Canada Juice Market Report: Trends, Growth and Forecast (2026-2032)

By Category (100% Juice (Not from Concentrate, Reconstituted), Juice Drinks (up to 24% Juice), Nectars (High Concentration (40% to 50% fruit content), Medium Concentration (30% to 39% fruit content), Low Concentration (25% to 29% fruit content)), Vegetable Juice, Fruit and Vegetable Blends), By Nature (Conventional, Organic), By Packaging Material (Plastic, Glass, Metal, Others), By Packaging Type (PET Bottles, Aseptic Packages (Cartons), Glass Bottles, Metal Cans, Disposable Cups & Pouches), By Sales Channel (Off-Trade (Hypermarkets/ Supermarkets, Retail Outlets, Convenience Stores, Online Platforms), On-Trade) ... Read more

|

Major Players

|

Canada Juice Market Statistics and Insights, 2026

- Market Size Statistics

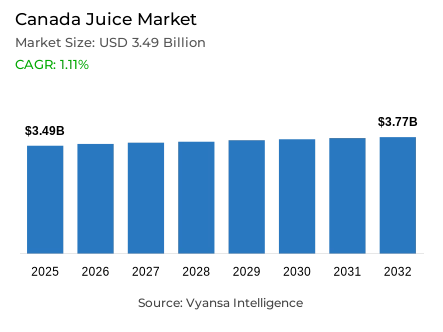

- Juice market size in Canada was estimated at USD 3.49 billion in 2025.

- The market size is expected to grow to USD 3.77 billion by 2032.

- Market to register a CAGR of around 1.11% during 2026-32.

- Category Shares

- 100% juice grabbed market share of 75%.

- Competition

- More than 20 companies are actively engaged in producing juice in Canada.

- Top 5 companies acquired around 60% of the market share.

- Ocean Spray Cranberries Inc, Campbell's Co, Snapple Beverage Corp, PepsiCo Beverages Canada, A Lassonde Inc etc., are few of the top companies.

- Sales Channel

- Off-trade grabbed 75% of the market.

Canada Juice Market Outlook

Canada juice market is in a structural adjustment phase with end users weighing a sugar budget against high retail prices. Despite the fact that inflation started to decrease in 2025, the shelf prices of core products like orange juice were still high because there were severe supply shortages in Florida and other major areas. In line with these issues, the market is estimated to be worth 3.49 billion dollars in 2025 and is expected to grow to 3.77 billion dollars by 2032 with a low CAGR of about 1.11 % over the forecast period.

The volume consumption will keep decreasing gradually, mainly due to the old health trends and the general dislike of sugar. A large number of Canadas are moving towards flavored sparkling water, plant waters, and functional drinks that better fit their wellness objectives. These headwinds notwithstanding, 100 Juice is the leading category with a 75 % market share, but it is under growing pressure due to new front-of-pack labelling laws that will become mandatory in early 2026.

Innovation will be a life-saving factor in the market, and the focus will be on functional benefits, including immunity and digestive health, and sustainability. Major brands such as Lassonde are already going plastic straw-free and switching to recycled PET, and smaller, agile brands like Loop Mission are already picking up with cold-pressed juices made of imperfect fruit. These high-end, values-based niches are likely to perform better than the mainstream market despite the low general demand.

The retail environment is still deeply rooted in home consumption, with 75 % of the market being controlled by the Off-Trade channels. Although the bulk-buying families continue to shop in supermarkets and discounters, online grocery shopping and click-and-collect are becoming a norm. With the market maturing, firms will probably target high-value functional blends and no-sugar-added assertions to stay pertinent in a competitive beverage environment that is becoming more non-alcoholic and sparkling waters.

Canada Juice Market Growth Driver

Clearer labels and online discovery lift premium choices

Commencing 1 January 2026, regulatory requirements in Canada will necessitate the implementation of front-of-package nutrition symbols on prepackaged food products containing elevated levels of sugar, sodium, and/or saturated fat. This regulatory development is expected to drive increased brand investment in prominent nutritional communication and labeling initiatives. Consequently, brands are expected to allocate increased investment toward prominent nutritional labeling and communication strategies. This change forces juice producers to focus on no added sugar, simplify ingredient labels, and create functional blends (electrolytes, immunity, digestion) that are more in line with daily wellness than a sweet treat.

These higher-value propositions are also based on distribution. According to Statistics Canada, retail e-commerce sales amounted to 4.3 billion dollars in December 2024, which is 6.1 % of the total retail trade. This information justifies a weekly shopping routine of click-and-collect and online bundles. An expanded online shelf makes it easier to discover, quickly compare, and buy cold-pressed, plant-water, and functional juice lines using saved carts and recurring orders.

