Global Agricultural Robots Market Report: Trends, Growth and Forecast (2026-2032)

By Robot Type (Unmanned Aerial Vehicles (UAVs)/Drones, Milking Robots, Driverless Tractors, Automated Harvesting Robots, Robotic Weeders, Automated Cultivation Systems, Livestock Farming Robots, Material Handling Robots, Others), By Offering (Hardware, Software, Services), By Application (Harvest Management, Field Mapping & Crop Monitoring, Spraying Management, Planting & Seeding Management, Soil & Irrigation Management, Weather Tracking & Forecasting, Inventory & Supply Chain Management, Others), By Farming Environment (Indoor, Outdoor), By Farm Size (Small-Sized Farms, Mid-Sized Farms, Large-Sized Farms), By Region (North America, South America, Europe, Middle East & Africa, Asia Pacific) ... Read more

|

Major Players

|

Global Agricultural Robots Market Statistics and Insights, 2026

- Market Size Statistics

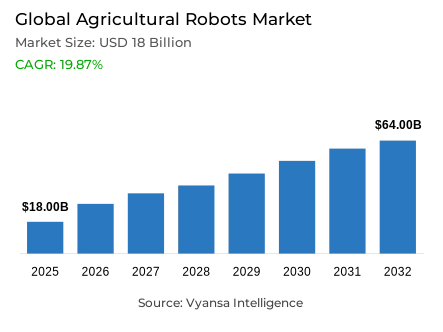

- Agricultural robots market size in Global was valued at USD 18 billion in 2025 and is estimated at USD 21 billion in 2026.

- The market size is expected to grow to USD 64 billion by 2032.

- Market to register a CAGR of around 19.87% during 2026-32.

- Robot Type Shares

- Unmanned aerial vehicles (uavs)/drones grabbed market share of 35%.

- Competition

- More than 20 companies are actively engaged in producing agricultural robots.

- Top 5 companies acquired around 35% of the market share.

- GEA Group AG, Kubota Corporation, XAG Co. Ltd., Deere & Company, SZ DJI Technology Co. Ltd. etc., are few of the top companies.

- Offering

- Hardware grabbed 55% of the market.

- Region

- North America leads with a 40% share of the global market.

Global Agricultural Robots Market Outlook

The Global agricultural robots market was valued at USD 18 billion in 2025 and is projected to advance from USD 21 billion in 2026 to USD 64 billion by 2032, registering a CAGR of 19.87% across the forecast period. This sustained and operationally grounded expansion reflects a commercially dependable growth environment within the Global agricultural robots market, where accelerating farm labor scarcity, rising input cost pressure, narrowing seasonal operating windows, and the demonstrated productivity gains of AI-powered agricultural robots are collectively converting automation from an aspirational investment into a procurement priority across commercial farms, agribusinesses, custom applicators, and equipment dealer networks globally. Growth is not driven by speculative technology enthusiasm but by documented field outcomes that link robotic deployment directly to measurable improvements in labor efficiency, chemical reduction, and crop operation predictability.

Regional adoption is shaped by distinct operational priorities rather than uniform technology readiness. North America benefits from commercial-scale farms, mature precision agriculture robotics infrastructure, specialty-crop labor pressure, and dealer-led automation support that accelerates grower procurement confidence, while Europe advances through sustainability mandates, chemical-reduction obligations, and farm-efficiency targets embedded in agricultural policy frameworks. Asia Pacific is supported by mechanisation gaps, food-security imperatives, and agricultural drones service models that extend automation access across fragmented smallholder and mid-scale farming systems, creating a commercially diverse and geographically distributed demand structure that no single regional adoption pattern defines.

Agricultural drones and UAVs command 35% of the robot type segment, anchored in their capacity for fast field access, scalable crop monitoring, flexible payload deployment, and lower operational friction than ground-based alternatives across scouting, spraying, and field-mapping applications. Hardware leads the offering segment at 58%, reflecting the structural reality that farm procurement still prioritises physical machines, sensors, actuators, sprayers, and navigation systems before software monetisation can scale across grower operations.

North America anchors the Agricultural Robots Market with 40% of global demand, supported by commercial-scale deployment readiness, supplier ecosystem depth, and faster integration of autonomous tractors and autonomy kits into high-value crop and large-acre farm workflows. As per data published by Bluewhite and New Holland, autonomous farming systems are already operating across 150,000 acres in the United States with more than 20 leading permanent crop growers, establishing North America as the most commercially advanced regional market for repeatable robotic field deployment at scale.

