Nigeria Room Air Conditioners Market Report: Trends, Growth and Forecast (2026-2032)

By Product Type (Split Air Conditioners (Up to 9,000 BTU/h, 9,001-12,000 BTU/h, 12,001-18,000 BTU/h, 18,001-24,000 BTU/h, Above 24,000 BTU/h), Window Air Conditioners (Up to 9,000 BTU/h, 9,001-12,000 BTU/h, 12,001-18,000 BTU/h, 18,001-24,000 BTU/h, Above 24,000 BTU/h), Others), By Technology (Inverter, Non-Inverter), By Price (Up to USD 300, USD 301 to USD 600, USD 601 to USD 1,000, Above USD 1,000), By End User (Residential (Individual Households, Apartments/Condominiums, Vacation/Secondary Homes), Commercial (Offices, Retail Stores/Showrooms, Hospitality, Healthcare Facilities, Educational Institutions, Small Commercial Establishments, Others)), By Sales Channel (Retail Online (Brand-Owned Websites/D2C, E-Commerce Marketplaces), Retail Offline (Exclusive Brand Stores, Multi-Brand Electronics & Appliance Stores, Specialty Stores, Hypermarkets/Supermarkets, Home Improvement Stores, Dealer/Distributor Network, Direct Sales/Institutional Sales, Local Independent Retailers)), By Refrigerant Type (R-32, R-410A, R-290, R-454B, Others), By Connectivity (Smart/Connected, Conventional/Non-Smart), By Energy Efficiency (1 Star, 2 Star, 3 Star, 4 Star, 5 Star), By Region (North Central, North East, North West, South East, Others) ... Read more

|

Major Players

|

Nigeria Room Air Conditioners Market Statistics and Insights, 2026

- Market Size Statistics

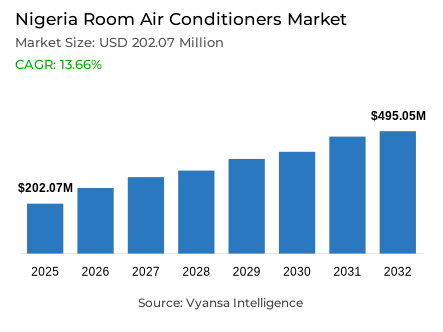

- Room air conditioners market size in Nigeria was valued at USD 202.07 million in 2025 and is estimated at USD 259.64 million in 2026.

- The market size is expected to grow to USD 495.05 million by 2032.

- Market to register a CAGR of around 13.66% during 2026-32.

- Product Type Shares

- Split air conditioners grabbed market share of 85%.

- Competition

- More than 10 companies are actively engaged in producing room air conditioners in Nigeria.

- Top 5 companies acquired around 80% of the market share.

- Royal United Nigeria Ltd, Midea Group Co Ltd, Panasonic Corp, Hisense Group, Haier Group etc., are few of the top companies.

- Sales Channel

- Retail offline grabbed 80% of the market.

Nigeria Room Air Conditioners Market Outlook

The Nigeria room air conditioners market was valued at USD 202.07 million in 2025, establishing a commercially meaningful foundation within the country's rapidly expanding home comfort appliance ecosystem. Projected to advance from USD 259.64 million in 2026 to USD 495.05 million by 2032, the sector registers a compound annual growth rate of 13.66% across the forecast horizon representing a near-tripling of market value that reflects the structural acceleration of cooling appliance demand across Nigeria's urbanizing, electricity-network-expanding consumer base. The pronounced value step-up from 2026 onward signals that institutional demand-creation factors including grid connectivity expansion, rising household income aspirations, and policy-driven efficiency standards are simultaneously compressing to generate accelerated commercial momentum across the forecast period.

The technological and product logic driving this market's expansion architecture is anchored in the overwhelming consumer preference for split air conditioner systems, which command approximately 85% of total product-type share. This concentration reflects a deliberate consumer judgment in favor of formats that deliver superior cooling performance, installation flexibility, noise reduction advantages, and aesthetic integration into residential spaces relative to window unit or portable alternatives. The scale of this preference consolidation with more than four-fifths of category demand concentrated in a single product format creates a highly focused competitive battleground where brand differentiation must be constructed on dimensions of energy efficiency, product reliability, after-sales service capability, and compliance with Nigeria's newly implemented Minimum Energy Performance Standards.

