Brazil Juice Market Report: Trends, Growth and Forecast (2026-2032)

By Category (100% Juice (Not from Concentrate, Reconstituted), Juice Drinks (up to 24% Juice), Nectars (High Concentration (40% to 50% fruit content), Medium Concentration (30% to 39% fruit content), Low Concentration (25% to 29% fruit content)), Vegetable Juice, Fruit and Vegetable Blends), By Nature (Conventional, Organic), By Packaging Material (Plastic, Glass, Metal, Others), By Packaging Type (PET Bottles, Aseptic Packages (Cartons), Glass Bottles, Metal Cans, Disposable Cups & Pouches), By Sales Channel (Off-Trade (Hypermarkets/ Supermarkets, Retail Outlets, Convenience Stores, Online Platforms), On-Trade), By Region (North, Center-West, Northeast, Southeast, South) ... Read more

|

Major Players

|

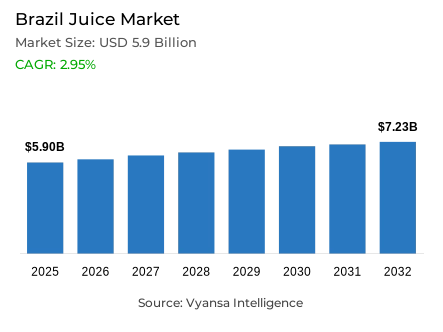

Brazil Juice Market Statistics and Insights, 2026

- Market Size Statistics

- Juice market size in Brazil was estimated at USD 5.9 billion in 2025.

- The market size is expected to grow to USD 7.23 billion by 2032.

- Market to register a CAGR of around 2.95% during 2026-32.

- Category Shares

- Juice drinks (up to 24% juice) grabbed market share of 30%.

- Competition

- More than 20 companies are actively engaged in producing juice in Brazil.

- Top 5 companies acquired around 40% of the market share.

- Amacoco Água de Côco da Amazônia Ltda, Wow Indústria e Comércio Ltda, Ducoco Alimentos SA, Sucos Del Valle do Brasil Ltda, Natural One SA etc., are few of the top companies.

- Sales Channel

- Off-trade grabbed 80% of the market.

Brazil Juice Market Outlook

Brazil juice market stands at a critical juncture, poised to demonstrate notable resilience and strategic adaptation through 2032. Despite confronting substantial supply chain disruptions—including climate-induced droughts and the persistent threat of greening disease—the market is projected to expand from an estimated valuation of USD 5.9 billion in 2025 to USD 7.23 billion by 2032, reflecting a compound annual growth rate of approximately 2.95% during the 2026-32 forecast period. This trajectory underscores the industry's capacity to navigate adversity within a sector historically anchored by orange juice production, as stakeholders implement structural adjustments to address record-low inventory levels and unprecedented price volatility.

In response to volatile citrus prices, manufacturers are aggressively diversifying into local fruit and vegetable blends. High-quality grape juice, particularly from southern production hubs, is gaining prominence as a reliable alternative. This diversification is further accelerated by a growing wellness trend among younger end users who are seeking functional nutrients and immune-boosting benefits. Additionally, upcoming tax reforms are expected to benefit the 100% juice segment, potentially slowing price increases and driving stronger volume growth in the latter half of the forecast period.

Innovation is increasingly focused on technical solutions for sugar reduction. Since juice sweetness is naturally derived, brands are investing in research to maintain flavor while lowering sugar content through innovative fruit-vegetable mixes. This shift aligns with Brazil’s new food labeling standards, which guide shoppers toward healthier options. Furthermore, the rise of ready-to-drink and convenient single-serve formats highlights a push toward meeting the needs of busy urban professionals and students.

The retail landscape remains heavily concentrated in physical stores, where Off-Trade channels grab 80% of the market. Supermarkets and hypermarkets account for nearly two-thirds of all sales, though discounters and warehouse clubs are gaining traction among price-sensitive families. While e-commerce remains a marginal channel for daily grocery staples, the market’s long-term stability is anchored by major players like Del Valle and Natural One, who continue to invest in sustainable distribution and alternative ingredients to maintain their market leadership.

