UK Premium Beauty and Personal Care Market Report: Trends, Growth and Forecast (2025-2030)

By Product (Colour Cosmetics, Fragrances, Deodorants, Hair Care, Skin Care, Bath and Shower, Baby and Child-specific Products), By End User (Men’s, Women’s, Unisex), By Sales Channel (Online, Offline) ... Read more

|

Major Players

|

UK Premium Beauty and Personal Care Market Statistics, 2025

- Market Size Statistics

- Premium Beauty and Personal Care in UK is estimated at $ 8.96 Billion.

- The market size is expected to grow to $ 11 Billion by 2030.

- Market to register a CAGR of around 3.48% during 2025-30.

- Product Shares

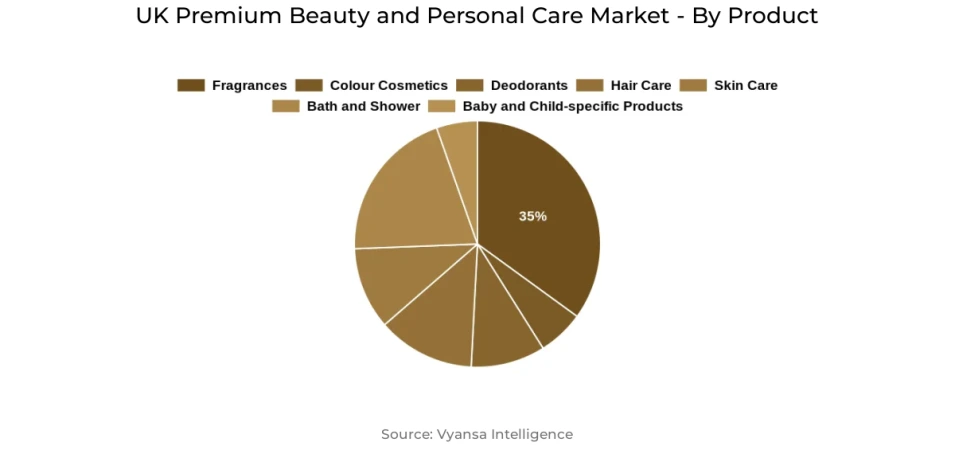

- Premium Fragrances grabbed market share of 35%.

- Competition

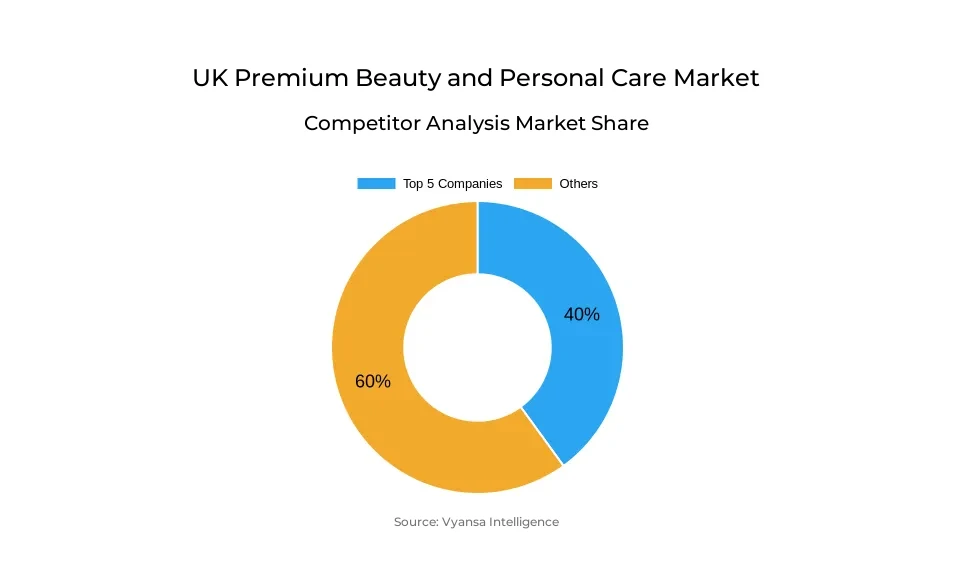

- More than 20 companies are actively engaged in producing Premium Beauty and Personal Care in UK.

