

- Competition

- More than 10 companies are actively engaged in producing juice in Dominican Republic.

- Top 5 companies acquired around 85% of the market share.

- Distribuidora Corripio CxA, Interfoods Dominicana SA, Grupo Jumex SA de CV, Pasteurizadora Rica SA, Parmalat Dominicana SA etc., are few of the top companies.

- Sales Channel

- Off-trade grabbed 85% of the market.

Dominican Republic Juice Market Outlook

The Dominican republic juice market has a distinct balance between nutritional perceptions and an increasing need of functional hydration in its juice market with its value projected to be USD 290 million in 2025. It is estimated that the market will grow to USD 360 million by 2032 with a CAGR of about 3.14% in the 2026-2032 period. Although juices will continue to be a staple due to their fruity taste and local appeal, the merket is experiencing a change as more end user are shifting to lighter and more refreshing beverages like flavored waters and isotonic beverages, especially with the increasing heat waves caused by climate changes.

Although the growth rate in traditional categories is slowing, the market is changing with premiumisation and targeted health claims. Local brands are using cold-press technology to preserve vitamins and minerals in a better way, attracting a niche but expanding group of health-conscious urbanites. Moreover, product innovation is devoted to particular functions, including stress reduction and cardiovascular support, which reflects the trends of personalised nutrition in the world. This is a strategic move to reverse the declining view of juice as something that is naturally healthy because of its sugar content.

The changes in generations also create new consumption moments, especially among younger end user. With Generation Z abandoning the conventional alcoholic beverages, there is a chance that juices can be marketed as base components of fancy mocktails and alcohol-free social drinks. This shift will enable juice to fill a new niche between regular drinks and high-end social drinks, which may tap into the sensory-driven preferences of the younger generation who want to experience something memorable without alcohol.

The local giant Pasteurizadora Rica still dominates the competitive environment, taking advantage of its extensive distribution network and 100% natural claims. Nonetheless, foreign brands like Del Valle are actively penetrating the nectar market. As nectars take a 45% market share and off-trade channel takes 85% of the sales, the market is set to experience a stable growth with a mix of traditional neighbourhood distribution and modern, tourism-driven foodservice growth.

Dominican Republic Juice Market Growth Driver

Strong Local Fruit Supply Reinforcing Consumer Trust in Natural and Familiar Juice Choices

The juice demand stays steady as a number of end user still consider it as a drink that is nutritious and tasty. Local tastes are associated with fruit flavors, and the brands have an advantage when they can introduce juice as a familiar product that can be incorporated into everyday life, especially among families and children.

This need is supported by a strong local fruit base that underpins made from fruit messages. According to the Ministry of Agriculture, the Oficina Nacional de Estadisticas reports 2,850,420.6 metric tons of fruit crop production in January to June 2025. This richness of supply allows brands to sustain a high product range and depend on local sourcing indicators that end user equate with freshness and authenticity.

Dominican Republic Juice Market Challenge

Climate-Induced Agricultural Disruptions Sustaining Upward Cost and Pricing Pressures

Juices face a clear challenge when weather shocks interfering with agricultural production and increasing expenses. The volatility of raw-materials as a limitation, and this is important since the cost of inputs is rapidly increasing, and this increases the price of juice, and it becomes more difficult to compete with cheaper hydration-based substitutes.

Recent inflation statistics show how agricultural disruption is converted to price pressure. According to the Banco Central de la República Dominicana, the consumer price index increased 0.71% in November 2025, with food and non-alcoholic beverages contributing 71.53% of that inflation, which was caused by crops damaged by heavy October rains and Storm Melissa. According to the same report, the year-on-year inflation stands at 4.81% between November 2024 and November 2025.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Dominican Republic Juice Market Trend

Rising Preference for Hydration-First Beverages Accelerating the Shift Toward Plant Waters

The trends that can be observed is the movement towards lighter, thirst-quenching beverages, with coconut water and other plant waters becoming increasingly popular as hydration plus. Coconut water as a natural hydration with electrolytes, which appeals to end user who want to feel refreshed without the weight of traditional juice. Both supply and climatic context support this trend. According to the Oficina Nacional de Estadisticas, coconut production is projected to be 309,644.4 metric tons in January to June 2025, which will allow more people to access coconut-based beverages.