Canada Juice Market Challenge

Price shock and citrus shortages keep demand under strain

Juice is still very price-sensitive and the category still has an inflationary aftereffect. According to Statistics Canada, the price of fruit-juice increased 15.7% annually (February 2023), with non-alcoholic beverages in general increasing 11.1%. As a result, lots of shoppers are cautious and more promotion-oriented, which stimulates downward trading, a shift to concentrates, or avoidance of nice-to-have formats.

There is an added strain of supply-side volatility. The 2024/25 orange crop in Florida is estimated by USDA to be 11.5 million boxes in February 2025, 36 % smaller than last season, which will constrain orange-juice inputs and help orange-heavy products fetch higher prices on shelves. At the same time, the compulsory front-of-pack label of high-sugar foods (since 1 January 2026) puts additional pressure on high-sugar juice drinks and nectars.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Canada Juice Market Trend

Less sugar, more function becomes the default message

The front-of-pack nutrition symbol is becoming mandatory on 1 January 2026, and packaging and claims are increasingly focused on sugar reduction and simpler recipes as the front-of-pack nutrition symbol is required on high-sugar, sodium, and/or saturated fat foods. Brands are using fast cues, like no added sugar, real fruit, electrolytes, clean labels, and refreshing packaging, so that end users can make decisions within seconds.

The shopping habits also change to planned, bundled shopping that is within the budget. Canada retail e-commerce sales increased 3.1% month-over-month to $4.3 billion in December 2024 and comprised 6.1 % of total retail trade, which supports multi-packs, variety packs, and stock-up formats online and in click-and-collect baskets. The trend benefits products that have a distinct value-per-serving, high search visibility, targeted promotions, and simple, consistent nutrition positioning.

Canada Juice Market Opportunity

Reformulation and smart blending create headroom to defend relevance

The 1 January 2026 front-of-pack symbol requirement encourages reformulation to ensure that fewer products will raise a warning about high in sugars, or redesign portions to ensure labels are more comfortable to read. This opens room to lower-sugar juice beverages, lighter nectars, juice-plus-tea mixtures, and functional shots where the benefits are simpler to clarify than sweetness.

Smart blending and sourcing is also promoted by input-cost pressure. As Florida is projected to grow oranges by 2024/25 to 11.5 million boxes (36 % lower than the previous season), brands can grow non-orange blends (apple, berry, tropical), strategically use concentrates, and diversify suppliers to avoid being exposed to one crop shock. Combining these shifts with online bundles (e-commerce sales of 4.3 billion dollars in December 2024) facilitates trial without heavy discounting.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Canada Juice Market Segmentation Analysis

By Category

- 100% Juice

- Not from Concentrate

- Reconstituted

- Juice Drinks (up to 24% Juice)

- Nectars

- High Concentration (40% to 50% fruit content)

- Medium Concentration (30% to 39% fruit content)

- Low Concentration (25% to 29% fruit content)

- Vegetable Juice

- Fruit and Vegetable Blends

The segment has the highest share around segment under the category for the Canadian market, where 100% Juice grabbed a market share of 75%. This dominant position persists despite significant challenges, such as record-high orange juice prices and growing end user concerns over naturally occurring sugars. Most Canadians still view 100% juice as a staple for its perceived nutritional value and absence of artificial additives, ensuring it remains the primary choice for household breakfast routines and family consumption.

However, the segment is undergoing a shift toward premiumization to offset volume declines. Interest in cold-pressed formats and functional blends—which highlight benefits like immunity and bone strength—is growing among health-conscious urban shoppers. While mainstream "from concentrate" products face pressure from sugar-averse end users, these nutrient-dense and minimally processed 100% variants are becoming the category's new centers for growth and innovation.

By Sales Channel

- Off-Trade

- Hypermarkets/ Supermarkets

- Retail Outlets

- Convenience Stores

- Online Platforms

- On-Trade

The segment has the highest share around segment under the Sales Channel is Off-Trade, which grabbed 75% of the market. This high market share is a result of juice being treated as an everyday grocery staple rather than an impulse purchase. Supermarkets and discounters are the dominant forces here, as Canadians increasingly seek value through multi-packs and larger formats to cope with elevated shelf prices. The physical retail environment remains crucial for these products due to their weight and the end user preference for planned, bulk-buying trips.

Simultaneously, the digital landscape is expanding as shoppers integrate online grocery orders into their weekly routines. While click-and-collect is the most popular model for heavy beverage products, major retailers like Loblaws and Walmart Canada are heavily investing in fulfillment infrastructure to support this growth. This multi-channel approach ensures that the off-trade segment remains the cornerstone of juice distribution in Canada through 2032.

