Global Video Surveillance Storage Market Report: Trends, Growth and Forecast (2026-2032)

By Storage Architecture (Edge Storage, Recorder-Based Storage, DVR-Based Storage, NVR-Based Storage, Centralized On-Premises Storage, Cloud Storage, Hybrid Storage), By End-User Vertical (Commercial Buildings, Retail and Hospitality, Industrial and Warehousing, Transport and Logistics, Government Sector, Critical Infrastructure and Utilities, Healthcare, Education, Residential and Multi-Dwelling), By Retention and Search Complexity (Basic Operational Recording, Standard Investigation-Centric Storage, Analytics-Assisted Searchable Storage, Evidence-Grade and Compliance-Sensitive Archival), By Sales Channel (Direct Sales, System Integrators, Value-Added Resellers, Distributors, Online Sales/E-Procurement, Managed Service Providers/Cloud Partners), By Region (North America, South America, Europe, Middle East & Africa, Asia Pacific) ... Read more

|

Major Players

|

Global Video Surveillance Storage Market Statistics and Insights, 2026

- Market Size Statistics

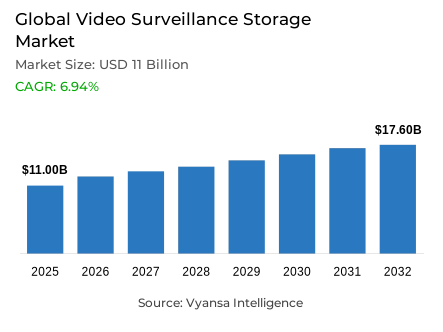

- Video surveillance storage market size in Global was valued at USD 11 billion in 2025 and is estimated at USD 11.8 billion in 2026.

- The market size is expected to grow to USD 17.6 billion by 2032.

- Market to register a CAGR of around 6.94% during 2026-32.

- Storage Architecture Shares

- Recorder-based storage grabbed market share of 35%.

- Competition

- More than 25 companies are actively engaged in producing video surveillance storage.

- Top 5 companies acquired around 40% of the market share.

- Hewlett Packard Enterprise (HPE), NetApp, Quantum, Seagate, Western Digital etc., are few of the top companies.

- End-User Vertical

- Government sector grabbed 25% of the market.

- Region

- Asia Pacific leads with a 45% share of the global market.

Global Video Surveillance Storage Market Outlook

The Global video surveillance storage market was valued at USD 11 billion in 2025, establishing a commercially stable and operationally well-anchored foundation within the world's most rapidly expanding public safety and physical security technology ecosystem. Projected to advance from USD 11.8 billion in 2026 to USD 17.6 billion by 2032, the sector registers a CAGR of 6.94% across the forecast horizon. This steady and structurally supported expansion trajectory reflects the sustained and growing institutional reliance on recorded video footage for security monitoring, incident investigation, operational oversight, and evidentiary documentation across public and private environments worldwide. Growth is anchored in genuine operational necessity rather than technology novelty adoption, giving this market a commercial resilience that sustains consistent storage capacity investment across diverse user segments and economic conditions.

The storage architecture defining this market's commercial structure is anchored in recorder-based configurations. Recorder-Based Storage commands approximately 35% of total storage architecture market share, reflecting the consistent and deeply embedded institutional preference for structured, locally managed footage capture and retention systems whose operational familiarity, retrieval practicality, and system control characteristics align naturally with the security management workflows of the market's most commercially significant user segments. This architecture concentration confirms that a large proportion of global video surveillance storage end users continue to prioritize proven, operationally predictable storage configurations whose management simplicity and reliability credentials sustain disproportionate procurement share across both new installation and system upgrade demand cycles.

The end-user architecture reinforces the structural centrality of the government sector as the category's dominant demand source. The Government Sector accounts for approximately 25% of total end-user vertical market share, reflecting the foundational role of public surveillance infrastructure in civic monitoring, transportation security, administrative facility protection, and public safety program management across national and municipal government deployments worldwide. The World Bank's documentation that 56% of the global population, equivalent to 4.4 billion people, lives in urban areas confirms the demographic concentration that sustains institutional demand for public-space surveillance infrastructure whose footage retention requirements generate consistent and compounding video storage capacity procurement across government user environments at every level of administrative organization.

