North America Municipal Water & Wastewater Pump Market Report: Trends, Growth and Forecast (2026-2032)

By Pump Type (Centrifugal Pumps (End Suction, Split Case, Vertical (Turbine, Axial Pump, Mixed Flow Pump), Submersible Pump), Positive Displacement Pumps (Progressing Cavity, Diaphragm, Gear Pump, Others)), By Application (Water, Wastewater), By Country (US, Canada, Mexico, Rest of North America) ... Read more

|

Major Players

|

North America Municipal Water & Wastewater Pump Market Statistics and Insights, 2026

- Market Size Statistics

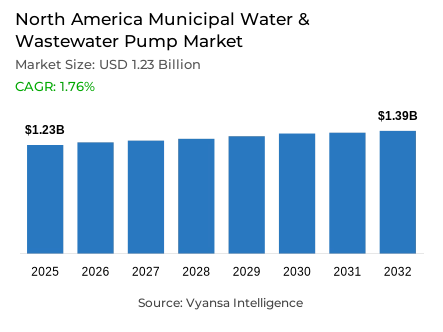

- North America municipal water & wastewater pump market is estimated at USD 1.23 billion in 2025.

- The market size is expected to grow to USD 1.39 billion by 2032.

- Market to register a cagr of around 1.76% during 2026-32.

- Pump Type Shares

- Centrifugal pumps grabbed market share of 90%.

- Competition

- More than 10 companies are actively engaged in producing municipal water & wastewater pump in North America.

- Top 5 companies acquired around 65% of the market share.

- KSB SE & Co. KGaA; ITT Inc.; Sulzer Ltd.; Xylem Inc.; Flowserve Corporation etc., are few of the top companies.

- Application

- Water grabbed 60% of the market.

- Country

- US leads with a 90% share of the North America market.

North America Municipal Water & Wastewater Pump Market Outlook

The North American municipal water & wastewater pump market was valued at USD 1.23 billion in 2025 and is expected to grow to USD 1.39 billion by 2032, registering a CAGR of 1.76% during the forecast period. The drivers of the municipal water & wastewater pumps market in the North American region are the rapidly growing demand to replace old municipal water and wastewater infrastructure, which has already aged out of its intended working lifespan in the USA and Canada. Most of the water pipelines, pumping infrastructure, and wastewater treatment plants are already past the intended service life and prone to frequent breakdowns, leaks, and maintenance costs.

Public entities are increasingly pursuing large-scale rehabilitation projects aimed at enhancing the distribution and treatment infrastructure. Financial assistance is allowing these entities to pursue deferred maintenance while also adopting new pumping technology that promotes greater flow efficiency, better pressure regulation, and durability. It is essential to ensure an unrelenting supply to consumers while optimizing the efficiency of the network.

In the pump type sub-sections, the centrifugal pump has emerged as the dominant type, accounting for about 90% of the market. This is because they can handle high flows and work on a continuous duty cycle, which is advisable in municipal applications such as intake, treatment, or distribution of water.

From an application point of view, water applications account for approximately 60% of the applications market, which can be attributed to the intense focus on ensuring the reliability of municipal potable water. The United States dominates the regional market with a share of close to 90%, leading the market as the key driver of applications through 2032.

North America Municipal Water & Wastewater Pump Market Growth Driver

Aging Infrastructure Renewal Accelerating Equipment Demand

The North America municipal water & wastewater pump market is being strongly shaped by accelerating needs to replace and modernize aging water infrastructure across the United States and Canada. Large portions of existing pipelines, pumping stations, and treatment facilities have exceeded their designed operational life, increasing failure risks and maintenance costs for municipal utilities. Widespread water main breaks, rising leakage levels, and deteriorating pump efficiency are compelling municipalities to prioritize replacement projects that ensure system reliability and continuity of service to end users. These conditions are thickening procurement of modern pumping systems capable of supporting higher flow rates, improved pressure control, and energy efficiency.

Public agencies are responding to infrastructure deterioration with plans for large-scale rehabilitation programs that target upgrading distribution networks and treatment assets. Replacement efforts tend to include the installation of advanced pump systems that are designed to integrate with modern control technologies and comply with updated performance standards. As municipalities tackle the backlog of deferred maintenance accumulated during decades, demand is growing for pumps that can operate reliably within aging networks while supporting long-term infrastructure resilience. This structural need for renewal remains one of the most consistent forces supporting sustained equipment demand across the regional market.

