Canada Bags and Luggage Market Report: Trends, Growth and Forecast (2026-2032)

By Category (Bags (Cross Body Bags, Bags and Backpacks, Business Bags, Duffle Bags, Clutches, Others), Luggage (Soft Luggage, Hard Luggage, Wheeled Luggage, Non-Wheeled Luggage)), By Sales Channel (Retail Offline, Retail Online), By Material Type (Soft Case (Nylon, Polyester, Ballistic Nylon), Hard Case (Polycarbonate, ABS (Acrylonitrile Butadiene Styrene), Polypropylene)), By Price Category (Luxury, Mass/Economy, Premium), By Application (Travel, Business) ... Read more

|

Major Players

|

Canada Bags and Luggage Market Statistics and Insights, 2026

- Market Size Statistics

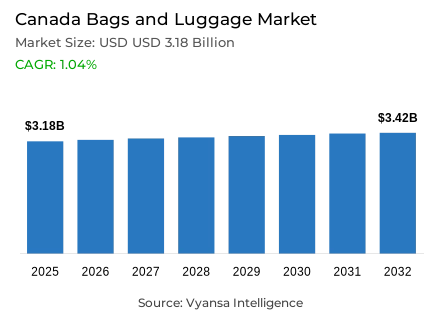

- Bags and luggage in Canada is estimated at USD 3.18 billion in 2025.

- The market size is expected to grow to USD 3.42 billion by 2032.

- Market to register a cagr of around 1.04% during 2026-32.

- Category Shares

- Bags grabbed market share of 90%.

- Competition

- More than 20 companies are actively engaged in producing bags and luggage in Canada.

- Top 5 companies acquired around 25% of the market share.

- Samsonite Canada Inc; Saint Laurent Canada Boutiques Inc; G Boutiques Inc; Michael Kors Canada Holdings Ltd; Louis Vuitton Canada Inc etc., are few of the top companies.

- Sales Channel

- Retail offline grabbed 85% of the market.

Canada Bags and Luggage Market Outlook

Canada bags and luggage market will experience a predicted moderate but consistent growth in the period of 2026-32 due to the continued travelling demand, high quality handbag sales, and the expansion of omnichannel offerings. In Canada, bags and luggage are estimated around USD 3.18 billion in 2025 and are expected to be USD 3.42 billion in 2032 with a CAGR of about 1.04% per annum in the forecast period. Despite the fact that the discretionary spending is still subject to inflation and increased cost of living, travel still remains a major priority to most Canadas, hence maintaining the need of luggage and other travel related accessories.

Bags remain a dominant product in the market due to their daily usage and style. Luxury handbags, especially, will be rather resilient, as they will be backed by wealthy end users, the premium prices of leading luxury brands, and the high resale value of high-end products. Although mid-market brands will need to deal with value-based and luxury competitors, value brands with trendy designs and affordable prices will work out. The rise in population through immigration is not expected to contribute substantially to the overall increase in values, with a large number of the new workers to the labor market still being price-sensitive.

The demand of luggage will also not decrease, as there is still interest in domestic and international tourism. Carry-on luggage will probably not be going away soon based on the airline baggage charges and the desire by end users to be convenient. Sustainability will become even more popular, and brands will increase the number of recycled materials, cruelty-free products, and circular projects to respond to the increasing consumer awareness of environmental and ethical issues.

Regarding the channels, retail offline is still predominant with approximately 85% share, and facilitated by bag and luggage experts and department stores with which end users can evaluate quality and brand experience physically. Nonetheless, retail online is going to remain an increasingly relevant research, comparison and convenience channel. In general, the market perspective is that of steady growth, which is influenced by the recovery of travel, polarisation of luxury and value brands, and a robust omnichannel orientation.

Canada Bags and Luggage Market Growth Driver

Rising Travel Activity Supporting Mobility-Related Expenditure

The sustained expansion of travel activity across Canada continues to support underlying demand for baggage and travel accessories within the country. Statistica Canada reports that in 2024, Canadian residents made 330.8 million trips, including 292.1 million domestic trips and 38.7 million international trips, which represent a 3.7% increase over 2023 and indicate ongoing consumer mobility and interest in leisure travel.

