US Ultrafiltration Market Report: Trends, Growth and Forecast (2026-2032)

By By Membrane Material (Polymeric Membranes, Polyvinylidene Fluoride, Polyethersulfone, Polysulfone, Polyacrylonitrile, Polyvinyl Chloride, Others, Ceramic Membranes), By By Module Type (Hollow Fiber, Tubular, Plate & Frame, Spiral Wound, Others), By By System Type (Pressurized Ultrafiltration Systems, Submerged Ultrafiltration Systems), By By Application (Municipal Water Treatment, Municipal Wastewater Treatment, Industrial Process Water Treatment, Wastewater Reuse & Recycling, Desalination Pre treatment, Food & Beverage Processing, Biopharmaceutical & Pharmaceutical Processing, Chemical & Petrochemical Processing, Others), By By End Use Industry (Municipal, Food & Beverage, Pharmaceutical & Biotechnology, Chemical & Petrochemical, Power Generation, Oil & Gas, Electronics & Semiconductor, Pulp & Paper, Textile, Others), By By Region (West, Midwest, South, North, Northeast) ... Read more

|

Major Players

|

US Ultrafiltration Market Statistics and Insights, 2026

- Market Size Statistics

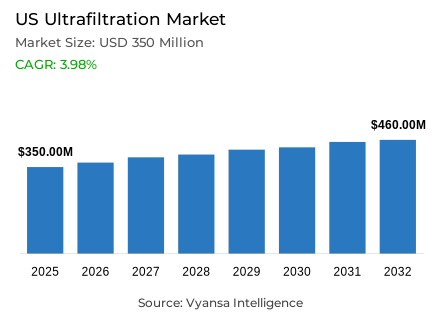

- Ultrafiltration market size in US was valued at USD 350 million in 2025 and is estimated at USD 364 million in 2026.

- The market size is expected to grow to USD 460 million by 2032.

- Market to register a CAGR of around 3.98% during 2026-32.

- Membrane Material Shares

- Polymeric membranes grabbed market share of 80%.

- Competition

- More than 10 companies are actively engaged in producing ultrafiltration in US.

- Top 5 companies acquired around 15% of the market share.

- Pentair X-Flow, Hydranautics / Nitto Group, MANN+HUMMEL Water & Membrane Solutions, DuPont Water Solutions, Veolia Water Technologies etc., are few of the top companies.

- Module Type

- Hollow fiber grabbed 60% of the market.

US Ultrafiltration Market Outlook

Valued at USD 350 million in 2025, the US ultrafiltration market is advancing from USD 364 million in 2026 toward USD 460 million by 2032, representing 3.98% compound annual growth rate throughout the forecast window. This steady expansion trajectory reflects consistent demand across key application areas, building gradually through forecast years. Market momentum remains underpinned by tighter drinking water regulation requiring advanced contaminant-removal systems, substantial federal funding supporting municipal water upgrades, and industry-wide shift toward water reuse and desalination-focused treatment innovation.

Tighter drinking water regulation and mandatory compliance requirements establish foundational market driver sustaining consistent demand for ultrafiltration systems throughout US municipal water utilities. Evidence from US Environmental Protection Agency reveals final PFAS drinking water rule is expected to reduce exposure for approximately 100 million people, with public water systems completing initial monitoring by 2027 and implementing solutions by 2029 if PFAS levels exceed established limits. This regulatory mandate directly translates into heightened market relevance for advanced treatment technologies including ultrafiltration-based process trains. Published data from US Environmental Protection Agency indicates additional USD 1 billion available through infrastructure investment and jobs act supporting states and territories implementing PFAS testing and treatment at public water systems and private well owners addressing contamination.

Water reuse expansion and desalination technology innovation reshape US ultrafiltration market toward multi-stage treatment applications supporting long-term water sustainability. Data from US Environmental Protection Agency indicates National Water Reuse Action Plan expanded from 37 actions to 73 action commitments by March 2025, establishing structured national water reuse framework. Published evidence from US Department of Energy reveals renewed funding of USD 75 million over five years for National Alliance for Water Innovation in 2024 advancing desalination and water reuse technologies. This innovation momentum supports market expansion for membrane-led water treatment solutions emphasizing lower-cost and energy-efficient purification systems.

Market segmentation demonstrates pronounced demand concentration within polymeric membrane materials and hollow fiber module designs supporting established treatment infrastructure. Polymeric membranes commands 80% market share through broad applicability across municipal and industrial treatment supporting practical deployment and commercial familiarity, while hollow fiber accounts for 60% of module demand reflecting alignment with recurring filtration needs and operational reliability. This US ultrafiltration market structure indicates utilities increasingly prioritize proven technologies and practical system choices supporting dependable long-term performance.

