Thailand Video Surveillance Storage Market Report: Trends, Growth and Forecast (2026-2032)

By Storage Architecture (Edge Storage, Recorder-Based Storage, DVR-Based Storage, NVR-Based Storage, Centralized On-Premises Storage, Cloud Storage, Hybrid Storage), By End-User Vertical (Commercial Buildings, Retail and Hospitality, Industrial and Warehousing, Transport and Logistics, Government Sector, Critical Infrastructure and Utilities, Healthcare, Education, Residential and Multi-Dwelling), By Retention and Search Complexity (Basic Operational Recording, Standard Investigation-Centric Storage, Analytics-Assisted Searchable Storage, Evidence-Grade and Compliance-Sensitive Archival), By Sales Channel (Direct Sales, System Integrators, Value-Added Resellers, Distributors, Online Sales/E-Procurement, Managed Service Providers/Cloud Partners) ... Read more

|

Major Players

|

Thailand Video Surveillance Storage Market Statistics and Insights, 2026

- Market Size Statistics

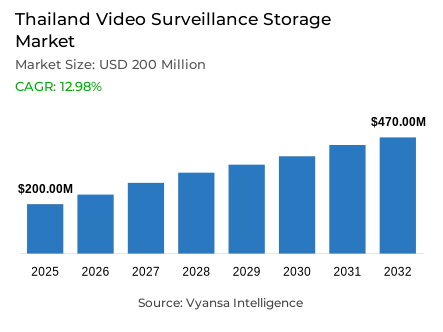

- Video surveillance storage market size in Thailand was valued at USD 200 million in 2025 and is estimated at USD 230 million in 2026.

- The market size is expected to grow to USD 470 million by 2032.

- Market to register a CAGR of around 12.98% during 2026-32.

- Storage Architecture Shares

- Recorder-based storage grabbed market share of 35%.

- Competition

- More than 10 companies are actively engaged in producing video surveillance storage in Thailand.

- Top 5 companies acquired around 40% of the market share.

- Uniview, VIVOTEK, i-PRO, Hikvision, Dahua Technology etc., are few of the top companies.

- End-User Vertical

- Government sector grabbed 30% of the market.

Thailand Video Surveillance Storage Market Outlook

Thailand video surveillance storage market was valued at USD 200 million in 2025, establishing a commercially energized and structurally well-supported foundation within one of Southeast Asia's most actively digitalizing public security ecosystems. Projected to advance from USD 230 million in 2026 to USD 470 million by 2032, the sector registers a CAGR of 12.98% across the forecast horizon. This strong and well-grounded expansion trajectory reflects the growing institutional reliance on recorded video footage for public space monitoring, civic facility oversight, incident documentation, and operational accountability across Thailand's most security-focused government and infrastructure environments. Growth is anchored in genuine operational necessity rather than technology adoption cycles, giving this market a commercial resilience that sustains consistent storage capacity investment across diverse user segments and economic conditions throughout the forecast period.

The storage architecture defining this market's commercial structure is anchored in recorder-based configurations. Recorder-Based Storage commands approximately 35% of total storage architecture market share, reflecting the consistent and deeply embedded institutional preference for structured, locally managed footage capture and retention systems. Their operational familiarity, direct recording capability, and practical on-site access characteristics align naturally with the security management workflows of the market's most commercially significant user segments. This architecture concentration confirms that a large share of Thailand's video surveillance storage end users continue to prioritize proven, operationally predictable configurations whose management simplicity and reliability credentials sustain disproportionate procurement share across both new installation and system upgrade demand cycles.

The end-user architecture reinforces the structural centrality of the government sector as the category's dominant demand source. The Government Sector accounts for approximately 30% of total end-user vertical market share, reflecting the foundational role of public institutions in driving storage demand for surveillance systems across administrative buildings, civic monitoring programs, and public safety networks. Thailand's rise to 52nd place out of 193 countries in the 2024 UN E-Government Development Index, retaining 2nd position in ASEAN as documented by DGA, confirms the digital governance momentum that is progressively expanding the scope of public-sector surveillance infrastructure whose footage retention obligations generate consistent and compounding storage capacity procurement demand.