Consumer demand behavior within this market is shaped by the dual dynamics of an expanding electricity customer base and persistent running-cost sensitivity that moderates adoption velocity relative to underlying cooling need. The National Bureau of Statistics documents total electricity customers reaching 12.99 million in Q2 2024, reflecting 13.24% year-on-year growth a structural expansion of the addressable consumer universe that progressively converts latent cooling demand into active purchase consideration. Simultaneously, the 2024 Nigeria Residential Energy Demand-Side Survey reveals that 94.6% of air conditioning units in surveyed households were purchased new and 56.4% were three years old or below demonstrating that the market's active consumer cohort is oriented toward modern, performance-reliable products rather than extended dependence on aging installed stock.

The forward outlook through 2032 is defined by the convergence of grid formalization, energy efficiency policy implementation, and the progressive normalization of room air conditioners as planned household appliance investments rather than discretionary premium purchases. The International Energy Agency's documentation of Nigeria's official approval and implementation of Minimum Energy Performance Standards for air conditioners creates a structural policy tailwind that favors efficiency-capable suppliers and accelerates the replacement of lower-performance legacy units. As electricity customer formalization deepens and the addressable consumer base expands, brands with compliant, energy-efficient product portfolios and well-developed physical retail distribution networks are positioned to capture disproportionate value from the market's high-velocity expansion through 2032.

Nigeria Room Air Conditioners Market Growth DriverElectricity Network Expansion Progressively Widens the Addressable Consumer Universe

The sustained expansion of Nigeria's formal electricity customer base represents the primary structural driver of room air conditioner market growth, functioning as the foundational prerequisite that converts latent cooling demand present across virtually all Nigerian geographies given the country's tropical climate profile into active, actionable purchase consideration. Grid connectivity formalization transforms households from theoretical cooling appliance prospects into commercially accessible consumers for whom the economic calculus of air conditioner ownership becomes practically evaluable. Each incremental electricity connection effectively adds a household to the addressable room air conditioner market, creating a structural demand expansion mechanism that operates independently of marketing investment or consumer preference campaigns.

The quantitative momentum of this grid expansion driver is validated with precision by the National Bureau of Statistics. Total electricity customers in Nigeria reached 12.33 million in Q1 2024, representing 9.47% year-on-year growth, with metered customers standing at 5.91 million up 11.26% from Q1 2023. The expansion continued into Q2 2024, with total electricity customers advancing further to 12.99 million, reflecting 13.24% year-on-year growth. The accelerating pace of customer base expansion with the growth rate itself increasing from Q1 to Q2 2024 signals a structural electricity formalization dynamic that is progressively building the addressable consumer infrastructure for sustained room air conditioner demand expansion through 2032.

Nigeria Room Air Conditioners Market ChallengeInflationary Pressure and Running-Cost Sensitivity Constrain Adoption Velocity

The compound effect of headline inflation, uncertain power supply reliability, and household budget pressure constitutes a critical structural challenge for the Nigeria room air conditioners market, creating a cost-sensitivity environment that moderates purchase decision velocity relative to the underlying cooling demand intensity across the consumer base. Air conditioners represent among the highest-consumption household appliances in terms of ongoing electricity cost a characteristic that makes running-cost uncertainty particularly damaging to purchase conversion rates in a market where power supply consistency remains variable and electricity billing transparency is limited for a significant proportion of consumers. This cost-perception barrier disproportionately affects first-time adoption decisions among the middle-income consumer segments whose entry into the market would most significantly accelerate overall volume growth.

The structural depth of this challenge is quantified by National Bureau of Statistics data that contextualizes both the cost environment and its demand-dampening mechanics. Headline inflation reached 33.88% in October 2024, and while subsequent moderation brought it to 22.22% in June 2025, the sustained inflationary environment continues to compress household discretionary spending capacity across the consumer segments most proximate to air conditioning adoption thresholds. Compounding the affordability pressure, electricity supply stood at 5,769.52 GWh in Q1 2024 down 1.41% year-on-year while estimated billing customers reached 6.43 million in the same quarter, reflecting a large cohort of consumers whose electricity cost visibility remains imprecise. This combination of inflationary household budget pressure and power supply uncertainty creates a persistent adoption friction that brands must actively address through financing solutions, energy efficiency communication, and total cost-of-ownership value articulation through 2032.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Nigeria Room Air Conditioners Market TrendConsumer Preference Migrates Decisively Toward Newer, Performance-Reliable Products

The clear and measurable shift in Nigerian air conditioner consumer behavior toward newer product acquisition rather than extended utilization of aging installed stock represents a defining structural trend that reshapes the market's demand composition and elevates the strategic importance of product quality, reliability, and efficiency communication for brands competing for replacement and upgrade purchases. This trend reflects a maturation of consumer expectations within the category, wherein the initial priority of simply accessing cooling capability is progressively complemented by performance reliability requirements, daily-use dependability standards, and awareness of the operational cost advantages that newer, more efficient models deliver relative to older units operating at degraded performance levels.

