Chile Juice Market Report: Trends, Growth and Forecast (2026-2032)

By Category (100% Juice (Not from Concentrate, Reconstituted), Juice Drinks (up to 24% Juice), Nectars (High Concentration (40% to 50% fruit content), Medium Concentration (30% to 39% fruit content), Low Concentration (25% to 29% fruit content)), Vegetable Juice, Fruit and Vegetable Blends), By Nature (Conventional, Organic), By Packaging Material (Plastic, Glass, Metal, Others), By Packaging Type (PET Bottles, Aseptic Packages (Cartons), Glass Bottles, Metal Cans, Disposable Cups & Pouches), By Sales Channel (Off-Trade (Hypermarkets/ Supermarkets, Retail Outlets, Convenience Stores, Online Platforms), On-Trade) ... Read more

|

Major Players

|

Chile Juice Market Statistics and Insights, 2026

- Market Size Statistics

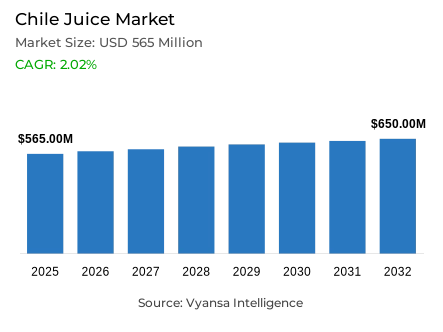

- Juice market size in Chile was estimated at USD 565 million in 2025.

- The market size is expected to grow to USD 650 million by 2032.

- Market to register a CAGR of around 2.02% during 2026-32.

- Category Shares

- Nectars grabbed market share of 70%.

- Competition

- More than 15 companies are actively engaged in producing juice in Chile.

- Top 5 companies acquired around 75% of the market share.

- Jugos Bless SA, Inter Asian Food Spa, Soprole SA, Promarca SA, Coca-Cola de Chile SA etc., are few of the top companies.

- Sales Channel

- Off-trade grabbed 80% of the market.

Chile Juice Market Outlook

The Chile juice market is going through a recovery phase after facing serious climatic and economic difficulties. The extreme weather and increasing prices of oranges in 2025 caused the transition to cheaper alternatives, including reconstituted juice and non-citrus blends. The market is still strong despite these challenges as the economic condition is getting better. It is estimated that the market will reach US 565 million in 2025 and will reach US 650 million by 2032 with a CAGR of about 2.02 percent in the 2026-32 period.

A trade-off between health and price is becoming a defining feature of end user behaviour. Although high inflation has forced shoppers to seek cheaper options at first, the trend towards natural and healthy products is on the rise. With the adjustment of wages and stabilisation of the economy, 100% juice is expected to record the best retail growth. Manufacturers are already adjusting to this by substituting the costly orange with flavours like peach, mango and strawberry to ensure that they remain accessible and yet satisfy the quality demand.

Sustainability is also emerging as a popular driver, especially among the younger generations. More than 50 percent of Chile end users are actively decreasing plastic consumption, and the general shift to glass and Tetra Pak packaging is observed. This trend does not only apply to high-end brands, with mainstream nectar brands like Watts and Vivo progressively using environmentally friendly materials. Brand owners are also targeting particular formats, including small 115 ml-200 ml cartons to children, to access more consistent segments of demand.

The distribution environment is well established in the home consumption, with 80 % of the market being controlled by the Off-Trade channels. Although the small grocers are under pressure due to the scale and promotions of the supermarkets, e-commerce is becoming the channel that is growing at the highest rate. Large retailers and direct-to-end user websites are offering superior value with quantity packages and home delivery. The market is in a good position to transform into a more sustainable and health-conscious future by 2032 with nectars already controlling 70 % of the market.

Chile Juice Market Growth Driver

Increasing Health Awareness Boosts Demand for Nutrient-Rich Juices

The Chile end users are increasingly becoming aware of the need to eat healthy as a way of ensuring long term health. The 2026 guidelines of the World Health Organization on a healthy diet highlight that a diet high in a wide range of minimally processed foods, such as fruits and vegetables, can protect against non-communicable diseases, including heart disease, diabetes, and obesity, by supplying the body with the necessary nutrients and minimizing the consumption of unhealthy fats, sugars, and sodium. This is a global public-health message that is shaping local food and beverage preferences, with end users favoring beverages that are seen as natural and rich in nutrients, including 100 % fruit juices.

Diet-related health problems are also high in Chile, which supports the need to offer healthier choices 33.7 % of adult women and 27.6 % of adult men are obese, as per the Global Nutrition Report, which highlights a population emphasis on better diets. This increased health consciousness is leading to a shift towards juices that contain more fruit and less added sugar, and segments that are healthier and positioned as such in the beverage market.