The forward outlook over the forecast period is defined by four converging structural forces whose combined commercial impact creates a video surveillance storage market of strong and policy-supported expansion momentum. Thailand's smart city pipeline reaching 227 development proposals submitted by January 2026, including 37 declared smart cities as of August 2025 and 190 smart city promotion zones still progressing through the system per depa, confirms the widening rollout of monitored urban infrastructure that sustains consistent footage generation and retention demand across government-linked deployments. The Board of Investment's documentation of digital sector investment applications rising 20-fold in the first half of 2025 to 522.6 billion baht, with data center projects alone attracting 521.2 billion baht across 28 projects, establishes the expanding digital backend infrastructure that creates progressively stronger commercial conditions for cloud-aware and hybrid surveillance storage services. The DGA's documentation of the government's Thang Rath platform delivering 197 government services by May 2025 confirms the public-sector platform integration trajectory that is progressively reshaping how government agencies approach operational data management, digital records governance, and surveillance footage retention. These converging forces define a commercial environment that consistently rewards storage providers with recorder-based deployment reliability, cloud-hybrid architecture capability, and government procurement alignment over the forecast period.

Thailand Video Surveillance Storage Market Growth Driver

Smart City Expansion Sustains Consistent Surveillance Storage Demand

The sustained and institutionally documented expansion of Thailand's national smart city program represents the primary structural driver of video surveillance storage demand. This expansion functions as a persistent footage generation mechanism that continuously intensifies storage capacity requirements across monitored urban assets, connected public facilities, and government-linked digital services whose operational continuity depends on consistent and reliably maintained surveillance retention systems. This smart city-driven demand dynamic transcends cyclical security budget fluctuations, reflecting a durable operational necessity whose procurement volume is structurally anchored in the continuous monitoring obligations of public-sector programs managing an expanding base of digitally governed civic environments.

The quantitative evidence validating this smart city-driven demand dynamic is documented with precision by depa. Thailand's smart city pipeline reaches 227 development proposals submitted by January 2026, including 220 existing cities and 7 new cities, while 37 smart cities have been formally declared as of August 2025 and 190 smart city promotion zones continue progressing through the national system. This widening rollout creates more monitored urban assets, public facilities, and connected services that generate consistent surveillance footage volumes requiring dependable and scalable storage capacity. Thailand's smart city model explicitly covering smart living, smart mobility, and smart governance confirms that the scope of digitally managed public environments generating surveillance retention demand is broadening across multiple program dimensions simultaneously. These smart city expansion dynamics are expected to sustain structural video surveillance storage demand growth over the forecast period.

Thailand Video Surveillance Storage Market Challenge

Low Digital Maturity Constrains Integrated Storage Adoption

The structural unevenness of digital maturity across Thai organizations represents the most consequential operational challenge confronting the Thailand video surveillance storage market. This maturity gap creates systematic integration, deployment complexity, and workflow connectivity constraints that moderate the pace at which organizations can adopt more scalable, centralized, and analytics-capable storage configurations whose operational value depends on a higher level of system integration across cameras, networks, access controls, and records management platforms. In a deployment environment where video surveillance storage's most advanced capabilities are unlocked by connected, unified system architectures, the digital fragmentation that characterizes a large share of the addressable end user population directly limits adoption velocity and upgrade investment confidence.

