China Industrial Gases Market Report: Trends, Growth and Forecast (2026-2032)

Gas Type (Nitrogen Gas, Oxygen Gas, Carbon Dioxide Gas, Argon Gas, Helium Gas, Hydrogen Gas, Other), Supply Mode (Cylinders, Bulk, On-Site Production (OSP), Captive, Other), Application (Combustion and Process Oxygen, Welding and Metal Fabrication, Inerting Blanketing and Heat Treating, Cryogenics and liquefaction, Chemical Synthesis and Hydrogenation, Purging and Purifications, Analytical and Calibration), End User Industry (General Manufacturing, Food, Metallurgy, Chemicals, Healthcare, Electronics, Refining & Energy, Glass, Pulp & Paper, Others) ... Read more

|

Major Players

|

China Industrial Gases Market Statistics and Insights, 2026

- Market Size Statistics

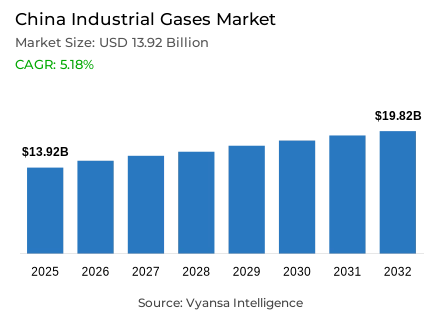

- Industrial gases market size in China was estimated at USD 13.92 billion in 2025.

- The market size is expected to grow to USD 19.82 billion by 2032.

- Market to register a CAGR of around 5.18% during 2026-32.

- Gas Type Shares

- Oxygen gas grabbed market share of 30%.

- Competition

- More than 10 companies are actively engaged in producing industrial gases in China.

- Top 5 companies acquired around 50% of the market share.

- StealthGas Inc, Iwatani Corporation, Yingde Gases, Linde plc, Air Products etc., are few of the top companies.

- Supply Mode

- On-site production (osp) grabbed 35% of the market.

China Industrial Gases Market Outlook

The China industrial gases market is set to experience a consistent growth, increasing to USD 19.82 billion in 2032, up to USD 13.92 billion in 2025, with a CAGR of approximately 5.18% in 2026-2032. The manufacturing base of the country remains a strong demand of industrial gases, which is supported by a 5.8% increase in industrial output in 2024. The rapid expansion of equipment and high-technology production, as well as the strong production of new energy vehicles and semiconductors, is maintaining the extensive use of oxygen, nitrogen, and argon in the metallurgical, chemical, and precision engineering industries.

The tightening of environmental regulations is transforming the operational strategies of gas producers. The current attempts of the government to address the issue of ozone pollution and improve the quality of air demand more stringent emission regulations and investments in cleaner production technologies. To meet these requirements and maintain the supply of key industries like steel and chemicals, producers are working on energy efficiency and integrating modern monitoring systems.

The structure of the market is also changing as the green hydrogen initiatives of China are increasing. By 2024, installed green hydrogen capacity had reached 125,000 metric tons per year, supported by 35 new projects and 4.9 GW of electrolyser manufacturing capacity. These advancements put industrial gas suppliers in line with the decarbonisation objectives of the country, with more than 600 hydrogen projects being built or planned to combine renewable energy with gas production.

Oxygen is the most common type of gas, with 30% of the total market share because of its necessity in steel making and chemical processing. In the meantime, on-site production (OSP) is the most prevalent mode of supply with a 35% share, which provides uninterrupted and cost-effective delivery to large-scale industrial clients. All these trends point to the fact that China is moving towards high-efficiency, sustainable, and technology-based industrial gas operations by 2032.

China Industrial Gases Market Growth Driver

Expanding Industrial Output Reinforcing Gas Consumption

The increasing pace of industrial production in China is creating a sustained demand of industrial gases in its growing manufacturing sector. The value-added industrial output of the country increased by 5.8% annually in 2024, compared to 4.6% in 2023, with equipment and high-tech manufacturing industries recording growth of 7.7% and 8.9% respectively, according to the National Bureau of Statistics. In 2024, manufacturing GDP was USD 4.67 trillion, which is almost a quarter of the national GDP, demonstrating the high interdependence between industrial production and industrial gas demand in various downstream industries.