Brazil Juice Market Growth Driver

Affordable Packs and Clear Labels Support Everyday Buying

The price pressure keeps juice in the basket by guiding shoppers to value-for-money products like juice drinks and nectars, but still uses the vast citrus base in Brazil to provide familiar taste. As per the statistics provided by the Brazilian Institute of Geography and Statistics (IBGE), the area of orange-growing in Brazil was 558,785 hectares in 2023, which contributes to a wide range of juice-based drinks sold in both traditional and modern retail outlets. Better for you positioning is also demanded by health and ingredient awareness.

In 2022, the Pan American Health Organization reports an overweight and obesity rate of 63.0% of people aged 15 years and above, and end users remain sensitive to sugar and nutrition messages on packaging. The new nutrition-labelling regulation RDC 429/2020, which came into force 24 months after its publication, simplifies the comparison of labels and strengthens the shift to fruit-based products with transparent labels.

Brazil Juice Market Challenge

Orange Supply Shocks Keep Costs Volatile

Orange juice is still subject to climatic stress and orchard disease, which spread across the broader juice aisle. Fundecitrus statistics provided by USDA indicate that in 2024, greening will be at an incidence of 44.35 % in the citrus belt, impacting about 90.36 million trees, thus lowering the yield and quality of juice and constraining the availability of raw-material. Restricted supply soon becomes price surges and brand and retailer pressure.

In May 2024, orange juice concentrate futures hit a record of 4.95 per pound, a demonstration of how quickly costs can be shifting when crops fail. Audited world stocks of Brazilian orange juice (FCOJ equivalent) were 116,710 metric tons on 30 June 2024, the third-lowest on record, constraining blending options and maintaining pack prices volatile.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Brazil Juice Market Trend

Blends and Smaller Packs Redefine the Shelf

Juice producers are inclined to mixing and dilution to control orange shortages and make everyday entry prices affordable. According to USDA, businesses mix orange with mango or passionfruit, water to make nectar, and even reduce the size of bottles by 1/3 to 700ml, a typical example of shrinkflation. Sourcing shifts also increase supply flexibility. Between July and November 2024, Brazil imported 16,434 MT of fresh oranges, which is 63 % higher than the same period the previous year, and assists processors in filling gaps when local fruit is unavailable.

Meanwhile, IFU data quoted by USDA indicate that the consumption of orange juice in Europe declined by 1520 % in 2023, and brands are now having to protect volume with mixed flavours and nectar-like propositions.

Brazil Juice Market Opportunity

Investment Outside the Citrus Belt Opens New Growth Paths

The supply risk is pushing upstream investment and new sourcing geographies, which are leaving more space to the juice pipelines. USDA documents a BRL 500 million (USD 83 million) initiative in Mato Grosso do Sul to plant irrigated orange trees and potentially construct a juice-processing plant an instance of capacity shifting outside the conventional citrus belt. Innovation beyond pure orange is also supported by export economics.

Orange juice exports amounted to USD 850.4 million in July-September 2024, which is 43.23% higher than the same period last year, which means that end users are willing to pay to have a stable supply. In reaction, Brazil is also interested in exporting other orange products like orange pulp to the Asian markets, thus creating space to the blended juices and value added formats based on the availability of local fruits.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Brazil Juice Market Segmentation Analysis

By Category

- 100% Juice

- Not from Concentrate

- Reconstituted

- Juice Drinks (up to 24% Juice)

- Nectars

- High Concentration (40% to 50% fruit content)

- Medium Concentration (30% to 39% fruit content)

- Low Concentration (25% to 29% fruit content)

- Vegetable Juice

- Fruit and Vegetable Blends

The segment has the highest share around the category for the Brazilian market, where Juice Drinks (up to 24% Juice) grabbed a market share of 30%. This significant market share is primarily driven by the extreme price sensitivity of the local population. As orange juice production faced climate and agricultural setbacks, end users increasingly favored these more affordable options. Juice drinks and nectars provide a cost-effective way for households to maintain juice consumption without the high price tags associated with premium 100% varieties.

