UK Bags and Luggage Market Report: Trends, Growth and Forecast (2026-2032)

By Category (Bags (Cross Body Bags, Bags and Backpacks, Business Bags, Duffle Bags, Clutches, Others), Luggage (Soft Luggage, Hard Luggage, Wheeled Luggage, Non-Wheeled Luggage)), By Sales Channel (Retail Offline, Retail Online), By Material Type (Soft Case (Nylon, Polyester, Ballistic Nylon), Hard Case (Polycarbonate, ABS (Acrylonitrile Butadiene Styrene), Polypropylene)), By Price Category (Luxury, Mass/Economy, Premium), By Application (Travel, Business), By Region (England, Wales, Scotland, Northern Ireland) ... Read more

|

Major Players

|

UK Bags and Luggage Market Statistics and Insights, 2026

- Market Size Statistics

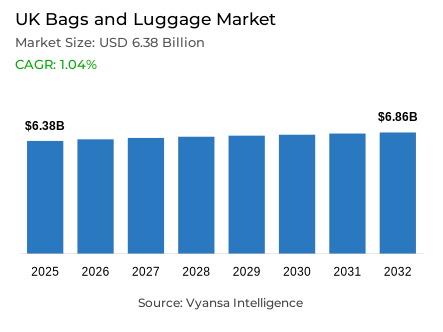

- Bags and luggage market size in UK was estimated at USD 6.38 billion in 2025.

- The market size is expected to grow to USD 6.86 billion by 2032.

- Market to register a CAGR of around 1.04% during 2026-32.

- Category Shares

- Bags grabbed market share of 90%.

- Competition

- More than 20 companies are actively engaged in producing bags and luggage in UK.

- Top 5 companies acquired around 30% of the market share.

- Michael Kors (UK) Ltd, Hermès International SCA, Kering SA, Louis Vuitton UK Ltd, Chanel Ltd etc., are few of the top companies.

- Sales Channel

- Retail offline grabbed 75% of the market.

UK Bags and Luggage Market Outlook

The UK bags and luggage market is undergoing transformation centred on premiumisation and sustainable innovation. While end-user spending is increasingly selective, demand is supported by investment-driven purchasing and high-versatility products. With domestic and international travel remaining lifestyle priorities, the market is valued at USD 6.38 billion in 2025 and is expected to remain broadly stable at USD 6.86 billion by 2032, reflecting a CAGR of approximately 1.04% over the forecast period.

This stability is reinforced by growing preference for durable, multi-use formats such as backpacks and duffel bags that meet low-cost airline hand-luggage limits. The luxury segment remains resilient, supported by heritage brands and expanding circular-economy models that widen access through resale and rental.

Sustainability and digital strategies are also shaping future direction. Preparations for the 2026 Digital Product Passport requirements are driving improved supply-chain transparency and consumer confidence. Distribution remains anchored in physical retail but is becoming more dynamic through omnichannel investment, including in-store repair services and interactive online launches.

Overall, the market outlook is positive, as brands respond to macro-economic pressure through innovation. Emphasis on recycled materials and smart features positions suppliers to appeal to environmentally conscious and tech-savvy travellers, supporting value retention even amid uneven volume trends.

UK Bags and Luggage Market Growth DriverTravel Intensity Fuels Versatile Carry Options

Outbound travel is also a strong demand driver of luggage and cabin-friendly bag formats. In 2024, the United Kingdom will experience 94.6 million foreign trips and spend £78.6 billion, which will keep luggage replacement and upgrade cycles active. Spain alone documents 17.8 million visits by residents of Great Britain, highlighting the importance of short-haul travel where small backpacks and duffel bags remain viable.

Against the backdrop of constrained household budgets, end users are focusing on bags that can serve both commuting and travelling purposes. Cross-body bags, backpacks, and duffel bags fit budget-airline hand-luggage specifications and provide higher perceived value due to their multi-use functionality. This preference supports demand for durable construction, lightweight design, and smart internal organisation, especially among frequent travellers seeking to avoid repeated purchases.

