South Africa Bags and Luggage Market Report: Trends, Growth and Forecast (2026-2032)

By Category (Bags (Cross Body Bags, Bags and Backpacks, Business Bags, Duffle Bags, Clutches, Others), Luggage (Soft Luggage, Hard Luggage, Wheeled Luggage, Non-Wheeled Luggage)), By Sales Channel (Retail Offline, Retail Online), By Material Type (Soft Case (Nylon, Polyester, Ballistic Nylon), Hard Case (Polycarbonate, ABS (Acrylonitrile Butadiene Styrene), Polypropylene)), By Price Category (Luxury, Mass/Economy, Premium), By Application (Travel, Business), By Region (Gauteng, Western Cape, Eastern Cape, North West, Others) ... Read more

|

Major Players

|

South Africa Bags and Luggage Market Statistics and Insights, 2026

- Market Size Statistics

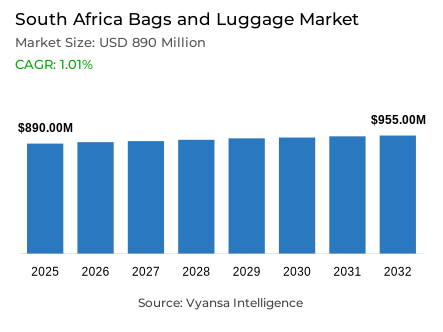

- Bags and luggage market size in South Africa was estimated at USD 890 million in 2025.

- The market size is expected to grow to USD 955 million by 2032.

- Market to register a CAGR of around 1.01% during 2026-32.

- Category Shares

- Bags grabbed market share of 90%.

- Competition

- More than 20 companies are actively engaged in producing bags and luggage in South Africa.

- Top 5 companies acquired around 20% of the market share.

- Edcon Holdings Ltd, Mr Price Group Ltd, Truworths International Ltd, Busby Trading SA (Pty) Ltd, Woolworths Holdings Ltd (South Africa) etc., are few of the top companies.

- Sales Channel

- Retail offline grabbed 95% of the market.

South Africa Bags and Luggage Market Outlook

The South Africa bags and luggage market is estimated at USD 890 million in 2025 and is projected to reach USD 955 million by 2032, registering a CAGR of around 1.01% during 2026–32. Growth over the forecast period will remain subdued, reflecting a prolonged period of end user caution driven by high living costs, unemployment pressures, and constrained disposable incomes. Bags and luggage are widely perceived as discretionary items, resulting in delayed purchases and a strong focus on affordability.

Bags will continue to dominate the market, supported by their everyday relevance and lower replacement costs compared to luggage. end user, particularly younger and price-sensitive shoppers, are increasingly trading down to entry-level and fast-fashion alternatives. Retailers are responding by shortening product development cycles and rapidly introducing trend-led designs to meet demand for instant gratification. Popular formats such as compact crossbody and camera-style bags highlight the importance of fashion relevance even in a low-growth environment.

Competition from low-cost international platforms has reshaped end user expectations around pricing and variety. While this intensifies pressure on local retailers, it has also accelerated differentiation strategies, particularly among local premium brands that emphasise craftsmanship, leather quality, and African-inspired design. At the same time, pre-loved bags are gaining traction as end user seek value-driven and sustainable options, especially within the luxury segment.

Retail offline will remain the backbone of the market, reflecting South Africa’s strong mall culture and preference for in-store product assessment. Although retail online will grow gradually, physical retail is expected to continue dominating sales, supported by improved in-store experiences and selective digital enhancements.

South Africa Bags and Luggage Market Growth Driver

Revived travel activity supporting luggage demand

In South Africa, the resurgence of travel, both domestic and international, remains a fundamental driver for increased luggage demand. According to the latest data, 2024 saw a 14.5% increase in international arrivals, boosting the need for durable, ergonomic luggage.

As travel activity rebounds, end users are investing in luggage that balances performance with aesthetic appeal. This demand is further supported by the growing trend of short-haul and impulse travel, where versatility and lightness in products like backpacks and duffels are preferred, positioning luggage as an essential part of modern, mobile lifestyles.