Beyond affordability, this segment thrives on Brazil’s immense biodiversity. Manufacturers are successfully incorporating a wide variety of local flavors and tropical blends to keep the category vibrant. While health-conscious segments like coconut water are growing rapidly, juice drinks remain the backbone of the market due to their extensive distribution and strong appeal to families and younger end users seeking flavorful, low-cost hydration.

By Sales Channel

- Off-Trade

- Hypermarkets/ Supermarkets

- Retail Outlets

- Convenience Stores

- Online Platforms

- On-Trade

The segment has the highest share around the Sales Channel is Off-Trade, which grabbed 80% of the market. This dominance reflects the central role of juice as a staple of the Brazilian family diet, typically purchased during weekly supermarket trips. Large modern grocery formats, including supermarkets and hypermarkets, remain the primary destinations for these shoppers, though the recent surge in unit prices has pushed many price-driven end users toward discounters and warehouse clubs to find better value.

While digital platforms are reshaping other sectors, retail e-commerce remains a minor channel for juice in Brazil. end users still prefer the immediate availability and physical browsing experience of traditional retail for their household staples. Consequently, the market continues to prioritize brick-and-mortar partnerships and prominent shelf placement in supermarkets to ensure that both established brands and innovative new blends reach the widest possible audience through 2032.

List of Companies Covered in Brazil Juice Market

The companies listed below are highly influential in the Brazil juice market, with a significant market share and a strong impact on industry developments.

- Amacoco Água de Côco da Amazônia Ltda

- Wow Indústria e Comércio Ltda

- Ducoco Alimentos SA

- Sucos Del Valle do Brasil Ltda

- Natural One SA

- Tampico Beverages Inc

- C L Pratinha-Eireli-ME

- Empresa Brasileira de Bebidas e Alimentos SA

- Sococo SA Indústrias Alimentícias

- Heineken do Brasil Comercial Ltda

Competitive Landscape

Brazil juice market remains highly concentrated, with established brands leveraging scale and distribution strength to navigate ongoing raw material and pricing volatility. Del Valle, backed by The Coca-Cola Co, continues to lead off-trade volume sales through its strong brand equity and presence across 100% juice, juice drinks and nectars, ensuring visibility even as orange juice constraints weigh on the category. Tampico, under Tampico Beverages, sustains its position through low pricing and child-friendly appeal, resonating with highly price-sensitive households. Meanwhile, Natural One is strengthening its competitive stance by investing heavily in supply chain capacity and diversifying beyond orange-based products, notably through fruit-and-vegetable blends. This strategic pivot toward alternative ingredients reflects a broader competitive shift, as players seek resilience against structural challenges in orange juice supply.

Frequently Asked Questions

Related Report

1. Market Segmentation

1.1. Research Scope

1.2. Research Methodology

1.3. Definitions and Assumptions

2. Executive Summary

3. Brazil Juice Market Policies, Regulations, and Standards

4. Brazil Juice Market Dynamics

4.1. Growth Factors

4.2. Challenges

4.3. Trends

4.4. Opportunities

5. Brazil Juice Market Statistics, 2022-2032F

5.1. Market Size & Growth Outlook

5.1.1.By Revenues in USD Million

5.1.2.By Quantity Sold in Million Litres

5.2. Market Segmentation & Growth Outlook

5.2.1.By Category

5.2.1.1. 100% Juice- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.1. Not from Concentrate- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.2. Reconstituted- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2. Juice Drinks (up to 24% Juice)- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3. Nectars- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3.1. High Concentration (40% to 50% fruit content)- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3.2. Medium Concentration (30% to 39% fruit content)- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3.3. Low Concentration (25% to 29% fruit content)- Market Insights and Forecast 2022-2032, USD Million

