Australia Menstrual Care Market Report: Trends, Growth and Forecast (2026-2032)

Product Type (Pantyliners, Tampons (Applicator Tampons, Digital Tampons), Towels (Standard Towels (Standard Towels with Wings, Standard Towels Without Wings), Slim/Thin/Ultra-Thin Towels (Slim/Thin/Ultra-Thin Towels with Wings, Slim/Thin/Ultra-Thin Towels Without Wings)), Intimate Wipes, Menstrual Cups, Period Underwear), Nature (Disposable, Reusable), Age Group (Up to 18 Years, 19-30 Years, 31-40 Years, 40 Years and Above), Sales Channel (Retail Offline, Retail Online) ... Read more

|

Major Players

|

Australia Menstrual Care Market Statistics and Insights, 2026

- Market Size Statistics

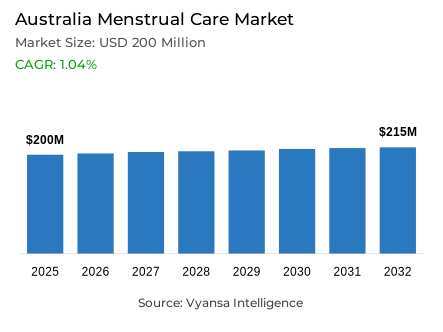

- Menstrual care in Australia is estimated at USD 200 million.

- The market size is expected to grow to USD 215 million by 2032.

- Market to register a cagr of around 1.04% during 2026-32.

- Product Type Shares

- Towels grabbed market share of 60%.

- Competition

- More than 15 companies are actively engaged in producing menstrual care in Australia.

- Top 5 companies acquired around 85% of the market share.

- Organic Initiative Ltd, Woolworths Group Ltd, Procter & Gamble Australia Pty Ltd, Essity AustralAsia, Kimberly-Clark Australia Pty Ltd etc., are few of the top companies.

- Sales Channel

- Retail offline grabbed 80% of the market.

Australia Menstrual Care Market Outlook

The Australia market for menstrual supplies is expected to rise from $200 million in 2025 to $215 million by 2032, resulting in a CAGR of about 1.04% from 2026-2032. The market may stabilize as immigration continues to bring awareness to menstrual health and maintain stable demand for menstrual products. The towels category holds about 60% of the market share and maintains the leading category based on high-frequency use and preference for slim and ultra-thin formats for comfort and convenience to an active lifestyle. Enhanced efforts to reduce the stigma around menstruation and campaigns promoting inclusion, expansion and access to products, and organized campaigns from organizations such as Share the Dignity have led to open discussion of menstruation and menstrual products, which have supported adoption across all age groups.

Leading suppliers, such as Essity Australasia, Kimberly-Clark Australia, and Wesfarmers Ltd., will likely maintain their positions by combining sustainability-led innovation with value-based options. Essity TOM Organic and Modibodi are leading brands that are leaning in to eco-solutions and reusable menstruation options such as menstrual cups, and period underwear. U by Kotex will continue to strengthen its brand position by attacking period poverty, while championing social causes through authentic methods that have fostered brand trust and loyalty. Meanwhile, U by Kotex continues strengthening its position by combating period poverty and advancing social causes in ways that garner brand trust and loyalty. Private label products at affordable prices from supermarket chains like Coles further appeal to the price sensitivity of end users burdened by an increase in the cost of living.

With a market share of approximately 80%, retail offline is still the most preferred channel due to the convenience, discounts, and variety in supermarkets like Woolworths and Coles. In this regard, retail online and subscriptions are gaining extra momentum, as there are now also time-saving options such as click-and-collect, and personalized deliveries.

In the longer term, the market will bring together AI-based period tracking applications and data-based health tools that will offer recommendations of products on a personalized basis, and this will allow the brand to advance end users engagement. and sustainability will remain a big factor, with reusable menstrual care products continuing to surface among environmentally based end users across Australia.

Australia Menstrual Care Market Growth DriverGovernment Awareness Campaigns and Immigration Sustain Market Growth

Australia menstrual care market is showing robust growth on the back of strong government initiatives, coupled with increasing public awareness about menstrual health. The Australia Government, through the Department of Health, continues to promote menstrual education in schools and the workplace as an ongoing strategy to normalize discussion and improve the health literacy of women. Indeed, Share the Dignity said 51% of women in Australia miss sports due to menstruation-a factor that calls for more awareness to help eliminate stigma and support inclusivity across communities.