Global Agricultural Robots Market Growth Driver

Labor Shortages Are Accelerating Autonomous Farm Operations

Farm labor scarcity is the most commercially significant and operationally immediate demand driver within the Global agricultural robots market, compelling growers to replace operator-dependent field tasks with autonomous platforms capable of performing spraying, scouting, weeding, harvesting, and orchard operations consistently across compressed seasonal windows when workforce availability is most constrained. As per data published by John Deere citing the American Farm Bureau Federation, approximately 2.4 million farm jobs need to be filled annually across the United States, while Deere introduced second-generation autonomous farm equipment combining computer vision, AI, and cameras in 2025, confirming that the labor gap sustaining smart farming robots procurement is both structurally persistent and commercially large enough to justify fleet-level automation investment among commercial growers, dealers, and custom service providers.

Certification complexity and field-integration barriers are simultaneously creating the most commercially consequential adoption challenge within the Agriculture Robotics Market, as aerial spraying operators must navigate aircraft certification, operating rules, payload management, and data workflow compliance obligations that raise deployment friction for smaller farms, cooperatives, and contractors before autonomous aerial services become routine practice. Industry findings confirm that regulatory approval readiness is becoming a measurable competitive differentiator for platform vendors and regional equipment distributors, while the strongest commercial opportunity lies in AI in agriculture precision application, where John Deere's See and Spray technology reduced non-residual herbicide use by nearly 50% across more than five million acres during the 2025 growing season, directly linking robotic farming equipment investment to documented input savings that shift supplier competition toward agronomic outcomes rather than equipment specifications alone.

Global Agricultural Robots Market Challenge

Certification and Field Integration Complexity Are Slowing Deployment

The most commercially consequential structural challenge within the agricultural automation market is the regulatory and operational complexity surrounding aerial spraying systems, which require aircraft certification, operating rule compliance, safety procedure documentation, payload handling protocols, and data workflow management before commercial-scale deployment can proceed in most regional markets. Based on data from the Federal Aviation Administration, agricultural aircraft operations are regulated under 14 CFR Part 137 and the certification pathway encompasses five structured phases from preapplication through certificate issuance, confirming that the compliance investment required before drone-based spraying becomes routine farm practice is substantial enough to delay supplier onboarding, constrain service-provider expansion, and raise deployment barriers most severely for smaller farms and cooperatives operating within fragmented seasonal spray windows.

Field-level integration requirements compound this regulatory challenge by creating a structural gap between automation capability and grower readiness across diverse farm sizes, equipment configurations, and digital infrastructure maturity levels. As indicated by authoritative sources across the precision agriculture sector, farms prioritising autonomous farming robots must manage terrain variability, connectivity limitations, crop-specific navigation requirements, technical training obligations, and maintenance serviceability before robotic systems can generate consistent operational value, creating adoption friction that rewards vendors offering turnkey deployment packages, dealer-supported integration, and documented uptime performance over suppliers delivering hardware capability alone.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Global Agricultural Robots Market Trend

AI-Enabled Precision Application Is Reshaping Farm Robotics

A well-defined and commercially consequential structural trend is reshaping product development priorities and buyer evaluation criteria across the Global agricultural robots market, as farms progressively move from blanket input application toward machine vision in agriculture interventions that identify weeds, apply chemicals precisely where needed, and generate field-level performance data that quantifies automation value beyond labor substitution. Evidence drawn from public data released by John Deere confirms that See and Spray technology operated across more than five million acres during the 2025 growing season, reducing non-residual herbicide use by nearly 50% and saving nearly 31 million gallons of herbicide mix, establishing AI-based precision application as a commercially validated automation outcome that strengthens the procurement case for robotic weeders, smart spraying systems, and sensor-equipped field robots across row crops, specialty crops, and custom application fleets.

The commercial implications of this trend extend beyond chemical reduction into the competitive architecture of the broader market. In line with findings from Auburn University and USDA-ARS, researchers are deploying drones and AI across crop scouting, pest identification, soil monitoring, pesticide application, cover crop seeding, fertiliser delivery, and autonomous sensor-data analysis, confirming that drone-based crop monitoring and active input delivery are converging into a single operational platform that rewards suppliers capable of combining adaptable payloads, software integration, and measurable agronomic outcome documentation — a shift that structurally advantages vendors who position robots as precision productivity tools rather than labor-replacement equipment.