The forward outlook is defined by four converging structural forces whose combined commercial impact creates a video surveillance storage market of sustained and well-grounded expansion momentum. The OECD's 2024 government innovation review, analyzing nearly 800 case studies from 83 countries, confirms that governments worldwide are actively investing in scalable digital infrastructure and emerging technologies including AI-enabled monitoring systems whose analytics requirements are progressively transforming the functional expectations placed on video surveillance storage platforms. The FBI's documentation of USD 16 billion in internet crime losses in 2024, a 33% increase from 2023, combined with CISA's June 2025 advisory highlighting vulnerabilities in connected camera systems, creates a security governance imperative that is simultaneously expanding storage investment and elevating the cyber resilience requirements that storage system providers must satisfy. The FedRAMP marketplace surpassing 400 authorized cloud products in April 2025 is progressively expanding the compliance-validated cloud storage ecosystem available to government and regulated enterprise end users. Asia Pacific's 45% global market share leadership establishes the geographic growth center around which competitive strategy and supply chain investment are organized over the forecast period.

Global Video Surveillance Storage Market Growth Driver

Urban Population Growth and Public Safety Digitization Sustain Institutional Storage Demand

The rapid and institutionally documented expansion of global urban populations combined with accelerating government investment in public safety digitization represents the primary structural driver of video surveillance storage demand, functioning as a persistent capacity expansion imperative that sustains consistent footage volume growth, retention requirement intensification, and storage system procurement investment across government and public infrastructure operator end user segments worldwide. As more of the world's population concentrates within urban environments whose civic monitoring, transportation security, and public space oversight requirements generate continuously expanding recorded footage volumes, the storage capacity requirements of institutional surveillance systems compound consistently, creating a structural demand expansion dynamic whose commercial implications for video surveillance storage procurement are direct, measurable, and durable across the forecast horizon.

The quantitative momentum of this urbanization and digitization-driven demand dynamic is documented with precision by the World Bank and OECD. The World Bank confirms that 56% of the global population, equivalent to 4.4 billion people, lives in urban areas, establishing the demographic concentration that sustains institutional demand for public-space surveillance infrastructure whose footage retention requirements generate consistent storage capacity procurement at scale. The OECD's 2024 government innovation review, analyzing nearly 800 case studies from 83 countries, confirms that governments worldwide are actively investing in scalable digital infrastructure and emerging technologies including AI-enabled surveillance and monitoring systems whose data generation requirements sustain expanding video storage capacity demand across diverse national and regional government contexts. These urbanization and digitization dynamics are expected to sustain structural video surveillance storage demand growth over the forecast period.

Global Video Surveillance Storage Market Challenge

Privacy Compliance and Cybersecurity Obligations Elevate Operational Complexity

The progressively more demanding privacy protection framework and cybersecurity threat environment surrounding video surveillance system operation represent the most consequential structural challenge confronting the global video surveillance storage market, creating systematic governance, retention policy management, access control, and cyber resilience investment burdens that elevate operational complexity and raise the compliance investment threshold for storage system procurement across the market's most institutionally significant end user segments. In an operating environment where video surveillance storage systems sit at the intersection of sensitive personal data capture, extended retention obligations, and networked system connectivity, the security and governance implications of inadequate configuration management and weak access controls are directly material to organizational risk profiles and regulatory compliance standing.