Meanwhile, international travel is a major factor that contributes to the demand of luggage and luxurious bags. In 2023, 27.2 million trips to Canada were made by non-Canadian visitors, with the main source countries being the United States, United Kingdom, France, Mexico, and India. Canadians spent US 73.5 billion on domestic tourism, thus showing the scale of travel-related spending that forms the basis of accessory purchases.

Canada Bags and Luggage Market Challenge

Household Spending Polarisation Under Inflation

The challenge that becomes salient in the Canada market is due to differentiated consumer spending patterns as a result of the inflationary pressures. Statistics show that inflation is one of the major concerns of the households and cost pressures cut across a wide range of goods and services. An example is that in December 2023 the Consumer Price Index rose by around 3.4% year-on-year, indicating further upward pressure on general prices and household budgets.

These inflationary issues make end users focus on significant and value-focused purchases, whereas luxury and discretionary segments might be considered only by more affluent groups. As a result, the mid-market bag and luggage brands feel pressure because low-end customers are looking for lower prices or are delaying discretionary spending which is dividing the demand in the category.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Canada Bags and Luggage Market Trend

Increasing popularity of Carry-on and lightweight luggage

Evolving travel patterns across Canada are reshaping end user preferences, with increasing emphasis on lightweight designs and carry-on luggage formats. Since millions of domestic and outbound journeys are made each year, travellers are adopting smaller luggage because it is convenient and easily carried. Canada residents made 90.6 million journeys in the second quarter of the year 2025 that comprised of a domestic visit, an increase of about 10.9% compared to the year before, showing strong mobility trends that support luggage demand, especially compact and easy-to-carry formats.

This consumer behavior conforms to airline fares, congestion at transit terminals, and carry-on baggage is the priority of the traveller to avoid checked-bag charges and delays. In line with this, manufacturers and retailers are customising product portfolios to lightweight, manoeuvrable luggage solutions that meet the needs of convenience and efficiency, and, as such, maintain category relevance.

Canada Bags and Luggage Market Opportunity

Sizing Brand-Managed Direct-to-Consumer and Omnichannel Plans

Brand operating in the Canada bags and luggage market are well positioned to strengthen future growth by expanding direct to end-user engagement and advancing integrated omnichannel strategies. The increased ability to control digital storefronts allows brands to define pricing, narrative, and product display and react quickly to changing end-user preferences. This would be especially relevant in segments like luggage and handbags, where brands are very important in determining the decision to purchase an item, design and durability are very important. Physical stores still have a significant role in demonstrating materials, fit and functionality, which builds trust and helps justify more high value purchasing.

At the same time, the further incorporation of the online and offline channels makes the experience more convenient and interactive. Online shopping experience is enhanced by services like click and collect, in-store returns on the online purchases, and customised digital assistance. Through decreasing dependency on wholesale collaborators and enhancing the value of the initial party association, brands would be able to attain affections, gain greater insight into margins, and react more to the value-conscious as well as high-end end end users in Canada.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Canada Bags and Luggage Market Segmentation Analysis

By Category

- Bags

- Cross Body Bags

- Bags and Backpacks

- Business Bags

- Duffle Bags

- Clutches

- Others

- Luggage

- Soft Luggage

- Hard Luggage

- Wheeled Luggage

- Non-Wheeled Luggage

Bags represent the largest segment of the Canada bags and luggage market with a market share of about 90% of the total market share. This hegemony indicates the daily applicability of bags in work, leisure and social events as opposed to luggage which is more closely associated with frequency of travel. The demand in handbags, backpacks, and shoulder bags remains steady because of their practical functionality and popularity.

The luxury handbags are significant in this segment, aided by wealthy customers, good brand equity and good resale value. Meanwhile, the value-based bags will stay in demand with the cost-effective end users who want to find the fashionable designs at a reasonable price. The bags segment is predicted to maintain its market leadership over the forecast period due to the lifestyle usage, the top-end premiumisation, and ongoing design and material innovation.

By Sales Channel

- Retail Offline

- Retail Online

The category with the largest market share in the sales channel type is retail offline, which currently holds a market share of approximately 85% for bags and luggage in Canada. Offline stores continue to play an important role, especially in the case of handbags and luggage, as customers want to see, touch, and evaluate the quality of the product before making a purchase. Specialists in bags and luggage offer extensive ranges and effective brand storytelling, while department stores help to support the premium positioning of brands.