UK Bags and Luggage Market ChallengeCost Pressures Keep Discretionary Spending Cautious

Discretionary spending remains constrained by persistent cost pressures. CPI inflation stands at 2.5% and CPIH inflation at 3.5% in the 12 months to December 2024. Within CPIH, housing and household services inflation reaches 6.0%, while owner-occupier housing costs rise 8.0% annually, reducing spending headroom for non-essential goods such as bags and luggage. This squeeze heightens price sensitivity across the sector.

Shoppers either trade down, delay purchases until promotions, or buy less frequently while opting for higher-end items perceived as longer-term investments. Mid-priced brands face the greatest pressure, as rising material and compliance costs are difficult to absorb while maintaining competitive pricing, limiting volume recovery.

Unlock Market Intelligence

Explore the market potential with our data-driven report

UK Bags and Luggage Market TrendResale Momentum Strengthens Circular Buying

Resale interaction with end users is increasing, supported by affordability concerns and circular-economy behaviour. According to ONS retail sales data, the seasonally adjusted volume index for retail sales of second-hand goods in stores rose from 95.5% in 2023 to 101% in 2024, indicating higher activity in the formal resale channel. This growth is reshaping behaviour in the primary market.

Consumers increasingly assess bags and luggage based on durability and resale potential, with second-hand purchases serving as a lower-cost entry point into premium brands. In response, brands and retailers are strengthening repair, recycling, and alternative-material strategies to extend product life. Luxury players are also reinforcing authentication and traceability to protect brand equity across both new and pre-owned transactions.

UK Bags and Luggage Market OpportunityOmnichannel Convenience Creates a Clear Growth Route

Retail online remains a large and stable channel, offering a transparent route for scalable growth. ONS data show that internet sales accounted for 28% of total retail sales in 2024, up from 27% in 2023, reflecting strong consumer willingness to shop online and compare prices. This supports blended digital-first and store-led strategies.

Retailers are using click-and-collect, flexible returns, and enhanced product content to reduce purchase hesitation, while stores provide fittings, personalisation, and aftercare services. Specialist retailers can differentiate through curated ranges and advisory expertise, with consistent omnichannel execution supporting loyalty and premium pricing despite value-conscious behaviour.

Unlock Market Intelligence

Explore the market potential with our data-driven report

UK Bags and Luggage Market Segmentation Analysis

By Category

- Bags

- Cross Body Bags

- Bags and Backpacks

- Business Bags

- Duffle Bags

- Clutches

- Others

- Luggage

- Soft Luggage

- Hard Luggage

- Wheeled Luggage

- Non-Wheeled Luggage

The segment with highest market share under category is Bags, holding approximately 90% market share. This dominance is driven by an investment-oriented mindset, where quality handbags and multi-purpose carry-alls are favoured over seasonal, lower-end items. British end users increasingly prioritise durability and multifunctional design, with backpacks and duffel bags replacing traditional business formats.

The expansion of resale platforms such as Vinted and eBay further supports this segment, particularly within luxury bags, helping sustain share despite inflationary pressures. Bags remain the primary contributor to overall market value by delivering long-term utility aligned with modern travel and lifestyle needs.

By Sales Channel

- Retail Offline

- Retail Online

Retail offline holds the largest share within sales channels, accounting for around 75% of the market. Physical stores remain preferred due to the tactile nature of bags and luggage, with consumers valuing in-person evaluation of materials and craftsmanship. Specialist retailers benefit by offering experiential environments that strengthen engagement and loyalty.

While digital strategies continue to grow in importance, physical retail remains critical for high-value purchases and brand storytelling. Luxury brands, in particular, rely on flagship stores for personalised services and repairs that are difficult to replicate online. Hybrid omnichannel models, including click-and-collect, reinforce offline dominance while delivering the convenience UK shoppers expect.

List of Companies Covered in UK Bags and Luggage Market

The companies listed below are highly influential in the UK bags and luggage market, with a significant market share and a strong impact on industry developments.

