China Juice Market Report: Trends, Growth and Forecast (2026-2032)

By Category (100% Juice (Not from Concentrate, Reconstituted), Juice Drinks (up to 24% Juice), Nectars (High Concentration (40% to 50% fruit content), Medium Concentration (30% to 39% fruit content), Low Concentration (25% to 29% fruit content)), Vegetable Juice, Fruit and Vegetable Blends), By Nature (Conventional, Organic), By Packaging Material (Plastic, Glass, Metal, Others), By Packaging Type (PET Bottles, Aseptic Packages (Cartons), Glass Bottles, Metal Cans, Disposable Cups & Pouches), By Sales Channel (Off-Trade (Hypermarkets/ Supermarkets, Retail Outlets, Convenience Stores, Online Platforms), On-Trade), By Region (North, East, Southwest, Northwest, North East, South) ... Read more

|

Major Players

|

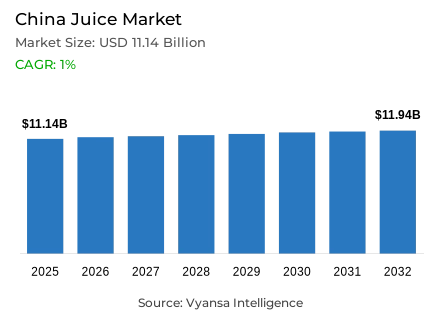

China Juice Market Statistics and Insights, 2026

- Market Size Statistics

- Juice market size in China was estimated at USD 11.14 billion in 2025.

- The market size is expected to grow to USD 11.94 billion by 2032.

- Market to register a CAGR of around 1% during 2026-32.

- Category Shares

- Juice drinks (up to 24% juice) grabbed market share of 53%.

- Competition

- More than 20 companies are actively engaged in producing juice in China.

- Top 5 companies acquired around 35% of the market share.

- Shenzhen Grandness Industry Groups Co Ltd, President Enterprises (China) Investment Co Ltd, Hangzhou Wei Chuan Foods Co, Coca-Cola China Ltd, Beijing Huiyuan Beverage & Food Group Corp etc., are few of the top companies.

- Sales Channel

- Off-trade grabbed 75% of the market.

China Juice Market Outlook

The China juice market is undergoing a significant transformation as end user preferences shift from high-sugar, traditional drinks to healthier, premium alternatives. While health-consciousness has led to a slight decline in volume for mainstream products, there is a clear trend toward premiumization. The market is estimated at $11.14 billion in 2025 and is expected to grow to $11.73 billion by 2032, registering a CAGR of around 1% during the 2026-32 period.

Despite the rise of premium segments, Juice Drinks (up to 24% juice) currently grab the largest market share at 53%. However, this category is facing ongoing contraction as middle-class end users in tier-one and tier-two cities increasingly reject added sugars and artificial additives. In their place, 100% fruit juices, Not From Concentrate (NFC) varieties, and coconut waters are gaining traction, with end users willing to pay higher prices for perceived quality and natural nutrients.

Technological innovation is spearheading this recovery. High-pressure processing (HPP) and advanced pasteurization techniques are allowing brands to preserve the original flavor and vitamins of fruits without heat damage. Furthermore, the market is seeing a surge in functional juices fortified with prebiotics, collagen, and electrolytes. Brands like Coca-Cola (Minute Maid) and General Beverage (iF) are leveraging these technologies to upgrade their portfolios and meet the demand for "burden-free" hydration.

Distribution remains dominated by the home-consumption sector, with Off-Trade channels grabbing 75% of the market. Supermarkets remain a stronghold due to their product diversity and promotional strategies, but e-commerce is the fastest-evolving channel. Platforms offering 30-minute delivery and big-data-driven marketing are making it easier for niche and premium brands to reach a broader audience across both urban and rural China.