The structural depth and financial scale of this privacy and cybersecurity challenge are documented with authority by the European Data Protection Supervisor, the FBI, and CISA. The European Data Protection Supervisor confirms that badly designed video surveillance systems can intrude on privacy and infringe fundamental rights, while data minimization remains a core compliance obligation across surveillance system design and footage retention management. The FBI's 2024 Internet Crime Report documents 859,532 complaints of suspected internet crime with losses exceeding USD 16 billion, a 33% increase from 2023, confirming the escalating financial impact of cybersecurity threats across organizations whose networked surveillance systems represent potential attack surfaces. CISA's June 2025 advisory highlighting vulnerabilities affecting connected pan-tilt-zoom cameras directly implicates surveillance system security architecture as a material operational risk variable that storage system providers must address with proactive cyber resilience design. Navigating this challenge demands simultaneous investment in privacy-compliant retention architecture, cybersecurity-hardened access controls, and regulatory compliance documentation capability over the forecast period.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Global Video Surveillance Storage Market Trend

AI-Enabled Video Analytics Integration Redefines Storage System Functional Requirements

The accelerating integration of artificial intelligence and advanced video analytics capabilities into surveillance system architectures represents the defining structural trend reshaping video surveillance storage system design priorities, performance specifications, and competitive differentiation parameters across the global market. This AI integration trend is progressively transforming the functional role of video surveillance storage from passive footage archive into an active, analytics-ready data infrastructure layer whose performance characteristics must support rapid content search, automated event detection, and real-time analytical processing alongside traditional capacity and retention management requirements. The commercial implications of this functional transformation are significant, as storage system providers that cannot demonstrate AI-analytics integration readiness are progressively disadvantaged in competitive procurement evaluations among the market's most technically sophisticated end user segments.

The institutional momentum and technical specificity of this AI-enabled analytics trend are documented with authority by NIST and OECD. NIST's video analytics program currently runs two active evaluations specifically designed to extract information from video streams, confirming that the technical standards infrastructure supporting AI-enabled video content analysis is advancing at an institutional level that will progressively formalize performance expectations across government and regulated enterprise storage procurement contexts. The OECD's documentation that governments across 83 countries are actively investing in scalable digital infrastructure and emerging technologies including automation and AI confirms that public-sector surveillance system modernization is driving AI-analytics capability adoption at a geographic breadth and institutional commitment level that creates consistent demand expansion for storage platforms whose architecture supports intelligent monitoring workflows. As AI-enabled surveillance capabilities advance toward mainstream institutional adoption, storage system AI-readiness will transition from a competitive differentiator to a baseline procurement requirement over the forecast period.

Global Video Surveillance Storage Market Opportunity

Compliant Cloud Storage Ecosystem Expansion Creates Scalable Demand Access Pathways

The accelerating expansion of the FedRAMP-authorized cloud storage ecosystem, combined with the growing institutional comfort of government and regulated enterprise end users with cloud-based surveillance footage management, creates a structurally significant and commercially durable opportunity for video surveillance storage vendors whose platforms combine compliance validation credentials with the scalability, multi-site accessibility, and cost-efficiency advantages that cloud-based storage architectures deliver relative to conventional on-premise alternatives. This cloud compliance opportunity is distinguished by its direct and measurable market access implications for vendors whose FedRAMP authorization status transforms regulatory compliance from a procurement barrier into a competitive credential that opens access to the most institutionally significant and commercially valuable government end user segments.

The quantitative scale and programmatic momentum of this cloud compliance opportunity are documented with precision by FedRAMP. A total of 29 new cloud services were authorized in April 2025 alone, bringing the fiscal-year total to 73 and pushing the overall FedRAMP marketplace past 400 authorized products. This authorization pace confirms that the compliance-validated cloud ecosystem available to government surveillance storage end users is expanding at an accelerating rate that progressively improves the accessibility and deployment confidence of cloud-based storage solutions across public-sector procurement environments. The 26 cloud service providers participating in the FedRAMP 20x Phase One pilot program in August 2025, against a backdrop of fewer than 350 total authorizations across the program's prior ten-year history, confirms that authorization throughput is accelerating in ways that will continue expanding the compliant cloud storage product landscape accessible to government and regulated enterprise surveillance end users. Vendors that invest in FedRAMP authorization, cloud-hybrid storage architecture, and compliance-validated deployment frameworks will capture disproportionate value from this expanding and policy-supported market opportunity over the forecast period.