South Africa Bags and Luggage Market Challenge

Inflationary pressures and shifting lifestyles challenge spending behaviour

South Africa faces inflationary pressures which are slowing the growth of bags and luggage sales. The 2023 inflation rate stood at 5.9%, creating increased caution among end users, particularly the middle- and low-income segments. Price sensitivity is becoming more pronounced, as end users are focusing on more affordable, entry-level products.

Additionally, the demand for traditional business bags is declining due to hybrid and remote work patterns, reducing the need for formal work-specific bags. As a result, brands must focus on offering value-oriented products, while also adapting to changing lifestyle preferences.

Unlock Market Intelligence

Explore the market potential with our data-driven report

South Africa Bags and Luggage Market Trend

Casualisation and immersive retail shaping consumer engagement

The demand for handbags in South Africa is increasingly polarised, reflecting shifting end user values. While luxury handbags are growing at 14%, non-luxury options are also experiencing strong growth, at 11%. end users are placing greater importance on personal expression and quality, driving demand for premium bags and encouraging brands to offer more diverse collections.

At the same time, affordable, stylish everyday bags continue to thrive in response to changing economic conditions and growing awareness of fashion trends. This segmentation strengthens overall handbag demand and showcases the bifurcation between high-end and budget-conscious buyers.

South Africa Bags and Luggage Market Opportunity

Omnichannel integration and multifunctionality opening growth avenues

The second-hand luxury market is an emerging growth area, particularly as end users seek affordable, sustainable alternatives to new high-end products. Platforms like Yaga and Luxity are gaining traction by offering pre-loved luxury bags at more accessible price points.

Additionally, the growth of retail online is revolutionizing end user buying patterns, with grocery-led platforms and on-demand services increasingly popular. Brands are responding with omnichannel strategies, integrating digital convenience with physical retail experiences to enhance end user engagement and improve sales potential.

Unlock Market Intelligence

Explore the market potential with our data-driven report

South Africa Bags and Luggage Market Segmentation Analysis

By Category

- Bags

- Cross Body Bags

- Bags and Backpacks

- Business Bags

- Duffle Bags

- Clutches

- Others

- Luggage

- Soft Luggage

- Hard Luggage

- Wheeled Luggage

- Non-Wheeled Luggage

The segment with the highest share under the category is bags, accounting for around 90% of the market. This dominance is driven by the frequent and practical use of bags across daily activities, including work, leisure, and social occasions. Unlike luggage, which is replaced infrequently, bags benefit from higher purchase frequency and stronger alignment with fashion trends.

Handbags and casual bags form the core of this segment, particularly entry-level and mid-priced options that appeal to cost-conscious end user. Trend-led designs at accessible prices have become critical, enabling retailers to maintain volumes despite weak discretionary spending. Crossbody and compact bags are especially popular, as they balance style with practicality. While premium bags hold aspirational appeal, overall category performance is anchored by affordable offerings, ensuring bags retain their leading position throughout the forecast period.

By Sales Channel

- Retail Offline

- Retail Online

The segment with the highest share under the sales channel is retail offline, holding around 95% of the market. Physical stores remain the preferred purchasing channel, as end user value the ability to assess size, material quality, and comfort before buying. South Africa’s strong shopping mall culture further reinforces the dominance of offline retail.

Department stores, fashion chains, and specialist bag retailers continue to attract steady footfall, particularly for replacement purchases. While online platforms are expanding and improving product presentation, trust and tactile evaluation remain key factors influencing purchasing decisions. Over the forecast period, retail offline is expected to maintain its leading position, supported by selective omnichannel strategies that enhance convenience without undermining in-store engagement.

List of Companies Covered in South Africa Bags and Luggage Market

The companies listed below are highly influential in the South Africa bags and luggage market, with a significant market share and a strong impact on industry developments.

