Ukraine Bags and Luggage Market Report: Trends, Growth and Forecast (2026-2032)

By Category (Bags (Cross Body Bags, Bags and Backpacks, Business Bags, Duffle Bags, Clutches, Others), Luggage (Soft Luggage, Hard Luggage, Wheeled Luggage, Non-Wheeled Luggage)), By Sales Channel (Retail Offline, Retail Online), By Material Type (Soft Case (Nylon, Polyester, Ballistic Nylon), Hard Case (Polycarbonate, ABS (Acrylonitrile Butadiene Styrene), Polypropylene)), By Price Category (Luxury, Mass/Economy, Premium), By Application (Travel, Business) ... Read more

|

Major Players

|

Ukraine Bags and Luggage Market Statistics and Insights, 2026

- Market Size Statistics

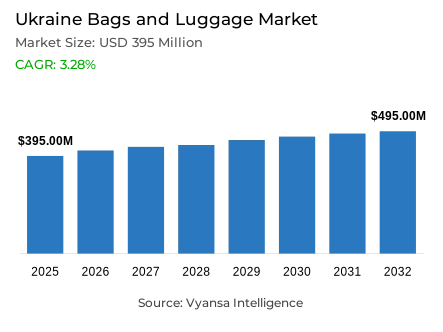

- Bags and luggage market size in Ukraine was estimated at USD 395 million in 2025.

- The market size is expected to grow to USD 495 million by 2032.

- Market to register a CAGR of around 3.28% during 2026-32.

- Category Shares

- Bags grabbed market share of 90%.

- Competition

- More than 20 companies are actively engaged in producing bags and luggage in Ukraine.

- Top 5 companies acquired around 5% of the market share.

- LPP Ukraine DP, GangZhou Dengji Travel Gear Co Ltd, Mezhybovskyi O S SPD, Puma Ukraina TOV, MTI TOV etc., are few of the top companies.

- Sales Channel

- Retail offline grabbed 85% of the market.

Ukraine Bags and Luggage Market Outlook

The Ukraine bags and luggage market operates within a complex environment shaped by demographic shifts and economic recovery efforts. Although ongoing conflict has weighed on end user confidence and disposable incomes, interest in personal style remains a foundational driver of long-term demand. As conditions stabilise, the market is expected to recover gradually, reaching USD 395 million in 2025 and USD 495 million by 2032, with a CAGR of approximately 3.28% during 2026-32.

Current end user preferences are defined by necessity and cost efficiency. Artificial leather and textile materials are increasingly favoured as affordable alternatives to traditional leather. Duffel bags and non-luxury handbags perform relatively well, supported by practical use cases and casual dress norms. Demand, particularly among women who view bags as essential style items, is likely to support diversification in shapes and colours as economic conditions improve.

Sustainability is emerging as a longer-term opportunity, with brands gradually introducing recyclable materials to align with global trends while maintaining affordability. Local designers are gaining visibility through social media, while the return of international players such as Inditex signals renewed competitive intensity. Together, these factors are expected to sustain end user interest despite demographic pressures.

Omnichannel strategies are increasingly interconnected, yet offline retail remains dominant, accounting for 85% of market sales. Ukrainian end users remain highly tactile, preferring to physically inspect products before purchase. Apparel and footwear specialists therefore continue to play a central role, supporting market recovery toward its projected USD 495 million value by 2032.

Ukraine Bags and Luggage Market Growth DriverMobility Needs Keep Practical Bags in Demand

Large-scale displacement continues to make bags and luggage an essential necessity rather than a fashion accessory. As of October 2025, the UNHCR Regional Bureau for Europe documents 5,310,800 Ukrainian refugees in Europe and 3.7 million internally displaced persons within the country. Frequent movement between cities, temporary accommodation, and cross-border travel increases demand for durable duffel bags, backpacks, and small organisers that can support both travel and everyday use.

At the same time, end users retain effective channels to acquire these products. Cashless payments now dominate card usage: in 2024, 94.6% of payment-card transactions were cashless, while online payments for goods and services accounted for 13.6% of cashless card transactions. This enables quick purchasing and replacement via retail online and chain stores, even when access to physical retail is uneven.