Chile Juice Market Challenge

Persistent Inflation and Food Price Pressures Restrain Consumption

The inflationary conditions in Chile is also a significant limitation to end user expenditure especially on price elastic goods like retail juices. Despite the fact that headline inflation has decreased to about 3.5 % by December 2025, food and non-alcoholic beverage prices, which are the key inputs in making juice affordable, have been increasing at a higher rate with food inflation of about 4.1 % reported by the National Statistics Institute of Chile at the end of 2025. High food prices lower discretionary spending on high-priced or premium juice products because households focus on necessary spending.

This inflationary pressure exacerbates cost pressures on farmers and producers. Although overall inflation has been tamed, price fluctuations in inputs and wages may undermine the real purchasing power of end users, making them more prone to trade down to less expensive beverage substitutes or lower quality juice blends. In this regard, the long-term price pressures are a structural issue to the juice market to be able to grow higher-value segments, especially in situations where end users have competing budget pressures across categories.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Chile Juice Market Trend

Rising Internet Connectivity Shapes Consumer Buying Patterns

The level of digital connectivity in Chile is very high and this has opened new opportunities where end users can learn about and buy beverages. According to World Bank statistics, about 94.46 % of the Chile population had access to the internet by 2023, which is a wide range of digital access among demographics. This ubiquitous connectivity underpins online search, social interaction, and e-commerce behaviours that affect food and beverage purchases, such as juices and other related products.

With the increased integration of internet into everyday life, end users are increasingly browsing product selections, price shopping and interacting with brands online prior to purchase. Digital marketing efforts by beverage companies and retailers are also supported by mobile and broadband penetration, allowing them to do targeted promotions and content that emphasize the benefits of the product, like natural ingredients or functional nutrition. This move towards online interaction is a definite behavioural pattern that defines the way Chiles relate to juice brands, beyond the conventional in-store shopping.

Chile Juice Market Opportunity

Digital Commerce Expansion Offers Growth Avenues for Juice Sales

The high internet penetration in Chile is not only a sign of connectivity but also allows juice brands and retailers to engage in more e-commerce. As internet penetration hits over 94 % of the population, online platforms are emerging as a standardised way of buying groceries and beverages, providing convenience, increased product choice, and home delivery. Retailers and juice manufacturers can use this digital infrastructure to launch bundled deals, subscription plans, and customised product suggestions that attract diverse end user groups.

This e-commerce wave is a strategic chance to reach younger, digitally-sensitive customers who are more concerned with convenience and value. Smaller-format pack promotions, sampling campaigns, and direct-to-end user brand storytelling can be supported online and may be harder to execute through traditional retail. Through the combination of online sales and the presence of strong digital marketing and logistics, the players in the juice market will be able to increase their reach and build stronger relationships with end users in an ever-omnichannel retail world.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Chile Juice Market Segmentation Analysis

By Category

- 100% Juice

- Not from Concentrate

- Reconstituted

- Juice Drinks (up to 24% Juice)

- Nectars

- High Concentration (40% to 50% fruit content)

- Medium Concentration (30% to 39% fruit content)

- Low Concentration (25% to 29% fruit content)

- Vegetable Juice

- Fruit and Vegetable Blends

The segment has the highest share around the category for the Chilean market, where Nectars grabbed a market share of 70%. This dominance is largely due to their lower price point compared to premium 100% juices, making them the preferred choice for cost-conscious households. Even as climatic issues pushed up the cost of raw ingredients, nectars remained the best-selling format in volume terms. Brands like Watt’s have consolidated this lead by innovating with affordable, smaller formats designed for school lunchboxes and on-the-go consumption.

While nectars remain the top-performing category, they are undergoing a significant transformation toward sustainability and health. Producers are increasingly moving away from plastic bottles in favor of Tetra Pak packaging and incorporating local fruits to diversify flavors. Although 100% juice is expected to see faster growth as the economy recovers, the widespread availability and affordability of nectars ensure they will remain the primary segment in Chile through the 2032 forecast period.

By Sales Channel

- Off-Trade

- Hypermarkets/ Supermarkets

- Retail Outlets

- Convenience Stores

- Online Platforms

- On-Trade

The segment has the highest share around the Sales Channel is Off-Trade, which grabbed 80% of the market. This high share reflects the fact that juice is a staple of the Chilean family diet, primarily purchased for consumption at home. While small local grocers historically led this channel, they are facing stiff competition from supermarkets and hypermarkets. These modern retailers use their large scale to offer more competitive pricing and aggressive promotions, which are essential for attracting price-sensitive shoppers in a high-inflation environment.