Meanwhile, the World Meteorological Organization estimates that the average global surface temperature will be 1.44°C higher than the average of 1850-1900 in 2025, ensuring that heat and hydration remain at the center of consumer attention.

Dominican Republic Juice Market Opportunity

Tourism-Driven Foodservice Expansion Unlocking Premium and Occasion-Led Juice Consumption

There is a good opportunity in hotels and restaurants where juices can be placed in social events and high-end services. Cites tourism-driven growth in foodservice, and this avenue promotes juice-based mocktail-style beverages and functional blends that align with leisure and dining experiences.

The scale of this channel is indicated by tourism inflow data. According to the Banco Central de la República Dominicana, there were 6,084,801 non-resident visitors arriving by air in January to August 2025, an increase of 123,321 people, or 2.1% per annum. During the same time, 86.4% of the tourists indicate that the primary reason of their visit is recreation and 80.1% stay in hotels. This forms the basis of consistent on-trade demand in which juice can grow beyond at-home consumption.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Dominican Republic Juice Market Segmentation Analysis

By Category

- 100% Juice

- Not from Concentrate

- Reconstituted

- Juice Drinks (up to 24% Juice)

- Nectars

- High Concentration (40% to 50% fruit content)

- Medium Concentration (30% to 39% fruit content)

- Low Concentration (25% to 29% fruit content)

- Vegetable Juice

- Fruit and Vegetable Blends

The segment has the highest share around the category in the Dominican Republic juice market, where Nectars grabbed a market share of 45%. This dominance is fueled by a strong consumer preference for beverages that offer a balance between high-quality fruit flavor and palatable sweetness. Brands like Del Valle have successfully penetrated this segment by leveraging extensive distribution networks to reach over 60,000 points of sale, emphasizing preservative-free formulas in convenient single-serve cans and tetra packs that appeal to busy urban shoppers.

While nectars lead in value and popularity, they face increasing competition from lower-calorie alternatives and pure 100% juices. To maintain this majority share, producers are focusing on "natural" and "local" positioning, utilizing fruits like passion fruit and guava that resonate with traditional Dominican tastes. Despite the rise of functional plant waters, nectars are expected to remain the primary choice for Dominican families due to their widespread availability and perceived nutritional value compared to carbonates.

By Sales Channel

- Off-Trade

- Hypermarkets/ Supermarkets

- Retail Outlets

- Convenience Stores

- Online Platforms

- On-Trade

The segment has the highest share around the Sales Channel is Off-Trade, which grabbed 85% of the market. This massive share is anchored by the country's unique retail infrastructure, specifically the "colmados" or independent neighborhood stores. With a penetration of roughly one store for every 174 inhabitants, colmados provide unrivaled geographic coverage and serve as the primary destination for both planned household purchases and immediate, impulse consumption of juice products.

While traditional grocery retailers remain the backbone of the off-trade channel, modern supermarkets are increasingly becoming hubs for premium and functional juice innovations, such as cold-pressed and organic varieties. Additionally, the digital shift is slowly beginning to influence this segment, as omnichannel distribution centers improve delivery efficiency to local grocers. Although the tourism-driven foodservice sector is growing, the deep-rooted reliance on local neighborhood retail ensures that the off-trade channel will continue to be the dominant force in the Dominican juice market through 2032.

List of Companies Covered in Dominican Republic Juice Market

The companies listed below are highly influential in the Dominican Republic juice market, with a significant market share and a strong impact on industry developments.

- Distribuidora Corripio CxA

- Interfoods Dominicana SA

- Grupo Jumex SA de CV

- Pasteurizadora Rica SA

- Parmalat Dominicana SA

- Industrias San Miguel del Caribe SA

- Bepensa Dominicana SA

- Bon Appetit SA

- Alvarez & Sanchez C Por A

Competitive Landscape

The Dominican Republic juice market is led by Pasteurizadora Rica, which maintains a strong competitive position through decades of brand trust, claims of 100% natural local fruit sourcing, and a robust nationwide distribution network spanning supermarkets and colmados. Del Valle, distributed by Bepensa Dominicana, is a key challenger in nectars, leveraging Coca Cola’s extensive route to market and convenient single serve formats to secure broad visibility across nearly 62,000 outlets. Indirect competition is intensifying from flavoured waters, isotonic drinks, and coconut water, which are gaining relevance due to hydration benefits and lower calorie perceptions amid climate driven heat waves. Emerging niche players using cold press technology and functional health claims highlight opportunities in premium wellness positioning, social occasion beverages, and hydration focused innovation beyond traditional juice consumption.