List of Companies Covered in Canada Juice Market

The companies listed below are highly influential in the Canada juice market, with a significant market share and a strong impact on industry developments.

- Ocean Spray Cranberries Inc

- Campbell's Co

- Snapple Beverage Corp

- PepsiCo Beverages Canada

- A Lassonde Inc

- Minute Maid Co of Canada

- Sun-Rype Products Ltd

- Loblaw Cos Ltd

- Canada Dry Motts Inc

- Saputo Inc

Competitive Landscape

The competitive landscape for juice in Canada in 2025 remains dominated by large, established players, although they are operating under sustained pressure. Tropicana Brands Group, Lassonde and Minute Maid Co of Canada continue to lead by scale and distribution strength, yet face structural challenges linked to sugar aversion, elevated orange juice input costs and difficulties repositioning legacy portfolios. Efforts to refresh brands through reduced-sugar variants, packaging updates and line extensions have delivered only limited relief. In contrast, smaller and more agile players are gaining visibility by focusing on cold-pressed formats, sustainability and differentiated use occasions. Brands such as Loop Mission and La Presserie are benefiting from premium positioning, food-waste reduction narratives and alignment with wellness and at-home consumption trends, gradually reshaping competitive dynamics at the margins.

Frequently Asked Questions

Related Report

1. Market Segmentation

1.1. Research Scope

1.2. Research Methodology

1.3. Definitions and Assumptions

2. Executive Summary

3. Canada Juice Market Policies, Regulations, and Standards

4. Canada Juice Market Dynamics

4.1. Growth Factors

4.2. Challenges

4.3. Trends

4.4. Opportunities

5. Canada Juice Market Statistics, 2022-2032F

5.1. Market Size & Growth Outlook

5.1.1.By Revenues in USD Million

5.1.2.By Quantity Sold in Million Litres

5.2. Market Segmentation & Growth Outlook

5.2.1.By Category

5.2.1.1. 100% Juice- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.1. Not from Concentrate- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.2. Reconstituted- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2. Juice Drinks (up to 24% Juice)- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3. Nectars- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3.1. High Concentration (40% to 50% fruit content)- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3.2. Medium Concentration (30% to 39% fruit content)- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3.3. Low Concentration (25% to 29% fruit content)- Market Insights and Forecast 2022-2032, USD Million