The structural depth and organizational specificity of this digital maturity challenge are quantified with precision by depa. The 2024 Digital Density Survey released in April 2025 shows that 70% of the sample group has reached only Industry 2.0 maturity levels, confirming that the majority of Thai organizations are operating technology environments whose integration capability constrains meaningful adoption of advanced surveillance storage configurations. The same survey finds that 90.67% of respondents in product development still rely on traditional tools, 87.33% in production process management continue using simple automation systems, and 69.33% in business management still use separate information systems across departments. For storage vendors, this digital maturity landscape creates a strategic imperative to develop deployment approaches and implementation frameworks that deliver meaningful surveillance storage value within the practical integration constraints of digitally transitioning end user environments over the forecast period.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Thailand Video Surveillance Storage Market Trend

Centralized Digital Government Platforms Reshape Storage Governance Expectations

The accelerating development of centralized public-sector digital platforms across Thailand represents the defining structural trend reshaping video surveillance storage system governance expectations, deployment model priorities, and competitive differentiation parameters across the government vertical. This platform centralization trend is progressively transforming how government agencies approach operational data management, access control, and digital records governance, elevating expectations for surveillance footage retention systems that support easier centralized management, stronger retrieval capability, and tighter access control across public-sector operating environments. The commercial implications are significant for storage vendors whose platform integration capability and governance architecture align with the connectivity and accessibility priorities of Thailand's most digitally progressive public institutions.

The institutional momentum and platform specificity of this centralization trend are documented with authority by DGA. Thailand rises to 52nd place out of 193 countries in the 2024 UN E-Government Development Index, maintaining its 2nd place ASEAN ranking and confirming the digital governance advancement that is progressively raising operational expectations across public-sector technology procurement contexts. The government's Thang Rath platform consolidates more than 153 public services in September 2024, expanding to 197 government services by May 2025, confirming that public-sector platform integration is advancing at a pace that creates progressively stronger institutional demand for surveillance storage systems whose architecture supports centralized data management and structured footage governance. As government digital platforms deepen their operational influence, surveillance storage systems that integrate cleanly with centralized access, retrieval, and records management workflows will attract disproportionate public-sector procurement share over the forecast period.

Thailand Video Surveillance Storage Market Opportunity

Data Center Investment Wave Creates Scalable Cloud Storage Headroom

The rapid and institutionally documented expansion of Thailand's data center and digital infrastructure investment base creates a structurally significant and commercially durable opportunity for video surveillance storage vendors whose platforms combine cloud archiving capability, hybrid retention architecture, and longer-period storage services tailored to the requirements of government agencies, smart cities, and infrastructure operators deploying increasingly data-intensive surveillance systems. This digital infrastructure opportunity is distinguished from conventional on-premise storage demand by its scalability potential, its recurring service revenue model characteristics, and its alignment with Thailand's most strategically important digital investment programs whose execution is creating progressively stronger commercial conditions for cloud-aware surveillance storage services across the country's most active deployment geographies.

The quantitative scale and investment specificity of this data center opportunity are documented with precision by the Board of Investment. Thailand's digital sector becomes the top-ranked investment sector in 2024 with 243.3 billion baht in pledged investment, confirming the institutional momentum behind the country's digital infrastructure expansion. Digital sector investment applications rise 20-fold in the first half of 2025 to 522.6 billion baht, while data center projects alone attract 521.2 billion baht across 28 projects, confirming that the physical infrastructure enabling scalable cloud surveillance storage services is expanding at an accelerating pace across Thailand's most commercially active digital geographies. Vendors that align their cloud archiving, redundancy, and extended retention service offerings with Thailand's expanding data center backbone and the government sector's growing platform integration priorities will capture disproportionate value from this structurally significant and policy-supported market opportunity over the forecast period.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Thailand Video Surveillance Storage Market Segmentation Analysis

By Storage Architecture

- Edge Storage

- Recorder-Based Storage

- DVR-Based Storage

- NVR-Based Storage

- Centralized On-Premises Storage

- Cloud Storage

- Hybrid Storage

The segment with highest market share under the Storage Architecture is Recorder-Based Storage, accounting for approximately 35% of the total market. This leading position reflects the deep structural alignment between recorder-based system characteristics and the specific footage management requirements of Thailand's most institutionally significant end user segments. Direct recording capability, local system control, structured retention management, and practical footage retrieval workflows make recorder-based configurations the reference storage architecture across government security operations, public facility surveillance, and infrastructure monitoring deployments throughout the country. With more than one-third of total market value concentrated within a single architecture category, Recorder-Based Storage defines the commercial priorities, system integration frameworks, and procurement evaluation criteria of the Thailand video surveillance storage market, establishing the reliability standards and workflow compatibility benchmarks against which all alternative storage architectures are assessed.