- Top 5 companies acquired 40% of the market share.

- Chanel Ltd, L'Occitane Ltd, Christian Dior (UK) Ltd, Estée Lauder Cosmetics Ltd, L'Oréal (UK) Ltd etc., are few of the top companies.

UK Premium Beauty and Personal Care Market Outlook

UK premium beauty and personal care market will continue to grow steadily between 2025 and 2030, led by demand for indulgence and experimentation, particularly as economic constraints start to ease. While core categories such as bath and shower or deodorants have experienced a migration to more value-priced alternatives, consumers are prepared to pay for prestige products that provide a perception of luxury, especially in skin care, color cosmetics, and fragrance. Premium fragrance will continue to be the largest and the fastest-growing category, boosted by the popularity of niche and intensely concentrated fragrances, and the sustained growth of the "fragrance wardrobe" phenomenon.

Social media platforms such as Instagram and TikTok will continue to influence consumer decisions, driving the fast growth of celebrity and indie brands. Younger generations are becoming more attracted to premium body mists because they are affordable, versatile, and tied to retro Y2K trends. This segment will be the most dynamic within the forecast period, with the likes of Sol de Janeiro heading the pack and inspiring others to access this fast-growing segment.

Trends like "quiet luxury" and cosmetic minimalism will shape marketing approaches, with increased consumer emphasis on product quality, efficacy, and understated sophistication over aggressive branding. This aligns with the success of unisex and understated luxury brands, as consumers increasingly value self-care and authenticity.

Lastly, personalisation will be a driving force for innovation. Developments in AI will make it possible for brands to provide bespoke solutions, delivering more consumer satisfaction and experience. But the emergence of home-use devices with salon quality might challenge traditional premium products, forcing brands to innovate even more to satisfy the need for high-performance, personalised beauty products.

UK Premium Beauty and Personal Care Market Challenge

Heritage brands are under increasing pressure to remain current as UK consumers trend towards more creative and individual beauty options. Estée Lauder Cosmetics Ltd, with its portfolio of iconic brands including Clinique, Estée Lauder, and MAC, lost market share in 2024. The classic appeal of these brands is undermined by increasing demand for novelty and individuality. But Jo Malone, yet another Estée Lauder company, has been well-suited to the transition with its unisex perfume lines that go along with current sensibilities regarding freedom of scent expression.

Concurrently, competition is mounting as agile players such as L'Oréal keep expanding their lead. Its portfolio of diverse brands enables rapid response to changing needs. Redken's stellar performance, fueled by consumer desire for professional hair care and preventive treatment, testifies to this trend. L'Oréal's purchase of Aesop also reinforced its hold in premium shower and bath categories that are being increasingly perceived as indulgence moments.

UK Premium Beauty and Personal Care Market Trend

Over the next few years, "quiet luxury" will powerfully dominate consumer decisioning throughout the UK premium beauty and personal care landscape. This movement is centered on subtle sophistication and advanced results over loud packaging or recognizable name recognition. Consumers are increasingly interested in products that give center stage to ingredients, fragrance, and performance. The perfume category is a prime example of this, with companies such as Le Labo, Byredo, and Jo Malone becoming more popular for their minimalist, unisex appeal.

As this trend continues, additional categories will also follow. It has already begun to show a trend towards cosmetic minimalism, with consumers increasingly favoring natural appearance compared to heavy makeup. Rather than trying to conceal imperfections, they are preferring products that promote skin health and texture. This change demonstrates a greater preference for authenticity, practicality, and self-care, all in keeping with the broader trend towards mindful beauty practice.