Ukraine Bags and Luggage Market ChallengeTight Household Budgets Limit Non‑Essential Upgrades

Households continue to prioritise food, utilities, and safety over discretionary accessories. Inflation stood at 12.0% year on year in December 2024, while core inflation reached 10.7%, reflecting broad-based price pressure. Using the real subsistence minimum threshold, the World Bank estimates the poverty rate at 37.0% in 2024. Under these conditions, promotions and discounts become critical, while end users delay replacement of handbags and luggage or switch to lower-cost materials.

Demand is further shaped by demographic pressures. UNHCR documents 5,310,800 Ukrainian refugees in Europe and estimates 3.7 million internally displaced persons within Ukraine. This smaller, more mobile end user base concentrates demand unevenly across cities, making it difficult to rely on stable footfall to support specialist retail formats.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Ukraine Bags and Luggage Market TrendOnline-First Shopping and Cashless Payments Gain Ground

Bags are increasingly purchased online, supported by widespread digital payment adoption. According to the National Bank of Ukraine, cashless transactions accounted for 94.6% of all payment-card transactions by volume in 2024, while online payments for goods and services represented 13.6% of cashless transactions, totalling UAH 622 billion. During the same year, the number of payment terminals rose by 10.5% to 496,600, enabling omnichannel retailers to serve both in-store and online demand.

App-based behaviour is also becoming standardised through digital public services. Government data report over 22 million users and 5.8 million active users of the Diia platform. This environment supports social commerce, rapid price comparison, and demand for affordable, casual bags over formal, occasion-driven purchases.

Ukraine Bags and Luggage Market OpportunityWider Digital Reach Enables Brands to Scale Beyond Major Cities

The retail payment network continues to expand despite disruption. According to the National Bank of Ukraine, 518,400 sales and service outlets accepted payment cards in 2024, an increase of 12.8% year on year, while active payment cards reached 58.8 million as of 1 January 2025. This supports wider distribution through chains and marketplaces and enables loyalty and cashback programmes that encourage repeat purchases beyond major urban centres.

Cross-border demand also remains significant. UNHCR records 5,310,800 Ukrainian refugees in Europe (October 2025), creating a large diaspora that frequently orders goods online and sends necessities to family members. With 60% of active cards contactless in 2024, brands can offer fast checkout experiences and parcel-friendly collections suited to mobile lifestyles.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Ukraine Bags and Luggage Market Segmentation Analysis

By Category

- Bags

- Cross Body Bags

- Bags and Backpacks

- Business Bags

- Duffle Bags

- Clutches

- Others

- Luggage

- Soft Luggage

- Hard Luggage

- Wheeled Luggage

- Non-Wheeled Luggage

The segment with highest market share under category is Bags represent the dominant category in the Ukraine market, accounting for approximately 90% of total value. This leadership reflects the cultural importance of bags as elements of personal image and everyday functionality. Even under economic constraints, non-luxury handbags and casual formats such as backpacks remain essential due to their practicality. The shift toward artificial leather and textile materials has helped maintain accessibility for a broad end user base during the recovery phase.

The growth of small local designers and the re-entry of global brands such as Zara have expanded product variety within the segment. As mobility increases and daily routines normalise, smaller and more dynamic bag styles are expected to show the strongest momentum. The segment’s high share underscores resilient demand that combines functional necessity with enduring fashion relevance.

By Sales Channel

- Retail Offline

- Retail Online

Retail offline remains the leading sales channel, accounting for 85% of the Ukraine bags and luggage market. Despite the convenience and expanding assortment offered by retail online, physical retail continues to play a critical role in purchase decisions. end users place strong value on the ability to touch, assess materials, and evaluate construction before buying, reinforcing the importance of branded chains and apparel specialists.

Although omnichannel strategies are expanding digital reach, offline shopping retains strong appeal, particularly for end users seeking coordinated, trend-driven looks in a single visit. Apparel and footwear specialists remain key destinations, offering curated selections of multinational brands alongside clothing. This immersive in-store experience is expected to sustain offline retail’s dominance through the forecast period ending in 2032.

List of Companies Covered in Ukraine Bags and Luggage Market

The companies listed below are highly influential in the Ukraine bags and luggage market, with a significant market share and a strong impact on industry developments.

