Romania Bags and Luggage Market Report: Trends, Growth and Forecast (2026-2032)

By Category (Bags (Cross Body Bags, Bags and Backpacks, Business Bags, Duffle Bags, Clutches, Others), Luggage (Soft Luggage, Hard Luggage, Wheeled Luggage, Non-Wheeled Luggage)), By Sales Channel (Retail Offline, Retail Online), By Material Type (Soft Case (Nylon, Polyester, Ballistic Nylon), Hard Case (Polycarbonate, ABS (Acrylonitrile Butadiene Styrene), Polypropylene)), By Price Category (Luxury, Mass/Economy, Premium), By Application (Travel, Business) ... Read more

|

Major Players

|

Romania Bags and Luggage Market Statistics and Insights, 2026

- Market Size Statistics

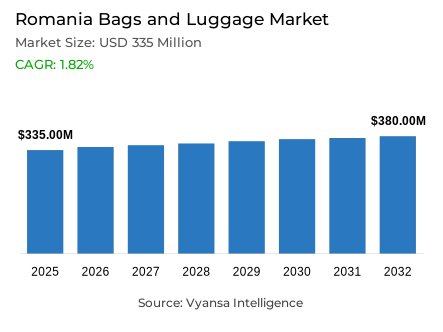

- Bags and luggage market size in Romania was estimated at USD 335 million in 2025.

- The market size is expected to grow to USD 380 million by 2032.

- Market to register a CAGR of around 1.82% during 2026-32.

- Category Shares

- Bags grabbed market share of 90%.

- Competition

- More than 20 companies are actively engaged in producing bags and luggage in Romania.

- Top 5 companies acquired around 20% of the market share.

- Kering SA, Michael Kors Srl, Nike Inc, Azad Enterprises Srl, LVMH Moët Hennessy Louis Vuitton SA etc., are few of the top companies.

- Sales Channel

- Retail offline grabbed 75% of the market.

Romania Bags and Luggage Market Outlook

The Romania Bags and Luggage Market is projected to reach USD 335 million in 2025 and USD 380 million in 2032 with a CAGR of about 1.82% over the forecast period. The growth will be moderate and stable as the market matures and the demand will be more affected by the lifestyle changes, travel recovery patterns and selective end-user spending priorities based on the broader economic considerations and changing consumption behaviours.

Despite the high travel recovery in 2024, future growth patterns will be more conservative as end user balance discretionary expenditure with broader cost-of-living considerations. Luggage will enjoy the sustained domestic and international travel, but growth will probably level off after the sharp rebound phase of post-restriction pent-up demand release. The Romanian end users are becoming more concerned with durability, ergonomics, and design when buying travel-related products because they view luggage as a long-term investment and not a high-frequency consumer product that needs to be replenished in the category on a regular basis.

Bags will continue to dominate the market, with the daily usage in work, leisure, education, and sports settings. Handbags will be especially good performers, as they will be motivated by premiumisation in the market and the increasing popularity of established brands. Nonetheless, demand will be more polarised, with growth being focused on low-end and luxury products and mid-priced products experiencing more competitive pressure as value and high-end products take over different consumer segments.

The sales will be pegged on the retail offline outlets, which will be backed by the end-user preference of physical quality and fit testing before committing to purchase. Although retail online growth is slowing, particularly among younger age groups, the physical stores will remain at the centre of structural functions during the forecast period, as they will have advantages of tactile product assessment and instant fulfilment benefits that cannot be easily matched by retail online channels.

Romania Bags and Luggage Market Growth Driver

Travel revival driving luggage demand

The restoration of domestic and inbound travel in Romania remains the foundation of the base demand of the luggage, especially durable and ergonomic luggage used in the repetitive travel patterns. Eurostat data shows that in 2024, Romania registered more than 14 million arrivals and 30 million overnight stays in registered accommodation establishments, which confirms the continued mobility in the leisure and visiting friends and relatives travel segments. This high volume of movement is directly converted into a repeat replacement and upgrade demand of suitcases and travel bags utilized in road, rail, and air transport modes.

In addition to volume measures, travel behaviour is becoming more and more inclined towards reliability and long-term value as opposed to impulse buying behaviour. With the increasing frequency of journeys but at a low cost, end users are focusing on durability, warranty, and comfort. This dynamic supports the positioning of luggage as a practical need and not a fashion accessory, which offers structural demand support despite the overall end-user expenditure being selective. Travel recovery creates favourable conditions to the growth of the luggage category by maintaining mobility trends and value-based purchasing behaviours that focus on product durability and functionality rather than on aesthetic fashion factors in the recovering tourism and domestic travel environment in Romania.