Frequently Asked Questions

Related Report

1. Market Segmentation

1.1. Research Scope

1.2. Research Methodology

1.3. Definitions and Assumptions

2. Executive Summary

3. Dominican Republic Juice Market Policies, Regulations, and Standards

4. Dominican Republic Juice Market Dynamics

4.1. Growth Factors

4.2. Challenges

4.3. Trends

4.4. Opportunities

5. Dominican Republic Juice Market Statistics, 2022-2032F

5.1. Market Size & Growth Outlook

5.1.1.By Revenues in USD Million

5.1.2.By Quantity Sold in Million Litres

5.2. Market Segmentation & Growth Outlook

5.2.1.By Category

5.2.1.1. 100% Juice- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.1. Not from Concentrate- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.2. Reconstituted- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2. Juice Drinks (up to 24% Juice)- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3. Nectars- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3.1. High Concentration (40% to 50% fruit content)- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3.2. Medium Concentration (30% to 39% fruit content)- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3.3. Low Concentration (25% to 29% fruit content)- Market Insights and Forecast 2022-2032, USD Million

5.2.1.4. Vegetable Juice- Market Insights and Forecast 2022-2032, USD Million

5.2.1.5. Fruit and Vegetable Blends- Market Insights and Forecast 2022-2032, USD Million

5.2.2.By Nature

5.2.2.1. Conventional- Market Insights and Forecast 2022-2032, USD Million

5.2.2.2. Organic- Market Insights and Forecast 2022-2032, USD Million

5.2.3.By Packaging Material

5.2.3.1. Plastic- Market Insights and Forecast 2022-2032, USD Million

5.2.3.2. Glass- Market Insights and Forecast 2022-2032, USD Million

5.2.3.3. Metal- Market Insights and Forecast 2022-2032, USD Million

5.2.3.4. Others- Market Insights and Forecast 2022-2032, USD Million

5.2.4.By Packaging Type

5.2.4.1. PET Bottles- Market Insights and Forecast 2022-2032, USD Million

5.2.4.2. Aseptic Packages (Cartons)- Market Insights and Forecast 2022-2032, USD Million

5.2.4.3. Glass Bottles- Market Insights and Forecast 2022-2032, USD Million

5.2.4.4. Metal Cans- Market Insights and Forecast 2022-2032, USD Million

5.2.4.5. Disposable Cups & Pouches- Market Insights and Forecast 2022-2032, USD Million

5.2.5.By Sales Channel

5.2.5.1. Off-Trade- Market Insights and Forecast 2022-2032, USD Million

5.2.5.1.1. Hypermarkets/ Supermarkets - Market Insights and Forecast 2022-2032, USD Million

5.2.5.1.2. Retail Outlets - Market Insights and Forecast 2022-2032, USD Million

5.2.5.1.3. Convenience Stores- Market Insights and Forecast 2022-2032, USD Million

5.2.5.1.4. Online Platforms- Market Insights and Forecast 2022-2032, USD Million

5.2.5.2. On-Trade- Market Insights and Forecast 2022-2032, USD Million

5.2.6.By Competitors

5.2.6.1. Competition Characteristics

5.2.6.2. Market Share & Analysis

6. Dominican Republic 100% Juice Market Statistics, 2022-2032

6.1. Market Size & Growth Outlook

6.1.1.By Revenues in USD Million

6.1.2.By Quantity Sold in Million Litres

6.2. Market Segmentation & Growth Outlook

6.2.1.By Nature- Market Insights and Forecast 2022-2032, USD Million

6.2.2.By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

6.2.3.By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

6.2.4.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

7. Dominican Republic Juice Drinks (up to 24% Juice) Market Statistics, 2022-2032

7.1. Market Size & Growth Outlook

7.1.1.By Revenues in USD Million

7.1.2.By Quantity Sold in Million Litres

7.2. Market Segmentation & Growth Outlook

7.2.1.By Nature- Market Insights and Forecast 2022-2032, USD Million

7.2.2.By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