Although retail e-commerce is gradually increasing its presence in the market due to convenience, price comparisons, and improved payment and delivery services, it has not yet challenged the offline market. Instead, brands are now focusing on omnichannel retailing, which combines online and offline retailing.

List of Companies Covered in Canada Bags and Luggage Market

The companies listed below are highly influential in the Canada bags and luggage market, with a significant market share and a strong impact on industry developments.

- Samsonite Canada Inc

- Saint Laurent Canada Boutiques Inc

- G Boutiques Inc

- Michael Kors Canada Holdings Ltd

- Louis Vuitton Canada Inc

- Kate Spade & Co Inc

- Coach Stores Canada Corp

- Hermès Canada Inc

- Guess Canada Corp

- Herschel Supply Co Ltd

Competitive Landscape

Canada bags and luggage market is characterised by strong competition between established global brands, premium luxury players, and emerging direct-to-consumer specialists. Michael Kors retained overall leadership with a 10% retail value share, although it faced pressure in handbags from competitors such as Coach, which benefited from the popularity of styles like the Tabby bag. In luggage, Samsonite Canada remained the clear leader, supported by strong brand equity, marketing campaigns, and a focus on durable and sustainable products. Specialist brands such as Monos strengthened their positions through omnichannel and direct-to-consumer strategies, while international luxury brands including Hermès, Chanel, and Louis Vuitton continued to drive growth at the premium end. Overall, competition is increasingly shaped by brand positioning, travel-led demand, and omnichannel execution.

Frequently Asked Questions

Related Report

1. Market Segmentation

1.1. Research Scope

1.2. Research Methodology

1.3. Definitions and Assumptions

2. Executive Summary

3. Canada Bags and Luggage Market Policies, Regulations, and Standards

4. Canada Bags and Luggage Market Dynamics

4.1. Growth Factors

4.2. Challenges

4.3. Trends

4.4. Opportunities

5. Canada Bags and Luggage Market Statistics, 2022-2032F

5.1. Market Size & Growth Outlook

5.1.1.By Revenues in USD Million

5.1.2.By Units Sold in Thousand Units

5.2. Market Segmentation & Growth Outlook

5.2.1.By Category

5.2.1.1. Bags- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.1. Cross Body Bags- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.2. Bags and Backpacks- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.3. Business Bags- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.4. Duffle Bags- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.5. Clutches- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.6. Others- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2. Luggage- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2.1. Soft Luggage- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2.2. Hard Luggage- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2.3. Wheeled Luggage- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2.4. Non-Wheeled Luggage- Market Insights and Forecast 2022-2032, USD Million

