Russia Room Air Conditioners Market Report: Trends, Growth and Forecast (2026-2032)

By Product Type (Split Air Conditioners (Up to 9,000 BTU/h, 9,001-12,000 BTU/h, 12,001-18,000 BTU/h, 18,001-24,000 BTU/h, Above 24,000 BTU/h), Window Air Conditioners (Up to 9,000 BTU/h, 9,001-12,000 BTU/h, 12,001-18,000 BTU/h, 18,001-24,000 BTU/h, Above 24,000 BTU/h), Others), By Technology (Inverter, Non-Inverter), By Price (Up to USD 300, USD 301 to USD 600, USD 601 to USD 1,000, Above USD 1,000), By End User (Residential (Individual Households, Apartments/Condominiums, Vacation/Secondary Homes), Commercial (Offices, Retail Stores/Showrooms, Hospitality, Healthcare Facilities, Educational Institutions, Small Commercial Establishments, Others)), By Sales Channel (Retail Online (Brand-Owned Websites/D2C, E-Commerce Marketplaces), Retail Offline (Exclusive Brand Stores, Multi-Brand Electronics & Appliance Stores, Specialty Stores, Hypermarkets/Supermarkets, Home Improvement Stores, Dealer/Distributor Network, Direct Sales/Institutional Sales, Local Independent Retailers)), By Refrigerant Type (R-32, R-410A, R-290, R-454B, Others), By Connectivity (Smart/Connected, Conventional/Non-Smart), By Energy Efficiency (1 Star, 2 Star, 3 Star, 4 Star, 5 Star) ... Read more

|

Major Players

|

Russia Room Air Conditioners Market Statistics and Insights, 2026

- Market Size Statistics

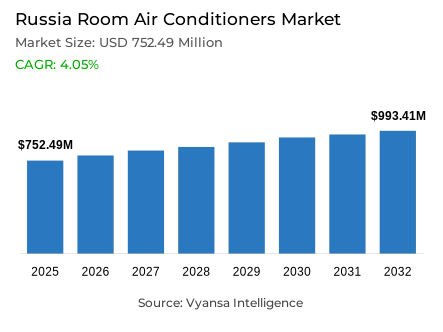

- Room air conditioners market size in Russia was valued at USD 752.49 million in 2025 and is estimated at USD 830.01 million in 2026.

- The market size is expected to grow to USD 993.41 million by 2032.

- Market to register a CAGR of around 4.05% during 2026-32.

- Product Type Shares

- Split air conditioners grabbed market share of 85%.

- Competition

- More than 10 companies are actively engaged in producing room air conditioners in Russia.

- Top 5 companies acquired around 95% of the market share.

- Ballu Industrial Group, AUX Group Co Ltd, Electrolux AB, Haier Group, Midea Group Co Ltd etc., are few of the top companies.

- End User

- Residential grabbed 75% of the market.

Russia Room Air Conditioners Market Outlook

The Russia room air conditioners market was valued at USD 752.49 million in 2025, establishing a commercially substantial foundation within one of Eastern Europe's largest and most structurally complex residential cooling appliance ecosystems. Projected to advance from USD 830.01 million in 2026 to USD 993.41 million by 2032, the sector registers a compound annual growth rate of approximately 4.05% across the forecast horizon a measured but structurally supported expansion trajectory reflecting the convergence of recurring summer heat intensity, rising household comfort expectations, and a vast residential dwelling base that collectively sustain consistent room air conditioner demand across Russia's geographically diverse urban and semi-urban housing geography.

The product architecture defining this market's commercial structure is characterized by pronounced format concentration within the split system category. Split air conditioners command approximately 85% of total product share a near-dominant position reflecting sustained consumer and installer preference for fixed, room-level cooling systems whose operational efficiency, installation practicality, and apartment-format compatibility align more naturally with Russian residential cooling requirements than portable or window-unit alternatives. Russia's household air-conditioner efficiency standard which remains in force and mandates visible energy performance labeling for split and portable room air conditioners up to 12 kW reinforces this format's structural leadership by creating a compliance-supported comparison framework that rewards certified, higher-efficiency split system offerings.