Romania Bags and Luggage Market Challenge

Remote and hybrid work patterns limiting business bag use

The trend of remote and hybrid work patterns remains a hindrance to the growth of demand of traditional business-specific bags in Romania. Eurostat estimates that in 2023, 22% of working adults in the EU worked at home at least once a week, a structural change that is still evident in Central and Eastern Europe. Less commuting per day means that the frequency of replacement of briefcases and formal office bags is reduced, and this puts a long-term volume strain on the traditional business-bag segments.

This change in behaviour does not kill demand but changes the relevance of products. Multifunctional designs that move between casual, travel, and occasional work applications are becoming more popular with end users, undermining the growth momentum of strictly formal formats. Conventional business bags therefore experience reduced turnover rates and increased substitution pressure by hybrid designs, limiting value growth in this particular application despite the stability of the bag-category. The trend of remote-working poses structural demand headwinds to formal business-bag segments and at the same time opens opportunities to versatile, multipurpose bag designs that can be used in a variety of contexts in the changing work-from-home environment in Romania.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Romania Bags and Luggage Market Trend

Polarised handbag demand and lifestyle diversification

The consumption of handbags in Romania is becoming more and more income-based polarised, as opposed to the homogeneous mid-market growth trends. According to Eurostat household expenditure data, the expenditure on discretionary goods including fashion and accessories is still increasing unevenly across income groups in the EU, with both the high-end and low-end segments being favoured. This consumption trend is reflected in Romania, where luxury handbags are recording higher value growth than mass-market substitutes, and low-end daily-use products are holding their own in price-sensitive consumer groups.

This difference is indicative of the dual role of handbags as both practical accessories and indicators of individual identity. End users with higher income are more concerned with craftsmanship, brand heritage, and durability, whereas value-oriented consumers are more concerned with affordability and high replacement rates. The outcome is a structurally diversified handbag segment in which premiumisation and budget demand co-exist, which strengthens handbags as one of the most dynamic elements in the larger bag category. The polarisation trend provides both premium positioning and value-based offerings at the same time, allowing brands to focus on different consumer segments with differentiated product strategies to meet divergent quality, price, and replacement-frequency expectations in the economically stratified consumer environment of Romania.

Romania Bags and Luggage Market Opportunity

Sports and smart products driving future category growth

The increase in outdoor and recreational activities will help in the future demand of functional backpacks and multipurpose bags in Romania. The European Commission estimates that more than 44% of adults in the EU take part in some kind of physical or outdoor activity at least once a week, and activities like hiking and cycling are still among the most popular due to their cost-effectiveness. This behavioural pattern generates repetitive use cases of durable, lightweight, and ergonomically designed backpacks that go beyond travel use cases to active lifestyle use cases.

At the same time, product innovation will become more and more differentiating in the future growth paths. The inclusion of smart features like USB charging, anti-theft, and modular compartments will likely attract younger, technology-focused demographics that want convenience and integration of connectivity. Brands that effectively combine functional outdoor performance with digital utility will be well-placed to tap into incremental demand and expand the use of bags into daily lifestyle situations. The innovation opportunity allows manufacturers to cross the conventional category lines, making bags a vital lifestyle accessory that supports both leisure activities and digital connectivity needs in the ever-busy, technology-saturated consumer base in Romania over the 2032 forecast horizon.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Romania Bags and Luggage Market Segmentation Analysis

By Category

- Bags

- Cross Body Bags

- Bags and Backpacks

- Business Bags

- Duffle Bags

- Clutches

- Others

- Luggage

- Soft Luggage

- Hard Luggage

- Wheeled Luggage

- Non-Wheeled Luggage

The higest category is bags, which constitute about 90% of the total market value. Their dominance is an indication of high purchase frequency and relevance in daily use scenarios, such as commuting, education, leisure, and sports activities. Compared to luggage that needs to be replaced infrequently, bags enjoy the benefits of fashion rotation patterns and functional diversification that facilitates more frequent purchase cycles across a wide range of consumer segments and usage occasions.

Handbags continue to be a major value driver, with premiumisation at the high end and steady demand of affordable everyday-use products across income groups. Outdoor activities, student demand, and multifunctional lifestyle applications also make backpacks highly relevant. Combined, these dynamics guarantee bags to be the main revenue anchor during the forecast period, which will help the category value grow due to the variety of use-cases applicability, high replacement rates, and high consumer interest across demographic lines in the changing consumer goods environment in Romania.

