Denmark Juice Market Report: Trends, Growth and Forecast (2026-2032)

By Category (100% Juice (Not from Concentrate, Reconstituted), Juice Drinks (up to 24% Juice), Nectars (High Concentration (40% to 50% fruit content), Medium Concentration (30% to 39% fruit content), Low Concentration (25% to 29% fruit content)), Vegetable Juice, Fruit and Vegetable Blends), By Nature (Conventional, Organic), By Packaging Material (Plastic, Glass, Metal, Others), By Packaging Type (PET Bottles, Aseptic Packages (Cartons), Glass Bottles, Metal Cans, Disposable Cups & Pouches), By Sales Channel (Off-Trade (Hypermarkets/ Supermarkets, Retail Outlets, Convenience Stores, Online Platforms), On-Trade) ... Read more

|

Major Players

|

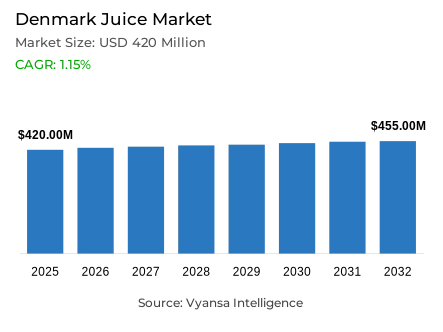

Denmark Juice Market Statistics and Insights, 2026

- Market Size Statistics

- Juice market size in Denmark was estimated at USD 420 million in 2025.

- The market size is expected to grow to USD 455 million by 2032.

- Market to register a CAGR of around 1.15% during 2026-32.

- Category Shares

- 100% juice grabbed market share of 70%.

- Competition

- More than 15 companies are actively engaged in producing juice in Denmark.

- Top 5 companies acquired around 50% of the market share.

- Vitamin Well AB, Capri Sun Group Holding AG, Lidl Danmark K/S, Rynkeby Foods A/S, Innocent ApS etc., are few of the top companies.

- Sales Channel

- Off-trade grabbed 80% of the market.

Denmark Juice Market Outlook

The Denmark juice market is in the process of a structural shift where end user are weighing a long-standing preference of high-quality fruit content against a growing need of functional, lower-sugar products. The market is projected to be USD 420 million in 2025 and is expected to be USD 455 million in 2032 with a CAGR of about 1.15% in the forecast period. Although the core category has been facing downturns because of high ingredient prices especially of oranges, the contraction rate is decreasing as prices stabilise and manufacturers are experimenting with more varied fruit and berry formulations.

There is a major change in the category as natural refreshing drinks and vitamin waters start to redefine the category. These new, single-serving juice beverages are catching on with health-conscious, busy end user who want convenience without the high sugar content of traditional carbonates. Rynkeby Foods and other brands are pioneering this shift by introducing vitamin waters and non-carbonated lemonades that retain a high content of juice but have a more modern, wellness-focused image.

Coconut and other plant waters are the most promising growth category, which perfectly fits the Denmark taste of natural and low-calorie hydration. Even though this segment has a smaller base, its growth rate is directly attributed to the fact that end user are abandoning traditional reconstituted juices in favor of products that are seen as purer. Moreover, the wider 100% juice segment is experiencing maturity, but the NFC (Not from Concentrate) niche is still reporting positive growth, which is backed by the shoppers who are willing to pay premium prices but demand high-quality ingredients.

Home consumption continues to dominate the retail environment with 80 % of the market being taken by Off-Trade channels. Juice is sold mainly in large modern grocery retailers, especially discounters and supermarkets, which have a large share of volume sales due to competitive prices and regular promotions. Although 100 % Juice is the dominant category with a 70 % market share, the future of the industry up to 2032 will be defined by a shift to functional benefits and omnichannel retail development.

Denmark Juice Market Growth Driver

Stabilising Input Cost Environment Enabling Affordable Reformulation and Flavour Diversification

Denmark juice manufacturers are also focusing on how to make their products cheaper by re-engineering recipes and increasing the number of flavours other than orange. In December 2025, the EU-harmonised consumer price index in Denmark was 1.9 per annum, which offers a more predictable pricing environment to households and daily grocery purchases. In 2025, the average global orange price was reported to be US1.42 per kilogram, which maintained high orange inputs but made them easier to plan with.

This stabilisation helps in the shift that you have outlined in your material where brands are focusing more on nectars and juice drinks and less on orange reliance by incorporating other fruits and berries. The resulting increased shelf assortment at affordable prices assists in keeping end user who are trading down to 100% juice instead of quitting the category.