North America Municipal Water & Wastewater Pump Market Challenge

Regulatory Pressure and Contaminant Management Complexity

Municipal water utilities throughout North America are under increasing operational constraints from tightening regulatory requirements and increasing complexity of water treatment challenges. New emerging contaminants-especially per- and polyfluoroalkyl substances-further burden treatment plants operating within these aged infrastructure environments. Compliance with new federal drinking water standards involves the adoption of advanced treatment processes, many of which require higher pressures, greater chemical exposure, and multistage filtration systems that put increased stress on pumping equipment. Requirements such as these increase both the capital and operating costs for municipalities, while acceptable technology choices are restricted further.

Utilities face significant planning and financial challenges in keeping up with infrastructure replacement and regulatory compliance. Upgrades to treatment must be done without disrupting water supply to end users; this requires pumps that offer consistent, reliable performance under demanding conditions. Corrosion resistance, chemical compatibility, and operational reliability have all become key selection factors, reducing flexibility for cost-driven procurement. Compliance timelines are shrinking, while monitoring is increasing, making it difficult for utilities to balance affordability against technical capability; constraints blur procurement decisions and impede project completion despite obvious infrastructure needs.

Unlock Market Intelligence

Explore the market potential with our data-driven report

North America Municipal Water & Wastewater Pump Market Trend

Standardization Around Proven Pump Technologies

Technology selection trends in the North America municipal water & wastewater pump market indicate that, among all technologies, there is a general trend for standardization around tried-and-tested pump designs, most of which are centrifugal systems. Municipal utilities have a preference for technologies that have good track records of operation, have predictability in maintenance, and therefore are widely accepted among engineering consultants. Centrifugal pumps have emerged as ideal for the normally high-volume, moderate-pressure applications involved in the intake, treatment, and distribution of water. Its relatively simple mechanical configuration allows ease of operation through wide variations in climatic and water-quality conditions across the region.

Workforce familiarity and compatibility with the existing infrastructure definitely act to reinforce centrifugal technology's widespread adoption. Utilities, whose experienced operator pool is reducing with retirees and their staffing constraints are on an uphill climb, give major consideration to equipment that doesn't require special training and reduces spare parts complexity. Second, standardization simplifies system integration during phased infrastructure upgrades. This enables municipalities to modernize their assets incrementally without introducing any form of operational risk into the system. Proven, scalable solutions continue to shape procurement strategies in this fashion and have reinforced centrifugal pumps as the leading choice across municipal water and wastewater applications.

North America Municipal Water & Wastewater Pump Market Opportunity

Government Funding Unlocking Modernization Potential

Large-scale public investment programs realize significant future potential for equipment suppliers serving the North America municipal water & wastewater pump market. Federal funding programs designed to improve drinking water, wastewater, and stormwater infrastructure allow municipalities to accelerate capital improvement projects that had long been delayed. Funding mechanisms make such capital-intensive upgrades more economically feasible for utilities by removing past constraints, thus enabling overall modernization programs involving the upgrade of pumping stations, treatment plants, and distribution systems supplying millions of customers.

Government-funded projects tend to focus on reliability considerations, energy efficiency, and adherence to standardized specifications, which gives the edge in competitive selection to more established pump technologies and their manufacturers. Deployment of funds into the thousands of municipal systems should ensure a steady rise in procurement volumes, especially for replacement pumps and integrated systems designed for long operation. Meeting in the middle-the regulatory pressure, infrastructure aging, and public investment-creates a very favorable climate for sustained market growth, in which pump suppliers are likely to benefit from predictable demands linked with publicly funded infrastructure programs.

North America Municipal Water & Wastewater Pump Market Country Analysis

By Country

- US

- Canada

- Mexico

- Rest of North America

The United States dominates the North America municipal water & wastewater pump market, accounting for approximately 90% of regional demand. This leadership position reflects the country’s large population base and extensive network of municipally operated water systems serving urban, suburban, and rural communities. Thousands of aging treatment plants, pumping stations, and distribution networks across the U.S. require ongoing replacement and modernization, creating sustained demand for pumping equipment across all major applications.

Federal infrastructure programs further strengthen U.S. market leadership by accelerating upgrade timelines and expanding project scopes. National assessments continue to highlight the condition of drinking water and wastewater systems as below optimal, reinforcing the need for continued investment. Compared to Canada, the scale and geographic spread of U.S. municipal systems generate significantly higher equipment requirements. As funding deployment advances, American municipalities are expected to remain the primary source of demand growth, shaping overall regional market dynamics.

