Colombia Juice Market Report: Trends, Growth and Forecast (2026-2032)

By Category (100% Juice (Not from Concentrate, Reconstituted), Juice Drinks (up to 24% Juice), Nectars (High Concentration (40% to 50% fruit content), Medium Concentration (30% to 39% fruit content), Low Concentration (25% to 29% fruit content)), Vegetable Juice, Fruit and Vegetable Blends), By Nature (Conventional, Organic), By Packaging Material (Plastic, Glass, Metal, Others), By Packaging Type (PET Bottles, Aseptic Packages (Cartons), Glass Bottles, Metal Cans, Disposable Cups & Pouches), By Sales Channel (Off-Trade (Hypermarkets/ Supermarkets, Retail Outlets, Convenience Stores, Online Platforms), On-Trade) ... Read more

|

Major Players

|

Colombia Juice Market Statistics and Insights, 2026

- Market Size Statistics

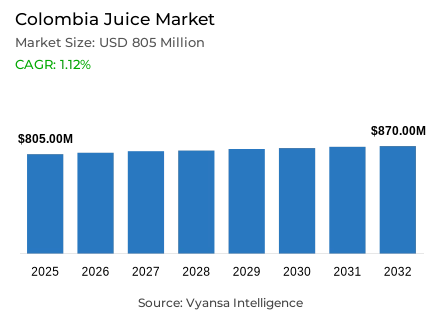

- Juice market size in Colombia was estimated at USD 805 million in 2025.

- The market size is expected to grow to USD 870 million by 2032.

- Market to register a CAGR of around 1.12% during 2026-32.

- Category Shares

- Juice drinks (up to 24% juice) grabbed market share of 80%.

- Competition

- More than 10 companies are actively engaged in producing juice in Colombia.

- Top 5 companies acquired around 75% of the market share.

- Conservas California SA, Various franchisees, Productos Naturales de la Sabana SA, Postobón SA, Fomento Económico Mexicano SAB de CV etc., are few of the top companies.

- Sales Channel

- Off-trade grabbed 85% of the market.

Colombia Juice Market Outlook

The Colombian juice market is operating in a complicated environment characterized by the sugar tax and changing end user priorities. Although the health tax has increased the prices and promoted the transition to flavored waters or dairy, the category is strong because of the long-standing popularity of fruit-based drinks. The market is projected to reach US$805 million in 2025 and reach US 870 million in 2032 with a CAGR of about 1.12 percent in the 2026-32 period.

The current end user behaviour is divided into price sensitivity and the need to have clean labels. Although Juice Drinks (up to 24 % juice) are under pressure due to the presence of cheaper substitutes, including their own-label milk, 100 % Juice is showing positive growth as health-conscious end users are seeking natural compositions. Nevertheless, Juice Drinks continue to enjoy a high 80 % market share due to their low prices and high presence in multi-unit packs in discounters like D1 and Aar.

Innovation is also leaning towards functional adult benefits like juices that are fortified with collagen, magnesium and prebiotic fiber. Other major brands such as Postobon are also speeding up their digitalization with the help of omnichannel platforms such as We Shop Postobon, which provides competitive prices and home delivery.

These measures are used to offset the difficulties of sugar-reduction formulations, which have occasionally been unsuccessful in end user satisfaction over flavor changes. The distribution environment is still deeply rooted in home consumption, with the off-trade channels holding 85 per cent of the market. Although the traditional small grocers are still the main point of sale, they are losing market to the discounters and supermarkets who are providing better value through promotions. E-commerce is also becoming relevant with brands investing in sponsored placements and online presence, which means that the juice category will continue to be a staple of Colombian households by 2032.

Colombia Juice Market Growth Driver

Sugar Tax Drives Consumers Toward Healthier Alternatives

The introduction of a significant healthy tax on sweet drinks by the Colombian government is essentially transforming the end user buying behavior. With these sugar-sweetened items, such as many juice beverages, becoming more costly, price-sensitive end users are reacting by switching to less expensive alternatives like flavored waters or even milk.

The effectiveness of this fiscal pressure is evidenced by similar efforts in other countries around the world in Mexico, a soda tax led to a 7.6 % decrease in total purchases of taxed beverages in just two years, and a more significant 11.7 % decrease in low-income households. This trend shows that the tax is successfully pushing both health-conscious and cost-conscious end users out of the traditional juices and towards other options that are seen as more helpful to their health and their budgets.