Global Video Surveillance Storage Market Regional Analysis

By Region

- North America

- South America

- Europe

- Middle East & Africa

- Asia Pacific

The segment with highest market share under the Region is Asia Pacific, accounting for approximately 45% of the total market. This dominant regional position reflects the convergence of the world's largest urban population concentration, the most extensive public surveillance infrastructure deployment programs, the highest concentration of smart city technology investment across key economies, and a manufacturing ecosystem that simultaneously drives surveillance technology innovation and maintains cost competitiveness across all product and storage system price tiers. With nearly half of total global market value concentrated within a single regional block, Asia Pacific defines the commercial scale, competitive intensity, and adoption trajectory parameters of the global video surveillance storage market.

The structural dominance of Asia Pacific is sustained by demand characteristics operating simultaneously across multiple commercial dimensions. Active large-scale surveillance infrastructure expansion among established deployments in China, Japan, South Korea, and Australia generates consistent storage capacity addition and upgrade demand across both government and enterprise end user segments. Rapid first-time surveillance system deployment momentum across high-growth emerging economies including India, Southeast Asia, and South Asia creates expanding new installation demand whose footage volume growth sustains consistent storage procurement activity. The World Bank's documentation of 56% global urbanization, heavily concentrated across Asia Pacific's rapidly expanding metropolitan areas, confirms the demographic pressure that sustains institutional demand for urban surveillance infrastructure whose storage requirements are compounding consistently across the region's most commercially active geographies. Asia Pacific's structural leadership as the global market's dominant demand anchor is expected to deepen over the forecast period.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Global Video Surveillance Storage Market Segmentation Analysis

By Storage Architecture

- Edge Storage

- Recorder-Based Storage

- DVR-Based Storage

- NVR-Based Storage

- Centralized On-Premises Storage

- Cloud Storage

- Hybrid Storage

The segment with highest market share under the Storage Architecture is Recorder-Based Storage, accounting for approximately 35% of the total market. This leading position reflects the deep structural alignment between recorder-based system characteristics and the specific footage management requirements of the market's most institutionally significant end user segments, where operational familiarity, direct recording capability, structured retention management, and practical footage retrieval workflows make recorder-based configurations the reference storage architecture across security operations centers, transportation monitoring environments, and facility-level surveillance deployments worldwide. With more than one-third of total market value concentrated within a single architecture category, Recorder-Based Storage defines the commercial priorities, system integration frameworks, and procurement evaluation criteria of the global video surveillance storage market.

The structural leadership of Recorder-Based Storage is sustained by the operational familiarity and deployment simplicity that have established this architecture as the default storage specification across the market's most volume-significant end user segments. As AI-enabled video analytics capabilities become more deeply integrated into surveillance system architectures, recorder-based platforms are progressively evolving to support searchable footage, faster analytical access, and performance levels suited to AI-augmented monitoring workflows. The NIST video analytics program's two active evaluations designed to extract information from video streams confirms that the technical integration between recording infrastructure and analytical capability is advancing at an institutional level that is progressively reshaping the functional requirements placed on recorder-based storage platforms. The segment's structural market leadership is expected to remain intact over the forecast period.

By End-User Vertical

- Commercial Buildings

- Retail and Hospitality

- Industrial and Warehousing

- Transport and Logistics

- Government Sector

- Critical Infrastructure and Utilities

- Healthcare

- Education

- Residential and Multi-Dwelling

The segment with highest market share under the end-user vertical is the government sector, accounting for approximately 25% of the total market. This dominant position reflects the foundational role of public surveillance infrastructure in civic monitoring, administrative security, transportation management, and public safety program delivery across national, regional, and municipal government deployments worldwide, where reliable footage retention, controlled access management, and consistent recording availability are non-negotiable operational requirements whose procurement scale generates disproportionate storage capacity investment relative to private sector end user segments of comparable organizational size. With one-quarter of total market value anchored in government sector demand, this end-user vertical defines the compliance requirements, retention policy frameworks, and system reliability standards of the global video surveillance storage market.

