UAE Industrial Gases Market Report: Trends, Growth and Forecast (2026-2032)

By Gas Type (Nitrogen Gas, Oxygen Gas, Carbon Dioxide Gas, Argon Gas, Helium Gas, Hydrogen Gas, Other), By Supply Mode (Cylinders, Bulk, On-Site Production, Captive, Other), By Application (Combustion and Process Oxygen, Welding and Metal Fabrication, Inerting Blanketing and Heat Treating, Cryogenics and liquefaction, Chemical Synthesis and Hydrogenation, Purging and Purifications, Analytical and Calibration), By End User Industry (General Manufacturing, Food, Metallurgy, Chemicals, Healthcare, Electronics, Refining & Energy, Glass, Pulp & Paper, Others) ... Read more

|

Major Players

|

UAE Industrial Gases Market Statistics and Insights, 2026

- Market Size Statistics

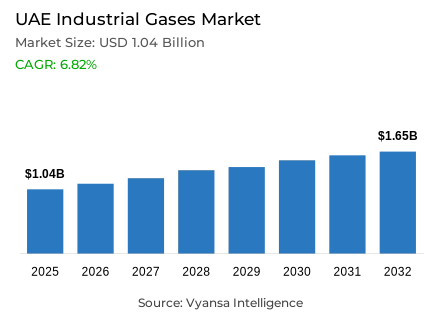

- Industrial gases in UAE is estimated at USD 1.04 billion in 2025.

- The market size is expected to grow to USD 1.65 billion by 2032.

- Market to register a cagr of around 6.82% during 2026-32.

- Gas Type Shares

- Oxygen gas grabbed market share of 40%.

- Competition

- More than 10 companies are actively engaged in producing industrial gases in UAE.

- Top 5 companies acquired around 80% of the market share.

- Dubai Industrial Gases; Brothers Gas; Emirates Industrial Gases Company L.L.C.; Linde; Air Liquide etc., are few of the top companies.

- Supply Mode

- Cylinders grabbed 40% of the market.

UAE Industrial Gases Market Outlook

The UAE industrial gases market is anticipated to grow from USD 1.04 Billion in 2025 to USD 1.65 Billion by 2032, with a CAGR of approximately 6.82% from 2026-32. The high growth rate of just under 8% per annum in the healthcare industry due to 10 new hospitals andmore than 150 new clinics opening in 2024 drives the demand for medical-grade oxygen, nitrogen, and specialty gases steadily. Supporting this trend, Abu Dhabi’s 5% increase in value added in manufacturing in Q1, 2025, boosts gas usage in fabrication and processing, along with other industrial processes. “Operation 300bn” and the National ICV Program initiated by the UAE government have been stabilizing the market by fostering domestic production capability.

With AED 168 billion industrial procurement and AED 7.8 billion new offtake agreement volumes, the projects increase the country's use of gas for welding, chemical manufacture, metallurgy processes, and other advanced productions. Then there's the country's hydrogen production goal of 1.4 million tonnes by the year 2031 to fuel the use of High Purity Gases.

The oxygen gas market leads with the highest market share of 40%. This is mainly due to its applications in the medical field and the use in metal fabrication, oxidation in the chemical process, and wastewater treatment. This is because the demands for quality and purity rise with the increasing expansion in the coming years.

Cylinder-based supply mode also take the lead, market share-wise, at 40%. This is driven by the material adoption by hospitals, laboratories, small-scale industry, F&B processors, and others. The increasing number over 2,500 new F&B enterprises, along with increasing licensing in industries, has driven gas consumption, hence making the cylinder-based system preferred by virtue of its flexible nature.

UAE Industrial Gases Market Growth Driver

Strong Healthcare and Industrial Expansion Supporting Market Momentum

Rapid growth in the UAE’s healthcare and industrial settings is further fueling the UAE Industrial Gases Market at a rapid pace. The healthcare industry is increasing at a rate of 8% per annum and is likely to reach USD 50 billion by 2029, mostly due to huge investments made by the UAE government. In 2024, the launch of 10 new hospitals and over 150 clinics, along with mandatory insurance for 98% of UAE residents, has significantly driven demands for oxygen, nitrogen, and other specialty gases in the UAE healthcare industry. Meanwhile, value added in the manufacturing industry in Abu Dhabi reached AED 28.5 billion in Q1 2025, mounting a 5% growth over previous years, further fueling gas consumption in fabrication, processing, and other industrial applications.