The empirical foundation of this behavioral trend is documented with compelling specificity by the 2024 Nigeria Residential Energy Demand-Side Survey. Air conditioners in surveyed households are used for an average of 3.18 hours per day confirming meaningful daily utility integration rather than occasional use patterns. Critically, 94.6% of surveyed units were purchased new rather than second-hand, and 56.4% were three years old or below a recency profile that confirms the market's active consumer cohort is oriented toward modern product acquisition rather than prolonged legacy unit dependence. This preference for newer units creates a structurally supportive environment for regular replacement purchasing cycles, brand loyalty development around product reliability, and progressive premiumisation as consumers accumulate category experience and elevate their performance expectations through 2032.

Nigeria Room Air Conditioners Market OpportunityMinimum Energy Performance Standards Create a Compliance-Led Upgrade Market

The official approval and implementation of Minimum Energy Performance Standards for air conditioners in Nigeria, as documented by the International Energy Agency, creates a structurally significant and policy-backed commercial opportunity for brands with energy-efficient compliant product portfolios establishing a regulatory differentiation axis that progressively disadvantages lower-efficiency legacy products while creating clear consumer messaging frameworks around electricity savings, product quality, and formal standards compliance. For suppliers positioned on the right side of this efficiency threshold, the policy framework transforms voluntary premiumisation into a compliance-driven upgrade imperative, accelerating the replacement purchasing cycle for Nigeria's installed base of below-standard cooling units and creating a government-endorsed rationale for trading up to higher-efficiency products.

The commercial magnitude of this opportunity is amplified by the simultaneous expansion of Nigeria's formal electricity customer base, which the National Bureau of Statistics documents at 12.99 million in Q2 2024 reflecting 13.24% year-on-year growth. Each household newly entering the formal electricity system represents a potential first-time air conditioner purchaser whose initial product selection will occur within a standards-compliant market environment creating a generation of consumers whose category entry point is defined by efficiency-oriented products rather than legacy low-performance alternatives. Manufacturers and distributors that invest in standards-compliant product portfolio development, energy savings communication, and retail staff education around compliance benefits will capture disproportionate value from this policy-enabled upgrade market opportunity through 2032.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Nigeria Room Air Conditioners Market Segmentation Analysis

By Product Type

- Split Air Conditioners

- Up to 9,000 BTU/h

- 9,001-12,000 BTU/h

- 12,001-18,000 BTU/h

- 18,001-24,000 BTU/h

- Above 24,000 BTU/h

- Window Air Conditioners

- Up to 9,000 BTU/h

- 9,001-12,000 BTU/h

- 12,001-18,000 BTU/h

- 18,001-24,000 BTU/h

- Above 24,000 BTU/h

- Others

The segment with highest market share under the product type is split air conditioners, accounting for approximately 85% of the total market. This dominant position reflects a deeply entrenched consumer preference for a cooling format that delivers superior performance characteristics including precise temperature control, lower operational noise, enhanced aesthetic compatibility with residential interiors, and greater energy efficiency relative to alternative configurations across the diverse housing typologies that characterize Nigeria's urban and peri-urban residential landscape. With more than four-fifths of total market revenue concentrated within a single product category, split air conditioners function as the structural and commercial backbone of the Nigeria room air conditioners industry, defining manufacturing investment priorities, distribution channel development focus, and competitive brand positioning strategy across the entire value chain.

The structural leadership of split air conditioners is reinforced by the alignment between this format's performance and installation characteristics and the specific cooling requirements of Nigeria's predominantly apartment-based and mid-density urban residential stock. As Nigeria's officially implemented Minimum Energy Performance Standards for air conditioners as documented by the International Energy Agency progressively elevate the technical baseline for compliant products in this segment, the competitive differentiation axis within split air conditioners will shift toward energy efficiency ratings, smart connectivity features, and after-sales service reliability. Brands that invest in compliant, efficiency-optimized split system portfolios while building robust installation and maintenance service networks will command the strongest consumer trust and purchase conversion advantages within this dominant segment through 2032.