Denmark Juice Market Challenge

Persistent Orange Price Volatility Undermining the Economic Viability of 100% Juice

The unstable prices of orange inputs still put pressure on 100% juice especially reconstituted products which are highly dependent on orange supply chains. According to the World Bank, oranges were sold at US1.97 per kilogram between January and March 2025 and fell to US0.95 per kilogram between October and December 2025, highlighting massive fluctuations in a year. The monthly average was still USD 0.92 per kilogram in December 2025, which further supports the speed at which costs can change.

This volatility complicates pricing and promotions in a price-sensitive retail environment, which reinforces the attraction of cheaper substitutes like nectars, juice drinks, and non-juice substitutes. Brands react to this by decreasing the amount of orange content and mixing in other fruits; however, 100% juice continues to experience pressure on demand when prices and shelf prices become more difficult to justify.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Denmark Juice Market Trend

Health-Led Hydration Preferences Redirecting Demand Toward Lighter and Functional Beverages

The preference of end user towards lighter beverages is driven by health and wellness, which is the foundation of the popularity of functional waters and plant waters as outlined in your content. According to NORMO 2025, in 2024, the total number of discretionary drinks consumed in Denmark was 6.5 servings per week, and the regional consumption increased by 3.9 to 5.6 servings per week during 2014-2024.

Meanwhile, the average consumption of fruits in Denmark was 0.9 servings per day in 2024, which means that the emphasis on the quality of the diet and healthier options remains. This atmosphere promotes a definite change in the definition of a healthy refreshment. Low-calorie, low-sugar and naturally positioned products are becoming more popular with end user, and this is why coconut and other plant waters and vitamin-style beverages are getting noticed compared to traditional 100% juice. Brands are changing their focus to functional advantages and abandoning traditional language of juice to stay relevant in health-led habits.

Denmark Juice Market Opportunity

Expanding Digital Grocery Adoption Accelerating Single-Serve and Functional Juice Formats

Single-serving and On-the-go, juice drinks with healthier positioning fit the opportunity described in your content, especially with digital retail and discovery. According to Statistics Denmark, 90% of the population between 16 and 74 years old used social media within the last three months, and 82% of the population made online purchases within the last year. This provides a high level of reach to new product education, targeted promotions and quick trial.

Grocery retailers investing in e-commerce and omnichannel models, online shelves can be used by the brands to create awareness of vitamin waters, juice-drink hybrids, and high-end single-serve products. This helps in making repeat purchase convenient, and in making these products appear as modern refreshment as opposed to traditional juice. Digital channels enable the scaling of innovation to keep up with busy lifestyles and health-conscious preferences in a category under pressure in bulk formats.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Denmark Juice Market Segmentation Analysis

By Category

- 100% Juice

- Not from Concentrate

- Reconstituted

- Juice Drinks (up to 24% Juice)

- Nectars

- High Concentration (40% to 50% fruit content)

- Medium Concentration (30% to 39% fruit content)

- Low Concentration (25% to 29% fruit content)

- Vegetable Juice

- Fruit and Vegetable Blends

The segment has the highest share around segment under the category for the Denmark market, where 100% Juice grabbed a market share of 70%. Despite facing stiff competition from lower-priced nectars and functional waters, this segment remains the cornerstone of the industry due to a deeply rooted consumer association between 100% fruit content and nutritional quality. While reconstituted variants have struggled with rising orange prices, "Not from Concentrate" (NFC) juices continue to find favor among premium-seeking households willing to pay more for freshness.

In response to a mature market, manufacturers are diversifying the 100% juice category by incorporating berries and mixed fruits to manage production costs. This strategy has broadened the flavor variety on retail shelves, ensuring that the segment retains its dominant position. Although health trends are boosting the popularity of plant waters, the massive volume share held by 100% juice ensures it remains the most significant revenue-generating pillar in Denmark through 2032.

By Sales Channel

- Off-Trade

- Hypermarkets/ Supermarkets

- Retail Outlets

- Convenience Stores

- Online Platforms

- On-Trade

The segment has the highest share around segment under the Sales Channel is Off-Trade, which grabbed 85% of the market. This high market share is driven by the fact that juice is a staple of the Denmark weekly shop, primarily purchased in bulk from large modern grocery retailers. Discounters and supermarkets lead this channel, attracting price-sensitive end user through aggressive promotions and a wide assortment of both private-label and branded products. This dominance reflects a culture of planned household consumption over impulse on-trade purchases.

While physical stores remain the primary touchpoint, e-commerce is emerging as the fastest-growing sub-channel within the off-trade segment. Major retailers like Salling Group are investing heavily in omnichannel platforms like BilkaToGo to meet the needs of busy urban shoppers. Although digital sales currently represent a low single-digit share, the continued investment in fulfillment infrastructure ensures that the off-trade channel will maintain its overwhelming lead in the Denmark juice market through 2032.