The expansion of industry is also supported in the country by initiatives such as Operation 300bn, which plans to increase the contribution of the industry sector’s GDP from its current value of AED 133 billion to AED 300 billion by 2031. Additionally, government initiatives such as the National ICV Program with industrial spending of AED 168 billion and new off-take agreements worth AED 7.8 billion ensure a steady growth base for gas providers who service the metallurgy, welding, chemical, and advanced manufacturing sectors.

UAE Industrial Gases Market Challenge

Rising Supply Chain Pressures and Input Dependency Restraining Market Efficiency

The UAE industrial gases market is witnessing various forces in the supply chain and logistics system that are pressuring the operation dynamics and pricing structures. Warehouse rentals are high, logistics are expensive, and the price for industrial property is high, thus pressuring the distribution systems, especially when the industries are storing high volumes of Liquefied Gas cylinders or volumes in the industries. Geopolitics is another factor that is pressuring the supply chain dynamics for the raw materials across the global markets due to increases in the complexities associated with the continuous procurement process.

High dependency on imports creates a new risk dynamic, especially with respect to specific gas use sectors such as the electronic and semiconductor sectors, as well as high-purity production. Ensuring a stable supply of qualified feedstock from international markets becomes even more challenging with these intensified fluctuations and international pricing patterns. Companies are forced to focus investment on a strong supply chain infrastructure, enhanced warehouse capacity, and supply chain redundancies that can drive up prices from the value chain.

Unlock Market Intelligence

Explore the market potential with our data-driven report

UAE Industrial Gases Market Trend

Expanding Focus on Green Hydrogen and Low-Carbon Gas Ecosystems

The UAE’s new focus on the production of green and blue hydrogen is already altering the demand structure in the industry gases market. The UAE plans, under the National Hydrogen Strategy, to achieve the production of 1.4 million tonnes of hydrogen by 2031, with 1 million tonnes of green hydrogen production via the massive use of electrolyzers. Large demand for the use of industry gases in the hydrogen production, purification, and transport chain will be needed in the course of this new technological push in the UAE. The federal regulation of energy management in industry (April 2023) is also forcing industry to use energy management systems, thereby increasing the demand for more efficient gas solutions.

Hydrogen projects range from petrochemical sectors to heavy industry and transportation; and the government is targeting a 25% reduction of emissions in difficult-to-cut sectors by 2031. The growing focus on industrial areas in Sharjah, Dubai, and Abu Dhabi, where over 1,600 businesses moved into the Free Zone in 2024, points to the growing focus on investment in sustainable industry infrastructure. This also points to more stringent requirements for gases that require high purity and low carbon footprints. The growing focus on infrastructure development for hydrogen use is making the UAE industry gases market experience a clear focus on sustainable applications.

UAE Industrial Gases Market Opportunity

Growing Potential within the Expanding Food and Beverage Manufacturing Base

The increasing food and beverage (F&B) manufacturing industry in the UAE is an emerging market for industrial gas companies. The F&B exports of the country registered an increase of 19% during H1 2024. Dubai Industrial City, an industrial zone, attracted projects worth AED 350 million from the F&B industry in the year 2024. A total of 25 companies leased space of 1.7 million sq. ft. here. Such increasing activities in the F&B sector translate into the increasing use of nitrogen, oxygen, and carbon dioxide gas, all of which are used for the freezing, processing, and packaging of F&B.

The industry is aided by the addition of 2,540 new firms to national chambers in the first ten months of 2024, with continued localization and entrepreneurship in the manufacturing industry. Other factors initiated by the government, like Operation 300bn and access to funding from the Emirates Development Bank’s portfolio of AED 30 billion, provide positive stimuli for the country to produce its food locally. As end-users increase the application of new technologies for preservation, packaging, and food quality testing, there will be increased collaboration by industry gases with providers of said services.

Unlock Market Intelligence

Explore the market potential with our data-driven report

UAE Industrial Gases Market Segmentation Analysis

By Gas Type

- Nitrogen Gas

- Oxygen Gas

- Carbon Dioxide Gas

- Argon Gas

- Helium Gas

- Hydrogen Gas

- Other

Oxygen gas holds the highest market share at 40% in the UAE Industrial Gases Market, reflecting its critical role across medical and industrial applications. The ongoing expansion of the healthcare sector-with 10 new hospitals and more than 150 clinics added in 2024-continues to drive heightened demand for medical-grade oxygen. Healthcare growth of around 8% annually underscores the essential nature of oxygen for respiratory care, surgical procedures, emergency response, and therapeutic treatments. Simultaneously, Abu Dhabi’s 5% annual manufacturing growth and the nationwide rise in industrial licensing support demand from welding, metal fabrication, combustion enhancement, and chemical oxidation processes.