Unlock Market Intelligence

Explore the market potential with our data-driven report

UK Premium Beauty and Personal Care Market Opportunity

Personalisation will be fueling innovation in the UK premium beauty and personal care industry between 2025-30. Increasing awareness of sustainability and tight purse strings mean consumers are increasingly seeking easier routines and products which are matched to their individual needs. In response, demand is changing towards personalised solutions that are highly effective without excess use. Technology advances in AI are making this possible, with bespoke formulations and diagnostics for individual consumers.

For example, Coty's collaboration with technology company Perfect Corp has enhanced its digital platform by providing AI-driven facial analysis to suggest appropriate products. This is also part of a wider trend where consumers are banking on technology-enabled solutions. But while this creates opportunities for high-end brands, it also brings in competition from consumer electronics companies providing salon-quality equipment for home use—capturing the attention of customers who want high-performance results with scientific validation.

| Report Coverage | Details |

|---|---|

| Market Forecast | 2025-30 |

| USD Value 2024 | $ 8.96 Billion |

| USD Value 2030 | $ 11 Billion |

| CAGR 2025-2030 | 3.48% |

| Largest Category | Premium Fragrances segment leads with 35% market share |

| Top Challenges | Struggles of Heritage Brands Amid Shifting Consumer Preferences Hindering Market Growth |

| Top Trends | Growing Traction Towards Quiet Luxury to Shape Consumer Preferences |

| Top Opportunities | Rising Demand for Personalised and Tech-Driven Beauty Solutions |

| Key Players | Chanel Ltd, L'Occitane Ltd, Christian Dior (UK) Ltd, Estée Lauder Cosmetics Ltd, L'Oréal (UK) Ltd, Coty UK Ltd, Puig UK Ltd, Clarins UK Ltd, Parfums Elemis Ltd, Charlotte Tilbury Beauty Ltd and Others. |

Unlock Market Intelligence

Explore the market potential with our data-driven report

UK Premium Beauty and Personal Care Market Segmentation

The leading segment of the UK Premium Beauty and Personal Care Market in 2024 was premium fragrances. The category registered high value and volume growth due to consumers' preference for novel fragrances and a move toward intensively concentrated, more expensive products. Indie brands picked up popularity, with the trend for uniqueness in fragrance preferences. The "fragrance wardrobe" trend also played a role, with consumers opting for varying fragrances depending on mood or occasion, promoting demand for smaller sizes.

In prestige fragrances, body mists are set to be the most innovative and growing subcategory during the forecast period (2025–30). Their popularity is increasing because they are light and wearable, with a lower price point compared to traditional eau de parfums, and are thus appealing to younger buyers. Their everyday use and ability to be reapplied have contributed to their popularity. The trend is also driven by the revival Y2K movement that has been popularized on social media and the popularity of cult brand Sol de Janeiro.

Top Companies in UK Premium Beauty and Personal Care Market

The top companies operating in the market include Chanel Ltd, L'Occitane Ltd, Christian Dior (UK) Ltd, Estée Lauder Cosmetics Ltd, L'Oréal (UK) Ltd, Coty UK Ltd, Puig UK Ltd, Clarins UK Ltd, Parfums Elemis Ltd, Charlotte Tilbury Beauty Ltd, etc., are the top players operating in the UK Premium Beauty and Personal Care Market.