The structural leadership of the Government Sector is being actively sustained by the accelerating institutional investment in smart city infrastructure and public safety digitization across major urban centers worldwide. The GAO's documentation that smart city technologies integrate cameras and other sensors with communications equipment that transmits data for centralized analysis confirms the expanding scope of government surveillance system deployment whose footage generation rates and retention requirements create consistent and compounding video storage capacity demand. The OECD's analysis of nearly 800 government innovation case studies across 83 countries confirms that public-sector technology investment momentum is sustaining institutional surveillance infrastructure procurement across diverse national and regional government contexts. The Government Sector's position as the market's dominant commercial demand anchor is expected to deepen over the forecast period.

Market Players in Global Video Surveillance Storage Market

These market players maintain a significant presence in the Global video surveillance storage market sector and contribute to its ongoing evolution.

- Hewlett Packard Enterprise (HPE)

- NetApp

- Quantum

- Seagate

- Western Digital

- Synology

- QNAP

- Dell Technologies

- Huawei

- PROMISE Technology

- Infortrend

- Toshiba

- Hikvision

- Dahua Technology

- Hanwha Vision

Market News & Updates

- Seagate, 2026:

Seagate announced that its 32TB SkyHawk AI, Exos, and IronWolf Pro drives were shipping globally and positioned the launch around the surge in AI-driven video analytics, noting that organizations expect video data volumes to at least double over the next five years and that the new portfolio is designed to support searchable, decision-ready video intelligence from edge to cloud. For the global video surveillance storage market, this is one of the most important developments because it directly raises usable storage density for surveillance and AI-video workloads, helping operators retain more footage, manage richer metadata, and scale recorder-based and centralized storage without proportionally expanding hardware footprint

- QNAP, 2025:

QNAP officially launched its next-generation QVR Surveillance platform, which the company said delivers higher performance, greater reliability, advanced AI analytics, and integration with myQNAPcloud Surveillance storage, while supporting up to 1,024 channels, centralized multi-site management, dedicated cloud backup for compliance-oriented retention, and long-term archiving support. For the global video surveillance storage market, this is a major strategic update because it shows how storage is evolving from simple video retention into scalable, cloud-linked, analytics-assisted infrastructure that supports larger camera estates, stronger resilience, and more efficient evidence retrieval.

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- Global Video Surveillance Storage Market Policies, Regulations, and Standards

- Global Video Surveillance Storage Market Case Study

- Global Video Surveillance Storage Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- Global Video Surveillance Storage Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Storage Architecture

- Edge Storage- Market Insights and Forecast 2022-2032, USD Million

- Recorder-Based Storage- Market Insights and Forecast 2022-2032, USD Million

- DVR-Based Storage- Market Insights and Forecast 2022-2032, USD Million

- NVR-Based Storage- Market Insights and Forecast 2022-2032, USD Million

- Centralized On-Premises Storage- Market Insights and Forecast 2022-2032, USD Million

- Cloud Storage- Market Insights and Forecast 2022-2032, USD Million

- Hybrid Storage- Market Insights and Forecast 2022-2032, USD Million

- By End-User Vertical

- Commercial Buildings- Market Insights and Forecast 2022-2032, USD Million

- Retail and Hospitality- Market Insights and Forecast 2022-2032, USD Million

- Industrial and Warehousing- Market Insights and Forecast 2022-2032, USD Million

- Transport and Logistics- Market Insights and Forecast 2022-2032, USD Million

- Government Sector- Market Insights and Forecast 2022-2032, USD Million

- Critical Infrastructure and Utilities- Market Insights and Forecast 2022-2032, USD Million

- Healthcare- Market Insights and Forecast 2022-2032, USD Million

- Education- Market Insights and Forecast 2022-2032, USD Million

- Residential and Multi-Dwelling- Market Insights and Forecast 2022-2032, USD Million

- By Retention and Search Complexity

- Basic Operational Recording- Market Insights and Forecast 2022-2032, USD Million

- Standard Investigation-Centric Storage- Market Insights and Forecast 2022-2032, USD Million