The structural leadership of Recorder-Based Storage is sustained by the operational practicality and deployment simplicity that have established this architecture as the default storage specification across the market's most volume-significant end user segments. As surveillance deployments in government facilities, smart city environments, and public safety networks expand in scale and complexity, the recorder-based format's established management discipline and controlled access characteristics continue to satisfy the footage retention and retrieval requirements of Thailand's most demanding institutional operators. The progressive broadening of Thailand's smart city rollout, documented by depa across 190 active promotion zones as of early 2026, creates consistent new installation demand for storage architectures whose operational reliability and deployment familiarity align with the practical management capabilities of expanding public-sector surveillance programs. The segment's structural market leadership is expected to remain comprehensively intact over the forecast period.

By End-User Vertical

- Commercial Buildings

- Retail and Hospitality

- Industrial and Warehousing

- Transport and Logistics

- Government Sector

- Critical Infrastructure and Utilities

- Healthcare

- Education

- Residential and Multi-Dwelling

The segment with highest market share under the End-User Vertical is the Government Sector, accounting for approximately 30% of the total market. This dominant position reflects the foundational role of public institutions in sustaining surveillance storage demand across administrative facilities, civic monitoring programs, and public safety infrastructure whose footage retention obligations create consistent and compounding storage capacity procurement requirements across national and municipal government operating environments. With nearly one-third of total market value anchored in government sector demand, this vertical defines the compliance requirements, retention policy frameworks, and system reliability standards of the Thailand video surveillance storage market, establishing the performance credibility threshold against which all storage solution providers are evaluated across the country's most institutionally significant procurement contexts.

The structural leadership of the Government Sector is being actively sustained by the accelerating pace of Thailand's public-sector digital transformation programs and smart city infrastructure expansion. Thailand's 2nd ASEAN ranking in the 2024 UN E-Government Development Index confirms the digital governance momentum that sustains consistent institutional investment in connected public-sector systems whose surveillance data management requirements drive expanding video storage procurement activity. The DGA's Thang Rath platform consolidating 197 government services by May 2025 confirms that public-sector digital integration is advancing at a pace that progressively elevates the operational importance of structured, secure, and centrally accessible surveillance footage retention across government agency environments. The Government Sector's position as the market's dominant commercial demand anchor is expected to deepen over the forecast period.

List of Companies Covered in Thailand Video Surveillance Storage Market

The companies listed below are highly influential in the Thailand video surveillance storage market, with a significant market share and a strong impact on industry developments.

- Uniview

- VIVOTEK

- i-PRO

- Hikvision

- Dahua Technology

- Axis Communications

- Bosch Security Systems

- Hanwha Vision

- IDIS

- Synology

Market News & Updates

- Axis Communications, 2025:

Axis Communications launched the AXIS Camera Station S1228 Rack AI Optimized Server, a recording server built for AI-based analytics and free-text search in AXIS Camera Station Pro; Axis said it includes an NVIDIA GPU, dual SSDs, 12 TB storage, and can handle up to 10 times more detections than a standard server, with search results appearing up to 1,000 times faster in busy scenes. For the Thailand video surveillance storage market, this is a highly relevant update because it raises the benchmark for recorder-based and centralized investigation workflows in high-traffic commercial and public environments where faster forensic search and higher ingest performance matter.

- Synology, 2026:

Synology’s Thai release notes for Surveillance Station 9.2.5-11979 added support for Sites in CMS to group recording servers together and introduced a new Site Admin privilege profile; Synology’s current Surveillance Station platform materials also emphasize simpler deployment, expanded AI-powered capabilities, and C2 Backup for Surveillance to keep a remote copy of recordings if the recording server is stolen or damaged. For the Thailand video surveillance storage market, this is a meaningful verified platform update because it strengthens multi-site administration, remote backup, and resilience for users moving from standalone NVR environments toward more centralized and hybrid surveillance storage models.