Frequently Asked Questions

Related Report

1. Market Segmentation

1.1. Research Scope

1.2. Research Methodology

1.3. Definitions and Assumptions

2. Executive Summary

3. UK Premium Beauty and Personal Care Market Policies, Regulations, and Standards

4. UK Premium Beauty and Personal Care Market Dynamics

4.1. Growth Factors

4.2. Challenges

4.3. Trends

4.4. Opportunities

5. UK Premium Beauty and Personal Care Market Statistics, 2020-2030F

5.1. Market Size & Growth Outlook

5.1.1.By Revenues in US$ Million

5.2. Market Segmentation & Growth Outlook

5.2.1.By Product

5.2.1.1. Colour Cosmetics- Market Insights and Forecast 2020-2030, USD Million

5.2.1.1.1. Eye Make-Up- Market Insights and Forecast 2020-2030, USD Million

5.2.1.1.2. Facial Make-Up- Market Insights and Forecast 2020-2030, USD Million

5.2.1.1.3. Lip Products- Market Insights and Forecast 2020-2030, USD Million

5.2.1.1.4. Nail Products- Market Insights and Forecast 2020-2030, USD Million

5.2.1.1.5. Colour Cosmetics Sets/Kits- Market Insights and Forecast 2020-2030, USD Million

5.2.1.2. Fragrances- Market Insights and Forecast 2020-2030, USD Million

5.2.1.3. Deodorants- Market Insights and Forecast 2020-2030, USD Million

5.2.1.4. Hair Care- Market Insights and Forecast 2020-2030, USD Million

5.2.1.5. Skin Care- Market Insights and Forecast 2020-2030, USD Million

5.2.1.5.1. Body Care- Market Insights and Forecast 2020-2030, USD Million

5.2.1.5.2. Facial Care- Market Insights and Forecast 2020-2030, USD Million

5.2.1.5.3. Hand Care- Market Insights and Forecast 2020-2030, USD Million

5.2.1.5.4. Skin Care Sets/Kits- Market Insights and Forecast 2020-2030, USD Million

5.2.1.5.5. Sun Protection- Market Insights and Forecast 2020-2030, USD Million

5.2.1.5.6. Self-Tanning- Market Insights and Forecast 2020-2030, USD Million

5.2.1.6. Bath and Shower- Market Insights and Forecast 2020-2030, USD Million

5.2.1.7. Baby and Child-specific Products- Market Insights and Forecast 2020-2030, USD Million

5.2.2.By End User

5.2.2.1. Men’s- Market Insights and Forecast 2020-2030, USD Million

5.2.2.2. Women’s- Market Insights and Forecast 2020-2030, USD Million

5.2.2.3. Unisex- Market Insights and Forecast 2020-2030, USD Million

5.2.3.By Sales Channel

5.2.3.1. Online- Market Insights and Forecast 2020-2030, USD Million

5.2.3.2. Offline- Market Insights and Forecast 2020-2030, USD Million

5.2.4.By Competitors

5.2.4.1. Competition Characteristics

5.2.4.2. Market Share & Analysis

6. UK Premium Colour Cosmetics Market Outlook, 2020-2030F

6.1. Market Size & Growth Outlook

6.1.1.By Revenues in US$ Million

6.2. Market Segmentation & Growth Outlook

6.2.1.By Product- Market Insights and Forecast 2020-2030, USD Million

6.2.2.By End User- Market Insights and Forecast 2020-2030, USD Million

6.2.3.By Sales Channel- Market Insights and Forecast 2020-2030, USD Million

7. UK Premium Fragrances Market Outlook, 2020-2030F

7.1. Market Size & Growth Outlook

7.1.1.By Revenues in US$ Million

7.2. Market Segmentation & Growth Outlook

7.2.1.By End User- Market Insights and Forecast 2020-2030, USD Million

7.2.2.By Sales Channel- Market Insights and Forecast 2020-2030, USD Million

8. UK Premium Deodorants Market Outlook, 2020-2030F

8.1. Market Size & Growth Outlook

8.1.1.By Revenues in US$ Million

8.2. Market Segmentation & Growth Outlook

8.2.1.By End User- Market Insights and Forecast 2020-2030, USD Million

8.2.2.By Sales Channel- Market Insights and Forecast 2020-2030, USD Million

