South Africa Sleep Aids Market Report: Trends, Growth and Forecast (2026-2032)

By Product (Single Ingredient (Doxylamine Succinate, Diphenhydramine, Melatonin), Combination Ingredient (Diphenhydramine + Acetaminophen, Other Antihistamine-Based Combinations), Herbal & Traditional Sleep Aids (Valerian root, Passionflower, Chamomile, Kava, Multi-Herbal Sleep Blends)), By Sleep Disorder (Insomnia, Sleep Apnea, Restless Legs Syndrome, Narcolepsy, Sleep Walking, Others), By Age Group (Young to Mid Adults (25-44 Years), Middle-Aged Adults (45-64 Years), Geriatric Population (65+ Years)), By Sales Channel (Retail Online, Retail Offline), By End User (Homecare/Individual Consumers, Hospitals, Sleep Centers & Clinics), By Formulation (Tablets, Gummies, Capsules, Liquid, Sublingual), By Region (Gauteng, Western Cape, Eastern Cape, North West, Others) ... Read more

|

Major Players

|

South Africa Sleep Aids Market Statistics and Insights, 2026

- Market Size Statistics

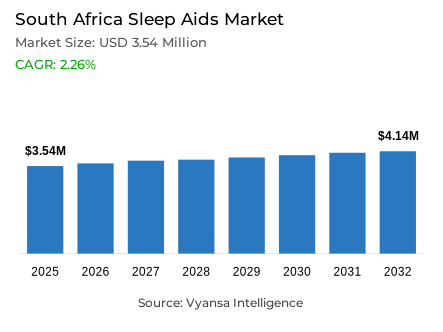

- Sleep aids market size in South Africa was estimated at USD 3.54 million in 2025

- The market size is expected to grow to USD 4.14 million by 2032.

- Market to register a CAGR of around 2.26% during 2026-32.

- Product Shares

- Melatonin grabbed market share of 40%.

- Competition

- More than 5 companies are actively engaged in producing sleep aids in South Africa.

- Top 3 companies acquired around 30% of the market share.

- GSK Consumer Healthcare, Aspen Pharmacare (Pty) Ltd, Adcock Ingram Holdings Ltd etc., are few of the top companies.

- Sales channel

- Retail offline grabbed 75% of the market.

South Africa Sleep Aids Market Outlook

The South Africa Sleep Aids Market size is estimated to be USD 3.54 million in 2025 and is expected to increase to USD 4.14 million in 2032 with a CAGR of approximately 2.26% over the forecast period. This trend is mainly caused by the high cost of living that has contributed to the rise in stress, anxiety, and depression among the local end users. Moreover, the long-term use of blue light on digital screens interferes with circadian rhythms, which is why many people are willing to find over-the-counter remedies in chained pharmacies to enhance their sleep.

In this landscape, melatonin has a market share of 40%, but herbal and traditional formulations prevail because of the preference to natural ingredients. A large portion of South Africans are still distrustful of chemical-based solutions and instead tend to prefer products with ashwagandha or CBD to prevent the perceived risk of addiction. These natural sleep products are finding considerable shelf space in health and personal-care retail outlets as brand education is eliminating the negative connotations that have existed in the past regarding cannabis-derived compounds.

Purchasing habits are also influenced by the regulatory environment, with many opting to use easier to obtain herbal substitutes due to stringent regulations on dispensing specific drugs. Although retail offline takes up 75 per cent of the market, the ease of not having to stand in queues to get dispensing services at the pharmacist still favours the expansion of non-prescription categories. Mid-to-high-income earners might continue to seek professional psychiatric assistance, yet the overall population is turning to these readily available wellness products to help them deal with their nighttime habits.

In the future, the category will have new entrants in the form of holistic lifestyle changes and wearable technology that monitors heart rates and sleeping habits. With the increase in mental-health awareness, the number of individuals utilizing mobile applications and free online services to minimize long-term dependence on conventional sleep-aid methods by engaging in regular physical activity and stress-reduction strategies is on the rise. Although these changes have been made towards behavioral changes, the market is still set to experience a consistent growth as the residents still focus on the effective ways to overcome the physical impact of a high-pressure economic environment.

South Africa Sleep Aids Market Growth Driver

Cost-of-Living Stress Sustains Affordable Sleep Aid Demand

Ongoing financial strain and day-to-day anxiety are reinforcing demand for affordable and accessible sleep solutions across South Africa. As disposable incomes remain constrained, many end users prioritise practical, retail-available products to manage stress-related sleep disruption rather than pursuing formal mental health pathways. Sleep aids therefore function as low-barrier coping tools in a climate of economic uncertainty.