The end-user architecture reinforces the primacy of residential demand as the category's primary commercial engine. Residential buyers account for approximately 75% of total market share confirming that home-based cooling demand defines the category's volume base and replacement cycle dynamics. Rosstat's documentation of Russia's total housing stock reaching 4,293.1 million sq. m in 2024, with average living space of 29.4 sq. m per inhabitant and 94.7% private ownership, validates the structural scale of the homeowner-led upgrade and retrofit demand base that is sustaining consistent room air conditioner purchase activity across the country's large and geographically distributed residential market.

The forward outlook through 2032 is defined by four structural market forces the recurring summer heat intensity documented by Rosgidromet that is progressively elevating household cooling investment priority across Russia's residential base, the vast privately owned dwelling stock that creates a large and accessible retrofit and replacement demand opportunity, the specification-led buying behavior supported by Rosstat's documentation of 90.4% household internet access in 2024 that is systematically elevating energy efficiency and performance transparency as purchase decision criteria, and the constrained macroeconomic environment documented by the Bank of Russia with GDP growth slowing to 1.0% in 2025 and the key rate held at 21.00% that shapes demand toward value-conscious, replacement-led purchasing patterns through 2032.

Russia Room Air Conditioners Market Growth DriverRecurring Summer Heat Intensity Sustains Structural Household Cooling Demand

The recurring and geographically pervasive intensification of summer heat conditions across Russia's major residential zones represents the primary structural driver of room air conditioner demand functioning as a persistent environmental motivator that systematically elevates household cooling investment priority among a consumer base confronting episodic but intense thermal discomfort across urban apartments, private homes, and semi-urban residential settings where passive heat management strategies prove increasingly inadequate. This climatic driver reflects a durable demand generation dynamic whose commercial relevance persists independently of macroeconomic cycle fluctuations.

The quantitative evidence validating this dynamic is documented with precision by Rosgidromet. On 3–4 June 2025, daytime temperatures in southern European Russia reach +23°C to +30°C, while on 14–15 June 2025, parts of Novosibirsk, Tomsk, and Altai record peak temperatures of up to +34°C conditions that create acute indoor discomfort across Russia's vast residential housing base and generate consistent first-purchase and replacement motivation among households seeking immediate room-level cooling relief. Combined with Rosstat's documentation of 4,293.1 million sq. m of total dwelling stock, the climatic intensity driver activates a structurally large demand base through 2032.

Russia Room Air Conditioners Market ChallengeRestrictive Monetary Conditions and Subdued Consumer Spending Constrain Adoption Velocity

Russia's persistently restrictive monetary policy environment and decelerating economic growth trajectory constitute the most consequential demand-side challenge confronting the room air conditioners market creating a sustained consumer spending constraint that moderates purchase decision velocity, amplifies price sensitivity across mid-range and premium product segments, and channels household appliance investment toward essential replacement rather than discretionary first-installation or multi-room upgrade purchasing. This macroeconomic headwind operates with particular intensity in a category where financing conditions directly influence the affordability calculus of a semi-discretionary comfort investment.

The structural depth of this challenge is quantified by the Bank of Russia. The key policy rate is held at 21.00% as of 25 April 2025, while GDP growth decelerates sharply from 4.9% in 2024 to 1.0% in 2025. The Bank further documents that the late-2025 sales upturn observed across non-food categories including household appliances and electronics is largely transitory with subdued demand conditions re-emerging across company reporting in January–February 2026. This combination of elevated borrowing costs and decelerating economic momentum keeps end user value-focused and replacement-led rather than expansion-driven through 2032.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Russia Room Air Conditioners Market TrendDigitally Enabled Specification-Led Buying Elevates Energy Efficiency as a Purchase Criterion

The progressive shift toward more informed, specification-driven purchase behavior among Russian room air conditioner buyers represents a defining structural trend reshaping the competitive differentiation environment fundamentally elevating energy efficiency credentials, cooling capacity transparency, and performance labeling visibility from background product attributes into front-line commercial differentiators that shape retail consideration, installer recommendation, and household purchase decision outcomes across the residential base.