Meanwhile, immigration is driving the growth of the end users population for menstrual products. According to the ABS, net overseas migration reached 733,000 between 2022 and 2023, providing a boost to product diversification and awareness. This is complemented by the arrival of skilled immigrants who have experience with international brands that increase the diversity of market demand. These social and demographic trends together have been sustaining consistent growth and promoting menstrual health awareness across Australia.

Australia Menstrual Care Market TrendPersonalisation and Data Integration Redefine Menstrual Health Engagement

Personalisation is fast becoming a defining feature of Australia menstrual care market, as brands harness technology and data-driven insights to create tailored user experiences. Adoption of menstrual tracking apps and digital wellness platforms allows users to track cycles and find product recommendations that suit individual needs. For example, this trend is being manifested in U by Kotex's Period Tracker app, which provides users with AI-driven analytics for personalized insights into their period cycles. According to the Australia Digital Health Agency, about 89% of Australias use a smartphone to track something related to their health, demonstrating huge potential for digital engagement.

AI integration with predictive analytics will also help brands create deeper connections with the end users. The WHO believes that menstrual health technologies contribute to improved health literacy and hygiene management. By marrying data insights to product innovation, menstrual care brands build trust, improve retention, and eventually turn menstrual care into a holistic wellness experience.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Australia Menstrual Care Market Opportunity Sustainability and Reusable Products Offer Long-Term Market Potential

Sustainability is becoming a key factor driving growth in Australia’s menstrual care market. There is a rising demand for eco-friendly and reusable solutions such as menstrual cups, washable pads, and period underwear, reflecting growing environmental awareness. According to the Australia Government Department of Climate Change, Energy, the Environment and Water, around 72% of Australians are actively trying to reduce household waste. Leading brands like Modibodi and TOM Organic are at the forefront of this shift, offering innovative reusable options that provide both sustainable and economical benefits to end users.

The need for sustainable menstrual care solutions is further supported by data from the United Nations Environment Programme, which estimates that over 200,000 tonnes of discarded hygiene products end up in landfills each year. As the market evolves, menstrual care companies will need to adopt sustainable materials, ensure ethical and transparent sourcing, and showcase genuine commitment to environmental responsibility. These efforts will be vital for aligning with the growing preferences of eco-conscious end users and maintaining long-term market relevance.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Australia Menstrual Care Market Segmentation Analysis

By Product Type

- Pantyliners

- Tampons

- Towels

- Intimate Wipes

- Menstrual Cups

- Period Underwear

The segment with the highest share under Product Type is towels, accounting for around 60% of the menstrual care market in Australia. Towels continue to dominate due to comfort, reliability, and wide availability across all retail channels. Slim, thin, and ultra-thin towels with wings hold great appeal, as they meet the growing demand for discreetness, comfort, and performance. Such diversity in the category has definitely enabled brands to address different flow intensities and lifestyle needs and thus sustain strong and consistent sales momentum.

The awareness about menstrual hygiene and health has also contributed to the demand for towels, basically among females looking for reliable solutions for daily use. As end users increasingly look for products that match their personal preferences and sensitivity needs, the segment of towels may continue to maintain the lead with innovations in skin-friendly and sustainable materials that meet the evolving expectations of end users.

By Sales Channel

- Retail Offline

- Retail Online

The segment with highest market share under sales channel is Retail offline captured the major share of nearly 80% of the Australia menstrual care market. Supermarkets such as Woolworths and Coles continue to dominate since they offer convenience, consistent product availability, and very frequent promotional offers. They also serve a wide range of income groups on the basis of an extended assortment portfolio-from premium, eco-friendly alternatives to affordable private labels-to ensure regular in-store traffic.

While there is gradually increasing in retail online selling through retail online and subscription-based sales, neither changes the fact that the majority of end users prefer in-store purchases of menstrual care products for brand comparisons and immediate discounts. Additionally, click-and-collect and membership benefits in offline stores further strengthened the position of this channel. With increasing urbanisation and higher population due to immigration, retail offline channels are expected to remain the primary point of purchase for menstrual care products throughout the forecast period.