China Juice Market Growth Driver

Government Nutrition Policy Encourages Healthier Juice Choices

The Food and Nutrition Development Guideline (2025-2030) published by the Ministry of Agriculture and Rural Affairs, the National Health Commission, and the Ministry of market and Information Technology actively promotes the decrease in sugar intake and the implementation of balanced diets in China. The guideline recommends a daily intake of added sugar to 25 0g and encourages the intake of foods rich in nutrients, such as fruit, to improve the overall quality of the diet. These governmental goals increase end user awareness of the health effects of sugar and force beverage manufacturers to re-formulate or launch lower-sugar, more-fruit-based juice products in line with national health goals.

This policy focus creates a resounding momentum in the juice market the products perceived as natural, nutrient-rich, and containing little added sugar are becoming more popular. Juice producers who focus on the use of real fruit and lower sugar levels have a better chance to meet the changing end user demands that are being created by the government through its promotion of healthier lifestyles.

China Juice Market Challenge

Rising Popularity of Low-Sugar Alternatives Challenges Traditional Juices

The changing consumption trends in China towards health-consciousness are changing the demand of beverages, thus presenting a challenge to the traditional juices that have a higher sugar content. The study showed that sales of low-sugar tea drinks grew by 41 % annually in 2024, indicating that end users shifted towards less sugary and healthier tea drinks compared to traditional sweetened ones. This change will divert end user spending on some of the segments of juices, especially those that are seen to contain high levels of added sugar, to other products that are more consistent with the wellness agenda.

At the same time, other non-alcoholic beverage segments, including bottled water and sugar-free beverages, are growing at a very high rate in the overall beverage market, which is estimated to have reached USD 170 billion in 2024 as per official market reports. This competitive landscape increases the strain on the traditional juice products to evolve or face the risk of becoming irrelevant to health-conscious end users.

Unlock Market Intelligence

Explore the market potential with our data-driven report

China Juice Market Trend

Expansion of Non-Alcoholic Beverages Signals Changing Consumption Patterns

The government nutrition policy in China sets high goals on the amount of fruit to be consumed per person annually, with the aim of boosting the consumption of fruits and other nutritious foods by 2030. According to official recommendations, the annual fruit intake goals are 130 kg per capita, which highlights the importance of the state in improving the overall quality of the diet. These targets generate a market niche of juice products that are positioned as complements to fresh fruit diets, especially 100% fruit juices that contain vitamins and minerals in an easy to use form.

Juice manufacturers that successfully position their products in line with these national nutritional goals, such as focusing on high fruit content, natural sourcing, and nutritional value, can appeal to end users who want to follow government-approved nutritional guidelines. This correspondence will enable product differentiation and can lead to the wider acceptance of high-quality juice categories as part of balanced diets.

China Juice Market Opportunity

National Fruit Consumption Targets Open New Pathways for Juice Demand

The China juice market is experiencing a major change in the shift of end user preference towards high-sugar, traditional beverages to healthier and premium drinks. Although the mainstream products have experienced a slight decrease in volume due to the rise in health consciousness, there is a definite trend towards premiumization. The market is projected to reach USD 11.14 billion in 2025 and USD 11.73 billion in 2032 with a CAGR of about 0.74 percent in the 2026-32 period. Although the premium segments have emerged, the largest share of 53 % is held by the juice drinks with up to 24 % of juice content. However, this segment is undergoing shrinkage with middle-income end users in tier-one and tier-two cities becoming more opposed to added sugar and artificial additives. Rather, 100 percent fruit juices, not-from-concentrate (NFC) types, and coconut waters are on the rise, and end users are ready to pay more money due to the perceived quality and natural nutrients. This recovery is being driven by technological innovation. Advanced pasteurization methods and high-pressure processing (HPP) allow brands to retain the original taste and vitamins of fruits without heat destruction.

Moreover, there is an increase in the number of functional juices that are fortified with prebiotics, collagen, and electrolytes in the market. Coca-Cola (Minute Maid) and General Beverage (iF) are some of the brands that are using these technologies to boost their portfolios and satisfy the need of burden-free hydration. The home-consumption segment continues to dominate distribution, with off-trade channels taking 75 % of the market. Supermarkets maintain a strong grip because of their product variety and promotional tactics, although e-commerce is the most rapidly developing channel. Solutions that provide 30-minute delivery and data-driven marketing enable wider coverage of niche and premium brands in urban and rural China.