- Edcon Holdings Ltd

- Mr Price Group Ltd

- Truworths International Ltd

- Busby Trading SA (Pty) Ltd

- Woolworths Holdings Ltd (South Africa)

- Foschini Group Ltd

- Cape Union Mart Group

- Louis Vuitton South Africa (Pty) Ltd

- Slam Industries LLC

- Super Brands (Pty) Ltd

Competitive Landscape

South Africa bags and luggage market remains highly fragmented, characterised by intense price competition and a widening gap between low-cost imports and differentiated local brands. Global fast-fashion platforms such as Shein and Temu have reshaped competitive dynamics by offering trendy designs at very low prices, forcing local retailers to accelerate product launches and introduce more entry-level ranges. At the same time, local brands are increasingly focusing on differentiation and premiumisation to defend margins. Artisanal and premium players such as Okapi and Hamethop emphasise quality leather, African-inspired design, and craftsmanship, while mid-priced brands like sak.sak stand out through distinctive branding and locally resonant product naming. Alongside this, the rise of pre-loved platforms such as Yaga and Luxity is adding another competitive layer, particularly within the luxury segment.

Frequently Asked Questions

Related Report

1. Market Segmentation

1.1. Research Scope

1.2. Research Methodology

1.3. Definitions and Assumptions

2. Executive Summary

3. South Africa Bags and Luggage Market Policies, Regulations, and Standards

4. South Africa Bags and Luggage Market Dynamics

4.1. Growth Factors

4.2. Challenges

4.3. Trends

4.4. Opportunities

5. South Africa Bags and Luggage Market Statistics, 2022-2032F

5.1. Market Size & Growth Outlook

5.1.1.By Revenues in USD Million

5.1.2.By Units Sold in Thousand Units

5.2. Market Segmentation & Growth Outlook

5.2.1.By Category

5.2.1.1. Bags- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.1. Cross Body Bags- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.2. Bags and Backpacks- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.3. Business Bags- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.4. Duffle Bags- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.5. Clutches- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.6. Others- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2. Luggage- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2.1. Soft Luggage- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2.2. Hard Luggage- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2.3. Wheeled Luggage- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2.4. Non-Wheeled Luggage- Market Insights and Forecast 2022-2032, USD Million