Top Companies in Australia Menstrual Care Market

The top companies operating in the market include Organic Initiative Ltd, Woolworths Group Ltd, Procter & Gamble Australia Pty Ltd, Essity AustralAsia, Kimberly-Clark Australia Pty Ltd, Johnson & Johnson Pacific Pty Ltd, Cottons Pty Ltd, Aldi Stores Supermarkets Pty Ltd, Wesfarmers Ltd, Zuru Pty Ltd, etc., are the top players operating in the Australia menstrual care market.

Market News & Updates

- Essity AustralAsia, 2024–2025:

Essity expanded sustainable menstrual-care options in Australia, with increased visibility of reusable period underwear and related product formats

- Kimberly‑Clark Australia, 2023–2025:

Kimberly‑Clark continued to market Kotex with sustainability messaging and local promotions throughout 2023-2025.

Frequently Asked Questions

Related Report

1. Market Segmentation

1.1. Research Scope

1.2. Research Methodology

1.3. Definitions and Assumptions

2. Executive Summary

3. Australia Menstrual Care Market Policies, Regulations, and Standards

4. Australia Menstrual Care Market Dynamics

4.1. Growth Factors

4.2. Challenges

4.3. Trends

4.4. Opportunities

5. Australia Menstrual Care Market Statistics, 2022-2032F

5.1. Market Size & Growth Outlook

5.1.1.By Revenues in USD Million

5.2. Market Segmentation & Growth Outlook

5.2.1.By Product Type

5.2.1.1. Pantyliners- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2. Tampons- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2.1. Applicator Tampons- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2.2. Digital Tampons- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3. Towels- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3.1. Standard Towels- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3.1.1. Standard Towels with Wings- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3.1.2. Standard Towels Without Wings- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3.2. Slim/Thin/Ultra-Thin Towels- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3.2.1. Slim/Thin/Ultra-Thin Towels with Wings- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3.2.2. Slim/Thin/Ultra-Thin Towels Without Wings- Market Insights and Forecast 2022-2032, USD Million