Unlock Market Intelligence

Explore the market potential with our data-driven report

China Juice Market Segmentation Analysis

By Category

- 100% Juice

- Not from Concentrate

- Reconstituted

- Juice Drinks (up to 24% Juice)

- Nectars

- High Concentration (40% to 50% fruit content)

- Medium Concentration (30% to 39% fruit content)

- Low Concentration (25% to 29% fruit content)

- Vegetable Juice

- Fruit and Vegetable Blends

The segment has the highest share around segment under the category for the Chinese market, where Juice Drinks (up to 24% Juice) grabbed a market share of 53%. This segment remains the largest in volume terms due to its long-standing presence and wide availability. However, it is currently the most challenged subcategory as rising health awareness leads end users to abandon drinks with high added sugar and artificial additives. Traditional favorites are increasingly viewed as "sugary drinks" rather than healthy options.

As demand for these traditional drinks contracts, the market is shifting toward 100% juice and NFC products. While Juice Drinks still hold more than half the market, the growth is moving toward items with cleaner ingredient lists and functional benefits. Brands are responding by upgrading their existing lines to include higher juice concentrations, ensuring the category evolves to meet the unprecedented level of sugar sensitivity among young and middle-class families.

By Sales Channel

- Off-Trade

- Hypermarkets/ Supermarkets

- Retail Outlets

- Convenience Stores

- Online Platforms

- On-Trade

The segment has the highest share around segment under the Sales Channel is Off-Trade, which grabbed 75% of the market. This dominance highlights that juice consumption in China is primarily a retail-driven activity for home and on-the-go use. Supermarkets serve as the backbone of this channel, utilizing vast distribution networks and diverse packaging formats like PET bottles and Tetra Paks to cater to fast-paced urban lifestyles and bulk household stocking.

While supermarkets maintain a stronghold, retail e-commerce is rapidly reshaping the off-trade landscape. Platforms offering instant delivery and live-streaming recommendations have turned juice into an impulsive digital purchase. This shift allows emerging brands, particularly in the coconut water and NFC segments, to penetrate deeper into third- and fourth-tier cities. Despite the rise of digital convenience, the off-trade channel as a whole continues to be the essential link between juice brands and the Chinese end user.

List of Companies Covered in China Juice Market

The companies listed below are highly influential in the China juice market, with a significant market share and a strong impact on industry developments.

- Shenzhen Grandness Industry Groups Co Ltd

- President Enterprises (China) Investment Co Ltd

- Hangzhou Wei Chuan Foods Co

- Coca-Cola China Ltd

- Beijing Huiyuan Beverage & Food Group Corp

- Tingyi (Cayman Islands) Holdings Corp

- Nongfu Spring Co Ltd

- General Beverage Co Ltd

- Paldo Co Ltd

- Shanghai Jiajun Beverage Co Ltd

Competitive Landscape

China’s juice market in 2025 is highly competitive and increasingly polarised around health-led propositions. Coca-Cola China Ltd retains leadership in value terms, anchored by Minute Maid’s broad portfolio spanning juice drinks, 100% juice, NFC juice, and coconut water, allowing the company to defend share through premiumisation despite volume pressure. Its nationwide off-trade distribution remains a structural advantage. At the same time, dynamic challengers such as General Beverage Co Ltd are gaining momentum, with its iF brand delivering double-digit growth by focusing on no-additive formulations, low sugar content, and premium packaging. Overall, competition is intensifying as brands race to differentiate through health credentials, processing technology, and mid-to-high-end positioning.