The automotive industry, which is a significant gas-intensive industry, manufactured 12.89 million new energy vehicles in 2024, an increase of 38.7%, generating large-scale oxygen and nitrogen requirements in the welding and fabrication process. Equally, integrated circuit production increased by 22.2%, which increased gas usage in semiconductor production. This wide-ranging industrial development maintains steady oxygen, nitrogen, and argon consumption in metallurgical, chemical, and precision engineering processes, which strengthens the structural demand base of the sector.

China Industrial Gases Market Challenge

Environmental Regulations Increasing Compliance Complexity

The increasing environmental controls in China pose an increasing operational risk to industrial gas manufacturers. Although the average PM2.5 levels have improved to 29.3 micrograms per cubic metre in 2024, which is in compliance with the standards over the fifth year in a row, the problem of ozone pollution is still acute, as the national levels increased by 0.7% in early 2024, and the levels in industrial areas, including Fenwei Plain and Beijing-Tianjin-Hebei, have grown by the numbers in the tens. The 2022 Action Plan of the government on Tackling Ozone Pollution requires more stringent emission monitoring and nitrogen-oxide control, which has a direct impact on gas producers located in the vicinity of large manufacturing clusters.

The suppliers of industrial gases are now forced to strike a balance between efficiency in production and environmental compliance because increased operations in the chemicals and non-ferrous metals industries increase the emission of ozone precursors. To comply with regulatory requirements, it is necessary to invest heavily in emission-monitoring systems, catalytic converters, and process-control equipment. These additional expenses, combined with more stringent inspection measures, add to capital-expenditure overheads and force operational optimisation to maintain sustainable supply flow to manufacturing end users.

Unlock Market Intelligence

Explore the market potential with our data-driven report

China Industrial Gases Market Trend

Rapid Expansion of Green Hydrogen Infrastructure

The green hydrogen potential in China is growing at a fast rate as a part of the larger decarbonisation plan. As of December 2024, the installed capacity of green hydrogen production was 125,000 metric tons per year, which is 50% of the global total, and was backed by 35 new projects initiated in the year. According to the National Energy Administration, the electrolyser production capacity in China was 4.9 GW, or 60% of the world capacity, which demonstrates its dominance in the technology of hydrogen production through renewable energy. This massive infrastructure development underscores the efforts of China to combine renewable energy with industrial gas generation.

Although in 2024, only 320,000 metric tons of hydrogen were generated by electrolyzing water, a minor portion of the total hydrogen production of 36.5 million metric tons, the rapid capacity additions are an indicator of a rapid increase in the near future. Over 600 green hydrogen projects are planned or being built, and 90 are already in operation as of September 2025. The industrial gas manufacturers are integrating air-separation plants and renewable energy resources to join this new hydrogen ecosystem, enhancing their role in the low-carbon industrial transformation of China.

China Industrial Gases Market Opportunity

Semiconductor Industry Offering Strategic Growth Prospects

The growing semiconductor production capacity in China presents a great potential to the suppliers of industrial gases. In 2024, the semiconductor market was USD 183 billion, and is projected to grow to USD 295 billion by 2030, with major investments, including the USD 47 billion semiconductor fund announced by the government in May 2024. The production of integrated circuits increased by 22.2% to 4,514 billion units, with the production of ultra-high-purity gases needed in the fabrication and lithography of wafer manufacturing.

Industrial gas companies are also finding themselves getting on-site supply contracts with semiconductor manufacturers who require constant supply of oxygen and nitrogen at high purity requirements. These partnerships facilitate the localised deployment of air-separation units in fabrication plants in major industrial corridors. As China aims to achieve 70% domestic semiconductor sourcing by 2025 and complete import substitution by 2030, gas producers that integrate into these high-tech manufacturing systems are set to enjoy long-term, high-value growth opportunities.