Beyond core applications, oxygen is integral to wastewater treatment, enhanced oil recovery, and advanced production lines requiring precise combustion environments. The UAE’s broader diversification under Operation 300bn, targeting AED 300 billion in industrial GDP contribution by 2031, is expanding oxygen-dependent manufacturing segments. Rising quality and purity requirements across medical, chemical, and materials industries further reinforce oxygen’s position as the dominant gas category. Its versatility, high utility across sectors, and alignment with national industrial expansion ensure its continued leadership among gas types used by end users.

By Supply Mode

- Cylinders

- Bulk

- On-Site Production

- Captive

- Other

Cylinder-based supply mode maintains a 40% market share within the UAE industrial gases supply mode landscape, supported by widespread adoption among healthcare facilities, laboratories, small-scale manufacturers, and distributed industrial operations. Cylinder supply offers operational flexibility for end users that lack the scale or infrastructure for on-site generation or pipeline connectivity. The healthcare sector’s continuous expansion—including new hospitals, clinics, and diagnostic centers—has strengthened demand for medical-grade oxygen and specialty gases delivered through cylinders. High insurance coverage and increasing patient volumes further reinforce recurring gas requirements across clinical environments.

Small and medium F&B manufacturers, fabrication units, and emerging enterprises in industrial zones continue to rely on cylinders for rapid deployment and manageable upfront costs. The influx of more than 2,500 new F&B companies in 2024 and the 4.7% rise in new industrial licenses have expanded the customer base for cylinder-delivered gases. While bulk and pipeline modes are preferred for high-volume operations, cylinders retain strong relevance due to ease of handling, compliance flexibility, and suitability for distributed operations. These attributes ensure cylinders remain a stable and essential component of the UAE’s industrial gases distribution ecosystem.

List of Companies Covered in UAE Industrial Gases Market

The companies listed below are highly influential in the UAE industrial gases market, with a significant market share and a strong impact on industry developments.

- Dubai Industrial Gases

- Brothers Gas

- Linde

- Air Liquide

- Air Products

- Gulf Cryo

- ADNOC Gas (Abu Dhabi Industrial Gas)

Market News & Updates

- Gulf Cryo, 2025:

Gulf Cryo opened the UAE’s first high-purity CO₂ capture and utilization plant in Ras Al Khaimah in October 2025. Built with RAK Ceramics, the facility captures 17,000 metric tons of CO₂ each year and converts it into 99.99% pure food-grade CO₂. This captured CO₂ is then used in industries such as food and beverage, healthcare, farming, and energy. The project supports the UAE’s efforts to reach net-zero emissions by 2050.

- ADNOC Gas, 2025:

ADNOC Gas signed a long-term agreement with Shell in early November 2025. Under this 15-year deal, ADNOC will supply up to 1 million metric tons of LNG each year from the upcoming Ruwais project. The Ruwais LNG plant will start operations in late 2028 and will have two production units. It will be the first LNG export facility in the Middle East and Africa powered by clean energy, making it one of the lowest-emission LNG projects worldwide.