Frequently Asked Questions

Related Report

1. Market Segmentation

1.1. Research Scope

1.2. Research Methodology

1.3. Definitions and Assumptions

2. Executive Summary

3. China Juice Market Policies, Regulations, and Standards

4. China Juice Market Dynamics

4.1. Growth Factors

4.2. Challenges

4.3. Trends

4.4. Opportunities

5. China Juice Market Statistics, 2022-2032F

5.1. Market Size & Growth Outlook

5.1.1.By Revenues in USD Million

5.1.2.By Quantity Sold in Million Litres

5.2. Market Segmentation & Growth Outlook

5.2.1.By Category

5.2.1.1. 100% Juice- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.1. Not from Concentrate- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.2. Reconstituted- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2. Juice Drinks (up to 24% Juice)- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3. Nectars- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3.1. High Concentration (40% to 50% fruit content)- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3.2. Medium Concentration (30% to 39% fruit content)- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3.3. Low Concentration (25% to 29% fruit content)- Market Insights and Forecast 2022-2032, USD Million

5.2.1.4. Vegetable Juice- Market Insights and Forecast 2022-2032, USD Million

5.2.1.5. Fruit and Vegetable Blends- Market Insights and Forecast 2022-2032, USD Million

5.2.2.By Nature

5.2.2.1. Conventional- Market Insights and Forecast 2022-2032, USD Million

5.2.2.2. Organic- Market Insights and Forecast 2022-2032, USD Million

5.2.3.By Packaging Material

5.2.3.1. Plastic- Market Insights and Forecast 2022-2032, USD Million

5.2.3.2. Glass- Market Insights and Forecast 2022-2032, USD Million

5.2.3.3. Metal- Market Insights and Forecast 2022-2032, USD Million

5.2.3.4. Others- Market Insights and Forecast 2022-2032, USD Million

5.2.4.By Packaging Type

5.2.4.1. PET Bottles- Market Insights and Forecast 2022-2032, USD Million

5.2.4.2. Aseptic Packages (Cartons)- Market Insights and Forecast 2022-2032, USD Million

5.2.4.3. Glass Bottles- Market Insights and Forecast 2022-2032, USD Million

5.2.4.4. Metal Cans- Market Insights and Forecast 2022-2032, USD Million

5.2.4.5. Disposable Cups & Pouches- Market Insights and Forecast 2022-2032, USD Million

5.2.5.By Sales Channel

5.2.5.1. Off-Trade- Market Insights and Forecast 2022-2032, USD Million

5.2.5.1.1. Hypermarkets/ Supermarkets - Market Insights and Forecast 2022-2032, USD Million

5.2.5.1.2. Retail Outlets - Market Insights and Forecast 2022-2032, USD Million

5.2.5.1.3. Convenience Stores- Market Insights and Forecast 2022-2032, USD Million

5.2.5.1.4. Online Platforms- Market Insights and Forecast 2022-2032, USD Million

5.2.5.2. On-Trade- Market Insights and Forecast 2022-2032, USD Million

5.2.6.By Region

5.2.6.1. North

5.2.6.2. East

5.2.6.3. Southwest

5.2.6.4. Northwest

5.2.6.5. North East

5.2.6.6. South

5.2.7.By Competitors

5.2.7.1. Competition Characteristics

5.2.7.2. Market Share & Analysis

6. China 100% Juice Market Statistics, 2022-2032

6.1. Market Size & Growth Outlook

6.1.1.By Revenues in USD Million

6.1.2.By Quantity Sold in Million Litres

6.2. Market Segmentation & Growth Outlook

6.2.1.By Nature- Market Insights and Forecast 2022-2032, USD Million

6.2.2.By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

6.2.3.By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

6.2.4.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

6.2.5.By Region- Market Insights and Forecast 2022-2032, USD Million

7. China Juice Drinks (up to 24% Juice) Market Statistics, 2022-2032

7.1. Market Size & Growth Outlook

7.1.1.By Revenues in USD Million

7.1.2.By Quantity Sold in Million Litres

7.2. Market Segmentation & Growth Outlook

7.2.1.By Nature- Market Insights and Forecast 2022-2032, USD Million

7.2.2.By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

7.2.3.By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

7.2.4.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

7.2.5.By Region- Market Insights and Forecast 2022-2032, USD Million