By Sales Channel

- Retail Offline

- Retail Online

The retail offline market is estimated to contribute about 75% of the market sales, which indicates that the end-users prefer to touch and feel the physical products before committing themselves to purchase. Fit, comfort, material quality and durability are still the determining factors of purchase, especially when it comes to high-end bags and luggage that needs to be touched and tried instantly to determine the level of functionality and quality that meets the expectations of the consumer before committing money.

Purchasing behaviour is dominated by specialist stores, shopping centres, and multi-brand retailers, particularly in peak travel and back-to-school periods that generate concentrated demand periods. Although online retail is growing slowly among digitally active younger consumers, it does not replace brick-and-mortar channels, but complements them. The structural dominance of retail offline will be sustained by consumer confidence in physical assessment, personal service benefits, and experience value that cannot be fully transferred to digital commerce, and channel primacy will be sustained by the benefits of physical product assessment and instant fulfilment to support informed purchasing decisions.

List of Companies Covered in Romania Bags and Luggage Market

The companies listed below are highly influential in the Romania bags and luggage market, with a significant market share and a strong impact on industry developments.

- Kering SA

- Michael Kors Srl

- Nike Inc

- Azad Enterprises Srl

- LVMH Moët Hennessy Louis Vuitton SA

- VF Corp

- General Business System SRL

- SC Roumasport SRL

- Case Logic Inc

- Burberry Group Plc

Competitive Landscape

Romania’s bags and luggage market is moderately fragmented, with competition shaped by international brands, strong specialist retailers, and value-driven seasonal demand. International players dominate the premium segment, benefiting from growing interest in fashionable and functional luggage as travel rebounds. At the same time, affordable and mid-priced brands remain highly relevant, supported by consumers seeking value and versatility, particularly during peak promotional periods such as Black Friday and back-to-school seasons. Retailers with broad assortments of handbags and backpacks are well positioned, as these categories show consistent growth across income groups. Sports-oriented retailers, led by players such as Decathlon, are strengthening their role in backpacks, driven by rising participation in hiking and outdoor activities. Overall, competition increasingly revolves around balancing style, functionality, and price, with emerging interest in smart and technology-enabled luggage adding a new layer to differentiation.

Frequently Asked Questions

Related Report

1. Market Segmentation

1.1. Research Scope

1.2. Research Methodology

1.3. Definitions and Assumptions

2. Executive Summary

3. Romania Bags and Luggage Market Policies, Regulations, and Standards

4. Romania Bags and Luggage Market Dynamics

4.1. Growth Factors

4.2. Challenges

4.3. Trends

4.4. Opportunities

5. Romania Bags and Luggage Market Statistics, 2022-2032F

5.1. Market Size & Growth Outlook

5.1.1.By Revenues in USD Million

5.1.2.By Units Sold in Thousand Units

5.2. Market Segmentation & Growth Outlook

5.2.1.By Category

5.2.1.1. Bags- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.1. Cross Body Bags- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.2. Bags and Backpacks- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.3. Business Bags- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.4. Duffle Bags- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.5. Clutches- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.6. Others- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2. Luggage- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2.1. Soft Luggage- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2.2. Hard Luggage- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2.3. Wheeled Luggage- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2.4. Non-Wheeled Luggage- Market Insights and Forecast 2022-2032, USD Million