According to Statistics South Africa, annual end user inflation measured 3.5% in November 2025, while food and non-alcoholic beverages inflation reached 4.4%. Persistent cost pressures intensify financial stress across households, indirectly sustaining demand for accessible over-the-counter sleep support products positioned as affordable wellness aids.

South Africa Sleep Aids Market Challenge

Prescription Pathways Split Market by Income Tier

End users who have the financial means to seek assistance tend to turn to professional assistance when sleep issues persist. The psychologist and psychiatrist routes generally entail controlled dosing and prescription products, which divert demand to over-the-counter and herbal products among the middle-to-high-income populations, and access barriers leave the lower-income end users with little choice but to follow the retail pharmacy routes.

Statistics South Africa reports that the official unemployment rate was 31.4% in Q4 2025, which emphasizes the prevalence of affordability limitations to formal healthcare and strengthens the dependence on retail pharmacy purchases. Nevertheless, prescription options remain intensively competitive where clinical access is available, forming a structurally divided market where growth opportunities and channel dynamics are not evenly distributed across income levels up to 2032.

Unlock Market Intelligence

Explore the market potential with our data-driven report

South Africa Sleep Aids Market Trend

Regulatory Scheduling Reinforces Herbal Preference Bias

There is an evident market trend whereby the timing of the regulation promotes the use of milder solutions by the end users and enhances the position of herbal and traditional sleep aids. In regions where OTC drugs are more tightly regulated, such as pharmacist dispensing and purchase tracking, a large proportion of shoppers will tend to favor formats that seem easier to use and more natural, continuing to give herbal-based sleep products a strong push.

South Africa, in its consolidated schedules of August 2025, as published by the Department of Health and SAHPRA, schedules melatonin under jet-lag use in a maximum dose of 6mg/day. This regulatory stance explains why more robust sleep solutions are still kept under stricter regulation, which supports a larger market bias in favor of non-prescription and herbal solutions that end users can more easily and confidently obtain.

South Africa Sleep Aids Market Opportunity

CBD Regulation Opens Compliant Shelf Expansion Route

CBD is becoming a more relaxation-oriented substitute, and its rising presence in health and personal-care retail offers a viable growth opportunity to sleep-support adjacencies, such as oils, supplements, and relaxing blends. With end users getting better acquainted with CBD via education and in-store merchandising, brands can grow sleep and unwind propositions without the need to use traditional sedative cues, especially among shoppers who are looking to use non-habit-forming products.

Under low-risk claims, cannabidiol is exempt in some complementary medicines with a maximum daily dose of 20mg that contain not more than 600mg per sales pack under low-risk claims as of August 2025 as per the consolidated schedules of the Department of Health and SAHPRA. This regulatory transparency offers a clear compliance framework that facilitates broader product implementation and scalable retail distribution by 2032.

Unlock Market Intelligence

Explore the market potential with our data-driven report

South Africa Sleep Aids Market Segmentation Analysis

By Product

- Single Ingredient

- Doxylamine Succinate

- Diphenhydramine

- Melatonin

- Combination Ingredient

- Diphenhydramine + Acetaminophen

- Other Antihistamine-Based Combinations

- Herbal & Traditional Sleep Aids

- Valerian root

- Passionflower

- Chamomile

- Kava

- Multi-Herbal Sleep Blends

The segment with highest market share under Product is Melatonin, which has about 40% of the total market. This leadership is anchored by the fact that end users have a high level of familiarity with melatonin as a direct and purpose-built sleep ingredient, and that it is highly compatible with short-term sleep disruption applications like stress-heavy periods, irregular routines, and screen-driven late nights that are becoming increasingly prevalent across South African urban demographics.

Although herbal and traditional substitutes compete on the natural positioning and attractiveness to shoppers with dependency or side effects concerns, the obvious functional connection of melatonin to sleep support keeps the product category at the top of the purchase list. This end user awareness has allowed the brands to have a consistent repeat demand via pharmacy and broader retail outlets, which strengthens the category leadership of melatonin through 2032.

By Sales Channel

- Retail Online

- Retail Offline

The Retail Offline segment, which is the largest segment in the sales channel, has a market share of about 75 % of the total market. In-store buying is still the leading method because a large number of customers like the advice of the pharmacist, reassurance of the product, and instant access, especially when sleep loss is interfering with normal functioning and the end user needs a solution without the delay that comes with online delivery.

There is also offline retail that is advantaged by the highly habitual shopping behaviour in chained pharmacies and general retail stores where sleep aids are sold alongside vitamins and other wellness products. Point-of-sale visibility and staff recommendation will help in high conversion rates, and end users who do not feel comfortable with the behind-the-counter processes of some products often change to shelf-available products. This dynamic will keep offline retail as the main volume driver even as online channel growth increases gradually until 2032.