9. UK Premium Hair Care Market Outlook, 2020-2030F

9.1. Market Size & Growth Outlook

9.1.1.By Revenues in US$ Million

9.2. Market Segmentation & Growth Outlook

9.2.1.By End User- Market Insights and Forecast 2020-2030, USD Million

9.2.2.By Sales Channel- Market Insights and Forecast 2020-2030, USD Million

10. UK Premium Skin Care Market Outlook, 2020-2030F

10.1. Market Size & Growth Outlook

10.1.1. By Revenues in US$ Million

10.2. Market Segmentation & Growth Outlook

10.2.1. By Product- Market Insights and Forecast 2020-2030, USD Million

10.2.2. By End User- Market Insights and Forecast 2020-2030, USD Million

10.2.3. By Sales Channel- Market Insights and Forecast 2020-2030, USD Million

11. UK Premium Bath and Shower Market Outlook, 2020-2030F

11.1. Market Size & Growth Outlook

11.1.1. By Revenues in US$ Million

11.2. Market Segmentation & Growth Outlook

11.2.1. By End User- Market Insights and Forecast 2020-2030, USD Million

11.2.2. By Sales Channel- Market Insights and Forecast 2020-2030, USD Million

12. UK Premium Baby and Child-specific Products Market Outlook, 2020-2030F

12.1. Market Size & Growth Outlook

12.1.1. By Revenues in US$ Million

12.2. Market Segmentation & Growth Outlook

12.2.1. By Sales Channel- Market Insights and Forecast 2020-2030, USD Million

13. Competitive Outlook

13.1. Company Profiles

13.1.1. Estée Lauder Cosmetics Ltd

13.1.1.1. Business Description

13.1.1.2. Product Portfolio

13.1.1.3. Collaborations & Alliances

13.1.1.4. Recent Developments

13.1.1.5. Financial Details

13.1.1.6. Others

13.1.2. L'Oréal (UK) Ltd

13.1.2.1. Business Description

13.1.2.2. Product Portfolio

13.1.2.3. Collaborations & Alliances

13.1.2.4. Recent Developments

13.1.2.5. Financial Details

13.1.2.6. Others

13.1.3. Coty UK Ltd

13.1.3.1. Business Description

13.1.3.2. Product Portfolio

13.1.3.3. Collaborations & Alliances

13.1.3.4. Recent Developments

13.1.3.5. Financial Details

13.1.3.6. Others

13.1.4. Puig UK Ltd

13.1.4.1. Business Description

13.1.4.2. Product Portfolio

13.1.4.3. Collaborations & Alliances

13.1.4.4. Recent Developments

13.1.4.5. Financial Details

13.1.4.6. Others

13.1.5. Clarins UK Ltd

13.1.5.1. Business Description

13.1.5.2. Product Portfolio

13.1.5.3. Collaborations & Alliances

13.1.5.4. Recent Developments

13.1.5.5. Financial Details

13.1.5.6. Others

13.1.6. Chanel Ltd

13.1.6.1. Business Description

13.1.6.2. Product Portfolio

13.1.6.3. Collaborations & Alliances

13.1.6.4. Recent Developments

13.1.6.5. Financial Details

13.1.6.6. Others

13.1.7. L'Occitane Ltd

13.1.7.1. Business Description

13.1.7.2. Product Portfolio

13.1.7.3. Collaborations & Alliances

13.1.7.4. Recent Developments

13.1.7.5. Financial Details

13.1.7.6. Others

13.1.8. Christian Dior (UK) Ltd

13.1.8.1. Business Description

13.1.8.2. Product Portfolio

13.1.8.3. Collaborations & Alliances

13.1.8.4. Recent Developments

13.1.8.5. Financial Details

13.1.8.6. Others

13.1.9. Elemis Ltd

13.1.9.1. Business Description

13.1.9.2. Product Portfolio

13.1.9.3. Collaborations & Alliances

13.1.9.4. Recent Developments

13.1.9.5. Financial Details

13.1.9.6. Others

13.1.10. Charlotte Tilbury Beauty Ltd

13.1.10.1. Business Description

13.1.10.2. Product Portfolio

13.1.10.3. Collaborations & Alliances

13.1.10.4. Recent Developments

13.1.10.5. Financial Details

13.1.10.6. Others

14. Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Product |

|

| By End User |

|

| By Sales Channel |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.