Bolivia Juice Market Report: Trends, Growth and Forecast (2026-2032)

By Category (100% Juice (Not from Concentrate, Reconstituted), Juice Drinks (up to 24% Juice), Nectars (High Concentration (40% to 50% fruit content), Medium Concentration (30% to 39% fruit content), Low Concentration (25% to 29% fruit content)), Vegetable Juice, Fruit and Vegetable Blends), By Nature (Conventional, Organic), By Packaging Material (Plastic, Glass, Metal, Others), By Packaging Type (PET Bottles, Aseptic Packages (Cartons), Glass Bottles, Metal Cans, Disposable Cups & Pouches), By Sales Channel (Off-Trade (Hypermarkets/ Supermarkets, Retail Outlets, Convenience Stores, Online Platforms), On-Trade) ... Read more

|

Major Players

|

Bolivia Juice Market Statistics and Insights, 2026

- Market Size Statistics

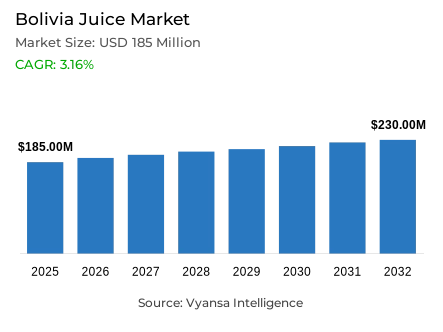

- Juice market size in Bolivia was estimated at USD 185 million in 2025.

- The market size is expected to grow to USD 230 million by 2032.

- Market to register a CAGR of around 3.16% during 2026-32.

- Category Shares

- Juice drinks (up to 24% juice) grabbed market share of 80%.

- Competition

- More than 5 companies are actively engaged in producing juice in Bolivia.

- Top 5 companies acquired around 85% of the market share.

- Industrias Venado SA, Agrov SRL, DICOM Distribuidores del Oriente SRL, Cía de Alimentos Ltda Delizia, Pil Andina SA etc., are few of the top companies.

- Sales Channel

- Off-trade grabbed 90% of the market.

Bolivia Juice Market Outlook

The Bolivian juice market is experiencing steady and stable growth, supported by a strong cultural preference for fruit-based beverages. Juice remains a daily consumption item despite inflationary pressures, as it is perceived as natural and readily accessible. The market is valued at USD 185 million in 2025 and is projected to reach USD 230 million by 2032, registering a CAGR of approximately 3.16% during the forecast period.

Growth is sustained by a multi-tier packaging strategy balancing value and convenience. Large 2–5 L PET bottles are increasingly popular among families seeking affordability, while 150–300 ml packs cater to students and urban workers. Juice drinks (up to 24% juice) dominate with an 80% market share, reflecting strong demand for refreshing citrus and tropical flavours suited to Bolivia’s warm climate.

Innovation focuses on local identity and wellness trends. Brands are investing in traditional flavours such as tamarind and achachairu, alongside culturally resonant beverages like mocochinchi. Health-oriented fruit-and-vegetable blends are also gaining traction. Producers such as Delizia and Industria Venado are leading this shift by combining international quality standards with affordable pricing and versatile packaging, including sachets and specialised PET formats.

Off-trade channels account for 90% of sales, anchored in home consumption. While traditional grocers remain critical for rural and peri-urban reach, supermarkets are the fastest-growing channel, offering better platforms for wellness-oriented products and seasonal promotions. Together, local flavours and flexible packaging position the Bolivian juice market for steady growth through 2032.

Bolivia Juice Market Growth Driver

Value Packs and Local Flavours Keep Juice in Daily Baskets

High prices keep shoppers value-conscious, prompting brands to rely on multi-pack strategies such as large family packs for home consumption and small single-serve packs for affordable refreshment. Frequent top-up shopping at neighbourhood stores sustains demand for these formats. Bolivia’s CPI shows a cumulative increase of 20.40% by December 2025, keeping households focused on price-per-litre value and encouraging brands to protect entry-level pricing.