Colombia Juice Market Challenge

Affordability and Reformulation Pose Challenges

The juice market is being squeezed by economic forces and health policies. In 2024, the food and beverage output in Colombia fell by 0.7 % due to the reduced end user spending power and new taxes on sugar. The levy on the sugar-sweetened beverage alone contributed about one percentage point to inflation, increasing the cost of juice and reducing demand. Firms have tried to cut down sugar content in juices to meet health standards but this has posed flavor problems.

Although the median sugar content of Colombian drinks decreased by 8.9g to 4.8g per 100ml per 100ml during the reformulation period (2015-2024), reformulated drinks can discourage end users. As 79 % of shoppers around the world focus on price and 58 % continue to focus on taste when buying drinks, juice brands face a daunting task to provide healthier and more affordable products without sacrificing the taste that makes people buy again.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Colombia Juice Market Trend

Clean-Label 100% Juices Gain Traction

The most interesting tendencies in the context of the general market downturn is the growing popularity of 100 percent fruit juices with no added sugar or additives. end users are increasingly questioning ingredients, with about 58 % of Latin American end users saying they read nutrition labels regularly, thus driving a trend towards clean label drinks. This has increased the 100 % juice segment in Colombia, with shoppers opting to buy natural products even at a higher price.

Retailers are cashing in on this trend hard-discount chains, which have risen to 18 percent of grocery retail by 2024, are selling cheap own-label 100 percent juices that promise value and naturalness. These efforts increase the availability of pure juices, and single-serving packages are offered, as well as family-size bottles. The 100⁻ percent juice is winning the battle against the declining trend thanks to the appeal of authenticity and perceived health benefits, which are adding volume to the category when other types of juices are declining.

Colombia Juice Market Opportunity

Functional Beverages Emerge as a Niche Opportunity

Functional juices are a promising prospect as Colombian end users are becoming more wellness-conscious, especially in an aging population. The ageing of Latin America is accelerating, with more people aged over 60 than under 5 by 2030, and this is creating a demand in healthy aging products. Juice companies are developing nutrient-enhanced drinks that address the health issues of adults. As an example, a local brand, Natural Freshly, has functional juices like an aloe vera drink with prebiotic fiber to support digestion and a cranberry concentrate with vitamin C, zinc, and selenium to support the immune system and skin health.

These value-added juices are still a niche, but they serve older and health-conscious end users who want to gain the benefits of better gut health, vitality, or beauty internally. With a focus on natural ingredients and established wellness additives, functional juice drinks will be able to expand at a slow pace, which is a long-term opportunity in a market that is otherwise experiencing headwinds.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Colombia Juice Market Segmentation Analysis

By Category

- 100% Juice

- Not from Concentrate

- Reconstituted

- Juice Drinks (up to 24% Juice)

- Nectars

- High Concentration (40% to 50% fruit content)

- Medium Concentration (30% to 39% fruit content)

- Low Concentration (25% to 29% fruit content)

- Vegetable Juice

- Fruit and Vegetable Blends

The segment has the highest share around the category for the Colombian market, where Juice Drinks (up to 24% Juice) grabbed a market share of 80%. This dominance is largely due to its high level of accessibility and broad appeal among low-to-middle-income households. Despite the impact of the sugar tax, these drinks remain the most common choice for daily consumption and school lunchboxes, reinforced by the strong retail presence of market leaders like Postobón and their brands HIT and Tutti Frutti.

While the segment currently leads, it faces competition from dairy products and flavored waters as consumers look for better nutritional value or lower prices. To defend this share, manufacturers are diversifying pack sizes and utilizing discounters to offer multi-unit bundles. Although 100% juice is growing due to clean-label trends, Juice Drinks are expected to maintain their majority position through 2032 because of their established flavor profiles and essential role in the Colombian beverage landscape.

By Sales Channel

- Off-Trade

- Hypermarkets/ Supermarkets

- Retail Outlets

- Convenience Stores

- Online Platforms

- On-Trade

The segment has the highest share around the Sales Channel is Off-Trade, which grabbed 85% of the market. This significant share highlights that Colombians primarily purchase juice for home consumption rather than in foodservice settings. While small local grocers remain the top channel, there is a clear migration toward discounters like D1 and Ara. These modern retailers have gained momentum by offering private-label options and competitive prices that help families manage their budgets amidst rising living costs and health taxes.

Supermarkets and hypermarkets also play a critical role by offering larger 3-liter formats and exclusive promotional deals. Meanwhile, e-commerce is emerging as a dynamic sub-channel, led by brand-owned platforms like "We Shop Postobón" and sponsored listings on retailer sites. This shift toward value-driven and digital channels ensures that the off-trade segment will continue to dominate the Colombian juice market's distribution through 2032.