By Sales Channel

- Retail Online

- Brand-Owned Websites/D2C

- E-Commerce Marketplaces

- Retail Offline

- Exclusive Brand Stores

- Multi-Brand Electronics & Appliance Stores

- Specialty Stores

- Hypermarkets/Supermarkets

- Home Improvement Stores

- Dealer/Distributor Network

- Direct Sales/Institutional Sales

- Local Independent Retailers

The segment with highest market share under the sales channel is retail offline, accounting for approximately 80% of the total market. This commanding share reflects the fundamental role that physical retail environments play in the room air conditioner purchase decision process a category characterized by high unit values, significant installation implications, and complex product specification comparisons that consumers consistently prefer to evaluate through direct in-store engagement rather than digital-only discovery. The dominance of offline retail confirms that for Nigerian consumers, the air conditioner purchase journey remains anchored in tangible product assessment, direct seller interaction, and the immediate purchase confidence that physical store environments uniquely facilitate.

The structural entrenchment of offline retail as the dominant channel is further reinforced by the category's dependence on post-purchase installation and service relationships that physical retail touchpoints are better positioned to initiate and support relative to online alternatives. Retail outlets function not merely as transaction venues but as comprehensive commercial touchpoints where brand visibility, product demonstration, specification communication, and financing option presentation converge to support purchase conversion. As the market expands and consumer exposure to air conditioning products deepens, offline retail's influence over brand consideration sets, specification preferences, and final buying decisions will remain the most strategically critical channel capability for market participants to develop and maintain through 2032.

List of Companies Covered in Nigeria Room Air Conditioners Market

The companies listed below are highly influential in the Nigeria room air conditioners market, with a significant market share and a strong impact on industry developments.

- Royal United Nigeria Ltd

- Midea Group Co Ltd

- Panasonic Corp

- Hisense Group

- Haier Group

- Fareast Mercantile Co Ltd

- LG Corp

- Jiangsu Skyrun International Group

- Daikin Industries Ltd

- Gree Electric Appliances Inc of Zhuhai

Market News & Updates

- Midea Group Co Ltd, 2025:

Midea used its 2025 Port Harcourt Dealer Conference in Nigeria to introduce an updated AC lineup including standing, split, and cassette air conditioners, while specifically highlighting the UNICOOL range’s inverter efficiency, 5-Level GenGear for unstable voltage, generator compatibility, wide-voltage protection, and durability features tailored to Nigerian conditions. This is a strong Nigeria room-AC market update because it directly addresses local pain points such as power instability, cost of operation, and the need for resilient residential and small-commercial cooling.

- Panasonic Corp, 2025:

Panasonic Middle East & Africa announced in February 2025 that Nigeria is a strategic growth market and said it would place a strong focus on the air conditioning business, expanding climate-control solutions and product offerings for local residential and commercial demand. This is relevant to the Nigeria room AC market because it signals an official portfolio and channel push by a major global brand in a market where demand is being shaped by heat, energy efficiency needs, and growing interest in higher-quality cooling systems.

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- Nigeria Room Air Conditioners Market Policies, Regulations, and Standards

- Nigeria Room Air Conditioners Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- Nigeria Room Air Conditioners Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Units Sold in Thousand Units

- Market Segmentation & Growth Outlook

- By Product Type

- Split Air Conditioners- Market Insights and Forecast 2022-2032, USD Million

- Up to 9,000 BTU/h- Market Insights and Forecast 2022-2032, USD Million

- 9,001-12,000 BTU/h- Market Insights and Forecast 2022-2032, USD Million

- 12,001-18,000 BTU/h- Market Insights and Forecast 2022-2032, USD Million

- 18,001-24,000 BTU/h- Market Insights and Forecast 2022-2032, USD Million

- Above 24,000 BTU/h- Market Insights and Forecast 2022-2032, USD Million

- Window Air Conditioners- Market Insights and Forecast 2022-2032, USD Million

- Up to 9,000 BTU/h- Market Insights and Forecast 2022-2032, USD Million

- 9,001-12,000 BTU/h- Market Insights and Forecast 2022-2032, USD Million

- 12,001-18,000 BTU/h- Market Insights and Forecast 2022-2032, USD Million

- 18,001-24,000 BTU/h- Market Insights and Forecast 2022-2032, USD Million

- Above 24,000 BTU/h- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- Split Air Conditioners- Market Insights and Forecast 2022-2032, USD Million

