India Hair Oil Market Report: Trends, Growth and Forecast (2026-2032)

By Product Type (Coconut Oil, Almond Oil, Argan Oil, Olive Oil, Castor Oil, Amla/Herbal Oil, Others), By Category (Non-Medicated Hair Oil, Medicated Hair Oil), By Formulation (Conventional/Synthetic, Herbal/Ayurvedic, Organic/Natural), By Application (Hair Nourishment, Hair Damage Repair, Hair Growth Support, Scalp Care, Styling & Frizz Control), By End User (Individual/Household, Commercial/Salon & Spa), By Sales Channel (Retail Online (E-commerce Platforms, Brand-Owned Websites, Online Beauty & Personal Care Stores), Retail Offline (Supermarkets & Hypermarkets, Pharmacies/Drug Stores, Specialty Beauty Stores, Convenience Stores, Department Stores, Others)), By Region (North, East, West, South) ... Read more

|

Major Players

|

India Hair Oil Market Statistics and Insights, 2026

- Market Size Statistics

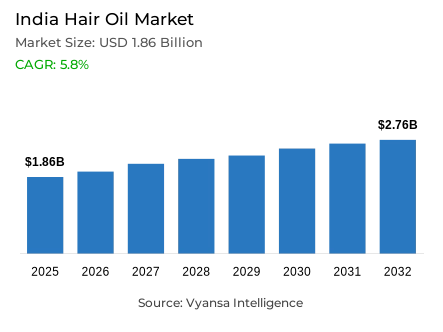

- Hair oil market size in India was valued at USD 1.86 billion in 2025 and is estimated at USD 1.97 billion in 2026.

- The market size is expected to grow to USD 2.76 billion by 2032.

- Market to register a CAGR of around 5.8% during 2026-32.

- Product Type Shares

- Coconut oil grabbed market share of 30%.

- Competition

- More than 10 companies are actively engaged in producing hair oil in India.

- Top 5 companies acquired around 35% of the market share.

- Patanjali Ayurved Ltd., Himalaya Wellness Company, Bio Veda Farmacy Pvt. Ltd., Marico Limited, Dabur India Ltd. etc., are few of the top companies.

- Sales Channel

- Retail offline grabbed 70% of the market.

India Hair Oil Market Outlook

The India hair oil market was valued at USD 1.86 billion in 2025 and is projected to advance from USD 1.97 billion in 2026 to USD 2.76 billion by 2032, registering a CAGR of 5.8% across the forecast period. This steady and structurally supported expansion reflects the enduring commercial relevance of the India hair oil market within the broader personal care hair oil market, where consistent household demand, deeply rooted grooming traditions, and stable product familiarity across income groups and geographies are collectively sustaining a reliable and broadly distributed consumption base. Growth is not being driven by category reinvention but by the progressive deepening of everyday oiling habits within a maturing and increasingly accessible mass consumer market.

Product demand is anchored by coconut oil, which commands 30% of the overall product type segment. This leading position reflects the durable and cross-generational consumer preference for coconut hair oil market formulations that are closely associated with routine nourishment, scalp comfort, and traditional grooming practices embedded in household use across India. As purchasing decisions remain tied to everyday utility and deeply familiar product associations, coconut-based variants continue to attract the strongest and most commercially consistent repeat purchase behaviour within the product landscape.

Sales channel dynamics are defined by the commanding position of Retail Offline, which holds 70% of the overall market. This structural dominance confirms that physical store environments, including kirana outlets, pharmacies, supermarkets, and general trade formats, continue to serve as the primary and most commercially significant route through which hair oil products reach Indian consumers. hair oil retail distribution through these formats remains the most dependable and highest-volume channel in a category where routine replenishment, small pack-size buying, and proximity-driven purchase convenience are primary commercial drivers.

The overall market trajectory through 2032 remains well-grounded as traditional product demand, broad offline retail strength, and stable household consumption patterns collectively underpin consistent growth. The strong position of coconut oil within the product mix, combined with the dominant role of physical retail in the sales channel structure, confirms that the hair oil industry outlook for India is built on commercial foundations that are deeply embedded in mass consumer behaviour and structurally resilient to short-term market disruptions throughout the forecast period.