Global Agricultural Robots Market Opportunity

Specialty Crop Automation Is Opening Scalable Deployment Windows

The most commercially significant and structurally concentrated growth opportunity within the Global agricultural robots market lies in specialty crop automation, where orchards, vineyards, vegetable systems, and high-value fruit operations face peak-season labor bottlenecks across harvesting, spraying, mowing, thinning, pruning, and crop monitoring that create compelling and time-bound procurement demand for robotic platforms capable of operating within structured rows, preserving crop quality, and maintaining field access during compressed operating windows. As per official figures from USDA Agricultural Research Service, a dual-arm apple harvesting robot developed with Michigan State University demonstrated up to a 34% improvement in harvesting efficiency compared with a single-arm design, directly validating the performance gains that automated harvesting robots can deliver and strengthening the commercial case for crop-specific end effectors, navigation systems, and grower training programmes across premium production environments where labor timing directly determines yield, grade consistency, and harvest completion.

The robotic farming service and aftermarket opportunity independently creates a separately significant commercial demand layer as equipment ownership models evolve toward leasing, robotics-as-a-service, and dealer-supported upgrade frameworks that reduce grower capital commitment while expanding supplier revenue streams. Data compiled from internationally recognised public authorities at USDA-ARS confirms that AI-enabled drones are advancing from imaging tools into active field operation platforms across multiple application types, confirming that the transition from single-use equipment sales toward integrated deployment packages, fleet management subscriptions, sensor upgrades, and application-specific software represents the next commercially durable revenue expansion path for agricultural robot manufacturers with established dealer networks and field-service infrastructure.

Global Agricultural Robots Market Regional Analysis

By Region

- North America

- South America

- Europe

- Middle East & Africa

- Asia Pacific

North America leads with 40% of global demand, a concentration that reflects the region's exceptional convergence of commercial-scale farm operations, mature equipment dealer networks, advanced precision agriculture infrastructure, and strong specialty-crop automation needs that together create both the operational urgency and the procurement readiness for robotic field deployment at commercial scale. As per data published by John Deere, the American Farm Bureau Federation estimates approximately 2.4 million annual farm job vacancies across the United States, while Bluewhite's autonomous farming systems are already operating across 150,000 acres with more than 20 leading permanent crop growers, confirming that the region's grower base is actively converting labor pain points into repeatable autonomous field operations supported by dealer distribution and fleet-management platforms.

The region's structural advantages extend beyond grower adoption into the supplier and service ecosystem depth that accelerates commercialisation for both established equipment manufacturers and agri-tech robotics startups seeking scalable deployment pathways. Validated reports from New Holland and Bluewhite confirm that autonomy retrofit kits, dealer-supported integration, and fleet management platforms are gaining commercial traction across orchards, vineyards, and specialty-crop systems in the United States, establishing North America as the global reference market for autonomous farming deployment models that international suppliers and regional agribusinesses are progressively adopting as the commercial benchmark for robotic field integration at scale.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Global Agricultural Robots Market Segmentation Analysis

By Robot Type

- Unmanned Aerial Vehicles (UAVs)/Drones

- Milking Robots

- Driverless Tractors

- Automated Harvesting Robots

- Robotic Weeders

- Automated Cultivation Systems

- Livestock Farming Robots

- Material Handling Robots

- Others

UAVs and agricultural drones command the highest share within the robot type category at 35%, reflecting the consistent and commercially embedded preference within the Global agricultural robots market for aerial platforms that deliver fast field access, scalable monitoring capability, flexible payload configurations, and lower deployment friction than most ground-based robotic alternatives across scouting, spraying, field mapping, fertiliser application, and cover crop seeding operations. Growers, custom applicators, and agribusinesses consistently prioritise UAV platforms because their capacity to cover large areas rapidly, access difficult terrain without crop damage, and adapt across seasonal tasks makes them operationally versatile in ways that crop-specific ground robots cannot replicate across the diverse field conditions and farm-size profiles that define global agricultural demand.

The segment's commercial durability deepens as application breadth continues to expand beyond imaging into active field operations. Evidence drawn from public data released by Auburn University confirms that USDA-ARS researchers are applying drones across pesticide delivery, cover crop seeding, fertiliser application, harvest aid administration, and autonomous sensor-data analysis, directly validating UAVs for farming as multi-function field platforms rather than single-purpose monitoring tools and supporting service-provider models, software integration partnerships, and payload innovation investment among suppliers serving diverse farm sizes and geographies.