Unlock Market Intelligence

Explore the market potential with our data-driven report

China Industrial Gases Market Segmentation Analysis

By Gas Type

- Nitrogen Gas

- Oxygen Gas

- Carbon Dioxide Gas

- Argon Gas

- Helium Gas

- Hydrogen Gas

- Other

The segment with highest market share under Gas type is Oxygen, accounting for 30% of total market share. Its dominance stems from extensive applications across steel manufacturing, chemical processing, and metal fabrication, where it enhances combustion efficiency and supports blast furnace operations. China produced 1.005 billion metric tons of crude steel in 2024, sustaining substantial oxygen demand across integrated steel mills. Despite state-imposed capacity controls, absolute steel output levels remain high, maintaining stable oxygen consumption across metallurgical end users.

In addition to metals production, oxygen demand spans water treatment, chemical synthesis, and medical applications, broadening its industrial relevance. The gas’s critical role in diverse and energy-intensive processes makes it the most revenue-generating segment of the market. Investment in large-scale air separation units to meet growing oxygen requirements is expanding across key manufacturing hubs, reflecting industrial gas producers’ strategic focus on this high-volume, multipurpose segment.

By Supply Mode

- Cylinders

- Bulk

- On-Site Production (OSP)

- Captive

- Other

The segment with highest market share under supply mode is On-site production (OSP), commanding 35% of total share. Dedicated air separation units within customer facilities enable continuous, large-volume supply with optimized cost structures and operational efficiency. End users in steel, chemical, semiconductor, and refining sectors favor OSP systems for their ability to ensure uninterrupted production while maintaining precise purity standards critical to high-value manufacturing processes.

The expansion of on-site systems aligns with China’s industrial modernization agenda, which promotes large, integrated manufacturing clusters. Government-backed investments in infrastructure and advanced air separation technologies are further supporting this supply model’s adoption. As industrial operations scale up across coastal and inland provinces, on-site production offers economic and logistical advantages over packaged or bulk delivery methods, ensuring reliability and long-term competitiveness for industrial gas suppliers serving China’s energy-intensive industries.

List of Companies Covered in China Industrial Gases Market

The companies listed below are highly influential in the China industrial gases market, with a significant market share and a strong impact on industry developments.

- StealthGas Inc

- Iwatani Corporation

- Yingde Gases

- Linde plc

- Air Products

- Air Liquide

- Nippon Sanso Holdings Corp

- SOL Group

- Air Water Inc.

- HangYang

Market News & Updates

- Linde plc, 2025:

Invested over USD 400 million in the Blue Point ASU project in Louisiana, driving revenue growth through new oxygen, nitrogen, and hydrogen supply.

- Air Liquide, 2025:

Added seven new Carrier Gas units across Asia, boosting electronics business growth by 6.3% despite weaker helium demand in China.

Frequently Asked Questions

Related Report

1. Market Segmentation

1.1. Research Scope

1.2. Research Methodology

1.3. Definitions and Assumptions

2. Executive Summary

3. China Industrial Gases Market Policies, Regulations, and Standards

4. China Industrial Gases Market Dynamics

4.1. Growth Factors

4.2. Challenges

4.3. Trends

4.4. Opportunities

5. China Industrial Gases Market Statistics, 2022-2032F

5.1. Market Size & Growth Outlook

5.1.1.By Revenues in USD Million

5.2. Market Segmentation & Growth Outlook

5.2.1.By Gas Type

5.2.1.1. Nitrogen Gas- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2. Oxygen Gas- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3. Carbon Dioxide Gas- Market Insights and Forecast 2022-2032, USD Million