5.2.1.4. Vegetable Juice- Market Insights and Forecast 2022-2032, USD Million

5.2.1.5. Fruit and Vegetable Blends- Market Insights and Forecast 2022-2032, USD Million

5.2.2.By Nature

5.2.2.1. Conventional- Market Insights and Forecast 2022-2032, USD Million

5.2.2.2. Organic- Market Insights and Forecast 2022-2032, USD Million

5.2.3.By Packaging Material

5.2.3.1. Plastic- Market Insights and Forecast 2022-2032, USD Million

5.2.3.2. Glass- Market Insights and Forecast 2022-2032, USD Million

5.2.3.3. Metal- Market Insights and Forecast 2022-2032, USD Million

5.2.3.4. Others- Market Insights and Forecast 2022-2032, USD Million

5.2.4.By Packaging Type

5.2.4.1. PET Bottles- Market Insights and Forecast 2022-2032, USD Million

5.2.4.2. Aseptic Packages (Cartons)- Market Insights and Forecast 2022-2032, USD Million

5.2.4.3. Glass Bottles- Market Insights and Forecast 2022-2032, USD Million

5.2.4.4. Metal Cans- Market Insights and Forecast 2022-2032, USD Million

5.2.4.5. Disposable Cups & Pouches- Market Insights and Forecast 2022-2032, USD Million

5.2.5.By Sales Channel

5.2.5.1. Off-Trade- Market Insights and Forecast 2022-2032, USD Million

5.2.5.1.1. Hypermarkets/ Supermarkets - Market Insights and Forecast 2022-2032, USD Million

5.2.5.1.2. Retail Outlets - Market Insights and Forecast 2022-2032, USD Million

5.2.5.1.3. Convenience Stores- Market Insights and Forecast 2022-2032, USD Million

5.2.5.1.4. Online Platforms- Market Insights and Forecast 2022-2032, USD Million

5.2.5.2. On-Trade- Market Insights and Forecast 2022-2032, USD Million

5.2.6.By Competitors

5.2.6.1. Competition Characteristics

5.2.6.2. Market Share & Analysis

6. Canada 100% Juice Market Statistics, 2022-2032

6.1. Market Size & Growth Outlook

6.1.1.By Revenues in USD Million

6.1.2.By Quantity Sold in Million Litres

6.2. Market Segmentation & Growth Outlook

6.2.1.By Nature- Market Insights and Forecast 2022-2032, USD Million

6.2.2.By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

6.2.3.By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

6.2.4.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

7. Canada Juice Drinks (up to 24% Juice) Market Statistics, 2022-2032

7.1. Market Size & Growth Outlook

7.1.1.By Revenues in USD Million

7.1.2.By Quantity Sold in Million Litres

7.2. Market Segmentation & Growth Outlook

7.2.1.By Nature- Market Insights and Forecast 2022-2032, USD Million

7.2.2.By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

7.2.3.By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

7.2.4.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

8. Canada Nectars Market Statistics, 2022-2032

8.1. Market Size & Growth Outlook

8.1.1.By Revenues in USD Million

8.1.2.By Quantity Sold in Million Litres

8.2. Market Segmentation & Growth Outlook

8.2.1.By Nature- Market Insights and Forecast 2022-2032, USD Million

8.2.2.By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

8.2.3.By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

8.2.4.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

9. Canada Vegetable Juice Market Statistics, 2022-2032

9.1. Market Size & Growth Outlook

9.1.1.By Revenues in USD Million

9.1.2.By Quantity Sold in Million Litres

9.2. Market Segmentation & Growth Outlook

9.2.1.By Nature- Market Insights and Forecast 2022-2032, USD Million

9.2.2.By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

9.2.3.By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

9.2.4.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

10. Canada Fruit and Vegetable Blends Market Statistics, 2022-2032

10.1. Market Size & Growth Outlook

10.1.1. By Revenues in USD Million

10.1.2. By Quantity Sold in Million Litres

10.2. Market Segmentation & Growth Outlook

10.2.1. By Nature- Market Insights and Forecast 2022-2032, USD Million

10.2.2. By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

10.2.3. By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

10.2.4. By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

11. Competitive Outlook

11.1. Company Profiles

11.1.1. PepsiCo Beverages Canada

11.1.1.1. Business Description

11.1.1.2. Product Portfolio

11.1.1.3. Collaborations & Alliances

11.1.1.4. Recent Developments

11.1.1.5. Financial Details

11.1.1.6. Others

11.1.2. A Lassonde Inc

11.1.2.1. Business Description

11.1.2.2. Product Portfolio

11.1.2.3. Collaborations & Alliances

11.1.2.4. Recent Developments

11.1.2.5. Financial Details

11.1.2.6. Others

11.1.3. Minute Maid Co of Canada

11.1.3.1. Business Description

11.1.3.2. Product Portfolio

11.1.3.3. Collaborations & Alliances

11.1.3.4. Recent Developments

11.1.3.5. Financial Details

11.1.3.6. Others

11.1.4. Sun-Rype Products Ltd

11.1.4.1. Business Description

11.1.4.2. Product Portfolio

11.1.4.3. Collaborations & Alliances

11.1.4.4. Recent Developments

11.1.4.5. Financial Details

11.1.4.6. Others

11.1.5. Loblaw Cos Ltd

11.1.5.1. Business Description

11.1.5.2. Product Portfolio

11.1.5.3. Collaborations & Alliances

11.1.5.4. Recent Developments

11.1.5.5. Financial Details

11.1.5.6. Others

11.1.6. Ocean Spray Cranberries Inc

11.1.6.1. Business Description

11.1.6.2. Product Portfolio

11.1.6.3. Collaborations & Alliances

11.1.6.4. Recent Developments

11.1.6.5. Financial Details

11.1.6.6. Others

11.1.7. Campbell's Co, The

11.1.7.1. Business Description

11.1.7.2. Product Portfolio

11.1.7.3. Collaborations & Alliances

11.1.7.4. Recent Developments

11.1.7.5. Financial Details

11.1.7.6. Others

11.1.8. Snapple Beverage Corp

11.1.8.1. Business Description

11.1.8.2. Product Portfolio

11.1.8.3. Collaborations & Alliances

11.1.8.4. Recent Developments

11.1.8.5. Financial Details

11.1.8.6. Others

11.1.9. Canada Dry Motts Inc

11.1.9.1. Business Description

11.1.9.2. Product Portfolio

11.1.9.3. Collaborations & Alliances

11.1.9.4. Recent Developments

11.1.9.5. Financial Details

11.1.9.6. Others

11.1.10. Saputo Inc

11.1.10.1.Business Description

11.1.10.2.Product Portfolio

11.1.10.3.Collaborations & Alliances

11.1.10.4.Recent Developments

11.1.10.5.Financial Details

11.1.10.6.Others

12. Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Category |

|

| By Nature |

|

| By Packaging Material |

|

| By Packaging Type |

|

| By Sales Channel |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.