By Offering

- Hardware

- Software

- Services

Hardware commands the highest share within the offering category at 58%, establishing physical machines, field implements, payload systems, and sensor assemblies as the most commercially prioritised and procurement-intensive component of farm automation investment within the Global agricultural robots market. Growers across row crops, orchards, vineyards, dairy operations, and large-scale broadacre systems consistently direct capital toward durable tractors, drone frames, batteries, actuators, controllers, end effectors, cameras, and navigation systems before advanced software monetisation can achieve commercial scale, creating a structurally front-loaded spending pattern that anchors near-term market revenue in equipment procurement and replacement cycles that are tied to seasonal field readiness requirements.

The segment's structural dominance is further reinforced by the crop-specific hardware configurations that leading manufacturers are bringing to market. As per data published by New Holland, its 2025 R4 robot series includes vineyard and orchard variants, with the R4 Electric Power using a 40 kWh battery pack and the R4 Hybrid Power using an HVO-compatible diesel engine with a 44 kW diesel-electric generator pack, confirming that growers increasingly require durable, configurable powertrains and crop-matched implements that convert farm automation systems from conceptual capability into practical field operations — a requirement that structurally advantages manufacturers with integrated platforms, attachments, and dealer service networks capable of supporting multi-season deployment.

Market Players in Global Agricultural Robots Market

These market players maintain a significant presence in the Global agricultural robots market sector and contribute to its ongoing evolution.

- GEA Group AG

- Kubota Corporation

- XAG Co. Ltd.

- Deere & Company

- SZ DJI Technology Co. Ltd.

- Lely Group

- DeLaval

- CNH Industrial

- Yanmar Holdings Co. Ltd.

- Solinftec

- Carbon Robotics

- Ecorobotix SA

- BouMatic Robotics

- Fullwood JOZ

- Naïo Technologies

Market News & Updates

- SZ DJI Technology Co. Ltd., 2025:

DJI Agriculture launched Agras T100, T70P, and T25P globally in July 2025. The new agricultural drones support spraying, spreading, and lifting applications, with higher payload capacity, improved safety systems, and more automated operation. The launch expands drone-based farm automation across crop protection and field operations.

- Deere & Company, 2025:

John Deere revealed new autonomous agricultural machines and second-generation autonomy technology at CES 2025. It includes the Autonomous 9RX Tractor for large-scale agriculture and the Autonomous 5ML Orchard Tractor for air blast spraying, using computer vision, AI, cameras, and LiDAR sensors. The release expands autonomous equipment options for field and orchard operations.

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- Global Agricultural Robots Market Policies, Regulations, and Standards

- Global Agricultural Robots Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- Global Agricultural Robots Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Units Sold in Thousand

- Market Segmentation & Growth Outlook

- By Robot Type

- Unmanned Aerial Vehicles (UAVs)/Drones- Market Insights and Forecast 2022-2032, USD Million

- Milking Robots- Market Insights and Forecast 2022-2032, USD Million

- Driverless Tractors- Market Insights and Forecast 2022-2032, USD Million

- Automated Harvesting Robots- Market Insights and Forecast 2022-2032, USD Million

- Robotic Weeders- Market Insights and Forecast 2022-2032, USD Million

- Automated Cultivation Systems- Market Insights and Forecast 2022-2032, USD Million

- Livestock Farming Robots- Market Insights and Forecast 2022-2032, USD Million

- Material Handling Robots- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By Offering

- Hardware- Market Insights and Forecast 2022-2032, USD Million

- Software- Market Insights and Forecast 2022-2032, USD Million

- Services- Market Insights and Forecast 2022-2032, USD Million

- By Application

- Harvest Management- Market Insights and Forecast 2022-2032, USD Million

- Field Mapping & Crop Monitoring- Market Insights and Forecast 2022-2032, USD Million

- Spraying Management- Market Insights and Forecast 2022-2032, USD Million

- Planting & Seeding Management- Market Insights and Forecast 2022-2032, USD Million

- Soil & Irrigation Management- Market Insights and Forecast 2022-2032, USD Million

- Weather Tracking & Forecasting- Market Insights and Forecast 2022-2032, USD Million

- Inventory & Supply Chain Management- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By Farming Environment

- Indoor- Market Insights and Forecast 2022-2032, USD Million

- Outdoor- Market Insights and Forecast 2022-2032, USD Million

- By Farm Size

- Small-Sized Farms- Market Insights and Forecast 2022-2032, USD Million

- Mid-Sized Farms- Market Insights and Forecast 2022-2032, USD Million

- Large-Sized Farms- Market Insights and Forecast 2022-2032, USD Million

- By Region

- North America

- South America

- Europe

- Middle East & Africa

- Asia Pacific

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Robot Type

- Market Size & Growth Outlook

- North America Agricultural Robots Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Units Sold in Thousand