Russia's digital infrastructure directly enables and accelerates this behavioral trend. Rosstat documents that in 2024, 90.4% of Russian households have internet access, 89.8% have broadband connectivity, and 95.5% of people aged 15–74 actively use the internet creating a digitally empowered consumer base with robust capacity for pre-purchase product comparison and efficiency rating evaluation. Russia's household air-conditioner efficiency standard reinforces this dynamic by mandating a visible energy performance label for split and portable room air conditioners up to 12 kW institutionalizing efficiency transparency at the point of sale and rewarding brands that invest in certified, top-tier performance engineering through 2032.

Russia Room Air Conditioners Market OpportunityVast Privately Owned Dwelling Stock Creates a Scalable Residential Retrofit Demand Base

Russia's vast and predominantly privately owned residential housing stock represents the market's most structurally durable commercial opportunity providing a large, geographically distributed, and progressively more cooling-motivated retrofit and replacement demand base whose conversion into active room air conditioner purchasing is enabled by high homeowner decision-making autonomy, recurring summer heat motivation, and an energy labeling framework that supports confident, efficiency-informed upgrade investment across the full residential income spectrum.

The quantitative scale of this opportunity is established with precision by Rosstat. Russia's total housing stock reaches 4,293.1 million sq. m in 2024, with average living space of 29.4 sq. m per inhabitant and 94.7% private ownership confirming the structural scale of the consumer-controlled upgrade decision base that room air conditioner suppliers can address through targeted residential channel investment. The room-by-room installation practicality of split systems aligns naturally with the incremental comfort upgrade behavior that characterizes value-conscious Russian household purchasing creating a retrofit demand dynamic whose commercial depth and geographic breadth will sustain consistent market growth through 2032.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Russia Room Air Conditioners Market Segmentation Analysis

By Product Type

- Split Air Conditioners

- Up to 9,000 BTU/h

- 9,001-12,000 BTU/h

- 12,001-18,000 BTU/h

- 18,001-24,000 BTU/h

- Above 24,000 BTU/h

- Window Air Conditioners

- Up to 9,000 BTU/h

- 9,001-12,000 BTU/h

- 12,001-18,000 BTU/h

- 18,001-24,000 BTU/h

- Above 24,000 BTU/h

- Others

The segment commanding the highest market share within the product type dimension is Split Air Conditioners, accounting for approximately 85% of total Russia room air conditioners market value. This near-dominant position reflects the deep structural alignment between split system technology and the specific installation and comfort management requirements of Russia's predominantly apartment-based residential housing stock where compact, wall-mounted configurations delivering room-level precision cooling without whole-building infrastructure modification make split systems the unambiguous product of choice across both urban and semi-urban residential geographies. With four-fifths of total market value concentrated within a single format, split air conditioners define the entire competitive and commercial agenda of the Russia room air conditioners market.

The structural leadership of split air conditioners is actively reinforced by Russia's household air-conditioner efficiency standard, which remains in force and explicitly covers split and portable room air conditioners up to 12 kW while mandating a visible energy performance label at the point of sale. This regulatory framework creates a compliance-supported differentiation axis that rewards brands with certified, higher-efficiency split system offerings and enables increasingly specification-conscious end user operating within a digitally connected household base where 90.4% have internet access to compare efficiency credentials with growing granularity. The segment's commanding revenue position is expected to remain structurally intact through 2032.

By End User

- Residential

- Individual Households

- Apartments/Condominiums

- Vacation/Secondary Homes

- Commercial

- Offices

- Retail Stores/Showrooms

- Hospitality

- Healthcare Facilities

- Educational Institutions

- Small Commercial Establishments

- Others

The segment commanding the highest market share within the end user dimension is Residential, accounting for approximately 75% of total Russia room air conditioners market value. This dominant position confirms household-based cooling demand as the category's primary commercial engine where purchase decisions are motivated by recurring summer heat episodes, indoor thermal discomfort across key living spaces, and the practical appeal of room-level cooling solutions that can be installed in individual apartments and private homes without whole-property system investment. With three-quarters of total market revenue anchored in residential consumption, the category's commercial trajectory is structurally inseparable from the dynamics shaping Russian household cooling adoption behavior.