India Hair Oil Market Growth Driver

Rising Household Consumption Expands the Category's Addressable Base

Strengthening household spending across India is providing a commercially durable and broadly distributed foundation for sustained hair oil demand across both rural and urban consumer segments. As per data published by the Ministry of Statistics and Programme Implementation, real private final consumption expenditure grew by 7.3% in FY 2024-25, accelerating meaningfully from the 4.0% growth recorded in the prior year, while average monthly per capita consumption expenditure reached Rs. 4,122 in rural India and Rs. 6,996 in urban India in 2023-24. This expanding household spending base directly supports more frequent purchases of everyday personal care products, with hair oil benefiting particularly strongly given its position as a low-ticket, high-frequency replenishment category within established daily grooming routines.

The narrowing urban-rural consumption gap adds further commercial depth to this demand driver by widening the geographic distribution of category growth. According to statistics released by the Ministry of Statistics and Programme Implementation, the urban-rural consumption expenditure gap narrowed to 70% in 2023-24, reflecting a meaningful convergence in household spending capacity that broadens the addressable consumer base for mass-market hair oil for traditional hair care routines positioning across previously underserved non-metro and rural markets. As both rural and urban consumption continue their upward trajectory, brands gain more stable volume foundations and more geographically diversified demand across the distribution network.

India Hair Oil Market Challenge

Input Cost Volatility Compresses Margin and Pricing Flexibility

Sharp and sustained increases in coconut and copra commodity prices are creating a structurally significant and commercially demanding challenge for hair oil manufacturers managing formulation economics, margin protection, and promotional investment across India's price-sensitive mass-market segments. Based on data from the coconut Development Board under the Ministry of Agriculture and Farmers Welfare, the annual average price of milling copra at Kangayam reached Rs. 11,566 per quintal in 2024-25, reflecting a 51.31% year-over-year increase, while ball copra at Tiptur rose 43.28% to reach Rs. 12,352 per quintal during the same period. These sharp input cost escalations directly raise formulation costs for coconut hair oil market dependent product lines, narrowing the pricing headroom available for promotional activity and making it considerably harder to protect margins while maintaining accessible mass-market price points.

The breadth of this challenge across multiple raw material categories compounds the strategic difficulty for manufacturers. As indicated by authoritative sources at the coconut Development Board, dry coconut at Kozhikode recorded an annual average price of Rs. 12,925 per quintal reflecting a 24.58% increase, while coconut without husk at Alappuzha averaged Rs. 23,066 per thousand nuts, rising 50.40% in 2024-25. This multi-input price escalation makes procurement planning, cost forecasting, and SKU-level pricing decisions significantly more complex, particularly for brands competing in value-conscious consumer segments where even modest retail price increases can trigger trade-down behaviour and volume loss across mainstream distribution channels.

Unlock Market Intelligence

Explore the market potential with our data-driven report

India Hair Oil Market Trend

Formalisation of Herbal Production Elevates Quality Standards Across the Category

A well-defined and commercially consequential structural trend is reshaping the competitive and formulation landscape of India's hair oil category, as the herbal and Ayurveda-linked personal care manufacturing ecosystem moves toward more rigorous production standards, structured quality controls, and formally documented compliance frameworks. Evidence drawn from public data released by the Ministry of Ayush confirms that India has more than 8,000 licensed Ayurvedic, Siddha, Unani, and Homoeopathy drug manufacturers, with Good Manufacturing Practice compliance mandated as a prerequisite for obtaining a manufacturing licence across this extensive production base. This formalisation is directly elevating the credibility of ayurvedic hair oil market product claims by anchoring traditional and herbal positioning in verifiable manufacturing quality rather than solely in heritage and cultural association.

The depth of this quality infrastructure adds meaningful commercial weight to the trend and differentiates India's herbal production ecosystem from less formally governed competitive environments. In line with findings from the Ministry of Ayush, 38 Ayurvedic drug manufacturing units have attained WHO-GMP Certificate of Pharmaceutical Products status and 102 drug testing laboratories are approved for Ayurveda, Siddha, and Unani drugs. As this quality-backed environment strengthens, brands investing in herbal extracts in hair oil formulations and premium Ayurveda-inspired product development are gaining more credible and defensible positioning that supports premium price acceptance and stronger consumer trust across both domestic and export markets.

India Hair Oil Market Opportunity

Digital Expansion Creates a Scalable Route to Premium Consumer Engagement

India's rapidly expanding digital connectivity infrastructure is creating a commercially significant and structurally durable opportunity for hair oil brands seeking to build premium, problem-solution, and ingredient-differentiated product positioning beyond the reach limitations of physical retail expansion. As per official figures from the Telecom Regulatory Authority of India, total internet subscribers grew from 954.40 million at the end of March 2024 to 969.10 million at the end of March 2025, while broadband subscribers increased from 924.07 million to 944.12 million over the same period, confirming that a large and rapidly deepening connected audience is now accessible to brands through digital discovery, targeted content, and direct-to-consumer engagement strategies across both metro and non-metro locations.