Unlock Market Intelligence

Explore the market potential with our data-driven report

North America Municipal Water & Wastewater Pump Market Segmentation Analysis

By Pump Type

- Centrifugal Pumps

- End Suction

- Split Case

- Vertical

- Turbine

- Axial Pump

- Mixed Flow Pump

- Submersible Pump

- Positive Displacement Pumps

- Progressing Cavity

- Diaphragm

- Gear Pump

- Others

Centrifugal pumps hold the highest market share in the North America municipal water & wastewater pump market, accounting for approximately 90% of total demand by pump type. Their dominance reflects suitability for the high-flow, continuous-duty requirements of municipal water treatment and distribution systems. These pumps are widely used across raw water intake, treatment processes, storage transfer, and distribution pumping, where consistent performance and operational efficiency are essential. Their ability to handle large volumes with relatively low maintenance requirements makes them the preferred choice for most municipal applications.

The continued preference for centrifugal pumps is reinforced by their cost-effectiveness over long operating lifecycles. Utilities value predictable maintenance schedules, ease of refurbishment, and broad availability of service expertise across North America. While positive displacement and specialty pumps address specific niche requirements, they remain secondary in overall adoption. As infrastructure modernization progresses, centrifugal systems are expected to maintain market leadership due to their established reliability, compatibility with existing networks, and strong acceptance among municipal engineers and planners.

By Application

- Water

- Wastewater

Under the application segment, water systems represent the largest share of the North America municipal water & wastewater pump market, capturing approximately 60% of total demand. Municipal investment priorities strongly favor potable water infrastructure, driven by the essential need to deliver safe and reliable drinking water to residential, commercial, and industrial end users. Pumping requirements within this segment span source extraction, treatment processes, storage facilities, and extensive distribution networks, all of which require consistent hydraulic performance and operational resilience.

Wastewater applications account for the remaining 40% of market demand, encompassing collection, conveyance, and treatment systems. While wastewater infrastructure remains critical, many municipalities have undertaken capacity upgrades in recent years, moderating immediate replacement urgency compared to water distribution assets. Regulatory emphasis on drinking water quality and system reliability continues to direct funding toward water applications, reinforcing their leading position. This application split reflects municipal priorities that place uninterrupted potable water supply ahead of wastewater conveyance in capital allocation decisions.

Various Market Players in North America Municipal Water & Wastewater Pump Market

The companies mentioned below are highly active in the North America municipal water & wastewater pump market, occupying a considerable portion of the market and shaping industry progress.

- KSB SE & Co. KGaA

- ITT Inc.

- Sulzer Ltd.

- Xylem Inc.

- Flowserve Corporation

- Grundfos Holding A/S

- Gorman-Rupp Company

- Pentair PLC

- Ebara Corporation

- Ingersoll Rand Inc.

Market News & Updates

- Xylem Inc., 2025:

Xylem’s all‑stock acquisition of Evoqua, valuing Evoqua at about 7.5 billion USD, combines Xylem’s global pump and water solutions portfolio with Evoqua’s advanced municipal and industrial water and wastewater treatment technologies, strong North American service network, and leadership in addressing emerging contaminants such as PFAS, creating a more integrated water technology platform capable of offering end‑to‑end solutions across the full water cycle for municipal, commercial, industrial and residential customers in North America.

- Gorman‑Rupp Company, 2025:

Gorman‑Rupp introduced the 6400 Series end‑suction centrifugal pumps in May 2025 as a cost‑effective solids‑handling line for flooded suction applications, engineered to move everything from clean liquids to solids‑laden mixtures in wastewater treatment plants, construction sites and mines, with 6‑ and 8‑inch discharge sizes, flows up to roughly 2,740 gallons per minute, heads up to about 170 feet and capability to pass 4‑inch solids, while leveraging interchangeable components from the Super T Series to simplify installation and maintenance for municipal and other infrastructure customers.

Frequently Asked Questions

Related Report

1. Market Segmentation

1.1. Research Scope

1.2. Research Methodology

1.3. Definitions and Assumptions

2. Executive Summary

3. North America Municipal Water & Wastewater Pump Market Policies, Regulations, and Standards

4. North America Municipal Water & Wastewater Pump Market Dynamics

4.1. Growth Factors

4.2. Challenges

4.3. Trends

4.4. Opportunities

5. North America Municipal Water & Wastewater Pump Market Statistics, 2022-2032F

5.1. Market Size & Growth Outlook

5.1.1.By Revenues in USD Million

5.1.2.By Units Sold in Million Units

5.2. Market Segmentation & Growth Outlook

5.2.1.By Pump Type

5.2.1.1. Centrifugal Pumps- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.1. End Suction- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.2. Split Case- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.3. Vertical- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.3.1. Turbine- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.3.2. Axial Pump- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.3.3. Mixed Flow Pump- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.4. Submersible Pump- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2. Positive Displacement Pumps- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2.1. Progressing Cavity- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2.2. Diaphragm- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2.3. Gear Pump- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2.4. Others- Market Insights and Forecast 2022-2032, USD Million