Juice also benefits from flavour variety. Nectars combine familiar fruits with local varieties, while pack claims highlighting real fruit content and natural cues help build trust. Strong shelf visibility and seasonal promotions in modern retail encourage trial and repeat purchases. This combination of value and local taste keeps juice firmly embedded in regular household baskets.

Bolivia Juice Market Challenge

Inflation and Weak Demand Pressure Affordability

Rising living costs make juice purchases more price-sensitive and less predictable across retail channels. Bolivia’s CPI is projected to reach 20.40% cumulative inflation by December 2025, while the economy recorded a cumulative decline of 1.63% between January and September 2025. These pressures strain household budgets and weigh on manufacturers dependent on packaging, sugar, and transport inputs.

Supply-side costs further complicate pricing decisions. Volatility in fuel, freight, and imported materials forces brands to choose between price increases, pack-size reductions, or reduced promotions. Seasonal availability of local fruits adds another challenge, as short harvest cycles can disrupt continuous production and make flavour consistency harder to maintain throughout the year.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Bolivia Juice Market Trend

Wellness Claims and Cleaner Labels Gain Shelf Space

Health and wellness positioning is gaining visibility on juice shelves, particularly in urban areas. In Bolivia, more than 65.1% of the population aged 15 and above was overweight or obese in 2022, prompting greater attention to sugar levels, calorie content, and natural cues in beverage choices. In response, brands are introducing fruitandvegetable blends and functional claims such as energy or detox, while maintaining affordability and taste appeal.

These shifts are reflected in packaging and communication strategies. Clear labelling of fruit content, vitamin inclusion, and use of local ingredients enhances transparency. Smaller readytodrink formats suit portion control and onthego consumption for students and workers, while childfriendly cartons remain prominent during schoolseason promotions.

Bolivia Juice Market Opportunity

Native Fruit Processing Unlocks Differentiated Nectars

Local fruit innovation presents a clear opportunity for differentiation beyond conventional citrus and tropical blends. Achachairu, cultivated around the Santa Cruz region on more than 5,000 acres with an estimated yield of 100 tons (90.7 metric tons), offers a strong base for limitededition nectars, blended products, and storytellingdriven branding.

Effective processing and supply planning are key to unlocking this potential. By converting seasonal fruits into pulp, concentrates, or frozen inputs, producers can reduce waste and preserve flavour yearround. This supports premium localised lines in modern retail, while small pack sizes enable trial through neighbourhood stores.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Bolivia Juice Market Segmentation Analysis

By Category

- 100% Juice

- Not from Concentrate

- Reconstituted

- Juice Drinks (up to 24% Juice)

- Nectars

- High Concentration (40% to 50% fruit content)

- Medium Concentration (30% to 39% fruit content)

- Low Concentration (25% to 29% fruit content)

- Vegetable Juice

- Fruit and Vegetable Blends

The segment with highest market share under Category is Juice drinks (up to 24% juice) hold the largest category share in Bolivia, accounting for approximately 80% of the market. This dominance reflects the segment’s ability to deliver refreshment and local flavours at accessible price points. Citrus blends such as orange and tangerine perform particularly well, aligning with climatic preferences. Manufacturers reinforce this leadership through diverse pack sizes, ranging from 5 L family bottles to 300 ml on-the-go formats.

Nectars represent the most dynamic sub-segment, supported by the inclusion of local fruits like guava and pineapple. However, juice drinks maintain clear leadership due to their affordability and extensive geographic reach. Flexible packaging, including PET bottles and sachets, ensures continued relevance for both family consumption and impulse purchases in school and work environments.

By Sales Channel

- Off-Trade

- Hypermarkets/ Supermarkets

- Retail Outlets

- Convenience Stores

- Online Platforms

- On-Trade

Off-trade dominates the Bolivian juice market with a 90% share, highlighting the importance of home-based consumption. Small neighbourhood grocers form the backbone of distribution, offering proximity and price transparency to shoppers who prefer frequent, low-value purchases. These outlets are essential for national brands such as Delizia and Frussion to reach rural and underserved areas.

Supermarkets and hypermarkets are emerging as the most dynamic off-trade formats. These stores attract health-conscious consumers and bulk buyers by providing prominent shelf space for innovative 150–300 ml child-friendly packs alongside large value formats. The coexistence of traditional retail and expanding modern trade ensures juice remains a core household staple in Bolivia through 2032.