The digital sub-channel is also seeing rapid development, benefiting from high internet penetration and a tech-savvy younger population. Major supermarket chains and independent players like Jugos Bless are investing in sophisticated e-commerce platforms and direct-to-end user delivery. These online stores are becoming increasingly popular for bulk-buying and specialized organic options, ensuring that off-trade distribution remains the dominant force in the Chilean juice market through 2032.

List of Companies Covered in Chile Juice Market

The companies listed below are highly influential in the Chile juice market, with a significant market share and a strong impact on industry developments.

- Jugos Bless SA

- Inter Asian Food Spa

- Soprole SA

- Promarca SA

- Coca-Cola de Chile SA

- Guallarauco SA

- Empresas Carozzi SA

- Tresmontes Lucchetti SA

- Walmart Chile SA

- Sofruco Alimentos Ltda

Competitive Landscape

Chile juice market in 2025 is characterised by consolidation at the top and selective disruption at the premium end. Promarca continues to strengthen its leadership, leveraging the breadth of the Watt’s and Frugo portfolios across nectars, reconstituted 100% juice and juice drinks, supported by ongoing format innovation such as small carton packs targeting children and on-the-go occasions. Its scale and pricing flexibility position it well amid inflation and volatile fruit costs. At the same time, Jugos Bless is emerging as the most dynamic challenger, capitalising on strong brand loyalty and expanding into reconstituted 100% juice with competitively priced carton formats. This combination of scale-driven leadership and agile niche expansion defines the current competitive structure.

Frequently Asked Questions

Related Report

1. Market Segmentation

1.1. Research Scope

1.2. Research Methodology

1.3. Definitions and Assumptions

2. Executive Summary

3. Chile Juice Market Policies, Regulations, and Standards

4. Chile Juice Market Dynamics

4.1. Growth Factors

4.2. Challenges

4.3. Trends

4.4. Opportunities

5. Chile Juice Market Statistics, 2022-2032F

5.1. Market Size & Growth Outlook

5.1.1.By Revenues in USD Million

5.1.2.By Quantity Sold in Million Litres

5.2. Market Segmentation & Growth Outlook

5.2.1.By Category

5.2.1.1. 100% Juice- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.1. Not from Concentrate- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.2. Reconstituted- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2. Juice Drinks (up to 24% Juice)- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3. Nectars- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3.1. High Concentration (40% to 50% fruit content)- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3.2. Medium Concentration (30% to 39% fruit content)- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3.3. Low Concentration (25% to 29% fruit content)- Market Insights and Forecast 2022-2032, USD Million