5.2.1.4. Vegetable Juice- Market Insights and Forecast 2022-2032, USD Million

5.2.1.5. Fruit and Vegetable Blends- Market Insights and Forecast 2022-2032, USD Million

5.2.2.By Nature

5.2.2.1. Conventional- Market Insights and Forecast 2022-2032, USD Million

5.2.2.2. Organic- Market Insights and Forecast 2022-2032, USD Million

5.2.3.By Packaging Material

5.2.3.1. Plastic- Market Insights and Forecast 2022-2032, USD Million

5.2.3.2. Glass- Market Insights and Forecast 2022-2032, USD Million

5.2.3.3. Metal- Market Insights and Forecast 2022-2032, USD Million

5.2.3.4. Others- Market Insights and Forecast 2022-2032, USD Million

5.2.4.By Packaging Type

5.2.4.1. PET Bottles- Market Insights and Forecast 2022-2032, USD Million

5.2.4.2. Aseptic Packages (Cartons)- Market Insights and Forecast 2022-2032, USD Million

5.2.4.3. Glass Bottles- Market Insights and Forecast 2022-2032, USD Million

5.2.4.4. Metal Cans- Market Insights and Forecast 2022-2032, USD Million

5.2.4.5. Disposable Cups & Pouches- Market Insights and Forecast 2022-2032, USD Million

5.2.5.By Sales Channel

5.2.5.1. Off-Trade- Market Insights and Forecast 2022-2032, USD Million

5.2.5.1.1. Hypermarkets/ Supermarkets - Market Insights and Forecast 2022-2032, USD Million

5.2.5.1.2. Retail Outlets - Market Insights and Forecast 2022-2032, USD Million

5.2.5.1.3. Convenience Stores- Market Insights and Forecast 2022-2032, USD Million

5.2.5.1.4. Online Platforms- Market Insights and Forecast 2022-2032, USD Million

5.2.5.2. On-Trade- Market Insights and Forecast 2022-2032, USD Million

5.2.6.By Region

5.2.6.1. North

5.2.6.2. Center-West

5.2.6.3. Northeast

5.2.6.4. Southeast

5.2.6.5. South

5.2.7.By Competitors

5.2.7.1. Competition Characteristics

5.2.7.2. Market Share & Analysis

6. Brazil 100% Juice Market Statistics, 2022-2032

6.1. Market Size & Growth Outlook

6.1.1.By Revenues in USD Million

6.1.2.By Quantity Sold in Million Litres

6.2. Market Segmentation & Growth Outlook

6.2.1.By Nature- Market Insights and Forecast 2022-2032, USD Million

6.2.2.By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

6.2.3.By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

6.2.4.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

6.2.5.By Region- Market Insights and Forecast 2022-2032, USD Million

7. Brazil Juice Drinks (up to 24% Juice) Market Statistics, 2022-2032

7.1. Market Size & Growth Outlook

7.1.1.By Revenues in USD Million

7.1.2.By Quantity Sold in Million Litres

7.2. Market Segmentation & Growth Outlook

7.2.1.By Nature- Market Insights and Forecast 2022-2032, USD Million

7.2.2.By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

7.2.3.By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

7.2.4.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

7.2.5.By Region- Market Insights and Forecast 2022-2032, USD Million

8. Brazil Nectars Market Statistics, 2022-2032

8.1. Market Size & Growth Outlook

8.1.1.By Revenues in USD Million

8.1.2.By Quantity Sold in Million Litres

8.2. Market Segmentation & Growth Outlook

8.2.1.By Nature- Market Insights and Forecast 2022-2032, USD Million

8.2.2.By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

8.2.3.By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

8.2.4.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

8.2.5.By Region- Market Insights and Forecast 2022-2032, USD Million

9. Brazil Vegetable Juice Market Statistics, 2022-2032