List of Companies Covered in South Africa Sleep Aids Market

The companies listed below are highly influential in the South Africa sleep aids market, with a significant market share and a strong impact on industry developments.

- GSK Consumer Healthcare

- Aspen Pharmacare (Pty) Ltd

- Adcock Ingram Holdings Ltd

Competitive Landscape

South Africa sleep aids market continues to expand, driven by elevated stress linked to high living costs and prolonged exposure to blue light from digital devices, both of which disrupt sleep cycles. Consumers without access to private mental health services often turn to OTC options available through major pharmacy chains such as Clicks. Herbal and traditional sleep aids dominate sales, reflecting a perception of being safer and less habit-forming than chemical-based alternatives. Brands such as GNC and Himalaya benefit from demand for ingredients like ashwagandha. Over the forecast period, CBD products are expected to gain shelf presence, although stricter OTC regulations and rising adoption of holistic sleep-management tools may moderate conventional product growth.

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- South Africa Sleep Aids Market Policies, Regulations, and Standards

- South Africa Sleep Aids Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- South Africa Sleep Aids Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Product

- Single Ingredient- Market Insights and Forecast 2022-2032, USD Million

- Doxylamine Succinate- Market Insights and Forecast 2022-2032, USD Million

- Diphenhydramine- Market Insights and Forecast 2022-2032, USD Million

- Melatonin- Market Insights and Forecast 2022-2032, USD Million

- Combination Ingredient- Market Insights and Forecast 2022-2032, USD Million

- Diphenhydramine + Acetaminophen- Market Insights and Forecast 2022-2032, USD Million

- Other Antihistamine-Based Combinations- Market Insights and Forecast 2022-2032, USD Million

- Herbal & Traditional Sleep Aids- Market Insights and Forecast 2022-2032, USD Million

- Valerian root- Market Insights and Forecast 2022-2032, USD Million

- Passionflower- Market Insights and Forecast 2022-2032, USD Million

- Chamomile- Market Insights and Forecast 2022-2032, USD Million

- Kava- Market Insights and Forecast 2022-2032, USD Million

- Multi-Herbal Sleep Blends- Market Insights and Forecast 2022-2032, USD Million

- Single Ingredient- Market Insights and Forecast 2022-2032, USD Million

- By Sleep Disorder

- Insomnia- Market Insights and Forecast 2022-2032, USD Million

- Sleep Apnea- Market Insights and Forecast 2022-2032, USD Million

- Restless Legs Syndrome- Market Insights and Forecast 2022-2032, USD Million

- Narcolepsy- Market Insights and Forecast 2022-2032, USD Million

- Sleep Walking- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By Age Group

- Young to Mid Adults (25-44 Years)- Market Insights and Forecast 2022-2032, USD Million

- Middle-Aged Adults (45-64 Years)- Market Insights and Forecast 2022-2032, USD Million

- Geriatric Population (65+ Years)- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel

- Retail Online- Market Insights and Forecast 2022-2032, USD Million

- Retail Offline- Market Insights and Forecast 2022-2032, USD Million

- By End User

- Homecare/Individual Consumers- Market Insights and Forecast 2022-2032, USD Million

- Hospitals- Market Insights and Forecast 2022-2032, USD Million

- Sleep Centers & Clinics- Market Insights and Forecast 2022-2032, USD Million

- By Formulation

- Tablets- Market Insights and Forecast 2022-2032, USD Million

- Gummies- Market Insights and Forecast 2022-2032, USD Million

- Capsules- Market Insights and Forecast 2022-2032, USD Million

- Liquid- Market Insights and Forecast 2022-2032, USD Million

- Sublingual- Market Insights and Forecast 2022-2032, USD Million

- By Region

- Gauteng

- Western Cape

- Eastern Cape

- North West

- Others

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Product

- Market Size & Growth Outlook

- South Africa Single Ingredient Sleep Aids Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Sleep Disorder- Market Insights and Forecast 2022-2032, USD Million

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- By Formulation- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- South Africa Combination Ingredient Sleep Aids Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Sleep Disorder- Market Insights and Forecast 2022-2032, USD Million

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- By Formulation- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- South Africa Herbal & Traditional Sleep Aids Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Sleep Disorder- Market Insights and Forecast 2022-2032, USD Million

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- By Formulation- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- Aspen Pharmacare (Pty) Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Adcock Ingram Holdings Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- GSK Consumer Healthcare

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Pfizer Laboratories (Pty) Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Others

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Aspen Pharmacare (Pty) Ltd

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Product |

|

| By Sleep Disorder |

|

| By Age Group |

|

| By Sales Channel |

|

| By End User |

|

| By Formulation |

|

| By Region |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.