5.2.1.4. Vegetable Juice- Market Insights and Forecast 2022-2032, USD Million

5.2.1.5. Fruit and Vegetable Blends- Market Insights and Forecast 2022-2032, USD Million

5.2.2.By Nature

5.2.2.1. Conventional- Market Insights and Forecast 2022-2032, USD Million

5.2.2.2. Organic- Market Insights and Forecast 2022-2032, USD Million

5.2.3.By Packaging Material

5.2.3.1. Plastic- Market Insights and Forecast 2022-2032, USD Million

5.2.3.2. Glass- Market Insights and Forecast 2022-2032, USD Million

5.2.3.3. Metal- Market Insights and Forecast 2022-2032, USD Million

5.2.3.4. Others- Market Insights and Forecast 2022-2032, USD Million

5.2.4.By Packaging Type

5.2.4.1. PET Bottles- Market Insights and Forecast 2022-2032, USD Million

5.2.4.2. Aseptic Packages (Cartons)- Market Insights and Forecast 2022-2032, USD Million

5.2.4.3. Glass Bottles- Market Insights and Forecast 2022-2032, USD Million

5.2.4.4. Metal Cans- Market Insights and Forecast 2022-2032, USD Million

5.2.4.5. Disposable Cups & Pouches- Market Insights and Forecast 2022-2032, USD Million

5.2.5.By Sales Channel

5.2.5.1. Off-Trade- Market Insights and Forecast 2022-2032, USD Million

5.2.5.1.1. Hypermarkets/ Supermarkets - Market Insights and Forecast 2022-2032, USD Million

5.2.5.1.2. Retail Outlets - Market Insights and Forecast 2022-2032, USD Million

5.2.5.1.3. Convenience Stores- Market Insights and Forecast 2022-2032, USD Million

5.2.5.1.4. Online Platforms- Market Insights and Forecast 2022-2032, USD Million

5.2.5.2. On-Trade- Market Insights and Forecast 2022-2032, USD Million

5.2.6.By Competitors

5.2.6.1. Competition Characteristics

5.2.6.2. Market Share & Analysis

6. Chile 100% Juice Market Statistics, 2022-2032

6.1. Market Size & Growth Outlook

6.1.1.By Revenues in USD Million

6.1.2.By Quantity Sold in Million Litres

6.2. Market Segmentation & Growth Outlook

6.2.1.By Nature- Market Insights and Forecast 2022-2032, USD Million

6.2.2.By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

6.2.3.By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

6.2.4.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

7. Chile Juice Drinks (up to 24% Juice) Market Statistics, 2022-2032

7.1. Market Size & Growth Outlook

7.1.1.By Revenues in USD Million

7.1.2.By Quantity Sold in Million Litres

7.2. Market Segmentation & Growth Outlook

7.2.1.By Nature- Market Insights and Forecast 2022-2032, USD Million

7.2.2.By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

7.2.3.By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

7.2.4.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

8. Chile Nectars Market Statistics, 2022-2032

8.1. Market Size & Growth Outlook

8.1.1.By Revenues in USD Million

8.1.2.By Quantity Sold in Million Litres

8.2. Market Segmentation & Growth Outlook

8.2.1.By Nature- Market Insights and Forecast 2022-2032, USD Million

8.2.2.By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

8.2.3.By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

8.2.4.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

9. Chile Vegetable Juice Market Statistics, 2022-2032

9.1. Market Size & Growth Outlook

9.1.1.By Revenues in USD Million

9.1.2.By Quantity Sold in Million Litres

9.2. Market Segmentation & Growth Outlook

9.2.1.By Nature- Market Insights and Forecast 2022-2032, USD Million

9.2.2.By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

9.2.3.By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

9.2.4.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

10. Chile Fruit and Vegetable Blends Market Statistics, 2022-2032

10.1. Market Size & Growth Outlook

10.1.1. By Revenues in USD Million

10.1.2. By Quantity Sold in Million Litres

10.2. Market Segmentation & Growth Outlook

10.2.1. By Nature- Market Insights and Forecast 2022-2032, USD Million

10.2.2. By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

10.2.3. By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

10.2.4. By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

11. Competitive Outlook

11.1. Company Profiles

11.1.1. Promarca SA

11.1.1.1. Business Description

11.1.1.2. Product Portfolio

11.1.1.3. Collaborations & Alliances

11.1.1.4. Recent Developments

11.1.1.5. Financial Details

11.1.1.6. Others

11.1.2. Coca-Cola de Chile SA

11.1.2.1. Business Description

11.1.2.2. Product Portfolio

11.1.2.3. Collaborations & Alliances

11.1.2.4. Recent Developments

11.1.2.5. Financial Details

11.1.2.6. Others

11.1.3. Guallarauco SA

11.1.3.1. Business Description

11.1.3.2. Product Portfolio

11.1.3.3. Collaborations & Alliances

11.1.3.4. Recent Developments

11.1.3.5. Financial Details

11.1.3.6. Others

11.1.4. Empresas Carozzi SA

11.1.4.1. Business Description

11.1.4.2. Product Portfolio

11.1.4.3. Collaborations & Alliances

11.1.4.4. Recent Developments

11.1.4.5. Financial Details

11.1.4.6. Others

11.1.5. Tresmontes Lucchetti SA

11.1.5.1. Business Description

11.1.5.2. Product Portfolio

11.1.5.3. Collaborations & Alliances

11.1.5.4. Recent Developments

11.1.5.5. Financial Details

11.1.5.6. Others

11.1.6. Jugos Bless SA

11.1.6.1. Business Description

11.1.6.2. Product Portfolio

11.1.6.3. Collaborations & Alliances

11.1.6.4. Recent Developments

11.1.6.5. Financial Details

11.1.6.6. Others

11.1.7. Inter Asian Food SpA

11.1.7.1. Business Description

11.1.7.2. Product Portfolio

11.1.7.3. Collaborations & Alliances

11.1.7.4. Recent Developments

11.1.7.5. Financial Details

11.1.7.6. Others

11.1.8. Soprole SA

11.1.8.1. Business Description

11.1.8.2. Product Portfolio

11.1.8.3. Collaborations & Alliances

11.1.8.4. Recent Developments

11.1.8.5. Financial Details

11.1.8.6. Others

11.1.9. Walmart Chile SA

11.1.9.1. Business Description

11.1.9.2. Product Portfolio

11.1.9.3. Collaborations & Alliances

11.1.9.4. Recent Developments

11.1.9.5. Financial Details

11.1.9.6. Others

11.1.10. Sofruco Alimentos Ltda

11.1.10.1.Business Description

11.1.10.2.Product Portfolio

11.1.10.3.Collaborations & Alliances

11.1.10.4.Recent Developments

11.1.10.5.Financial Details

11.1.10.6.Others

12. Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Category |

|

| By Nature |

|

| By Packaging Material |

|

| By Packaging Type |

|

| By Sales Channel |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.