- Michael Kors (UK) Ltd

- Hermès International SCA

- Kering SA

- Louis Vuitton UK Ltd

- Chanel Ltd

- Gucci Ltd

- Prada UK Retail Ltd

- Christian Dior (UK) Ltd

- Samsonite Ltd

- Burberry Group Plc

Competitive Landscape

The bags and luggage market in the UK remains highly fragmented, shaped by strong price sensitivity and growing consumer polarisation. Luxury players continue to dominate value terms, with brands such as Louis Vuitton, Chanel, Gucci and Prada retaining leadership positions despite softer demand and slowing sales momentum. Hermès stands out as an exception, benefiting from pricing power and sustained interest in heritage-led storytelling. At the other end of the spectrum, value and fast-fashion brands continue to attract cost-conscious shoppers with trend-led designs at accessible price points. Mid-priced brands face the greatest pressure, as consumers increasingly either trade down to affordable alternatives or invest less frequently in premium, durable products perceived as long-term value.

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- UK Bags and Luggage Market Policies, Regulations, and Standards

- UK Bags and Luggage Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- UK Bags and Luggage Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Units Sold in Thousand Units

- Market Segmentation & Growth Outlook

- By Category

- Bags- Market Insights and Forecast 2022-2032, USD Million

- Cross Body Bags- Market Insights and Forecast 2022-2032, USD Million

- Bags and Backpacks- Market Insights and Forecast 2022-2032, USD Million

- Business Bags- Market Insights and Forecast 2022-2032, USD Million

- Duffle Bags- Market Insights and Forecast 2022-2032, USD Million

- Clutches- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- Luggage- Market Insights and Forecast 2022-2032, USD Million

- Soft Luggage- Market Insights and Forecast 2022-2032, USD Million

- Hard Luggage- Market Insights and Forecast 2022-2032, USD Million

- Wheeled Luggage- Market Insights and Forecast 2022-2032, USD Million

- Non-Wheeled Luggage- Market Insights and Forecast 2022-2032, USD Million

- Bags- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel

- Retail Offline- Market Insights and Forecast 2022-2032, USD Million

- Retail Online- Market Insights and Forecast 2022-2032, USD Million

- By Material Type

- Soft Case- Market Insights and Forecast 2022-2032, USD Million

- Nylon- Market Insights and Forecast 2022-2032, USD Million

- Polyester- Market Insights and Forecast 2022-2032, USD Million

- Ballistic Nylon- Market Insights and Forecast 2022-2032, USD Million

- Hard Case- Market Insights and Forecast 2022-2032, USD Million

- Polycarbonate- Market Insights and Forecast 2022-2032, USD Million

- ABS (Acrylonitrile Butadiene Styrene)- Market Insights and Forecast 2022-2032, USD Million

- Polypropylene- Market Insights and Forecast 2022-2032, USD Million

- Soft Case- Market Insights and Forecast 2022-2032, USD Million

- By Price Category

- Luxury- Market Insights and Forecast 2022-2032, USD Million

- Mass/Economy- Market Insights and Forecast 2022-2032, USD Million

- Premium- Market Insights and Forecast 2022-2032, USD Million

- By Application

- Travel- Market Insights and Forecast 2022-2032, USD Million

- Business- Market Insights and Forecast 2022-2032, USD Million

- By Region

- England

- Wales

- Scotland

- Northern Ireland

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Category

- Market Size & Growth Outlook

- UK Bags Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Units Sold in Thousand Units

- Market Segmentation & Growth Outlook

- By Category- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Material Type- Market Insights and Forecast 2022-2032, USD Million

- By Price Category- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- UK Luggage Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Units Sold in Thousand Units

- Market Segmentation & Growth Outlook

- By Category- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Material Type- Market Insights and Forecast 2022-2032, USD Million

- By Price Category- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- Louis Vuitton UK Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Chanel Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Gucci Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Prada UK Retail Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Christian Dior (UK) Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Michael Kors (UK) Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Hermès International SCA

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Kering SA

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Samsonite Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Burberry Group Plc

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Louis Vuitton UK Ltd

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Category |

|

| By Sales Channel |

|

| By Material Type |

|

| By Price Category |

|

| By Application |

|

| By Region |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.