9.1. Market Size & Growth Outlook

9.1.1.By Revenues in USD Million

9.1.2.By Quantity Sold in Million Litres

9.2. Market Segmentation & Growth Outlook

9.2.1.By Nature- Market Insights and Forecast 2022-2032, USD Million

9.2.2.By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

9.2.3.By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

9.2.4.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

9.2.5.By Region- Market Insights and Forecast 2022-2032, USD Million

10. Brazil Fruit and Vegetable Blends Market Statistics, 2022-2032

10.1. Market Size & Growth Outlook

10.1.1. By Revenues in USD Million

10.1.2. By Quantity Sold in Million Litres

10.2. Market Segmentation & Growth Outlook

10.2.1. By Nature- Market Insights and Forecast 2022-2032, USD Million

10.2.2. By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

10.2.3. By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

10.2.4. By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

10.2.5. By Region- Market Insights and Forecast 2022-2032, USD Million

11. Competitive Outlook

11.1. Company Profiles

11.1.1. Sucos Del Valle do Brasil Ltda

11.1.1.1. Business Description

11.1.1.2. Product Portfolio

11.1.1.3. Collaborations & Alliances

11.1.1.4. Recent Developments

11.1.1.5. Financial Details

11.1.1.6. Others

11.1.2. Natural One SA

11.1.2.1. Business Description

11.1.2.2. Product Portfolio

11.1.2.3. Collaborations & Alliances

11.1.2.4. Recent Developments

11.1.2.5. Financial Details

11.1.2.6. Others

11.1.3. Tampico Beverages Inc

11.1.3.1. Business Description

11.1.3.2. Product Portfolio

11.1.3.3. Collaborations & Alliances

11.1.3.4. Recent Developments

11.1.3.5. Financial Details

11.1.3.6. Others

11.1.4. C L Pratinha-Eireli-ME

11.1.4.1. Business Description

11.1.4.2. Product Portfolio

11.1.4.3. Collaborations & Alliances

11.1.4.4. Recent Developments

11.1.4.5. Financial Details

11.1.4.6. Others

11.1.5. Empresa Brasileira de Bebidas e Alimentos SA

11.1.5.1. Business Description

11.1.5.2. Product Portfolio

11.1.5.3. Collaborations & Alliances

11.1.5.4. Recent Developments

11.1.5.5. Financial Details

11.1.5.6. Others

11.1.6. Amacoco Água de Côco da Amazônia Ltda

11.1.6.1. Business Description

11.1.6.2. Product Portfolio

11.1.6.3. Collaborations & Alliances

11.1.6.4. Recent Developments

11.1.6.5. Financial Details

11.1.6.6. Others

11.1.7. Wow Indústria e Comércio Ltda

11.1.7.1. Business Description

11.1.7.2. Product Portfolio

11.1.7.3. Collaborations & Alliances

11.1.7.4. Recent Developments

11.1.7.5. Financial Details

11.1.7.6. Others

11.1.8. Ducoco Alimentos SA

11.1.8.1. Business Description

11.1.8.2. Product Portfolio

11.1.8.3. Collaborations & Alliances

11.1.8.4. Recent Developments

11.1.8.5. Financial Details

11.1.8.6. Others

11.1.9. Sococo SA Indústrias Alimentícias

11.1.9.1. Business Description

11.1.9.2. Product Portfolio

11.1.9.3. Collaborations & Alliances

11.1.9.4. Recent Developments

11.1.9.5. Financial Details

11.1.9.6. Others

11.1.10. Heineken do Brasil Comercial Ltda

11.1.10.1.Business Description

11.1.10.2.Product Portfolio

11.1.10.3.Collaborations & Alliances

11.1.10.4.Recent Developments

11.1.10.5.Financial Details

11.1.10.6.Others

12. Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Category |

|

| By Nature |

|

| By Packaging Material |

|

| By Packaging Type |

|

| By Sales Channel |

|

| By Region |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.