List of Companies Covered in Denmark Juice Market

The companies listed below are highly influential in the Denmark juice market, with a significant market share and a strong impact on industry developments.

- Vitamin Well AB

- Capri Sun Group Holding AG

- Lidl Danmark K/S

- Rynkeby Foods A/S

- Innocent ApS

- Co-Ro Food A/S

- Coop Danmark A/S

- Salling Group A/S

- Dagrofa ApS

- Tropicana Brands Group

Competitive Landscape

Denmark juice market remains led by Rynkeby Foods, which holds the strongest retail volume and value position through broad category coverage and active innovation across juice drinks, nectars, and adjacent formats. Rynkeby is increasingly repositioning away from traditional 100% juice toward juice drinks, vitamin waters, and natural lemonades to manage high orange input costs and align with health and convenience trends. Green Coco Europe is the fastest growing challenger, benefiting from rising demand for coconut and other plant waters positioned around low sugar, natural hydration, and wellness. Indirect competition from functional bottled water, vitamin waters, and non carbonated lemonades continues to draw consumers away from core juice. Key differentiation opportunities lie in premium not from concentrate offerings, single portion on the go formats, and health led hybrid drinks that balance quality with reduced sugar.

Frequently Asked Questions

Related Report

1. Market Segmentation

1.1. Research Scope

1.2. Research Methodology

1.3. Definitions and Assumptions

2. Executive Summary

3. Denmark Juice Market Policies, Regulations, and Standards

4. Denmark Juice Market Dynamics

4.1. Growth Factors

4.2. Challenges

4.3. Trends

4.4. Opportunities

5. Denmark Juice Market Statistics, 2022-2032F

5.1. Market Size & Growth Outlook

5.1.1.By Revenues in USD Million

5.1.2.By Quantity Sold in Million Litres

5.2. Market Segmentation & Growth Outlook

5.2.1.By Category

5.2.1.1. 100% Juice- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.1. Not from Concentrate- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.2. Reconstituted- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2. Juice Drinks (up to 24% Juice)- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3. Nectars- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3.1. High Concentration (40% to 50% fruit content)- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3.2. Medium Concentration (30% to 39% fruit content)- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3.3. Low Concentration (25% to 29% fruit content)- Market Insights and Forecast 2022-2032, USD Million