Frequently Asked Questions

Related Report

1. Market Segmentation

1.1. Research Scope

1.2. Research Methodology

1.3. Definitions and Assumptions

2. Executive Summary

3. UAE Industrial Gases Market Policies, Regulations, and Standards

4. UAE Industrial Gases Market Dynamics

4.1. Growth Factors

4.2. Challenges

4.3. Trends

4.4. Opportunities

5. UAE Industrial Gases Market Statistics, 2022-2032F

5.1. Market Size & Growth Outlook

5.1.1.By Revenues in USD Million

5.1.2.By Quantity Sold in Tons

5.2. Market Segmentation & Growth Outlook

5.2.1.By Gas Type

5.2.1.1. Nitrogen Gas- Market Insights and Forecast 2022-2032, USD Million & Quantity in Tons

5.2.1.2. Oxygen Gas- Market Insights and Forecast 2022-2032, USD Million & Quantity in Tons

5.2.1.3. Carbon Dioxide Gas- Market Insights and Forecast 2022-2032, USD Million & Quantity in Tons

5.2.1.4. Argon Gas- Market Insights and Forecast 2022-2032, USD Million & Quantity in Tons

5.2.1.5. Helium Gas- Market Insights and Forecast 2022-2032, USD Million & Quantity in Tons

5.2.1.6. Hydrogen Gas- Market Insights and Forecast 2022-2032, USD Million & Quantity in Tons

5.2.1.7. Other- Market Insights and Forecast 2022-2032, USD Million & Quantity in Tons

5.2.2.By Supply Mode

5.2.2.1. Cylinders- Market Insights and Forecast 2022-2032, USD Million & Quantity in Tons

5.2.2.2. Bulk- Market Insights and Forecast 2022-2032, USD Million & Quantity in Tons

5.2.2.3. On-Site Production- Market Insights and Forecast 2022-2032, USD Million & Quantity in Tons

5.2.2.4. Captive- Market Insights and Forecast 2022-2032, USD Million & Quantity in Tons

5.2.2.5. Other- Market Insights and Forecast 2022-2032, USD Million & Quantity in Tons

5.2.3.By Application

5.2.3.1. Combustion and Process Oxygen- Market Insights and Forecast 2022-2032, USD Million & Quantity in Tons

5.2.3.2. Welding and Metal Fabrication- Market Insights and Forecast 2022-2032, USD Million & Quantity in Tons

5.2.3.3. Inerting Blanketing and Heat Treating- Market Insights and Forecast 2022-2032, USD Million & Quantity in Tons

5.2.3.4. Cryogenics and liquefaction- Market Insights and Forecast 2022-2032, USD Million & Quantity in Tons

5.2.3.5. Chemical Synthesis and Hydrogenation- Market Insights and Forecast 2022-2032, USD Million & Quantity in Tons

5.2.3.6. Purging and Purifications- Market Insights and Forecast 2022-2032, USD Million & Quantity in Tons

5.2.3.7. Analytical and Calibration- Market Insights and Forecast 2022-2032, USD Million & Quantity in Tons

5.2.4.By End User Industry

5.2.4.1. General Manufacturing- Market Insights and Forecast 2022-2032, USD Million & Quantity in Tons

5.2.4.2. Food- Market Insights and Forecast 2022-2032, USD Million & Quantity in Tons

5.2.4.3. Metallurgy- Market Insights and Forecast 2022-2032, USD Million & Quantity in Tons

5.2.4.4. Chemicals- Market Insights and Forecast 2022-2032, USD Million & Quantity in Tons

5.2.4.5. Healthcare- Market Insights and Forecast 2022-2032, USD Million & Quantity in Tons

5.2.4.6. Electronics- Market Insights and Forecast 2022-2032, USD Million & Quantity in Tons

5.2.4.7. Refining & Energy- Market Insights and Forecast 2022-2032, USD Million & Quantity in Tons

5.2.4.8. Glass- Market Insights and Forecast 2022-2032, USD Million & Quantity in Tons

5.2.4.9. Pulp & Paper- Market Insights and Forecast 2022-2032, USD Million & Quantity in Tons

5.2.4.10. Others- Market Insights and Forecast 2022-2032, USD Million & Quantity in Tons

5.2.5.By Competitors

5.2.5.1. Competition Characteristics

5.2.5.2. Market Share & Analysis

6. UAE Nitrogen Gas Market Statistics, 2022-2032

6.1. Market Size & Growth Outlook

6.1.1.By Revenues in USD Million

6.1.2.By Quantity Sold in Tons

6.2. Market Segmentation & Growth Outlook

6.2.1.By Supply Mode- Market Insights and Forecast 2022-2032, USD Million & Quantity in Tons

6.2.2.By Application- Market Insights and Forecast 2022-2032, USD Million & Quantity in Tons

6.2.3.By End User Industry- Market Insights and Forecast 2022-2032, USD Million & Quantity in Tons

7. UAE Oxygen Gas Market Statistics, 2022-2032

7.1. Market Size & Growth Outlook

7.1.1.By Revenues in USD Million

7.1.2.By Quantity Sold in Tons

7.2. Market Segmentation & Growth Outlook

7.2.1.By Supply Mode- Market Insights and Forecast 2022-2032, USD Million & Quantity in Tons

7.2.2.By Application- Market Insights and Forecast 2022-2032, USD Million & Quantity in Tons