- Market Segmentation & Growth Outlook

- By Robot Type- Market Insights and Forecast 2022-2032, USD Million

- By Offering- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Farming Environment- Market Insights and Forecast 2022-2032, USD Million

- By Farm Size- Market Insights and Forecast 2022-2032, USD Million

- By Country

- The US

- Canada

- Mexico

- Rest of North America

- The US Agricultural Robots Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Units Sold in Thousand

- Market Segmentation & Growth Outlook

- By Robot Type- Market Insights and Forecast 2022-2032, USD Million

- By Offering- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Farming Environment- Market Insights and Forecast 2022-2032, USD Million

- By Farm Size- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Canada Agricultural Robots Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Units Sold in Thousand

- Market Segmentation & Growth Outlook

- By Robot Type- Market Insights and Forecast 2022-2032, USD Million

- By Offering- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Farming Environment- Market Insights and Forecast 2022-2032, USD Million

- By Farm Size- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Mexico Agricultural Robots Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Units Sold in Thousand

- Market Segmentation & Growth Outlook

- By Robot Type- Market Insights and Forecast 2022-2032, USD Million

- By Offering- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Farming Environment- Market Insights and Forecast 2022-2032, USD Million

- By Farm Size- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Market Size & Growth Outlook

- South America Agricultural Robots Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Units Sold in Thousand

- Market Segmentation & Growth Outlook

- By Robot Type- Market Insights and Forecast 2022-2032, USD Million

- By Offering- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Farming Environment- Market Insights and Forecast 2022-2032, USD Million

- By Farm Size- Market Insights and Forecast 2022-2032, USD Million

- By Country

- Brazil

- Argentina

- Rest of South America

- Brazil Agricultural Robots Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Units Sold in Thousand

- Market Segmentation & Growth Outlook

- By Robot Type- Market Insights and Forecast 2022-2032, USD Million

- By Offering- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Farming Environment- Market Insights and Forecast 2022-2032, USD Million

- By Farm Size- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Argentina Agricultural Robots Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Units Sold in Thousand

- Market Segmentation & Growth Outlook

- By Robot Type- Market Insights and Forecast 2022-2032, USD Million

- By Offering- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Farming Environment- Market Insights and Forecast 2022-2032, USD Million

- By Farm Size- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Market Size & Growth Outlook

- Europe Agricultural Robots Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Units Sold in Thousand

- Market Segmentation & Growth Outlook

- By Robot Type- Market Insights and Forecast 2022-2032, USD Million

- By Offering- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Farming Environment- Market Insights and Forecast 2022-2032, USD Million

- By Farm Size- Market Insights and Forecast 2022-2032, USD Million

- By Country

- Germany

- The UK

- France

- Italy

- Spain

- Rest of Europe

- Germany Agricultural Robots Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Units Sold in Thousand

- Market Segmentation & Growth Outlook

- By Robot Type- Market Insights and Forecast 2022-2032, USD Million

- By Offering- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Farming Environment- Market Insights and Forecast 2022-2032, USD Million

- By Farm Size- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- The UK Agricultural Robots Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Units Sold in Thousand

- Market Segmentation & Growth Outlook

- By Robot Type- Market Insights and Forecast 2022-2032, USD Million

- By Offering- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Farming Environment- Market Insights and Forecast 2022-2032, USD Million

- By Farm Size- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- France Agricultural Robots Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Units Sold in Thousand

- Market Segmentation & Growth Outlook

- By Robot Type- Market Insights and Forecast 2022-2032, USD Million

- By Offering- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Farming Environment- Market Insights and Forecast 2022-2032, USD Million

- By Farm Size- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Italy Agricultural Robots Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Units Sold in Thousand

- Market Segmentation & Growth Outlook

- By Robot Type- Market Insights and Forecast 2022-2032, USD Million

- By Offering- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Farming Environment- Market Insights and Forecast 2022-2032, USD Million

- By Farm Size- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Spain Agricultural Robots Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Units Sold in Thousand

- Market Segmentation & Growth Outlook

- By Robot Type- Market Insights and Forecast 2022-2032, USD Million

- By Offering- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Farming Environment- Market Insights and Forecast 2022-2032, USD Million

- By Farm Size- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Market Size & Growth Outlook