US Ultrafiltration Market Growth Driver

PFAS Compliance Keeps Treatment Demand Strong

Tighter drinking water regulation and mandatory contaminant removal requirements establish sustained demand for ultrafiltration systems throughout US municipal water treatment infrastructure. Statistics from US Environmental Protection Agency confirm final PFAS drinking water rule is expected to reduce exposure for approximately 100 million people, with public water systems completing initial monitoring by 2027 and implementing solutions by 2029 if PFAS levels exceed limits. This regulatory mandate directly translates into heightened market relevance for advanced treatment technologies including ultrafiltration-based process trains supporting compliance achievement. Regulatory structure ensures utilities remain dependent on professional ultrafiltration infrastructure supporting consistent compliance with mandated treatment timelines.

Federal funding availability and compliance support mechanisms strengthen commercial foundation for comprehensive ultrafiltration system deployment. Published data from US Environmental Protection Agency indicates additional USD 1 billion available through Infrastructure Investment and Jobs Act supporting states and territories implementing PFAS testing and treatment at public water systems and private well owners addressing contamination. This federal funding support directly improves project economics supporting accelerated ultrafiltration adoption across US municipal water systems. Compliance funding ensures sustained demand for professional ultrafiltration infrastructure supporting water quality improvement throughout extended forecast period.

US Ultrafiltration Market Challenge

Upgrade Costs Keep Adoption Decisions Tight

Ultrafiltration market faces substantial challenge from high infrastructure spending burden affecting technology adoption timeline and utility budget prioritization. Official records from US Environmental Protection Agency indicate drinking water systems in United States need USD 625 billion for pipe replacement, treatment plant upgrades, storage tanks, and other key assets ensuring safe drinking water. This substantial capital requirement makes technology adoption more difficult, especially where utilities must balance treatment priorities with broader system repair needs. Large infrastructure spending requirements create competitive pressures affecting ultrafiltration deployment timing and adoption pace.

Funding gap pressure and competing capital allocation demands intensify operating complexity for ultrafiltration market development. Evidence from US Environmental Protection Agency reveals Infrastructure Investment and Jobs Act delivers more than USD 50 billion to EPA for drinking water, wastewater, and stormwater infrastructure, establishing major commitment while demonstrating substantial capital pressure facing sector. For ultrafiltration suppliers, challenge extends beyond technical suitability to timing and affordability of full-system upgrades. Service providers must develop cost-effective solutions addressing budget constraints facing resource-limit

Unlock Market Intelligence

Explore the market potential with our data-driven report

US Ultrafiltration Market Trend

Water Reuse Innovation Is Moving to the Forefront

US ultrafiltration market demonstrates pronounced shift toward reuse and desalination-focused treatment innovation reshaping municipal water planning priorities. Market data from US Environmental Protection Agency indicates National Water Reuse Action Plan expanded from 37 actions to 73 action commitments by March 2025, establishing structured water reuse framework more firmly embedded in national water planning. This water reuse expansion directly supports ultrafiltration market growth through demand for pretreatment, water-quality stabilization, and broader system reliability support in multi-stage treatment setups. Reuse project expansion creates market opportunity for ultrafiltration providers developing pretreatment capabilities supporting reuse system integration.

Federal technology innovation programs and energy efficiency emphasis strengthen industry-wide desalination and reuse adoption momentum. Published data from US Department of Energy reveals renewed funding of USD 75 million over five years for National Alliance for Water Innovation in 2024 advancing desalination and water reuse technologies. This innovation emphasis keeps industry activity centered on lower-cost and more energy-efficient purification systems supporting wider commercial interest in membrane-led water treatment solutions. Technology innovation focus supports market expansion for ultrafiltration systems incorporating advanced efficiency features and integrated multi-stage treatment capabilities.

US Ultrafiltration Market Opportunity

Non-traditional Water Sources Open New White Space

Strong opportunities emerge in treatment and reuse of non-traditional water sources supporting water scarcity mitigation and beneficial reuse applications. Official records from US Geological Survey indicate oil and gas operations in United States produce four trillion liters of produced water annually, establishing very large treatment opportunity. This substantial non-traditional water source creates commercial opportunity especially in water-scarce areas where treated water can be reused for livestock, road maintenance, and other beneficial purposes. Ultrafiltration gains relevance through this shift because non-traditional water reuse requires stronger solids and contaminant management before final application.