5.2.2.By Sales Channel

5.2.2.1. Retail Offline- Market Insights and Forecast 2022-2032, USD Million

5.2.2.2. Retail Online- Market Insights and Forecast 2022-2032, USD Million

5.2.3.By Material Type

5.2.3.1. Soft Case- Market Insights and Forecast 2022-2032, USD Million

5.2.3.1.1. Nylon- Market Insights and Forecast 2022-2032, USD Million

5.2.3.1.2. Polyester- Market Insights and Forecast 2022-2032, USD Million

5.2.3.1.3. Ballistic Nylon- Market Insights and Forecast 2022-2032, USD Million

5.2.3.2. Hard Case- Market Insights and Forecast 2022-2032, USD Million

5.2.3.2.1. Polycarbonate- Market Insights and Forecast 2022-2032, USD Million

5.2.3.2.2. ABS (Acrylonitrile Butadiene Styrene)- Market Insights and Forecast 2022-2032, USD Million

5.2.3.2.3. Polypropylene- Market Insights and Forecast 2022-2032, USD Million

5.2.4.By Price Category

5.2.4.1. Luxury- Market Insights and Forecast 2022-2032, USD Million

5.2.4.2. Mass/Economy- Market Insights and Forecast 2022-2032, USD Million

5.2.4.3. Premium- Market Insights and Forecast 2022-2032, USD Million

5.2.5.By Application

5.2.5.1. Travel- Market Insights and Forecast 2022-2032, USD Million

5.2.5.2. Business- Market Insights and Forecast 2022-2032, USD Million

5.2.6.By Competitors

5.2.6.1. Competition Characteristics

5.2.6.2. Market Share & Analysis

6. Canada Bags Market Statistics, 2022-2032

6.1. Market Size & Growth Outlook

6.1.1.By Revenues in USD Million

6.1.2.By Units Sold in Thousand Units

6.2. Market Segmentation & Growth Outlook

6.2.1.By Category- Market Insights and Forecast 2022-2032, USD Million

6.2.2.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

6.2.3.By Material Type- Market Insights and Forecast 2022-2032, USD Million

6.2.4.By Price Category- Market Insights and Forecast 2022-2032, USD Million

6.2.5.By Application- Market Insights and Forecast 2022-2032, USD Million

7. Canada Luggage Market Statistics, 2022-2032

7.1. Market Size & Growth Outlook

7.1.1.By Revenues in USD Million

7.1.2.By Units Sold in Thousand Units

7.2. Market Segmentation & Growth Outlook

7.2.1.By Category- Market Insights and Forecast 2022-2032, USD Million

7.2.2.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

7.2.3.By Material Type- Market Insights and Forecast 2022-2032, USD Million

7.2.4.By Price Category- Market Insights and Forecast 2022-2032, USD Million

7.2.5.By Application- Market Insights and Forecast 2022-2032, USD Million

8. Competitive Outlook

8.1. Company Profiles

8.1.1.Michael Kors Canada Holdings Ltd

8.1.1.1. Business Description

8.1.1.2. Product Portfolio

8.1.1.3. Collaborations & Alliances

8.1.1.4. Recent Developments

8.1.1.5. Financial Details

8.1.1.6. Others

8.1.2.Louis Vuitton Canada Inc

8.1.2.1. Business Description

8.1.2.2. Product Portfolio

8.1.2.3. Collaborations & Alliances

8.1.2.4. Recent Developments

8.1.2.5. Financial Details

8.1.2.6. Others

8.1.3.Kate Spade & Co Inc

8.1.3.1. Business Description

8.1.3.2. Product Portfolio

8.1.3.3. Collaborations & Alliances

8.1.3.4. Recent Developments

8.1.3.5. Financial Details

8.1.3.6. Others

8.1.4.Coach Stores Canada Corp

8.1.4.1. Business Description

8.1.4.2. Product Portfolio

8.1.4.3. Collaborations & Alliances

8.1.4.4. Recent Developments

8.1.4.5. Financial Details

8.1.4.6. Others

8.1.5.Hermès Canada Inc

8.1.5.1. Business Description

8.1.5.2. Product Portfolio

8.1.5.3. Collaborations & Alliances

8.1.5.4. Recent Developments

8.1.5.5. Financial Details

8.1.5.6. Others

8.1.6.Samsonite Canada Inc

8.1.6.1. Business Description

8.1.6.2. Product Portfolio

8.1.6.3. Collaborations & Alliances

8.1.6.4. Recent Developments

8.1.6.5. Financial Details

8.1.6.6. Others

8.1.7.Saint Laurent Canada Boutiques Inc

8.1.7.1. Business Description

8.1.7.2. Product Portfolio

8.1.7.3. Collaborations & Alliances

8.1.7.4. Recent Developments

8.1.7.5. Financial Details

8.1.7.6. Others

8.1.8.G Boutiques Inc

8.1.8.1. Business Description

8.1.8.2. Product Portfolio

8.1.8.3. Collaborations & Alliances

8.1.8.4. Recent Developments

8.1.8.5. Financial Details

8.1.8.6. Others

8.1.9.Guess Canada Corp

8.1.9.1. Business Description

8.1.9.2. Product Portfolio

8.1.9.3. Collaborations & Alliances

8.1.9.4. Recent Developments

8.1.9.5. Financial Details

8.1.9.6. Others

8.1.10. Herschel Supply Co Ltd

8.1.10.1. Business Description

8.1.10.2. Product Portfolio

8.1.10.3. Collaborations & Alliances

8.1.10.4. Recent Developments

8.1.10.5. Financial Details

8.1.10.6. Others

9. Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Category |

|

| By Sales Channel |

|

| By Material Type |

|

| By Price Category |

|

| By Application |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.