List of Companies Covered in Bolivia Juice Market

The companies listed below are highly influential in the Bolivia juice market, with a significant market share and a strong impact on industry developments.

- Industrias Venado SA

- Agrov SRL

- DICOM Distribuidores del Oriente SRL

- Cía de Alimentos Ltda Delizia

- Pil Andina SA

- Embotelladoras Bolivianas Unidas SA (EMBOL)

Competitive Landscape

Bolivia juice market in 2025 is led by strong domestic players that compete primarily on affordability, packaging flexibility, and local relevance. Cía de Alimentos Ltda – Delizia retains leadership by volume, supported by its extensive local production base and a diversified portfolio spanning nectars and juice drinks. Its multi-format strategy, combining large PET bottles for value-seeking households with smaller PET bottles and sachets for portioned consumption, has reinforced its mass-market appeal, while the Tampico brand strengthens its positioning through consistent quality and flavour innovation. Meanwhile, Industrias Venado SA stands out as the most dynamic player, leveraging sharp price positioning, locally resonant flavours, and new nectar launches in 300 ml PET formats to expand reach across traditional and modern retail channels.

Frequently Asked Questions

Related Report

1. Market Segmentation

1.1. Research Scope

1.2. Research Methodology

1.3. Definitions and Assumptions

2. Executive Summary

3. Bolivia Juice Market Policies, Regulations, and Standards

4. Bolivia Juice Market Dynamics

4.1. Growth Factors

4.2. Challenges

4.3. Trends

4.4. Opportunities

5. Bolivia Juice Market Statistics, 2022-2032F

5.1. Market Size & Growth Outlook

5.1.1.By Revenues in USD Million

5.1.2.By Quantity Sold in Million Litres

5.2. Market Segmentation & Growth Outlook

5.2.1.By Category

5.2.1.1. 100% Juice- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.1. Not from Concentrate- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.2. Reconstituted- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2. Juice Drinks (up to 24% Juice)- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3. Nectars- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3.1. High Concentration (40% to 50% fruit content)- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3.2. Medium Concentration (30% to 39% fruit content)- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3.3. Low Concentration (25% to 29% fruit content)- Market Insights and Forecast 2022-2032, USD Million