Water reuse and desalination project pipeline expansion strengthens commercial foundation for ultrafiltration deployment. Evidence from US Bureau of Reclamation reveals 31 planning projects received USD 28.97 million in appropriated funding for potential new water reuse and desalination projects, supporting wider pipeline of facilities requiring membrane-based treatment stages. As reuse planning expands, ultrafiltration suppliers strengthen position in pretreatment design, pilot work, and full-scale project integration. Project funding support directly enables accelerated ultrafiltration adoption throughout US water treatment infrastructure modernization initiatives.

Unlock Market Intelligence

Explore the market potential with our data-driven report

US Ultrafiltration Market Segmentation Analysis

By Membrane Material

- Polymeric Membranes

- Polyvinylidene Fluoride

- Polyethersulfone

- Polysulfone

- Polyacrylonitrile

- Polyvinyl Chloride

- Others

- Ceramic Membranes

Polymeric membranes commands market leadership at 80% share within US ultrafiltration market, establishing dominant membrane-material positioning through broad applicability across municipal and industrial treatment applications. This market segment maintains leading position due to utility preference for materials supporting practical deployment, broader commercial use, and easier fit across diverse treatment applications, generating sustained demand for polymeric membrane solutions. Polymeric membrane solutions deliver accessible positioning supporting routine treatment deployment while maintaining adequate filtration performance across varied feedwater conditions, establishing broad appeal across municipal and industrial operators.

This market leadership position reflects utilities' continued selection of membrane materials supporting practical deployment and operational familiarity. Polymeric membranes remain important because they are widely associated with routine water and wastewater treatment needs across multiple end-use settings, offering balanced performance and scalable use. The 80% market share indicates this segment continues shaping material demand, production focus, and broader competitive direction throughout US ultrafiltration industry. Manufacturers maintaining polymeric membrane leadership develop competitive advantages enabling broader market penetration and sustained revenue growth supporting category expansion.

By Module Type

- Hollow Fiber

- Tubular

- Plate & Frame

- Spiral Wound

- Others

Hollow fiber commands market leadership at 60% share within US ultrafiltration market, establishing dominant module-type positioning through alignment with recurring filtration needs and dependable system performance across water treatment environments. This market segment maintains leading position due to utility preference for module formats supporting broad operational use and fit within established treatment layouts, generating sustained demand for hollow fiber solutions. Hollow fiber solutions deliver accessible positioning supporting routine treatment deployment while maintaining adequate filtration performance across varied applications, establishing broad appeal across municipal and industrial operators.

This market leadership position reflects utilities' continued selection of module types supporting operational reliability and system familiarity. Hollow fiber remains important because it supports widespread use across water treatment environments where consistent filtration and operational familiarity matter, providing dependable performance across recurring filtration needs. The 60% market share indicates this segment continues influencing module selection, installation patterns, and broader demand structure throughout US ultrafiltration industry. Manufacturers maintaining hollow fiber module leadership develop competitive advantages enabling customer retention and sustained market growth supporting category expansion throughout extended forecast period.

List of Companies Covered in US Ultrafiltration Market

The companies listed below are highly influential in the US ultrafiltration market, with a significant market share and a strong impact on industry developments.

- Pentair X-Flow

- Hydranautics / Nitto Group

- MANN+HUMMEL Water & Membrane Solutions

- DuPont Water Solutions

- Veolia Water Technologies

- Pall Corporation

- Toray Membrane USA

- Kovalus Separation Solutions

- Synder Filtration

- Alfa Laval

Market News & Updates

- DuPont Water Solutions, 2026:

DuPont Water Solutions launched Inge™ ultrafiltration modules with integrated pre-filter technology in April 2026, positioning the update as a space-saving and cost-efficient solution for drinking water and seawater applications. The product combines pre-filtration and ultrafiltration inside one module housing, reducing the need for separate upstream pre-filtration infrastructure and supporting lower plant footprint, capital cost, and operating complexity. For the US ultrafiltration market, this strengthens demand for compact UF systems across municipal water treatment, desalination pre-treatment, containerized plants, and industrial water users, including microelectronics facilities. Its ability to maintain existing membrane materials, dimensions, and drinking-water certifications also supports retrofit and expansion opportunities without major redesign. The launch is strategically significant because US utilities and industrial users increasingly need resilient systems that handle feedwater variability while improving pathogen removal and permeate consistency.