5.2.2.By Sales Channel

5.2.2.1. Retail Offline- Market Insights and Forecast 2022-2032, USD Million

5.2.2.2. Retail Online- Market Insights and Forecast 2022-2032, USD Million

5.2.3.By Material Type

5.2.3.1. Soft Case- Market Insights and Forecast 2022-2032, USD Million

5.2.3.1.1. Nylon- Market Insights and Forecast 2022-2032, USD Million

5.2.3.1.2. Polyester- Market Insights and Forecast 2022-2032, USD Million

5.2.3.1.3. Ballistic Nylon- Market Insights and Forecast 2022-2032, USD Million

5.2.3.2. Hard Case- Market Insights and Forecast 2022-2032, USD Million

5.2.3.2.1. Polycarbonate- Market Insights and Forecast 2022-2032, USD Million

5.2.3.2.2. ABS (Acrylonitrile Butadiene Styrene)- Market Insights and Forecast 2022-2032, USD Million

5.2.3.2.3. Polypropylene- Market Insights and Forecast 2022-2032, USD Million

5.2.4.By Price Category

5.2.4.1. Luxury- Market Insights and Forecast 2022-2032, USD Million

5.2.4.2. Mass/Economy- Market Insights and Forecast 2022-2032, USD Million

5.2.4.3. Premium- Market Insights and Forecast 2022-2032, USD Million

5.2.5.By Application

5.2.5.1. Travel- Market Insights and Forecast 2022-2032, USD Million

5.2.5.2. Business- Market Insights and Forecast 2022-2032, USD Million

5.2.6.By Competitors

5.2.6.1. Competition Characteristics

5.2.6.2. Market Share & Analysis

6. Romania Bags Market Statistics, 2022-2032

6.1. Market Size & Growth Outlook

6.1.1.By Revenues in USD Million

6.1.2.By Units Sold in Thousand Units

6.2. Market Segmentation & Growth Outlook

6.2.1.By Category- Market Insights and Forecast 2022-2032, USD Million

6.2.2.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

6.2.3.By Material Type- Market Insights and Forecast 2022-2032, USD Million

6.2.4.By Price Category- Market Insights and Forecast 2022-2032, USD Million

6.2.5.By Application- Market Insights and Forecast 2022-2032, USD Million

7. Romania Luggage Market Statistics, 2022-2032

7.1. Market Size & Growth Outlook

7.1.1.By Revenues in USD Million

7.1.2.By Units Sold in Thousand Units

7.2. Market Segmentation & Growth Outlook

7.2.1.By Category- Market Insights and Forecast 2022-2032, USD Million

7.2.2.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

7.2.3.By Material Type- Market Insights and Forecast 2022-2032, USD Million

7.2.4.By Price Category- Market Insights and Forecast 2022-2032, USD Million

7.2.5.By Application- Market Insights and Forecast 2022-2032, USD Million

8. Competitive Outlook

8.1. Company Profiles

8.1.1.Azad Enterprises Srl

8.1.1.1. Business Description

8.1.1.2. Product Portfolio

8.1.1.3. Collaborations & Alliances

8.1.1.4. Recent Developments

8.1.1.5. Financial Details

8.1.1.6. Others

8.1.2.LVMH Moët Hennessy Louis Vuitton SA

8.1.2.1. Business Description

8.1.2.2. Product Portfolio

8.1.2.3. Collaborations & Alliances

8.1.2.4. Recent Developments

8.1.2.5. Financial Details

8.1.2.6. Others

8.1.3.VF Corp

8.1.3.1. Business Description

8.1.3.2. Product Portfolio

8.1.3.3. Collaborations & Alliances

8.1.3.4. Recent Developments

8.1.3.5. Financial Details

8.1.3.6. Others

8.1.4.General Business System SRL

8.1.4.1. Business Description

8.1.4.2. Product Portfolio

8.1.4.3. Collaborations & Alliances

8.1.4.4. Recent Developments

8.1.4.5. Financial Details

8.1.4.6. Others

8.1.5.SC Roumasport SRL

8.1.5.1. Business Description

8.1.5.2. Product Portfolio

8.1.5.3. Collaborations & Alliances

8.1.5.4. Recent Developments

8.1.5.5. Financial Details

8.1.5.6. Others

8.1.6.Kering SA

8.1.6.1. Business Description

8.1.6.2. Product Portfolio

8.1.6.3. Collaborations & Alliances

8.1.6.4. Recent Developments

8.1.6.5. Financial Details

8.1.6.6. Others

8.1.7.Michael Kors Srl

8.1.7.1. Business Description

8.1.7.2. Product Portfolio

8.1.7.3. Collaborations & Alliances

8.1.7.4. Recent Developments

8.1.7.5. Financial Details

8.1.7.6. Others

8.1.8.Nike Inc

8.1.8.1. Business Description

8.1.8.2. Product Portfolio

8.1.8.3. Collaborations & Alliances

8.1.8.4. Recent Developments

8.1.8.5. Financial Details

8.1.8.6. Others

8.1.9.Case Logic Inc

8.1.9.1. Business Description

8.1.9.2. Product Portfolio

8.1.9.3. Collaborations & Alliances

8.1.9.4. Recent Developments

8.1.9.5. Financial Details

8.1.9.6. Others

8.1.10. Burberry Group Plc

8.1.10.1. Business Description

8.1.10.2. Product Portfolio

8.1.10.3. Collaborations & Alliances

8.1.10.4. Recent Developments

8.1.10.5. Financial Details

8.1.10.6. Others

9. Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Category |

|

| By Sales Channel |

|

| By Material Type |

|

| By Price Category |

|

| By Application |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.