5.2.2.By Application

5.2.2.1. Water- Market Insights and Forecast 2022-2032, USD Million

5.2.2.2. Wastewater- Market Insights and Forecast 2022-2032, USD Million

5.2.3.By Country

5.2.3.1. US

5.2.3.2. Canada

5.2.3.3. Mexico

5.2.3.4. Rest of North America

5.2.4.By Competitors

5.2.4.1. Competition Characteristics

5.2.4.2. Market Share & Analysis

6. US Municipal Water & Wastewater Pump Market Statistics, 2022-2032F

6.1. Market Size & Growth Outlook

6.1.1.By Revenues in USD Million

6.1.2.By Units Sold in Million Units

6.2. Market Segmentation & Growth Outlook

6.2.1.By Pump Type- Market Insights and Forecast 2022-2032, USD Million

6.2.2.By Application - Market Insights and Forecast 2022-2032, USD Million

7. Canada Municipal Water & Wastewater Pump Market Statistics, 2022-2032F

7.1. Market Size & Growth Outlook

7.1.1.By Revenues in USD Million

7.1.2.By Units Sold in Million Units

7.2. Market Segmentation & Growth Outlook

7.2.1.By Pump Type- Market Insights and Forecast 2022-2032, USD Million

7.2.2.By Application - Market Insights and Forecast 2022-2032, USD Million

8. Mexico Municipal Water & Wastewater Pump Market Statistics, 2022-2032F

8.1. Market Size & Growth Outlook

8.1.1.By Revenues in USD Million

8.1.2.By Units Sold in Million Units

8.2. Market Segmentation & Growth Outlook

8.2.1.By Pump Type- Market Insights and Forecast 2022-2032, USD Million

8.2.2.By Application - Market Insights and Forecast 2022-2032, USD Million

9. Competitive Outlook

9.1. Company Profiles

9.1.1.Xylem Inc.

9.1.1.1. Business Description

9.1.1.2. Product Portfolio

9.1.1.3. Collaborations & Alliances

9.1.1.4. Recent Developments

9.1.1.5. Financial Details

9.1.1.6. Others

9.1.2.Flowserve Corporation

9.1.2.1. Business Description

9.1.2.2. Product Portfolio

9.1.2.3. Collaborations & Alliances

9.1.2.4. Recent Developments

9.1.2.5. Financial Details

9.1.2.6. Others

9.1.3.Grundfos Holding A/S

9.1.3.1. Business Description

9.1.3.2. Product Portfolio

9.1.3.3. Collaborations & Alliances

9.1.3.4. Recent Developments

9.1.3.5. Financial Details

9.1.3.6. Others

9.1.4.Gorman-Rupp Company

9.1.4.1. Business Description

9.1.4.2. Product Portfolio

9.1.4.3. Collaborations & Alliances

9.1.4.4. Recent Developments

9.1.4.5. Financial Details

9.1.4.6. Others

9.1.5.Pentair PLC

9.1.5.1. Business Description

9.1.5.2. Product Portfolio

9.1.5.3. Collaborations & Alliances

9.1.5.4. Recent Developments

9.1.5.5. Financial Details

9.1.5.6. Others

9.1.6.KSB SE & Co. KGaA

9.1.6.1. Business Description

9.1.6.2. Product Portfolio

9.1.6.3. Collaborations & Alliances

9.1.6.4. Recent Developments

9.1.6.5. Financial Details

9.1.6.6. Others

9.1.7.ITT Inc.

9.1.7.1. Business Description

9.1.7.2. Product Portfolio

9.1.7.3. Collaborations & Alliances

9.1.7.4. Recent Developments

9.1.7.5. Financial Details

9.1.7.6. Others

9.1.8.Sulzer Ltd.

9.1.8.1. Business Description

9.1.8.2. Product Portfolio

9.1.8.3. Collaborations & Alliances

9.1.8.4. Recent Developments

9.1.8.5. Financial Details

9.1.8.6. Others

9.1.9.Ebara Corporation

9.1.9.1. Business Description

9.1.9.2. Product Portfolio

9.1.9.3. Collaborations & Alliances

9.1.9.4. Recent Developments

9.1.9.5. Financial Details

9.1.9.6. Others

9.1.10. Ingersoll Rand Inc.

9.1.10.1. Business Description

9.1.10.2. Product Portfolio

9.1.10.3. Collaborations & Alliances

9.1.10.4. Recent Developments

9.1.10.5. Financial Details

9.1.10.6. Others

10. Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Pump Type |

|

| By Application |

|

| By Country |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.