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- Thailand Video Surveillance Storage Market Policies, Regulations, and Standards

- Thailand Video Surveillance Storage Market Case Study

- Thailand Video Surveillance Storage Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- Thailand Video Surveillance Storage Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Storage Architecture

- Edge Storage- Market Insights and Forecast 2022-2032, USD Million

- Recorder-Based Storage- Market Insights and Forecast 2022-2032, USD Million

- DVR-Based Storage- Market Insights and Forecast 2022-2032, USD Million

- NVR-Based Storage- Market Insights and Forecast 2022-2032, USD Million

- Centralized On-Premises Storage- Market Insights and Forecast 2022-2032, USD Million

- Cloud Storage- Market Insights and Forecast 2022-2032, USD Million

- Hybrid Storage- Market Insights and Forecast 2022-2032, USD Million

- By End-User Vertical

- Commercial Buildings- Market Insights and Forecast 2022-2032, USD Million

- Retail and Hospitality- Market Insights and Forecast 2022-2032, USD Million

- Industrial and Warehousing- Market Insights and Forecast 2022-2032, USD Million

- Transport and Logistics- Market Insights and Forecast 2022-2032, USD Million

- Government Sector- Market Insights and Forecast 2022-2032, USD Million

- Critical Infrastructure and Utilities- Market Insights and Forecast 2022-2032, USD Million

- Healthcare- Market Insights and Forecast 2022-2032, USD Million

- Education- Market Insights and Forecast 2022-2032, USD Million

- Residential and Multi-Dwelling- Market Insights and Forecast 2022-2032, USD Million

- By Retention and Search Complexity

- Basic Operational Recording- Market Insights and Forecast 2022-2032, USD Million

- Standard Investigation-Centric Storage- Market Insights and Forecast 2022-2032, USD Million

- Analytics-Assisted Searchable Storage- Market Insights and Forecast 2022-2032, USD Million

- Evidence-Grade and Compliance-Sensitive Archival- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel

- Direct Sales- Market Insights and Forecast 2022-2032, USD Million

- System Integrators- Market Insights and Forecast 2022-2032, USD Million

- Value-Added Resellers- Market Insights and Forecast 2022-2032, USD Million

- Distributors- Market Insights and Forecast 2022-2032, USD Million

- Online Sales/E-Procurement- Market Insights and Forecast 2022-2032, USD Million

- Managed Service Providers/Cloud Partners- Market Insights and Forecast 2022-2032, USD Million

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Storage Architecture

- Market Size & Growth Outlook

- Thailand Edge Storage Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By End-User Vertical- Market Insights and Forecast 2022-2032, USD Million

- By Retention and Search Complexity- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Thailand Recorder-Based Storage Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By End-User Vertical- Market Insights and Forecast 2022-2032, USD Million

- By Retention and Search Complexity- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Thailand DVR-Based Storage Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By End-User Vertical- Market Insights and Forecast 2022-2032, USD Million

- By Retention and Search Complexity- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Thailand NVR-Based Storage Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By End-User Vertical- Market Insights and Forecast 2022-2032, USD Million

- By Retention and Search Complexity- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Thailand Centralized On-Premises Storage Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By End-User Vertical- Market Insights and Forecast 2022-2032, USD Million

- By Retention and Search Complexity- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Thailand Cloud Storage Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By End-User Vertical- Market Insights and Forecast 2022-2032, USD Million

- By Retention and Search Complexity- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Thailand Hybrid Storage Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By End-User Vertical- Market Insights and Forecast 2022-2032, USD Million

- By Retention and Search Complexity- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- Hikvision

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Dahua Technology

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Axis Communications

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Bosch Security Systems

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Hanwha Vision

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Uniview

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- VIVOTEK

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- i-PRO

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- IDIS

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Synology

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Hikvision

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Storage Architecture |

|

| By End-User Vertical |

|

| By Retention and Search Complexity |

|

| By Sales Channel |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.