5.2.1.4. Vegetable Juice- Market Insights and Forecast 2022-2032, USD Million

5.2.1.5. Fruit and Vegetable Blends- Market Insights and Forecast 2022-2032, USD Million

5.2.2.By Nature

5.2.2.1. Conventional- Market Insights and Forecast 2022-2032, USD Million

5.2.2.2. Organic- Market Insights and Forecast 2022-2032, USD Million

5.2.3.By Packaging Material

5.2.3.1. Plastic- Market Insights and Forecast 2022-2032, USD Million

5.2.3.2. Glass- Market Insights and Forecast 2022-2032, USD Million

5.2.3.3. Metal- Market Insights and Forecast 2022-2032, USD Million

5.2.3.4. Others- Market Insights and Forecast 2022-2032, USD Million

5.2.4.By Packaging Type

5.2.4.1. PET Bottles- Market Insights and Forecast 2022-2032, USD Million

5.2.4.2. Aseptic Packages (Cartons)- Market Insights and Forecast 2022-2032, USD Million

5.2.4.3. Glass Bottles- Market Insights and Forecast 2022-2032, USD Million

5.2.4.4. Metal Cans- Market Insights and Forecast 2022-2032, USD Million

5.2.4.5. Disposable Cups & Pouches- Market Insights and Forecast 2022-2032, USD Million

5.2.5.By Sales Channel

5.2.5.1. Off-Trade- Market Insights and Forecast 2022-2032, USD Million

5.2.5.1.1. Hypermarkets/ Supermarkets - Market Insights and Forecast 2022-2032, USD Million

5.2.5.1.2. Retail Outlets - Market Insights and Forecast 2022-2032, USD Million

5.2.5.1.3. Convenience Stores- Market Insights and Forecast 2022-2032, USD Million

5.2.5.1.4. Online Platforms- Market Insights and Forecast 2022-2032, USD Million

5.2.5.2. On-Trade- Market Insights and Forecast 2022-2032, USD Million

5.2.6.By Competitors

5.2.6.1. Competition Characteristics

5.2.6.2. Market Share & Analysis

6. Denmark 100% Juice Market Statistics, 2022-2032

6.1. Market Size & Growth Outlook

6.1.1.By Revenues in USD Million

6.1.2.By Quantity Sold in Million Litres

6.2. Market Segmentation & Growth Outlook

6.2.1.By Nature- Market Insights and Forecast 2022-2032, USD Million

6.2.2.By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

6.2.3.By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

6.2.4.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

7. Denmark Juice Drinks (up to 24% Juice) Market Statistics, 2022-2032

7.1. Market Size & Growth Outlook

7.1.1.By Revenues in USD Million

7.1.2.By Quantity Sold in Million Litres

7.2. Market Segmentation & Growth Outlook

7.2.1.By Nature- Market Insights and Forecast 2022-2032, USD Million

7.2.2.By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

7.2.3.By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

7.2.4.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

8. Denmark Nectars Market Statistics, 2022-2032

8.1. Market Size & Growth Outlook

8.1.1.By Revenues in USD Million

8.1.2.By Quantity Sold in Million Litres

8.2. Market Segmentation & Growth Outlook

8.2.1.By Nature- Market Insights and Forecast 2022-2032, USD Million

8.2.2.By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

8.2.3.By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

8.2.4.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

9. Denmark Vegetable Juice Market Statistics, 2022-2032

9.1. Market Size & Growth Outlook

9.1.1.By Revenues in USD Million

9.1.2.By Quantity Sold in Million Litres

9.2. Market Segmentation & Growth Outlook

9.2.1.By Nature- Market Insights and Forecast 2022-2032, USD Million

9.2.2.By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

9.2.3.By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

9.2.4.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

10. Denmark Fruit and Vegetable Blends Market Statistics, 2022-2032

10.1. Market Size & Growth Outlook

10.1.1. By Revenues in USD Million

10.1.2. By Quantity Sold in Million Litres

10.2. Market Segmentation & Growth Outlook

10.2.1. By Nature- Market Insights and Forecast 2022-2032, USD Million

10.2.2. By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

10.2.3. By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

10.2.4. By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

11. Competitive Outlook

11.1. Company Profiles

11.1.1. Rynkeby Foods A/S

11.1.1.1. Business Description

11.1.1.2. Product Portfolio

11.1.1.3. Collaborations & Alliances

11.1.1.4. Recent Developments

11.1.1.5. Financial Details

11.1.1.6. Others

11.1.2. Innocent ApS

11.1.2.1. Business Description

11.1.2.2. Product Portfolio

11.1.2.3. Collaborations & Alliances

11.1.2.4. Recent Developments

11.1.2.5. Financial Details

11.1.2.6. Others

11.1.3. Co-Ro Food A/S

11.1.3.1. Business Description

11.1.3.2. Product Portfolio

11.1.3.3. Collaborations & Alliances

11.1.3.4. Recent Developments

11.1.3.5. Financial Details

11.1.3.6. Others

11.1.4. Coop Danmark A/S

11.1.4.1. Business Description

11.1.4.2. Product Portfolio

11.1.4.3. Collaborations & Alliances

11.1.4.4. Recent Developments

11.1.4.5. Financial Details

11.1.4.6. Others

11.1.5. Salling Group A/S

11.1.5.1. Business Description

11.1.5.2. Product Portfolio

11.1.5.3. Collaborations & Alliances

11.1.5.4. Recent Developments

11.1.5.5. Financial Details

11.1.5.6. Others

11.1.6. Vitamin Well AB

11.1.6.1. Business Description

11.1.6.2. Product Portfolio

11.1.6.3. Collaborations & Alliances

11.1.6.4. Recent Developments

11.1.6.5. Financial Details

11.1.6.6. Others

11.1.7. Capri Sun Group Holding AG

11.1.7.1. Business Description

11.1.7.2. Product Portfolio

11.1.7.3. Collaborations & Alliances

11.1.7.4. Recent Developments

11.1.7.5. Financial Details

11.1.7.6. Others

11.1.8. Lidl Danmark K/S

11.1.8.1. Business Description

11.1.8.2. Product Portfolio

11.1.8.3. Collaborations & Alliances

11.1.8.4. Recent Developments

11.1.8.5. Financial Details

11.1.8.6. Others

11.1.9. Dagrofa ApS

11.1.9.1. Business Description

11.1.9.2. Product Portfolio

11.1.9.3. Collaborations & Alliances

11.1.9.4. Recent Developments

11.1.9.5. Financial Details

11.1.9.6. Others

11.1.10. Tropicana Brands Group

11.1.10.1.Business Description

11.1.10.2.Product Portfolio

11.1.10.3.Collaborations & Alliances

11.1.10.4.Recent Developments

11.1.10.5.Financial Details

11.1.10.6.Others

12. Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Category |

|

| By Nature |

|

| By Packaging Material |

|

| By Packaging Type |

|

| By Sales Channel |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.