5.2.1.4. Argon Gas- Market Insights and Forecast 2022-2032, USD Million

5.2.1.5. Helium Gas- Market Insights and Forecast 2022-2032, USD Million

5.2.1.6. Hydrogen Gas- Market Insights and Forecast 2022-2032, USD Million

5.2.1.7. Other- Market Insights and Forecast 2022-2032, USD Million

5.2.2.By Supply Mode

5.2.2.1. Cylinders- Market Insights and Forecast 2022-2032, USD Million

5.2.2.2. Bulk- Market Insights and Forecast 2022-2032, USD Million

5.2.2.3. On-Site Production (OSP)- Market Insights and Forecast 2022-2032, USD Million

5.2.2.4. Captive- Market Insights and Forecast 2022-2032, USD Million

5.2.2.5. Other- Market Insights and Forecast 2022-2032, USD Million

5.2.3.By Application

5.2.3.1. Combustion and Process Oxygen- Market Insights and Forecast 2022-2032, USD Million

5.2.3.2. Welding and Metal Fabrication- Market Insights and Forecast 2022-2032, USD Million

5.2.3.3. Inerting Blanketing and Heat Treating- Market Insights and Forecast 2022-2032, USD Million

5.2.3.4. Cryogenics and liquefaction- Market Insights and Forecast 2022-2032, USD Million

5.2.3.5. Chemical Synthesis and Hydrogenation- Market Insights and Forecast 2022-2032, USD Million

5.2.3.6. Purging and Purifications- Market Insights and Forecast 2022-2032, USD Million

5.2.3.7. Analytical and Calibration- Market Insights and Forecast 2022-2032, USD Million

5.2.4.By End User Industry

5.2.4.1. General Manufacturing- Market Insights and Forecast 2022-2032, USD Million

5.2.4.2. Food- Market Insights and Forecast 2022-2032, USD Million

5.2.4.3. Metallurgy- Market Insights and Forecast 2022-2032, USD Million

5.2.4.4. Chemicals- Market Insights and Forecast 2022-2032, USD Million

5.2.4.5. Healthcare- Market Insights and Forecast 2022-2032, USD Million

5.2.4.6. Electronics- Market Insights and Forecast 2022-2032, USD Million

5.2.4.7. Refining & Energy- Market Insights and Forecast 2022-2032, USD Million

5.2.4.8. Glass- Market Insights and Forecast 2022-2032, USD Million

5.2.4.9. Pulp & Paper- Market Insights and Forecast 2022-2032, USD Million

5.2.4.10. Others- Market Insights and Forecast 2022-2032, USD Million

5.2.5.By Competitors

5.2.5.1. Competition Characteristics

5.2.5.2. Market Share & Analysis

6. China Nitrogen Gas Market Statistics, 2022-2032

6.1. Market Size & Growth Outlook

6.1.1.By Revenues in USD Million

6.2. Market Segmentation & Growth Outlook

6.2.1.By Supply Mode- Market Insights and Forecast 2022-2032, USD Million

6.2.2.By Application- Market Insights and Forecast 2022-2032, USD Million

6.2.3.By End User Industry- Market Insights and Forecast 2022-2032, USD Million

7. China Oxygen Gas Market Statistics, 2022-2032

7.1. Market Size & Growth Outlook

7.1.1.By Revenues in USD Million

7.2. Market Segmentation & Growth Outlook

7.2.1.By Supply Mode- Market Insights and Forecast 2022-2032, USD Million

7.2.2.By Application- Market Insights and Forecast 2022-2032, USD Million

7.2.3.By End User Industry- Market Insights and Forecast 2022-2032, USD Million

8. China Carbon Dioxide Gas Market Statistics, 2022-2032

8.1. Market Size & Growth Outlook

8.1.1.By Revenues in USD Million

8.2. Market Segmentation & Growth Outlook

8.2.1.By Supply Mode- Market Insights and Forecast 2022-2032, USD Million

8.2.2.By Application- Market Insights and Forecast 2022-2032, USD Million

8.2.3.By End User Industry- Market Insights and Forecast 2022-2032, USD Million