7.2.3.By End User Industry- Market Insights and Forecast 2022-2032, USD Million & Quantity in Tons

8. UAE Carbon Dioxide Gas Market Statistics, 2022-2032

8.1. Market Size & Growth Outlook

8.1.1.By Revenues in USD Million

8.1.2.By Quantity Sold in Tons

8.2. Market Segmentation & Growth Outlook

8.2.1.By Supply Mode- Market Insights and Forecast 2022-2032, USD Million & Quantity in Tons

8.2.2.By Application- Market Insights and Forecast 2022-2032, USD Million & Quantity in Tons

8.2.3.By End User Industry- Market Insights and Forecast 2022-2032, USD Million & Quantity in Tons

9. UAE Argon Gas Market Statistics, 2022-2032

9.1. Market Size & Growth Outlook

9.1.1.By Revenues in USD Million

9.1.2.By Quantity Sold in Tons

9.2. Market Segmentation & Growth Outlook

9.2.1.By Supply Mode- Market Insights and Forecast 2022-2032, USD Million & Quantity in Tons

9.2.2.By Application- Market Insights and Forecast 2022-2032, USD Million & Quantity in Tons

9.2.3.By End User Industry- Market Insights and Forecast 2022-2032, USD Million & Quantity in Tons

10. UAE Helium Gas Market Statistics, 2022-2032

10.1. Market Size & Growth Outlook

10.1.1. By Revenues in USD Million

10.1.2. By Quantity Sold in Tons

10.2. Market Segmentation & Growth Outlook

10.2.1. By Supply Mode- Market Insights and Forecast 2022-2032, USD Million & Quantity in Tons

10.2.2. By Application- Market Insights and Forecast 2022-2032, USD Million & Quantity in Tons

10.2.3. By End User Industry- Market Insights and Forecast 2022-2032, USD Million & Quantity in Tons

11. UAE Hydrogen Gas Market Statistics, 2022-2032

11.1. Market Size & Growth Outlook

11.1.1. By Revenues in USD Million

11.1.2. By Quantity Sold in Tons

11.2. Market Segmentation & Growth Outlook

11.2.1. By Supply Mode- Market Insights and Forecast 2022-2032, USD Million & Quantity in Tons

11.2.2. By Application- Market Insights and Forecast 2022-2032, USD Million & Quantity in Tons

11.2.3. By End User Industry- Market Insights and Forecast 2022-2032, USD Million & Quantity in Tons

12. Competitive Outlook

12.1. Company Profiles

12.1.1. Linde

12.1.1.1. Business Description

12.1.1.2. Product Portfolio

12.1.1.3. Collaborations & Alliances

12.1.1.4. Recent Developments

12.1.1.5. Financial Details

12.1.1.6. Others

12.1.2. Air Liquide

12.1.2.1. Business Description

12.1.2.2. Product Portfolio

12.1.2.3. Collaborations & Alliances

12.1.2.4. Recent Developments

12.1.2.5. Financial Details

12.1.2.6. Others

12.1.3. Air Products

12.1.3.1. Business Description

12.1.3.2. Product Portfolio

12.1.3.3. Collaborations & Alliances

12.1.3.4. Recent Developments

12.1.3.5. Financial Details

12.1.3.6. Others

12.1.4. Gulf Cryo

12.1.4.1. Business Description

12.1.4.2. Product Portfolio

12.1.4.3. Collaborations & Alliances

12.1.4.4. Recent Developments

12.1.4.5. Financial Details

12.1.4.6. Others

12.1.5. ADNOC Gas (Abu Dhabi Industrial Gas)

12.1.5.1. Business Description

12.1.5.2. Product Portfolio

12.1.5.3. Collaborations & Alliances

12.1.5.4. Recent Developments

12.1.5.5. Financial Details

12.1.5.6. Others

12.1.6. Dubai Industrial Gases

12.1.6.1. Business Description

12.1.6.2. Product Portfolio

12.1.6.3. Collaborations & Alliances

12.1.6.4. Recent Developments

12.1.6.5. Financial Details

12.1.6.6. Others

12.1.7. Brothers Gas

12.1.7.1. Business Description

12.1.7.2. Product Portfolio

12.1.7.3. Collaborations & Alliances

12.1.7.4. Recent Developments

12.1.7.5. Financial Details

12.1.7.6. Others

13. Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Gas Type |

|

| By Supply Mode |

|

| By Application |

|

| By End User Industry |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.