5.2.1.4. Intimate Wipes- Market Insights and Forecast 2022-2032, USD Million

5.2.1.5. Menstrual Cups- Market Insights and Forecast 2022-2032, USD Million

5.2.1.6. Period Underwear- Market Insights and Forecast 2022-2032, USD Million

5.2.2.By Nature

5.2.2.1. Disposable- Market Insights and Forecast 2022-2032, USD Million

5.2.2.2. Reusable- Market Insights and Forecast 2022-2032, USD Million

5.2.3.By Age Group

5.2.3.1. Up to 18 Years- Market Insights and Forecast 2022-2032, USD Million

5.2.3.2. 19-30 Years- Market Insights and Forecast 2022-2032, USD Million

5.2.3.3. 31-40 Years- Market Insights and Forecast 2022-2032, USD Million

5.2.3.4. 40 Years and Above- Market Insights and Forecast 2022-2032, USD Million

5.2.4.By Sales Channel

5.2.4.1. Retail Offline- Market Insights and Forecast 2022-2032, USD Million

5.2.4.2. Retail Online- Market Insights and Forecast 2022-2032, USD Million

5.2.5.By Competitors

5.2.5.1. Competition Characteristics

5.2.5.2. Market Share & Analysis

6. Australia Pantyliners Menstrual Care Market Statistics, 2022-2032

6.1. Market Size & Growth Outlook

6.1.1.By Revenues in USD Million

6.2. Market Segmentation & Growth Outlook

6.2.1.By Nature- Market Insights and Forecast 2022-2032, USD Million

6.2.2.By Age Group- Market Insights and Forecast 2022-2032, USD Million

6.2.3.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

7. Australia Tampons Menstrual Care Market Statistics, 2022-2032

7.1. Market Size & Growth Outlook

7.1.1.By Revenues in USD Million

7.2. Market Segmentation & Growth Outlook

7.2.1.By Product Type- Market Insights and Forecast 2022-2032, USD Million

7.2.2.By Nature- Market Insights and Forecast 2022-2032, USD Million

7.2.3.By Age Group- Market Insights and Forecast 2022-2032, USD Million

7.2.4.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

8. Australia Towels Menstrual Care Market Statistics, 2022-2032

8.1. Market Size & Growth Outlook

8.1.1.By Revenues in USD Million

8.2. Market Segmentation & Growth Outlook

8.2.1.By Product Type- Market Insights and Forecast 2022-2032, USD Million

8.2.2.By Nature- Market Insights and Forecast 2022-2032, USD Million

8.2.3.By Age Group- Market Insights and Forecast 2022-2032, USD Million

8.2.4.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

9. Australia Intimate Wipes Market Statistics, 2022-2032

9.1. Market Size & Growth Outlook

9.1.1.By Revenues in USD Million

9.2. Market Segmentation & Growth Outlook

9.2.1.By Nature- Market Insights and Forecast 2022-2032, USD Million

9.2.2.By Age Group- Market Insights and Forecast 2022-2032, USD Million

9.2.3.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

10. Australia Menstrual Cups Menstrual Care Market Statistics, 2022-2032

10.1. Market Size & Growth Outlook

10.1.1. By Revenues in USD Million

10.2. Market Segmentation & Growth Outlook

10.2.1. By Nature- Market Insights and Forecast 2022-2032, USD Million

10.2.2. By Age Group- Market Insights and Forecast 2022-2032, USD Million

10.2.3. By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

11. Australia Period Underwear Menstrual Care Market Statistics, 2022-2032

11.1. Market Size & Growth Outlook

11.1.1. By Revenues in USD Million

11.2. Market Segmentation & Growth Outlook

11.2.1. By Nature- Market Insights and Forecast 2022-2032, USD Million

11.2.2. By Age Group- Market Insights and Forecast 2022-2032, USD Million

11.2.3. By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

12. Competitive Outlook

12.1. Company Profiles

12.1.1. Essity AustralAsia

12.1.1.1. Business Description

12.1.1.2. Product Portfolio

12.1.1.3. Collaborations & Alliances

12.1.1.4. Recent Developments

12.1.1.5. Financial Details

12.1.1.6. Others

12.1.2. Kimberly-Clark Australia Pty Ltd

12.1.2.1. Business Description

12.1.2.2. Product Portfolio

12.1.2.3. Collaborations & Alliances

12.1.2.4. Recent Developments

12.1.2.5. Financial Details

12.1.2.6. Others

12.1.3. Johnson & Johnson Pacific Pty Ltd

12.1.3.1. Business Description

12.1.3.2. Product Portfolio

12.1.3.3. Collaborations & Alliances

12.1.3.4. Recent Developments

12.1.3.5. Financial Details

12.1.3.6. Others

12.1.4. Cottons Pty Ltd

12.1.4.1. Business Description

12.1.4.2. Product Portfolio

12.1.4.3. Collaborations & Alliances

12.1.4.4. Recent Developments

12.1.4.5. Financial Details

12.1.4.6. Others

12.1.5. Aldi Stores Supermarkets Pty Ltd

12.1.5.1. Business Description

12.1.5.2. Product Portfolio

12.1.5.3. Collaborations & Alliances

12.1.5.4. Recent Developments

12.1.5.5. Financial Details

12.1.5.6. Others

12.1.6. Organic Initiative Ltd

12.1.6.1. Business Description

12.1.6.2. Product Portfolio

12.1.6.3. Collaborations & Alliances

12.1.6.4. Recent Developments

12.1.6.5. Financial Details

12.1.6.6. Others

12.1.7. Woolworths Group Ltd

12.1.7.1. Business Description

12.1.7.2. Product Portfolio

12.1.7.3. Collaborations & Alliances

12.1.7.4. Recent Developments

12.1.7.5. Financial Details

12.1.7.6. Others

12.1.8. Procter & Gamble Australia Pty Ltd

12.1.8.1. Business Description

12.1.8.2. Product Portfolio

12.1.8.3. Collaborations & Alliances

12.1.8.4. Recent Developments

12.1.8.5. Financial Details

12.1.8.6. Others

12.1.9. Wesfarmers Ltd

12.1.9.1. Business Description

12.1.9.2. Product Portfolio

12.1.9.3. Collaborations & Alliances

12.1.9.4. Recent Developments

12.1.9.5. Financial Details

12.1.9.6. Others

12.1.10. Zuru Pty Ltd

12.1.10.1.Business Description

12.1.10.2.Product Portfolio

12.1.10.3.Collaborations & Alliances

12.1.10.4.Recent Developments

12.1.10.5.Financial Details

12.1.10.6.Others

13. Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Product Type |

|

| By Nature |

|

| By Age Group |

|

| By Sales Channel |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.