The commercial intensity of this digital opportunity is reinforced by the growing depth of online engagement across India's connected consumer base. Data compiled from internationally recognised public authorities at the Telecom Regulatory Authority of India confirms that wireless data usage climbed from 1,94,774 PB in 2023-24 to 2,28,779 PB in 2024-25, reflecting a 17.46% increase, while wireless data revenue grew 15.49% to reach Rs. 2,15,078 crore during the same period. For premium hair oil for millennials and urban consumer-focused brands, this expanding digital engagement depth supports stronger online visibility for value-added, herbal, and scalp-care variants that can scale their addressable market through cost-efficient digital campaigns without depending exclusively on physical shelf availability and traditional trade investment.

Unlock Market Intelligence

Explore the market potential with our data-driven report

India Hair Oil Market Segmentation Analysis

By Product Type

- Coconut Oil

- Almond Oil

- Argan Oil

- Olive Oil

- Castor Oil

- Amla/Herbal Oil

- Others

The segment with highest market share under Product Type coconut oil with around 30%, reflecting consistent and deeply embedded consumer demand for nourishment-associated, culturally familiar, and routinely trusted hair oil for scalp nourishment formulations across India's broad and demographically diverse consumer base. Consumers across income groups, age cohorts, and geographic markets within India consistently select coconut-based hair oil because it combines strong cultural resonance with a widely understood and dependable benefit profile centred on everyday nourishment, softness, and scalp maintenance, creating a commercial proposition that sustains very high repeat purchase frequency and exceptional category loyalty. Its market leadership confirms that heritage, familiarity, and routine-use compatibility remain the most commercially durable purchase drivers within the India hair oil product landscape.

Its sustained dominance also reflects a wider category dynamic in which consumers continue to reward formulations that integrate naturally and effortlessly into established daily grooming habits without requiring behavioural change or educational investment at the point of purchase. coconut oil variants maintain their lead across diverse retail environments because they support strong shelf conversion, benefit from deep and multigenerational consumer recall, and serve a broad range of hair types and usage occasions across both household and personal care settings. As ayurvedic ingredients for hair care and value-added variant innovation continue to advance, this segment is expected to retain its anchor position as the most commercially significant product type within the India hair oil market throughout the forecast period.

By Sales Channel

- Retail Online

- E-commerce Platforms

- Brand-Owned Websites

- Online Beauty & Personal Care Stores

- Retail Offline

- Supermarkets & Hypermarkets

- Pharmacies/Drug Stores

- Specialty Beauty Stores

- Convenience Stores

- Department Stores

- Others

Retail Offline commands the highest share within the sales channel category at 70%, establishing physical store environments as the most commercially significant and volume-generating route through which hair oil products reach consumers across India. Consumers continue to favour in-store purchasing for a category defined by small pack-size buying, routine replenishment frequency, and proximity-driven purchase convenience, with hair oil in supermarkets and hypermarkets, kirana outlets, and pharmacy retail formats all contributing meaningfully to the commercial breadth and depth of this channel across urban and rural geographies. Its dominant position confirms that physical retail accessibility, immediate product availability, and in-store brand visibility remain the primary commercial anchors of the India hair oil sales channel structure.

Its continued leadership is expected to remain structurally stable through the forecast period because offline retail uniquely supports habitual replenishment behaviour, impulse purchase occasions, and broad geographic market penetration across the millions of neighbourhood and general trade retail points that form the commercial backbone of India's personal care distribution ecosystem. As digital commerce continues to expand its influence on awareness and premium product discovery, physical retail is expected to retain its position as the highest-volume and most commercially dependable distribution channel within the India hair oil market through 2032.

List of Companies Covered in India Hair Oil Market

The companies listed below are highly influential in the India hair oil market, with a significant market share and a strong impact on industry developments.

- Patanjali Ayurved Ltd.

- Himalaya Wellness Company

- Bio Veda Farmacy Pvt. Ltd.

- Marico Limited

- Dabur India Ltd.

- Emami Limited

- Bajaj Consumer Care Ltd.

- Hindustan Unilever Limited

- Honasa Consumer Ltd.