- Middle East & Africa Agricultural Robots Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Units Sold in Thousand

- Market Segmentation & Growth Outlook

- By Robot Type- Market Insights and Forecast 2022-2032, USD Million

- By Offering- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Farming Environment- Market Insights and Forecast 2022-2032, USD Million

- By Farm Size- Market Insights and Forecast 2022-2032, USD Million

- By Country

- The UAE

- Saudi Arabia

- South Africa

- Egypt

- Rest of Middle East and Africa

- The UAE Agricultural Robots Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Units Sold in Thousand

- Market Segmentation & Growth Outlook

- By Robot Type- Market Insights and Forecast 2022-2032, USD Million

- By Offering- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Farming Environment- Market Insights and Forecast 2022-2032, USD Million

- By Farm Size- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Saudi Arabia Agricultural Robots Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Units Sold in Thousand

- Market Segmentation & Growth Outlook

- By Robot Type- Market Insights and Forecast 2022-2032, USD Million

- By Offering- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Farming Environment- Market Insights and Forecast 2022-2032, USD Million

- By Farm Size- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- South Africa Agricultural Robots Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Units Sold in Thousand

- Market Segmentation & Growth Outlook

- By Robot Type- Market Insights and Forecast 2022-2032, USD Million

- By Offering- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Farming Environment- Market Insights and Forecast 2022-2032, USD Million

- By Farm Size- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Egypt Agricultural Robots Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Units Sold in Thousand

- Market Segmentation & Growth Outlook

- By Robot Type- Market Insights and Forecast 2022-2032, USD Million

- By Offering- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Farming Environment- Market Insights and Forecast 2022-2032, USD Million

- By Farm Size- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Market Size & Growth Outlook

- Asia Pacific Agricultural Robots Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Units Sold in Thousand

- Market Segmentation & Growth Outlook

- By Robot Type- Market Insights and Forecast 2022-2032, USD Million

- By Offering- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Farming Environment- Market Insights and Forecast 2022-2032, USD Million

- By Farm Size- Market Insights and Forecast 2022-2032, USD Million

- By Country

- China

- India

- Japan

- South Korea

- Australia

- Indonesia

- Rest of Asia Pacific

- China Agricultural Robots Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Units Sold in Thousand

- Market Segmentation & Growth Outlook

- By Robot Type- Market Insights and Forecast 2022-2032, USD Million

- By Offering- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Farming Environment- Market Insights and Forecast 2022-2032, USD Million

- By Farm Size- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- India Agricultural Robots Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Units Sold in Thousand

- Market Segmentation & Growth Outlook

- By Robot Type- Market Insights and Forecast 2022-2032, USD Million

- By Offering- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Farming Environment- Market Insights and Forecast 2022-2032, USD Million

- By Farm Size- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Japan Agricultural Robots Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Units Sold in Thousand

- Market Segmentation & Growth Outlook

- By Robot Type- Market Insights and Forecast 2022-2032, USD Million

- By Offering- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Farming Environment- Market Insights and Forecast 2022-2032, USD Million

- By Farm Size- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- South Korea Agricultural Robots Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Units Sold in Thousand

- Market Segmentation & Growth Outlook

- By Robot Type- Market Insights and Forecast 2022-2032, USD Million

- By Offering- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Farming Environment- Market Insights and Forecast 2022-2032, USD Million

- By Farm Size- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Australia Agricultural Robots Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Units Sold in Thousand

- Market Segmentation & Growth Outlook

- By Robot Type- Market Insights and Forecast 2022-2032, USD Million

- By Offering- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Farming Environment- Market Insights and Forecast 2022-2032, USD Million

- By Farm Size- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Indonesia Agricultural Robots Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Units Sold in Thousand

- Market Segmentation & Growth Outlook

- By Robot Type- Market Insights and Forecast 2022-2032, USD Million

- By Offering- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Farming Environment- Market Insights and Forecast 2022-2032, USD Million

- By Farm Size- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- Deere & Company

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- SZ DJI Technology Co. Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Lely Group

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- DeLaval

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- CNH Industrial

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- GEA Group AG

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Kubota Corporation

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- XAG Co. Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Yanmar Holdings Co. Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Solinftec

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Carbon Robotics

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Ecorobotix SA

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- BouMatic Robotics

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Fullwood JOZ

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Naïo Technologies

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Deere & Company

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Robot Type |

|

| By Offering |

|

| By Application |

|

| By Farming Environment |

|

| By Farm Size |

|

| By Region |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.