9. China Argon Gas Market Statistics, 2022-2032

9.1. Market Size & Growth Outlook

9.1.1.By Revenues in USD Million

9.2. Market Segmentation & Growth Outlook

9.2.1.By Supply Mode- Market Insights and Forecast 2022-2032, USD Million

9.2.2.By Application- Market Insights and Forecast 2022-2032, USD Million

9.2.3.By End User Industry- Market Insights and Forecast 2022-2032, USD Million

10. China Helium Gas Market Statistics, 2022-2032

10.1. Market Size & Growth Outlook

10.1.1. By Revenues in USD Million

10.2. Market Segmentation & Growth Outlook

10.2.1. By Supply Mode- Market Insights and Forecast 2022-2032, USD Million

10.2.2. By Application- Market Insights and Forecast 2022-2032, USD Million

10.2.3. By End User Industry- Market Insights and Forecast 2022-2032, USD Million

11. China Hydrogen Gas Market Statistics, 2022-2032

11.1. Market Size & Growth Outlook

11.1.1. By Revenues in USD Million

11.2. Market Segmentation & Growth Outlook

11.2.1. By Supply Mode- Market Insights and Forecast 2022-2032, USD Million

11.2.2. By Application- Market Insights and Forecast 2022-2032, USD Million

11.2.3. By End User Industry- Market Insights and Forecast 2022-2032, USD Million

12. Competitive Outlook

12.1. Company Profiles

12.1.1. Linde plc

12.1.1.1. Business Description

12.1.1.2. Product Portfolio

12.1.1.3. Collaborations & Alliances

12.1.1.4. Recent Developments

12.1.1.5. Financial Details

12.1.1.6. Others

12.1.2. Air Products

12.1.2.1. Business Description

12.1.2.2. Product Portfolio

12.1.2.3. Collaborations & Alliances

12.1.2.4. Recent Developments

12.1.2.5. Financial Details

12.1.2.6. Others

12.1.3. Air Liquide

12.1.3.1. Business Description

12.1.3.2. Product Portfolio

12.1.3.3. Collaborations & Alliances

12.1.3.4. Recent Developments

12.1.3.5. Financial Details

12.1.3.6. Others

12.1.4. Nippon Sanso Holdings Corp

12.1.4.1. Business Description

12.1.4.2. Product Portfolio

12.1.4.3. Collaborations & Alliances

12.1.4.4. Recent Developments

12.1.4.5. Financial Details

12.1.4.6. Others

12.1.5. SOL Group

12.1.5.1. Business Description

12.1.5.2. Product Portfolio

12.1.5.3. Collaborations & Alliances

12.1.5.4. Recent Developments

12.1.5.5. Financial Details

12.1.5.6. Others

12.1.6. StealthGas Inc

12.1.6.1. Business Description

12.1.6.2. Product Portfolio

12.1.6.3. Collaborations & Alliances

12.1.6.4. Recent Developments

12.1.6.5. Financial Details

12.1.6.6. Others

12.1.7. Iwatani Corporation

12.1.7.1. Business Description

12.1.7.2. Product Portfolio

12.1.7.3. Collaborations & Alliances

12.1.7.4. Recent Developments

12.1.7.5. Financial Details

12.1.7.6. Others

12.1.8. Yingde Gases

12.1.8.1. Business Description

12.1.8.2. Product Portfolio

12.1.8.3. Collaborations & Alliances

12.1.8.4. Recent Developments

12.1.8.5. Financial Details

12.1.8.6. Others

12.1.9. Air Water Inc.

12.1.9.1. Business Description

12.1.9.2. Product Portfolio

12.1.9.3. Collaborations & Alliances

12.1.9.4. Recent Developments

12.1.9.5. Financial Details

12.1.9.6. Others

12.1.10. HangYang

12.1.10.1.Business Description

12.1.10.2.Product Portfolio

12.1.10.3.Collaborations & Alliances

12.1.10.4.Recent Developments

12.1.10.5.Financial Details

12.1.10.6.Others

13. Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Gas Type |

|

| By Supply Mode |

|

| By Application |

|

| By End User Industry |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.