The structural centrality of residential demand is validated and amplified by Rosstat's documentation of Russia's total housing stock reaching 4,293.1 million sq. m in 2024 with average living space of 29.4 sq. m per inhabitant and 94.7% private ownership confirming the structural scale of the homeowner-led decision-making base that drives comfort upgrade and retrofit purchasing activity. When Rosgidromet documents peak temperatures of up to +34°C across parts of Novosibirsk, Tomsk, and Altai in June 2025, room-level cooling relevance intensifies across this vast residential base sustaining the segment's structural dominance as the market's primary demand anchor through 2032.

List of Companies Covered in Russia Room Air Conditioners Market

The companies listed below are highly influential in the Russia room air conditioners market, with a significant market share and a strong impact on industry developments.

- Ballu Industrial Group

- AUX Group Co Ltd

- Electrolux AB

- Haier Group

- Midea Group Co Ltd

- Hisense Group

- Daikin Industries Ltd

- Gree Electric Appliances Inc of Zhuhai

- Panasonic Corp

- LG Corp

Market News & Updates

- AUX Group Co Ltd, 2026:

AUX’s official Russia platform is positioning Basic Inverter as its “hottest new product of 2026,” describing it as a modern inverter room AC built around R32 refrigerant and high-temperature self-cleaning, while the same Russia catalog shows a broad localized lineup spanning Basic Inverter, Comfort Inverter, Premium Inverter, ART variants and other wall-mounted split series distributed through official dealers. In Russia, this is a significant development because it signals a deliberate market-building strategy rather than a single SKU launch, giving AUX a stronger ladder from affordable to premium inverter products and improving its ability to capture consumers looking for better efficiency, hygiene features and smarter operation in a market that remains price-sensitive but increasingly feature-aware.

- Haier Group, 2025:

Haier’s official Russia site is selling the Flexis On-Off 2025 line and, more broadly, lists 106 room-air-conditioner SKUs in its Russian catalog, with feature filters covering inverter, UV lamp, Self Clean, SteriClean 56°C, Wi-Fi and Nano-Aqua, plus evo-app connectivity for remote control and status monitoring. The market impact is scale and segmentation: Haier is not relying on one hero model but on a wide, locally merchandised assortment that covers multiple BTU bands, price points and health- or smart-oriented feature sets, which improves channel coverage and gives Russian consumers more upgrade paths into connected and higher-spec room AC across mainstream and premium tiers.

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- Russia Room Air Conditioners Market Policies, Regulations, and Standards

- Russia Room Air Conditioners Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- Russia Room Air Conditioners Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Units Sold in Thousand Units

- Market Segmentation & Growth Outlook

- By Product Type

- Split Air Conditioners- Market Insights and Forecast 2022-2032, USD Million

- Up to 9,000 BTU/h- Market Insights and Forecast 2022-2032, USD Million

- 9,001-12,000 BTU/h- Market Insights and Forecast 2022-2032, USD Million

- 12,001-18,000 BTU/h- Market Insights and Forecast 2022-2032, USD Million

- 18,001-24,000 BTU/h- Market Insights and Forecast 2022-2032, USD Million

- Above 24,000 BTU/h- Market Insights and Forecast 2022-2032, USD Million

- Window Air Conditioners- Market Insights and Forecast 2022-2032, USD Million

- Up to 9,000 BTU/h- Market Insights and Forecast 2022-2032, USD Million

- 9,001-12,000 BTU/h- Market Insights and Forecast 2022-2032, USD Million

- 12,001-18,000 BTU/h- Market Insights and Forecast 2022-2032, USD Million

- 18,001-24,000 BTU/h- Market Insights and Forecast 2022-2032, USD Million

- Above 24,000 BTU/h- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- Split Air Conditioners- Market Insights and Forecast 2022-2032, USD Million