- LPP Ukraine DP

- GangZhou Dengji Travel Gear Co Ltd

- Mezhybovskyi O S SPD

- Puma Ukraina TOV

- MTI TOV

- Robinzon Ukraine TOV

- Zara Ukraina TOV

- BNS Trade TOV

- adidas Ukraine DP

- Ultra Group

Competitive Landscape

Ukraine bags and luggage market remained highly fragmented, shaped by economic pressure, shifting demand toward affordability, and the growing role of digital channels. Puma Ukraina TOV retained its leading position despite holding only a small retail value share, supported by strong demand for sports-inspired and casual bags aligned with everyday wear. MTI TOV, through its Intertop chain, continued to play a key role by offering a mix of international brands and private labels at accessible price points. The return of Inditex, with Zara re-entering the market, strengthened competition in trend-led, affordable handbags. At the same time, small local designers such as Kachorovska and Bagllet gained visibility via social media, reflecting rising interest in locally made, competitively priced designs.

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- Ukraine Bags and Luggage Market Policies, Regulations, and Standards

- Ukraine Bags and Luggage Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- Ukraine Bags and Luggage Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Units Sold in Thousand Units

- Market Segmentation & Growth Outlook

- By Category

- Bags- Market Insights and Forecast 2022-2032, USD Million

- Cross Body Bags- Market Insights and Forecast 2022-2032, USD Million

- Bags and Backpacks- Market Insights and Forecast 2022-2032, USD Million

- Business Bags- Market Insights and Forecast 2022-2032, USD Million

- Duffle Bags- Market Insights and Forecast 2022-2032, USD Million

- Clutches- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- Luggage- Market Insights and Forecast 2022-2032, USD Million

- Soft Luggage- Market Insights and Forecast 2022-2032, USD Million

- Hard Luggage- Market Insights and Forecast 2022-2032, USD Million

- Wheeled Luggage- Market Insights and Forecast 2022-2032, USD Million

- Non-Wheeled Luggage- Market Insights and Forecast 2022-2032, USD Million

- Bags- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel

- Retail Offline- Market Insights and Forecast 2022-2032, USD Million

- Retail Online- Market Insights and Forecast 2022-2032, USD Million

- By Material Type

- Soft Case- Market Insights and Forecast 2022-2032, USD Million

- Nylon- Market Insights and Forecast 2022-2032, USD Million

- Polyester- Market Insights and Forecast 2022-2032, USD Million

- Ballistic Nylon- Market Insights and Forecast 2022-2032, USD Million

- Hard Case- Market Insights and Forecast 2022-2032, USD Million

- Polycarbonate- Market Insights and Forecast 2022-2032, USD Million

- ABS (Acrylonitrile Butadiene Styrene)- Market Insights and Forecast 2022-2032, USD Million

- Polypropylene- Market Insights and Forecast 2022-2032, USD Million

- Soft Case- Market Insights and Forecast 2022-2032, USD Million

- By Price Category

- Luxury- Market Insights and Forecast 2022-2032, USD Million

- Mass/Economy- Market Insights and Forecast 2022-2032, USD Million

- Premium- Market Insights and Forecast 2022-2032, USD Million

- By Application

- Travel- Market Insights and Forecast 2022-2032, USD Million

- Business- Market Insights and Forecast 2022-2032, USD Million

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Category

- Market Size & Growth Outlook

- Ukraine Bags Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Units Sold in Thousand Units

- Market Segmentation & Growth Outlook

- By Category- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Material Type- Market Insights and Forecast 2022-2032, USD Million

- By Price Category- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Ukraine Luggage Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Units Sold in Thousand Units

- Market Segmentation & Growth Outlook

- By Category- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Material Type- Market Insights and Forecast 2022-2032, USD Million

- By Price Category- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- Puma Ukraina TOV

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- MTI TOV

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Robinzon Ukraine TOV

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Zara Ukraina TOV

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- BNS Trade TOV

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- LPP Ukraine DP

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- GangZhou Dengji Travel Gear Co Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Mezhybovskyi O S SPD

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- adidas Ukraine DP

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Ultra Group

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Puma Ukraina TOV

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Category |

|

| By Sales Channel |

|

| By Material Type |

|

| By Price Category |

|

| By Application |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.