8. China Nectars Market Statistics, 2022-2032

8.1. Market Size & Growth Outlook

8.1.1.By Revenues in USD Million

8.1.2.By Quantity Sold in Million Litres

8.2. Market Segmentation & Growth Outlook

8.2.1.By Nature- Market Insights and Forecast 2022-2032, USD Million

8.2.2.By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

8.2.3.By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

8.2.4.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

8.2.5.By Region- Market Insights and Forecast 2022-2032, USD Million

9. China Vegetable Juice Market Statistics, 2022-2032

9.1. Market Size & Growth Outlook

9.1.1.By Revenues in USD Million

9.1.2.By Quantity Sold in Million Litres

9.2. Market Segmentation & Growth Outlook

9.2.1.By Nature- Market Insights and Forecast 2022-2032, USD Million

9.2.2.By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

9.2.3.By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

9.2.4.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

9.2.5.By Region- Market Insights and Forecast 2022-2032, USD Million

10. China Fruit and Vegetable Blends Market Statistics, 2022-2032

10.1. Market Size & Growth Outlook

10.1.1. By Revenues in USD Million

10.1.2. By Quantity Sold in Million Litres

10.2. Market Segmentation & Growth Outlook

10.2.1. By Nature- Market Insights and Forecast 2022-2032, USD Million

10.2.2. By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

10.2.3. By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

10.2.4. By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

10.2.5. By Region- Market Insights and Forecast 2022-2032, USD Million

11. Competitive Outlook

11.1. Company Profiles

11.1.1. Coca-Cola China Ltd

11.1.1.1. Business Description

11.1.1.2. Product Portfolio

11.1.1.3. Collaborations & Alliances

11.1.1.4. Recent Developments

11.1.1.5. Financial Details

11.1.1.6. Others

11.1.2. Beijing Huiyuan Beverage & Food Group Corp

11.1.2.1. Business Description

11.1.2.2. Product Portfolio

11.1.2.3. Collaborations & Alliances

11.1.2.4. Recent Developments

11.1.2.5. Financial Details

11.1.2.6. Others

11.1.3. Tingyi (Cayman Islands) Holdings Corp

11.1.3.1. Business Description

11.1.3.2. Product Portfolio

11.1.3.3. Collaborations & Alliances

11.1.3.4. Recent Developments

11.1.3.5. Financial Details

11.1.3.6. Others

11.1.4. Nongfu Spring Co Ltd

11.1.4.1. Business Description

11.1.4.2. Product Portfolio

11.1.4.3. Collaborations & Alliances

11.1.4.4. Recent Developments

11.1.4.5. Financial Details

11.1.4.6. Others

11.1.5. Shenzhen Grandness Industry Groups Co Ltd

11.1.5.1. Business Description

11.1.5.2. Product Portfolio

11.1.5.3. Collaborations & Alliances

11.1.5.4. Recent Developments

11.1.5.5. Financial Details

11.1.5.6. Others

11.1.6. General Beverage Co Ltd

11.1.6.1. Business Description

11.1.6.2. Product Portfolio

11.1.6.3. Collaborations & Alliances

11.1.6.4. Recent Developments

11.1.6.5. Financial Details

11.1.6.6. Others

11.1.7. President Enterprises (China) Investment Co Ltd

11.1.7.1. Business Description

11.1.7.2. Product Portfolio

11.1.7.3. Collaborations & Alliances

11.1.7.4. Recent Developments

11.1.7.5. Financial Details

11.1.7.6. Others

11.1.8. Hangzhou Wei Chuan Foods Co

11.1.8.1. Business Description

11.1.8.2. Product Portfolio

11.1.8.3. Collaborations & Alliances

11.1.8.4. Recent Developments

11.1.8.5. Financial Details

11.1.8.6. Others

11.1.9. Paldo Co Ltd

11.1.9.1. Business Description

11.1.9.2. Product Portfolio

11.1.9.3. Collaborations & Alliances

11.1.9.4. Recent Developments

11.1.9.5. Financial Details

11.1.9.6. Others

11.1.10. Shanghai Jiajun Beverage Co Ltd

11.1.10.1.Business Description

11.1.10.2.Product Portfolio

11.1.10.3.Collaborations & Alliances

11.1.10.4.Recent Developments

11.1.10.5.Financial Details

11.1.10.6.Others

12. Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Category |

|

| By Nature |

|

| By Packaging Material |

|

| By Packaging Type |

|

| By Sales Channel |

|

| By Region |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.