- WOW Skin Science

Market News & Updates

- Marico Limited, 2025:

Marico launched Parachute Advansed Olive Enriched Coconut Hair Oil in India as a new variant in its premium hair nourishment range. The product combines coconut hair oil with olive and expands the brand’s superblend portfolio, which already includes rosemary, bhringraj, almond, and castor-shea variants.

- Emami Limited, 2025:

Emami rebranded Kesh King as Kesh King GOLD in India and introduced an upgraded Ayurveda + Science proposition. The refreshed range combines 21 Ayurvedic herbs with ingredients such as Gro Biotin and Plant Omega 3-6-9, along with updated packaging and a new Advanced Hair Growth Serum.

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- India Hair Oil Market Policies, Regulations, and Standards

- India Hair Oil Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- India Hair Oil Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Product Type

- Coconut Oil- Market Insights and Forecast 2022-2032, USD Million

- Almond Oil- Market Insights and Forecast 2022-2032, USD Million

- Argan Oil- Market Insights and Forecast 2022-2032, USD Million

- Olive Oil- Market Insights and Forecast 2022-2032, USD Million

- Castor Oil- Market Insights and Forecast 2022-2032, USD Million

- Amla/Herbal Oil- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By Category

- Non-Medicated Hair Oil- Market Insights and Forecast 2022-2032, USD Million

- Medicated Hair Oil- Market Insights and Forecast 2022-2032, USD Million

- By Formulation

- Conventional/Synthetic- Market Insights and Forecast 2022-2032, USD Million

- Herbal/Ayurvedic- Market Insights and Forecast 2022-2032, USD Million

- Organic/Natural- Market Insights and Forecast 2022-2032, USD Million

- By Application

- Hair Nourishment- Market Insights and Forecast 2022-2032, USD Million

- Hair Damage Repair- Market Insights and Forecast 2022-2032, USD Million

- Hair Growth Support- Market Insights and Forecast 2022-2032, USD Million

- Scalp Care- Market Insights and Forecast 2022-2032, USD Million

- Styling & Frizz Control- Market Insights and Forecast 2022-2032, USD Million

- By End User

- Individual/Household- Market Insights and Forecast 2022-2032, USD Million

- Commercial/Salon & Spa- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel

- Retail Online- Market Insights and Forecast 2022-2032, USD Million

- E-commerce Platforms- Market Insights and Forecast 2022-2032, USD Million

- Brand-Owned Websites- Market Insights and Forecast 2022-2032, USD Million

- Online Beauty & Personal Care Stores- Market Insights and Forecast 2022-2032, USD Million

- Retail Offline- Market Insights and Forecast 2022-2032, USD Million

- Supermarkets & Hypermarkets- Market Insights and Forecast 2022-2032, USD Million

- Pharmacies/Drug Stores- Market Insights and Forecast 2022-2032, USD Million

- Specialty Beauty Stores- Market Insights and Forecast 2022-2032, USD Million

- Convenience Stores- Market Insights and Forecast 2022-2032, USD Million

- Department Stores- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- Retail Online- Market Insights and Forecast 2022-2032, USD Million

- By Region

- North- Market Insights and Forecast 2022-2032, USD Million

- East- Market Insights and Forecast 2022-2032, USD Million

- West- Market Insights and Forecast 2022-2032, USD Million

- South- Market Insights and Forecast 2022-2032, USD Million

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Product Type

- Market Size & Growth Outlook

- India Coconut Oil Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Category- Market Insights and Forecast 2022-2032, USD Million

- By Formulation- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- India Almond Oil Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Category- Market Insights and Forecast 2022-2032, USD Million

- By Formulation- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- India Argan Oil Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Category- Market Insights and Forecast 2022-2032, USD Million

- By Formulation- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- India Olive Oil Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Category- Market Insights and Forecast 2022-2032, USD Million

- By Formulation- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- India Castor Oil Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Category- Market Insights and Forecast 2022-2032, USD Million

- By Formulation- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- India Amla/Herbal Oil Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Category- Market Insights and Forecast 2022-2032, USD Million

- By Formulation- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- Marico Limited

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Dabur India Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Emami Limited

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Bajaj Consumer Care Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Hindustan Unilever Limited

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Patanjali Ayurved Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Himalaya Wellness Company

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Bio Veda Farmacy Pvt. Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Honasa Consumer Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- WOW Skin Science

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Marico Limited

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Product Type |

|

| By Category |

|

| By Formulation |

|

| By Application |

|

| By End User |

|

| By Sales Channel |

|

| By Region |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.