- By Technology

- Inverter- Market Insights and Forecast 2022-2032, USD Million

- Non-Inverter- Market Insights and Forecast 2022-2032, USD Million

- By Price

- Up to USD 300- Market Insights and Forecast 2022-2032, USD Million

- USD 301 to USD 600- Market Insights and Forecast 2022-2032, USD Million

- USD 601 to USD 1,000- Market Insights and Forecast 2022-2032, USD Million

- Above USD 1,000- Market Insights and Forecast 2022-2032, USD Million

- By End User

- Residential- Market Insights and Forecast 2022-2032, USD Million

- Individual Households- Market Insights and Forecast 2022-2032, USD Million

- Apartments/Condominiums- Market Insights and Forecast 2022-2032, USD Million

- Vacation/Secondary Homes- Market Insights and Forecast 2022-2032, USD Million

- Commercial- Market Insights and Forecast 2022-2032, USD Million

- Offices- Market Insights and Forecast 2022-2032, USD Million

- Retail Stores/Showrooms- Market Insights and Forecast 2022-2032, USD Million

- Hospitality- Market Insights and Forecast 2022-2032, USD Million

- Healthcare Facilities- Market Insights and Forecast 2022-2032, USD Million

- Educational Institutions- Market Insights and Forecast 2022-2032, USD Million

- Small Commercial Establishments- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- Residential- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel

- Retail Online- Market Insights and Forecast 2022-2032, USD Million

- Brand-Owned Websites/D2C- Market Insights and Forecast 2022-2032, USD Million

- E-Commerce Marketplaces- Market Insights and Forecast 2022-2032, USD Million

- Retail Offline- Market Insights and Forecast 2022-2032, USD Million

- Exclusive Brand Stores- Market Insights and Forecast 2022-2032, USD Million

- Multi-Brand Electronics & Appliance Stores- Market Insights and Forecast 2022-2032, USD Million

- Specialty Stores- Market Insights and Forecast 2022-2032, USD Million

- Hypermarkets/Supermarkets- Market Insights and Forecast 2022-2032, USD Million

- Home Improvement Stores- Market Insights and Forecast 2022-2032, USD Million

- Dealer/Distributor Network- Market Insights and Forecast 2022-2032, USD Million

- Direct Sales/Institutional Sales- Market Insights and Forecast 2022-2032, USD Million

- Local Independent Retailers- Market Insights and Forecast 2022-2032, USD Million

- Retail Online- Market Insights and Forecast 2022-2032, USD Million

- By Refrigerant Type

- R-32- Market Insights and Forecast 2022-2032, USD Million

- R-410A- Market Insights and Forecast 2022-2032, USD Million

- R-290- Market Insights and Forecast 2022-2032, USD Million

- R-454B- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By Connectivity

- Smart/Connected- Market Insights and Forecast 2022-2032, USD Million

- Conventional/Non-Smart- Market Insights and Forecast 2022-2032, USD Million

- By Energy Efficiency

- 1 Star- Market Insights and Forecast 2022-2032, USD Million

- 2 Star- Market Insights and Forecast 2022-2032, USD Million

- 3 Star- Market Insights and Forecast 2022-2032, USD Million

- 4 Star- Market Insights and Forecast 2022-2032, USD Million

- 5 Star- Market Insights and Forecast 2022-2032, USD Million

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Product Type

- Market Size & Growth Outlook

- Russia Split Air Conditioners Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Units Sold in Thousand Units

- Market Segmentation & Growth Outlook

- By Technology- Market Insights and Forecast 2022-2032, USD Million

- By Price- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Refrigerant Type- Market Insights and Forecast 2022-2032, USD Million

- By Connectivity- Market Insights and Forecast 2022-2032, USD Million

- By Energy Efficiency- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Russia Window Air Conditioners Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Units Sold in Thousand Units

- Market Segmentation & Growth Outlook

- By Technology- Market Insights and Forecast 2022-2032, USD Million

- By Price- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Refrigerant Type- Market Insights and Forecast 2022-2032, USD Million

- By Connectivity- Market Insights and Forecast 2022-2032, USD Million

- By Energy Efficiency- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- Haier Group

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Midea Group Co Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Hisense Group

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Daikin Industries Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Gree Electric Appliances Inc of Zhuhai

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Ballu Industrial Group

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- AUX Group Co Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Electrolux AB

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Panasonic Corp

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- LG Corp

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Haier Group

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Product Type |

|

| By Technology |

|

| By Price |

|

| By End User |

|

| By Sales Channel |

|

| By Refrigerant Type |

|

| By Connectivity |

|

| By Energy Efficiency |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.