- By Technology

- Inverter- Market Insights and Forecast 2022-2032, USD Million

- Non-Inverter- Market Insights and Forecast 2022-2032, USD Million

- By Price

- Up to USD 300- Market Insights and Forecast 2022-2032, USD Million

- USD 301 to USD 600- Market Insights and Forecast 2022-2032, USD Million

- USD 601 to USD 1,000- Market Insights and Forecast 2022-2032, USD Million

- Above USD 1,000- Market Insights and Forecast 2022-2032, USD Million

- By End User

- Residential- Market Insights and Forecast 2022-2032, USD Million

- Individual Households- Market Insights and Forecast 2022-2032, USD Million

- Apartments/Condominiums- Market Insights and Forecast 2022-2032, USD Million

- Vacation/Secondary Homes- Market Insights and Forecast 2022-2032, USD Million

- Commercial- Market Insights and Forecast 2022-2032, USD Million

- Offices- Market Insights and Forecast 2022-2032, USD Million

- Retail Stores/Showrooms- Market Insights and Forecast 2022-2032, USD Million

- Hospitality- Market Insights and Forecast 2022-2032, USD Million

- Healthcare Facilities- Market Insights and Forecast 2022-2032, USD Million

- Educational Institutions- Market Insights and Forecast 2022-2032, USD Million

- Small Commercial Establishments- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- Residential- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel

- Retail Online- Market Insights and Forecast 2022-2032, USD Million

- Brand-Owned Websites/D2C- Market Insights and Forecast 2022-2032, USD Million

- E-Commerce Marketplaces- Market Insights and Forecast 2022-2032, USD Million

- Retail Offline- Market Insights and Forecast 2022-2032, USD Million

- Exclusive Brand Stores- Market Insights and Forecast 2022-2032, USD Million

- Multi-Brand Electronics & Appliance Stores- Market Insights and Forecast 2022-2032, USD Million

- Specialty Stores- Market Insights and Forecast 2022-2032, USD Million

- Hypermarkets/Supermarkets- Market Insights and Forecast 2022-2032, USD Million

- Home Improvement Stores- Market Insights and Forecast 2022-2032, USD Million

- Dealer/Distributor Network- Market Insights and Forecast 2022-2032, USD Million

- Direct Sales/Institutional Sales- Market Insights and Forecast 2022-2032, USD Million

- Local Independent Retailers- Market Insights and Forecast 2022-2032, USD Million

- Retail Online- Market Insights and Forecast 2022-2032, USD Million

- By Refrigerant Type

- R-32- Market Insights and Forecast 2022-2032, USD Million

- R-410A- Market Insights and Forecast 2022-2032, USD Million

- R-290- Market Insights and Forecast 2022-2032, USD Million

- R-454B- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By Connectivity

- Smart/Connected- Market Insights and Forecast 2022-2032, USD Million

- Conventional/Non-Smart- Market Insights and Forecast 2022-2032, USD Million

- By Energy Efficiency

- 1 Star- Market Insights and Forecast 2022-2032, USD Million

- 2 Star- Market Insights and Forecast 2022-2032, USD Million

- 3 Star- Market Insights and Forecast 2022-2032, USD Million

- 4 Star- Market Insights and Forecast 2022-2032, USD Million

- 5 Star- Market Insights and Forecast 2022-2032, USD Million

- By Region

- North Central

- North East

- North West

- South East

- Others

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Product Type

- Market Size & Growth Outlook

- Nigeria Split Air Conditioners Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Units Sold in Thousand Units

- Market Segmentation & Growth Outlook

- By Technology- Market Insights and Forecast 2022-2032, USD Million

- By Price- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Refrigerant Type- Market Insights and Forecast 2022-2032, USD Million

- By Connectivity- Market Insights and Forecast 2022-2032, USD Million

- By Energy Efficiency- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Nigeria Window Air Conditioners Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Units Sold in Thousand Units

- Market Segmentation & Growth Outlook

- By Technology- Market Insights and Forecast 2022-2032, USD Million

- By Price- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Refrigerant Type- Market Insights and Forecast 2022-2032, USD Million

- By Connectivity- Market Insights and Forecast 2022-2032, USD Million

- By Energy Efficiency- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- Hisense Group

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Haier Group

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Fareast Mercantile Co Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- LG Corp

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Jiangsu Skyrun International Group

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Royal United Nigeria Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Midea Group Co Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Panasonic Corp

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Daikin Industries Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Gree Electric Appliances Inc of Zhuhai

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Hisense Group

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Product Type |

|

| By Technology |

|

| By Price |

|

| By End User |

|

| By Sales Channel |

|

| By Refrigerant Type |

|

| By Connectivity |

|

| By Energy Efficiency |

|

| By Region |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.