7.2.3.By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

7.2.4.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

8. Dominican Republic Nectars Market Statistics, 2022-2032

8.1. Market Size & Growth Outlook

8.1.1.By Revenues in USD Million

8.1.2.By Quantity Sold in Million Litres

8.2. Market Segmentation & Growth Outlook

8.2.1.By Nature- Market Insights and Forecast 2022-2032, USD Million

8.2.2.By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

8.2.3.By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

8.2.4.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

9. Dominican Republic Vegetable Juice Market Statistics, 2022-2032

9.1. Market Size & Growth Outlook

9.1.1.By Revenues in USD Million

9.1.2.By Quantity Sold in Million Litres

9.2. Market Segmentation & Growth Outlook

9.2.1.By Nature- Market Insights and Forecast 2022-2032, USD Million

9.2.2.By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

9.2.3.By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

9.2.4.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

10. Dominican Republic Fruit and Vegetable Blends Market Statistics, 2022-2032

10.1. Market Size & Growth Outlook

10.1.1. By Revenues in USD Million

10.1.2. By Quantity Sold in Million Litres

10.2. Market Segmentation & Growth Outlook

10.2.1. By Nature- Market Insights and Forecast 2022-2032, USD Million

10.2.2. By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

10.2.3. By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

10.2.4. By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

11. Competitive Outlook

11.1. Company Profiles

11.1.1. Pasteurizadora Rica SA

11.1.1.1. Business Description

11.1.1.2. Product Portfolio

11.1.1.3. Collaborations & Alliances

11.1.1.4. Recent Developments

11.1.1.5. Financial Details

11.1.1.6. Others

11.1.2. Parmalat Dominicana SA

11.1.2.1. Business Description

11.1.2.2. Product Portfolio

11.1.2.3. Collaborations & Alliances

11.1.2.4. Recent Developments

11.1.2.5. Financial Details

11.1.2.6. Others

11.1.3. Industrias San Miguel del Caribe SA

11.1.3.1. Business Description

11.1.3.2. Product Portfolio

11.1.3.3. Collaborations & Alliances

11.1.3.4. Recent Developments

11.1.3.5. Financial Details

11.1.3.6. Others

11.1.4. Bepensa Dominicana SA

11.1.4.1. Business Description

11.1.4.2. Product Portfolio

11.1.4.3. Collaborations & Alliances

11.1.4.4. Recent Developments

11.1.4.5. Financial Details

11.1.4.6. Others

11.1.5. Bon Appetit SA

11.1.5.1. Business Description

11.1.5.2. Product Portfolio

11.1.5.3. Collaborations & Alliances

11.1.5.4. Recent Developments

11.1.5.5. Financial Details

11.1.5.6. Others

11.1.6. Distribuidora Corripio CxA

11.1.6.1. Business Description

11.1.6.2. Product Portfolio

11.1.6.3. Collaborations & Alliances

11.1.6.4. Recent Developments

11.1.6.5. Financial Details

11.1.6.6. Others

11.1.7. Interfoods Dominicana SA

11.1.7.1. Business Description

11.1.7.2. Product Portfolio

11.1.7.3. Collaborations & Alliances

11.1.7.4. Recent Developments

11.1.7.5. Financial Details

11.1.7.6. Others

11.1.8. Grupo Jumex SA de CV

11.1.8.1. Business Description

11.1.8.2. Product Portfolio

11.1.8.3. Collaborations & Alliances

11.1.8.4. Recent Developments

11.1.8.5. Financial Details

11.1.8.6. Others

11.1.9. Alvarez & Sanchez C Por A

11.1.9.1. Business Description

11.1.9.2. Product Portfolio

11.1.9.3. Collaborations & Alliances

11.1.9.4. Recent Developments

11.1.9.5. Financial Details

11.1.9.6. Others

12. Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Category |

|

| By Nature |

|

| By Packaging Material |

|

| By Packaging Type |

|

| By Sales Channel |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.