- Analytics-Assisted Searchable Storage- Market Insights and Forecast 2022-2032, USD Million

- Evidence-Grade and Compliance-Sensitive Archival- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel

- Direct Sales- Market Insights and Forecast 2022-2032, USD Million

- System Integrators- Market Insights and Forecast 2022-2032, USD Million

- Value-Added Resellers- Market Insights and Forecast 2022-2032, USD Million

- Distributors- Market Insights and Forecast 2022-2032, USD Million

- Online Sales/E-Procurement- Market Insights and Forecast 2022-2032, USD Million

- Managed Service Providers/Cloud Partners- Market Insights and Forecast 2022-2032, USD Million

- By Region

- North America

- South America

- Europe

- Middle East & Africa

- Asia Pacific

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Storage Architecture

- Market Size & Growth Outlook

- North America Video Surveillance Storage Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Storage Architecture- Market Insights and Forecast 2022-2032, USD Million

- By End-User Vertical- Market Insights and Forecast 2022-2032, USD Million

- By Retention and Search Complexity- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Country

- US

- Canada

- Mexico

- Rest of North America

- US Video Surveillance Storage Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Storage Architecture- Market Insights and Forecast 2022-2032, USD Million

- By End-User Vertical- Market Insights and Forecast 2022-2032, USD Million

- By Retention and Search Complexity- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Canada Video Surveillance Storage Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Storage Architecture- Market Insights and Forecast 2022-2032, USD Million

- By End-User Vertical- Market Insights and Forecast 2022-2032, USD Million

- By Retention and Search Complexity- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Mexico Video Surveillance Storage Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Storage Architecture- Market Insights and Forecast 2022-2032, USD Million

- By End-User Vertical- Market Insights and Forecast 2022-2032, USD Million

- By Retention and Search Complexity- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Market Size & Growth Outlook

- South America Video Surveillance Storage Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Storage Architecture- Market Insights and Forecast 2022-2032, USD Million

- By End-User Vertical- Market Insights and Forecast 2022-2032, USD Million

- By Retention and Search Complexity- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Country

- Brazil

- Argentina

- Rest of South America

- Brazil Video Surveillance Storage Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Storage Architecture- Market Insights and Forecast 2022-2032, USD Million

- By End-User Vertical- Market Insights and Forecast 2022-2032, USD Million

- By Retention and Search Complexity- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Argentina Video Surveillance Storage Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Storage Architecture- Market Insights and Forecast 2022-2032, USD Million

- By End-User Vertical- Market Insights and Forecast 2022-2032, USD Million

- By Retention and Search Complexity- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Market Size & Growth Outlook

- Europe Video Surveillance Storage Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Storage Architecture- Market Insights and Forecast 2022-2032, USD Million

- By End-User Vertical- Market Insights and Forecast 2022-2032, USD Million

- By Retention and Search Complexity- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Country

- Germany

- UK

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Germany Video Surveillance Storage Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Storage Architecture- Market Insights and Forecast 2022-2032, USD Million

- By End-User Vertical- Market Insights and Forecast 2022-2032, USD Million

- By Retention and Search Complexity- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- UK Video Surveillance Storage Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Storage Architecture- Market Insights and Forecast 2022-2032, USD Million

- By End-User Vertical- Market Insights and Forecast 2022-2032, USD Million

- By Retention and Search Complexity- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- France Video Surveillance Storage Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Storage Architecture- Market Insights and Forecast 2022-2032, USD Million

- By End-User Vertical- Market Insights and Forecast 2022-2032, USD Million

- By Retention and Search Complexity- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Italy Video Surveillance Storage Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Storage Architecture- Market Insights and Forecast 2022-2032, USD Million

- By End-User Vertical- Market Insights and Forecast 2022-2032, USD Million

- By Retention and Search Complexity- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Spain Video Surveillance Storage Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Storage Architecture- Market Insights and Forecast 2022-2032, USD Million

- By End-User Vertical- Market Insights and Forecast 2022-2032, USD Million

- By Retention and Search Complexity- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Russia Video Surveillance Storage Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Storage Architecture- Market Insights and Forecast 2022-2032, USD Million