5.2.1.4. Vegetable Juice- Market Insights and Forecast 2022-2032, USD Million

5.2.1.5. Fruit and Vegetable Blends- Market Insights and Forecast 2022-2032, USD Million

5.2.2.By Nature

5.2.2.1. Conventional- Market Insights and Forecast 2022-2032, USD Million

5.2.2.2. Organic- Market Insights and Forecast 2022-2032, USD Million

5.2.3.By Packaging Material

5.2.3.1. Plastic- Market Insights and Forecast 2022-2032, USD Million

5.2.3.2. Glass- Market Insights and Forecast 2022-2032, USD Million

5.2.3.3. Metal- Market Insights and Forecast 2022-2032, USD Million

5.2.3.4. Others- Market Insights and Forecast 2022-2032, USD Million

5.2.4.By Packaging Type

5.2.4.1. PET Bottles- Market Insights and Forecast 2022-2032, USD Million

5.2.4.2. Aseptic Packages (Cartons)- Market Insights and Forecast 2022-2032, USD Million

5.2.4.3. Glass Bottles- Market Insights and Forecast 2022-2032, USD Million

5.2.4.4. Metal Cans- Market Insights and Forecast 2022-2032, USD Million

5.2.4.5. Disposable Cups & Pouches- Market Insights and Forecast 2022-2032, USD Million

5.2.5.By Sales Channel

5.2.5.1. Off-Trade- Market Insights and Forecast 2022-2032, USD Million

5.2.5.1.1. Hypermarkets/ Supermarkets - Market Insights and Forecast 2022-2032, USD Million

5.2.5.1.2. Retail Outlets - Market Insights and Forecast 2022-2032, USD Million

5.2.5.1.3. Convenience Stores- Market Insights and Forecast 2022-2032, USD Million

5.2.5.1.4. Online Platforms- Market Insights and Forecast 2022-2032, USD Million

5.2.5.2. On-Trade- Market Insights and Forecast 2022-2032, USD Million

5.2.6.By Competitors

5.2.6.1. Competition Characteristics

5.2.6.2. Market Share & Analysis

6. Bolivia 100% Juice Market Statistics, 2022-2032

6.1. Market Size & Growth Outlook

6.1.1.By Revenues in USD Million

6.1.2.By Quantity Sold in Million Litres

6.2. Market Segmentation & Growth Outlook

6.2.1.By Nature- Market Insights and Forecast 2022-2032, USD Million

6.2.2.By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

6.2.3.By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

6.2.4.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

7. Bolivia Juice Drinks (up to 24% Juice) Market Statistics, 2022-2032

7.1. Market Size & Growth Outlook

7.1.1.By Revenues in USD Million

7.1.2.By Quantity Sold in Million Litres

7.2. Market Segmentation & Growth Outlook

7.2.1.By Nature- Market Insights and Forecast 2022-2032, USD Million

7.2.2.By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

7.2.3.By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

7.2.4.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

8. Bolivia Nectars Market Statistics, 2022-2032

8.1. Market Size & Growth Outlook

8.1.1.By Revenues in USD Million

8.1.2.By Quantity Sold in Million Litres

8.2. Market Segmentation & Growth Outlook

8.2.1.By Nature- Market Insights and Forecast 2022-2032, USD Million

8.2.2.By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

8.2.3.By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

8.2.4.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

9. Bolivia Vegetable Juice Market Statistics, 2022-2032

9.1. Market Size & Growth Outlook

9.1.1.By Revenues in USD Million

9.1.2.By Quantity Sold in Million Litres

9.2. Market Segmentation & Growth Outlook

9.2.1.By Nature- Market Insights and Forecast 2022-2032, USD Million

9.2.2.By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

9.2.3.By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

9.2.4.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

10. Bolivia Fruit and Vegetable Blends Market Statistics, 2022-2032

10.1. Market Size & Growth Outlook

10.1.1. By Revenues in USD Million

10.1.2. By Quantity Sold in Million Litres

10.2. Market Segmentation & Growth Outlook

10.2.1. By Nature- Market Insights and Forecast 2022-2032, USD Million

10.2.2. By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

10.2.3. By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

10.2.4. By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

11. Competitive Outlook

11.1. Company Profiles

11.1.1. Cía de Alimentos Ltda Delizia

11.1.1.1. Business Description

11.1.1.2. Product Portfolio

11.1.1.3. Collaborations & Alliances

11.1.1.4. Recent Developments

11.1.1.5. Financial Details

11.1.1.6. Others

11.1.2. Pil Andina SA

11.1.2.1. Business Description

11.1.2.2. Product Portfolio

11.1.2.3. Collaborations & Alliances

11.1.2.4. Recent Developments

11.1.2.5. Financial Details

11.1.2.6. Others

11.1.3. Embotelladoras Bolivianas Unidas SA (EMBOL)

11.1.3.1. Business Description

11.1.3.2. Product Portfolio

11.1.3.3. Collaborations & Alliances

11.1.3.4. Recent Developments

11.1.3.5. Financial Details

11.1.3.6. Others

11.1.4. Industrias Venado SA

11.1.4.1. Business Description

11.1.4.2. Product Portfolio

11.1.4.3. Collaborations & Alliances

11.1.4.4. Recent Developments

11.1.4.5. Financial Details

11.1.4.6. Others

11.1.5. Agrov SRL

11.1.5.1. Business Description

11.1.5.2. Product Portfolio

11.1.5.3. Collaborations & Alliances

11.1.5.4. Recent Developments

11.1.5.5. Financial Details

11.1.5.6. Others

11.1.6. DICOM Distribuidores del Oriente SRL

11.1.6.1. Business Description

11.1.6.2. Product Portfolio

11.1.6.3. Collaborations & Alliances

11.1.6.4. Recent Developments

11.1.6.5. Financial Details

11.1.6.6. Others

12. Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Category |

|

| By Nature |

|

| By Packaging Material |

|

| By Packaging Type |

|

| By Sales Channel |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.