- Veolia Water Technologies, 2025:

Veolia Water Technologies secured a major US semiconductor water-management contract in 2025, covering the design, construction, and 16-year operation of a state-of-the-art water and wastewater treatment facility for a semiconductor manufacturing plant in the Midwest. The official update states that the project uses latest-generation ultrafiltration and reverse osmosis membrane technologies, including ZeeWeed™ hollow-fiber membranes, and can recycle around 8,000 cubic meters, or 2.1 million gallons, of water per day. This is a significant US ultrafiltration market development because semiconductor manufacturing requires high-purity water, reliable wastewater recycling, and advanced membrane-based treatment capacity. The contract also links UF adoption with reshoring and expansion of domestic semiconductor production, strengthening industrial demand beyond traditional municipal applications. Its long operating period further supports recurring service demand, technology validation, and higher confidence in UF-led water reuse systems for advanced manufacturing.

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- US Ultrafiltration Market Policies, Regulations, and Standards

- US Ultrafiltration Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- US Ultrafiltration Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Membrane Material

- Polymeric Membranes- Market Insights and Forecast 2022-2032, USD Million

- Polyvinylidene Fluoride- Market Insights and Forecast 2022-2032, USD Million

- Polyethersulfone- Market Insights and Forecast 2022-2032, USD Million

- Polysulfone- Market Insights and Forecast 2022-2032, USD Million

- Polyacrylonitrile- Market Insights and Forecast 2022-2032, USD Million

- Polyvinyl Chloride- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- Ceramic Membranes- Market Insights and Forecast 2022-2032, USD Million

- By Module Type

- Hollow Fiber- Market Insights and Forecast 2022-2032, USD Million

- Tubular- Market Insights and Forecast 2022-2032, USD Million

- Plate & Frame- Market Insights and Forecast 2022-2032, USD Million

- Spiral Wound- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By System Type

- Pressurized Ultrafiltration Systems- Market Insights and Forecast 2022-2032, USD Million

- Submerged Ultrafiltration Systems- Market Insights and Forecast 2022-2032, USD Million

- By Application

- Municipal Water Treatment- Market Insights and Forecast 2022-2032, USD Million

- Municipal Wastewater Treatment- Market Insights and Forecast 2022-2032, USD Million

- Industrial Process Water Treatment- Market Insights and Forecast 2022-2032, USD Million

- Wastewater Reuse & Recycling- Market Insights and Forecast 2022-2032, USD Million

- Desalination Pre treatment- Market Insights and Forecast 2022-2032, USD Million

- Food & Beverage Processing- Market Insights and Forecast 2022-2032, USD Million

- Biopharmaceutical & Pharmaceutical Processing- Market Insights and Forecast 2022-2032, USD Million

- Chemical & Petrochemical Processing- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By End Use Industry

- Municipal- Market Insights and Forecast 2022-2032, USD Million

- Food & Beverage- Market Insights and Forecast 2022-2032, USD Million

- Pharmaceutical & Biotechnology- Market Insights and Forecast 2022-2032, USD Million

- Chemical & Petrochemical- Market Insights and Forecast 2022-2032, USD Million

- Power Generation- Market Insights and Forecast 2022-2032, USD Million

- Oil & Gas- Market Insights and Forecast 2022-2032, USD Million

- Electronics & Semiconductor- Market Insights and Forecast 2022-2032, USD Million

- Pulp & Paper- Market Insights and Forecast 2022-2032, USD Million

- Textile- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By Region

- West- Market Insights and Forecast 2022-2032, USD Million

- Midwest- Market Insights and Forecast 2022-2032, USD Million

- South- Market Insights and Forecast 2022-2032, USD Million

- North- Market Insights and Forecast 2022-2032, USD Million

- Northeast- Market Insights and Forecast 2022-2032, USD Million

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Membrane Material

- Market Size & Growth Outlook

- US Polymeric Membranes Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Module Type- Market Insights and Forecast 2022-2032, USD Million

- By System Type- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By End Use Industry- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- US Ceramic Membranes Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Module Type- Market Insights and Forecast 2022-2032, USD Million

- By System Type- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By End Use Industry- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- DuPont Water Solutions

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Veolia Water Technologies

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Pall Corporation

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Toray Membrane USA

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Kovalus Separation Solutions

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Pentair X-Flow

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Hydranautics / Nitto Group

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- MANN+HUMMEL Water & Membrane Solutions

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Synder Filtration

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Alfa Laval

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- DuPont Water Solutions

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Membrane Material |

|

| By Module Type |

|

| By System Type |

|

| By Application |

|

| By End Use Industry |

|

| By Region |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.