List of Companies Covered in Colombia Juice Market

The companies listed below are highly influential in the Colombia juice market, with a significant market share and a strong impact on industry developments.

- Conservas California SA

- Various franchisees

- Productos Naturales de la Sabana SA

- Postobón SA

- Fomento Económico Mexicano SAB de CV

- Ajecolombia SA

- Alpina Productos Alimenticios SA

- Quala SA

- Levapan SA

- Meals de Colombia SA

Competitive Landscape

The juice market in Colombia in 2025 remains highly competitive but increasingly polarised, shaped by reformulation pressures, private label expansion and strategic exits. Postobón continues to lead through scale, distribution strength and brand recognition, although sugar-reduction reformulations have diluted consumer loyalty and gradually eroded share. Multinationals are selectively strengthening positions via health-oriented partnerships, as seen in Pepsi-Cola Colombia’s collaboration with Ocean Spray, which targets adult, antioxidant-focused consumption occasions. At the same time, rising cost pressures and margin compression have forced traditional players such as Country Hill to exit the category. Discounters are reshaping competition by accelerating private label penetration and redefining value benchmarks, intensifying pressure on mid-tier branded offerings.

Frequently Asked Questions

Related Report

1. Market Segmentation

1.1. Research Scope

1.2. Research Methodology

1.3. Definitions and Assumptions

2. Executive Summary

3. Colombia Juice Market Policies, Regulations, and Standards

4. Colombia Juice Market Dynamics

4.1. Growth Factors

4.2. Challenges

4.3. Trends

4.4. Opportunities

5. Colombia Juice Market Statistics, 2022-2032F

5.1. Market Size & Growth Outlook

5.1.1.By Revenues in USD Million

5.1.2.By Quantity Sold in Million Litres

5.2. Market Segmentation & Growth Outlook

5.2.1.By Category

5.2.1.1. 100% Juice- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.1. Not from Concentrate- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.2. Reconstituted- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2. Juice Drinks (up to 24% Juice)- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3. Nectars- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3.1. High Concentration (40% to 50% fruit content)- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3.2. Medium Concentration (30% to 39% fruit content)- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3.3. Low Concentration (25% to 29% fruit content)- Market Insights and Forecast 2022-2032, USD Million