5.2.2.By Sales Channel

5.2.2.1. Retail Offline- Market Insights and Forecast 2022-2032, USD Million

5.2.2.2. Retail Online- Market Insights and Forecast 2022-2032, USD Million

5.2.3.By Material Type

5.2.3.1. Soft Case- Market Insights and Forecast 2022-2032, USD Million

5.2.3.1.1. Nylon- Market Insights and Forecast 2022-2032, USD Million

5.2.3.1.2. Polyester- Market Insights and Forecast 2022-2032, USD Million

5.2.3.1.3. Ballistic Nylon- Market Insights and Forecast 2022-2032, USD Million

5.2.3.2. Hard Case- Market Insights and Forecast 2022-2032, USD Million

5.2.3.2.1. Polycarbonate- Market Insights and Forecast 2022-2032, USD Million

5.2.3.2.2. ABS (Acrylonitrile Butadiene Styrene)- Market Insights and Forecast 2022-2032, USD Million

5.2.3.2.3. Polypropylene- Market Insights and Forecast 2022-2032, USD Million

5.2.4.By Price Category

5.2.4.1. Luxury- Market Insights and Forecast 2022-2032, USD Million

5.2.4.2. Mass/Economy- Market Insights and Forecast 2022-2032, USD Million

5.2.4.3. Premium- Market Insights and Forecast 2022-2032, USD Million

5.2.5.By Application

5.2.5.1. Travel- Market Insights and Forecast 2022-2032, USD Million

5.2.5.2. Business- Market Insights and Forecast 2022-2032, USD Million

5.2.6.By Region

5.2.6.1. Gauteng

5.2.6.2. Western Cape

5.2.6.3. Eastern Cape

5.2.6.4. North West

5.2.6.5. Others

5.2.7.By Competitors

5.2.7.1. Competition Characteristics

5.2.7.2. Market Share & Analysis

6. South Africa Bags Market Statistics, 2022-2032

6.1. Market Size & Growth Outlook

6.1.1.By Revenues in USD Million

6.1.2.By Units Sold in Thousand Units

6.2. Market Segmentation & Growth Outlook

6.2.1.By Category- Market Insights and Forecast 2022-2032, USD Million

6.2.2.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

6.2.3.By Material Type- Market Insights and Forecast 2022-2032, USD Million

6.2.4.By Price Category- Market Insights and Forecast 2022-2032, USD Million

6.2.5.By Application- Market Insights and Forecast 2022-2032, USD Million

6.2.6.By Region- Market Insights and Forecast 2022-2032, USD Million

7. South Africa Luggage Market Statistics, 2022-2032

7.1. Market Size & Growth Outlook

7.1.1.By Revenues in USD Million

7.1.2.By Units Sold in Thousand Units

7.2. Market Segmentation & Growth Outlook

7.2.1.By Category- Market Insights and Forecast 2022-2032, USD Million

7.2.2.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

7.2.3.By Material Type- Market Insights and Forecast 2022-2032, USD Million

7.2.4.By Price Category- Market Insights and Forecast 2022-2032, USD Million

7.2.5.By Application- Market Insights and Forecast 2022-2032, USD Million

7.2.6.By Region- Market Insights and Forecast 2022-2032, USD Million

8. Competitive Outlook

8.1. Company Profiles

8.1.1.Busby Trading SA (Pty) Ltd

8.1.1.1. Business Description

8.1.1.2. Product Portfolio

8.1.1.3. Collaborations & Alliances

8.1.1.4. Recent Developments

8.1.1.5. Financial Details

8.1.1.6. Others

8.1.2.Woolworths Holdings Ltd

8.1.2.1. Business Description

8.1.2.2. Product Portfolio

8.1.2.3. Collaborations & Alliances

8.1.2.4. Recent Developments

8.1.2.5. Financial Details

8.1.2.6. Others

8.1.3.The Foschini Group Ltd

8.1.3.1. Business Description

8.1.3.2. Product Portfolio

8.1.3.3. Collaborations & Alliances

8.1.3.4. Recent Developments

8.1.3.5. Financial Details

8.1.3.6. Others

8.1.4.Cape Union Mart Group

8.1.4.1. Business Description

8.1.4.2. Product Portfolio

8.1.4.3. Collaborations & Alliances

8.1.4.4. Recent Developments

8.1.4.5. Financial Details

8.1.4.6. Others

8.1.5.Louis Vuitton South Africa (Pty) Ltd

8.1.5.1. Business Description

8.1.5.2. Product Portfolio

8.1.5.3. Collaborations & Alliances

8.1.5.4. Recent Developments

8.1.5.5. Financial Details

8.1.5.6. Others

8.1.6.Edcon Holdings Ltd

8.1.6.1. Business Description

8.1.6.2. Product Portfolio

8.1.6.3. Collaborations & Alliances

8.1.6.4. Recent Developments

8.1.6.5. Financial Details

8.1.6.6. Others

8.1.7.Mr Price Group Ltd

8.1.7.1. Business Description

8.1.7.2. Product Portfolio

8.1.7.3. Collaborations & Alliances

8.1.7.4. Recent Developments

8.1.7.5. Financial Details

8.1.7.6. Others

8.1.8.Truworths International Ltd

8.1.8.1. Business Description

8.1.8.2. Product Portfolio

8.1.8.3. Collaborations & Alliances

8.1.8.4. Recent Developments

8.1.8.5. Financial Details

8.1.8.6. Others

8.1.9.Slam Industries LLC

8.1.9.1. Business Description

8.1.9.2. Product Portfolio

8.1.9.3. Collaborations & Alliances

8.1.9.4. Recent Developments

8.1.9.5. Financial Details

8.1.9.6. Others

8.1.10. Super Brands (Pty) Ltd

8.1.10.1. Business Description

8.1.10.2. Product Portfolio

8.1.10.3. Collaborations & Alliances

8.1.10.4. Recent Developments

8.1.10.5. Financial Details

8.1.10.6. Others

9. Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Category |

|

| By Sales Channel |

|

| By Material Type |

|

| By Price Category |

|

| By Application |

|

| By Region |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.