- By End-User Vertical- Market Insights and Forecast 2022-2032, USD Million

- By Retention and Search Complexity- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Market Size & Growth Outlook

- Middle East & Africa Video Surveillance Storage Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Storage Architecture- Market Insights and Forecast 2022-2032, USD Million

- By End-User Vertical- Market Insights and Forecast 2022-2032, USD Million

- By Retention and Search Complexity- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Country

- Saudi Arabia

- UAE

- South Africa

- Rest of Middle East & Africa

- Saudi Arabia Video Surveillance Storage Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Storage Architecture- Market Insights and Forecast 2022-2032, USD Million

- By End-User Vertical- Market Insights and Forecast 2022-2032, USD Million

- By Retention and Search Complexity- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- UAE Video Surveillance Storage Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Storage Architecture- Market Insights and Forecast 2022-2032, USD Million

- By End-User Vertical- Market Insights and Forecast 2022-2032, USD Million

- By Retention and Search Complexity- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- South Africa Video Surveillance Storage Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Storage Architecture- Market Insights and Forecast 2022-2032, USD Million

- By End-User Vertical- Market Insights and Forecast 2022-2032, USD Million

- By Retention and Search Complexity- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Market Size & Growth Outlook

- Asia Pacific Video Surveillance Storage Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Storage Architecture- Market Insights and Forecast 2022-2032, USD Million

- By End-User Vertical- Market Insights and Forecast 2022-2032, USD Million

- By Retention and Search Complexity- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Country

- China

- India

- Japan

- South Korea

- Australia

- Malaysia

- Thailand

- Indonesia

- Rest of Asia Pacific

- China Video Surveillance Storage Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Storage Architecture- Market Insights and Forecast 2022-2032, USD Million

- By End-User Vertical- Market Insights and Forecast 2022-2032, USD Million

- By Retention and Search Complexity- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- India Video Surveillance Storage Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Storage Architecture- Market Insights and Forecast 2022-2032, USD Million

- By End-User Vertical- Market Insights and Forecast 2022-2032, USD Million

- By Retention and Search Complexity- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Japan Video Surveillance Storage Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Storage Architecture- Market Insights and Forecast 2022-2032, USD Million

- By End-User Vertical- Market Insights and Forecast 2022-2032, USD Million

- By Retention and Search Complexity- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- South Korea Video Surveillance Storage Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Storage Architecture- Market Insights and Forecast 2022-2032, USD Million

- By End-User Vertical- Market Insights and Forecast 2022-2032, USD Million

- By Retention and Search Complexity- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Australia Video Surveillance Storage Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Storage Architecture- Market Insights and Forecast 2022-2032, USD Million

- By End-User Vertical- Market Insights and Forecast 2022-2032, USD Million

- By Retention and Search Complexity- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Malaysia Video Surveillance Storage Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Storage Architecture- Market Insights and Forecast 2022-2032, USD Million

- By End-User Vertical- Market Insights and Forecast 2022-2032, USD Million

- By Retention and Search Complexity- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Thailand Video Surveillance Storage Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Storage Architecture- Market Insights and Forecast 2022-2032, USD Million

- By End-User Vertical- Market Insights and Forecast 2022-2032, USD Million

- By Retention and Search Complexity- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Indonesia Video Surveillance Storage Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Storage Architecture- Market Insights and Forecast 2022-2032, USD Million

- By End-User Vertical- Market Insights and Forecast 2022-2032, USD Million

- By Retention and Search Complexity- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- Seagate

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Western Digital

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Synology

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- QNAP

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Dell Technologies

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Hewlett Packard Enterprise (HPE)

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- NetApp

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Quantum

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Huawei

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- PROMISE Technology

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Infortrend

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Toshiba

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Hikvision

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Dahua Technology

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Hanwha Vision

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Seagate

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Storage Architecture |

|

| By End-User Vertical |

|

| By Retention and Search Complexity |

|

| By Sales Channel |

|

| By Region |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.