5.2.1.4. Vegetable Juice- Market Insights and Forecast 2022-2032, USD Million

5.2.1.5. Fruit and Vegetable Blends- Market Insights and Forecast 2022-2032, USD Million

5.2.2.By Nature

5.2.2.1. Conventional- Market Insights and Forecast 2022-2032, USD Million

5.2.2.2. Organic- Market Insights and Forecast 2022-2032, USD Million

5.2.3.By Packaging Material

5.2.3.1. Plastic- Market Insights and Forecast 2022-2032, USD Million

5.2.3.2. Glass- Market Insights and Forecast 2022-2032, USD Million

5.2.3.3. Metal- Market Insights and Forecast 2022-2032, USD Million

5.2.3.4. Others- Market Insights and Forecast 2022-2032, USD Million

5.2.4.By Packaging Type

5.2.4.1. PET Bottles- Market Insights and Forecast 2022-2032, USD Million

5.2.4.2. Aseptic Packages (Cartons)- Market Insights and Forecast 2022-2032, USD Million

5.2.4.3. Glass Bottles- Market Insights and Forecast 2022-2032, USD Million

5.2.4.4. Metal Cans- Market Insights and Forecast 2022-2032, USD Million

5.2.4.5. Disposable Cups & Pouches- Market Insights and Forecast 2022-2032, USD Million

5.2.5.By Sales Channel

5.2.5.1. Off-Trade- Market Insights and Forecast 2022-2032, USD Million

5.2.5.1.1. Hypermarkets/ Supermarkets - Market Insights and Forecast 2022-2032, USD Million

5.2.5.1.2. Retail Outlets - Market Insights and Forecast 2022-2032, USD Million

5.2.5.1.3. Convenience Stores- Market Insights and Forecast 2022-2032, USD Million

5.2.5.1.4. Online Platforms- Market Insights and Forecast 2022-2032, USD Million

5.2.5.2. On-Trade- Market Insights and Forecast 2022-2032, USD Million

5.2.6.By Competitors

5.2.6.1. Competition Characteristics

5.2.6.2. Market Share & Analysis

6. Colombia 100% Juice Market Statistics, 2022-2032

6.1. Market Size & Growth Outlook

6.1.1.By Revenues in USD Million

6.1.2.By Quantity Sold in Million Litres

6.2. Market Segmentation & Growth Outlook

6.2.1.By Nature- Market Insights and Forecast 2022-2032, USD Million

6.2.2.By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

6.2.3.By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

6.2.4.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

7. Colombia Juice Drinks (up to 24% Juice) Market Statistics, 2022-2032

7.1. Market Size & Growth Outlook

7.1.1.By Revenues in USD Million

7.1.2.By Quantity Sold in Million Litres

7.2. Market Segmentation & Growth Outlook

7.2.1.By Nature- Market Insights and Forecast 2022-2032, USD Million

7.2.2.By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

7.2.3.By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

7.2.4.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

8. Colombia Nectars Market Statistics, 2022-2032

8.1. Market Size & Growth Outlook

8.1.1.By Revenues in USD Million

8.1.2.By Quantity Sold in Million Litres

8.2. Market Segmentation & Growth Outlook

8.2.1.By Nature- Market Insights and Forecast 2022-2032, USD Million

8.2.2.By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

8.2.3.By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

8.2.4.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

9. Colombia Vegetable Juice Market Statistics, 2022-2032

9.1. Market Size & Growth Outlook

9.1.1.By Revenues in USD Million

9.1.2.By Quantity Sold in Million Litres

9.2. Market Segmentation & Growth Outlook

9.2.1.By Nature- Market Insights and Forecast 2022-2032, USD Million

9.2.2.By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

9.2.3.By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

9.2.4.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

10. Colombia Fruit and Vegetable Blends Market Statistics, 2022-2032

10.1. Market Size & Growth Outlook

10.1.1. By Revenues in USD Million

10.1.2. By Quantity Sold in Million Litres

10.2. Market Segmentation & Growth Outlook

10.2.1. By Nature- Market Insights and Forecast 2022-2032, USD Million

10.2.2. By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

10.2.3. By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

10.2.4. By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

11. Competitive Outlook

11.1. Company Profiles

11.1.1. Postobón SA

11.1.1.1. Business Description

11.1.1.2. Product Portfolio

11.1.1.3. Collaborations & Alliances

11.1.1.4. Recent Developments

11.1.1.5. Financial Details

11.1.1.6. Others

11.1.2. Fomento Económico Mexicano SAB de CV

11.1.2.1. Business Description

11.1.2.2. Product Portfolio

11.1.2.3. Collaborations & Alliances

11.1.2.4. Recent Developments

11.1.2.5. Financial Details

11.1.2.6. Others

11.1.3. Ajecolombia SA

11.1.3.1. Business Description

11.1.3.2. Product Portfolio

11.1.3.3. Collaborations & Alliances

11.1.3.4. Recent Developments

11.1.3.5. Financial Details

11.1.3.6. Others

11.1.4. Alpina Productos Alimenticios SA

11.1.4.1. Business Description

11.1.4.2. Product Portfolio

11.1.4.3. Collaborations & Alliances

11.1.4.4. Recent Developments

11.1.4.5. Financial Details

11.1.4.6. Others

11.1.5. Quala SA

11.1.5.1. Business Description

11.1.5.2. Product Portfolio

11.1.5.3. Collaborations & Alliances

11.1.5.4. Recent Developments

11.1.5.5. Financial Details

11.1.5.6. Others

11.1.6. Conservas California SA

11.1.6.1. Business Description

11.1.6.2. Product Portfolio

11.1.6.3. Collaborations & Alliances

11.1.6.4. Recent Developments

11.1.6.5. Financial Details

11.1.6.6. Others

11.1.7. Various franchisees

11.1.7.1. Business Description

11.1.7.2. Product Portfolio

11.1.7.3. Collaborations & Alliances

11.1.7.4. Recent Developments

11.1.7.5. Financial Details

11.1.7.6. Others

11.1.8. Productos Naturales de la Sabana SA

11.1.8.1. Business Description

11.1.8.2. Product Portfolio

11.1.8.3. Collaborations & Alliances

11.1.8.4. Recent Developments

11.1.8.5. Financial Details

11.1.8.6. Others

11.1.9. Levapan SA

11.1.9.1. Business Description

11.1.9.2. Product Portfolio

11.1.9.3. Collaborations & Alliances

11.1.9.4. Recent Developments

11.1.9.5. Financial Details

11.1.9.6. Others

11.1.10. Meals de Colombia SA

11.1.10.1.Business Description

11.1.10.2.Product Portfolio

11.1.10.3.Collaborations & Alliances

11.1.10.4.Recent Developments

11.1.10.5.Financial Details

11.1.10.6.Others

12. Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Category |

|

| By Nature |

|

| By Packaging Material |

|

| By Packaging Type |

|

| By Sales Channel |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.