Netherlands Bags and Luggage Market Report: Trends, Growth and Forecast (2026-2032)

By Category (Bags (Cross Body Bags, Bags and Backpacks, Business Bags, Duffle Bags, Clutches, Others), Luggage (Soft Luggage, Hard Luggage, Wheeled Luggage, Non-Wheeled Luggage)), By Sales Channel (Retail Offline, Retail Online), By Material Type (Soft Case (Nylon, Polyester, Ballistic Nylon), Hard Case (Polycarbonate, ABS (Acrylonitrile Butadiene Styrene), Polypropylene)), By Price Category (Luxury, Mass/Economy, Premium), By Application (Travel, Business) ... Read more

|

Major Players

|

Netherlands Bags and Luggage Market Statistics and Insights, 2026

- Market Size Statistics

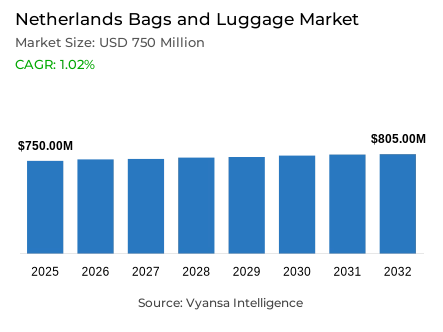

- Bags and luggage market size in Netherlands was estimated at USD 750 million in 2025.

- The market size is expected to grow to USD 805 million by 2032.

- Market to register a CAGR of around 1.02% during 2026-32.

- Category Shares

- Bags grabbed market share of 70%.

- Competition

- More than 20 companies are actively engaged in producing bags and luggage in Netherlands.

- Top 5 companies acquired around 30% of the market share.

- Gils Investment Fund NV, Delsey SA, Magazijn de Bijenkorf BV, Samsonite BV, VF (J) Nederland BV etc., are few of the top companies.

- Sales Channel

- Retail offline grabbed 80% of the market.

Netherlands Bags and Luggage Market Outlook

The Netherlands bags and luggage market is estimated at USD 750 million in 2025 and is projected to reach USD 785 million by 2032, registering a CAGR of around 0.65% during 2026–32. The market is expected to record modest but stable growth, reflecting its mature nature and relatively cautious consumer spending environment. While overall expansion will be limited, demand will remain supported by consumers’ ongoing interest in functional, durable, and well-designed personal accessories.

Bags will continue to represent the core of the market, accounting for a substantial share of total sales. Dutch consumers increasingly view bags as everyday essentials that combine practicality with personal style, supporting steady replacement cycles. The growing acceptance of bags among male consumers, along with rising demand for locally produced and sustainably positioned products, will further underpin category stability. Brands that emphasise quality craftsmanship and timeless design are likely to perform better than trend-driven, short-lifecycle offerings.

Luggage demand will be primarily sustained by continued travel activity, particularly short breaks and international holidays. Innovation focused on lightweight construction, enhanced functionality, and visual differentiation will remain important in maintaining consumer interest. Niche developments, including customisable luggage and solutions designed for specific use cases, are expected to contribute incremental growth rather than transform overall market dynamics.

From a distribution perspective, retail offline will remain the dominant sales channel, supported by consumer preference for in-store evaluation of materials, size, and build quality. While retail e-commerce will continue to play a complementary role through promotions and product discovery, physical retail is expected to retain a central position, particularly for mid- to high-value purchases.

Netherlands Bags and Luggage Market Growth Driver

Travel-Oriented Lifestyles Sustain Replacement Demand

Frequent travel patterns represent a core demand driver for bags and luggage in the Netherlands, as mobility-oriented lifestyles continue to encourage regular product replacement and periodic upgrades.Statistics Netherlands (CBS) reported that in 2023, Dutch residents made 37.6 million holiday trips, of which 20.9 million were outbound trips, indicating a continued interest in leisure travel. Frequent movement causes damage to luggage, which supports the need to have durable, lightweight, and useful products that can support frequent use during domestic and international travels.

This mobility-based demand environment is further supported by spending data. According to CBS, the spending on tourism activities in the Netherlands amounts to EUR 111.2 billion in 2024, which demonstrates the economic importance of traveling activities. High travel expenditure favours the purchase of travel related accessories such as bags and luggage because end user focus on quality and functionality to supplement frequent travel and long mobility trends.

Netherlands Bags and Luggage Market Challenge

Heightened Price Awareness Constrains Value Expansion

The challange of price sensitivity is a structural problem to discretionary product categories in the Netherlands. Statistics Netherlands (CBS) states that the average consumer prices have increased by 4.1% annually in January 2024, which indicates the ongoing inflationary pressure on household budgets. An increase in the cost of living is prompting end user to reevaluate non-essential spending, such as bags and luggage, and tend to postpone upgrades or find less expensive options to be more mindful of discretionary spending.

This pricing situation increases the intensity of competition within the category. end user are more price-sensitive, comparing prices across various channels and reacting very well to promotions, making them less tolerant of high prices. With the increasing dependence of brands on discounts to drive demand, it becomes difficult to sustain margins, and value growth is constrained despite the fact that the underlying demand of bags and luggage is not declining.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Netherlands Bags and Luggage Market Trend

Functional Design Shapes Everyday Usage Patterns

The shift in mobility and digitally connected lifestyles still affects the expectations of bags and luggage in the Netherlands. According to Eurostat, 83% of people in the Netherlands access mobile internet every day, which shows that the population is highly mobile and dependent on digital devices. This trend favours the need to have small, lightweight, and ergonomic designs that can carry daily necessities effectively without reducing comfort.

In addition to functionality, bags and luggage are becoming lifestyle accessories that are used on a daily basis and not on a special occasion basis. end user prefer products that are attractive and yet functional, which prompts manufacturers to incorporate design-based aspects with durability and convenience. This structural change influences the product development strategies, whereby the focus is on versatility, comfort, and long-term use in a variety of settings.

Netherlands Bags and Luggage Market Opportunity

Sustainability-Led Differentiation Supports Long-Term Growth

Sustainability is also becoming a factor in consumer buying behavior in the Netherlands, and it opens the possibility of differentiation in bags and luggage. The European Commission states that 74% of Dutch end user take into account the environmental impact when making a purchase, which supports the demand on products that prove to be durable, responsibly sourced, and with a smaller environmental footprint. Brands that match product messages with sustainability values enhance relevance among environmentally conscious end user.

Simultaneously, larger social changes favor the need of inclusive and convenient designs. An ageing population and heightened sensitivity to accessibility are driving the demand towards lightweight, ergonomic, and easy-to-carry luggage solutions. Sustainable products with functional simplicity are in a good position to take the long-term demand and strengthen premium positioning without depending on aggressive pricing.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Netherlands Bags and Luggage Market Segmentation Analysis

By Category

- Bags

- Cross Body Bags

- Bags and Backpacks

- Business Bags

- Duffle Bags

- Clutches

- Others

- Luggage

- Soft Luggage

- Hard Luggage

- Wheeled Luggage

- Non-Wheeled Luggage

The segment with highest market share under category is bags, which occupies approximately 70% of the market. This superiority is a manifestation of the necessity and dailyness of bags that are utilized in work, recreational, and traveling events. Bags are more frequently replaced than luggage and are more directly associated with lifestyle and fashion choices, which helps maintain steady demand even in times of economic restraint. The bags segment is facilitated by consumer preference towards versatility, durability, and design quality.

Compact everyday formats, crossbody bags, and backpacks are becoming popular as end user lead more mobile and flexible lifestyles. Moreover, the growing interest in sustainability is stimulating the demand in locally-made bags and materials that are responsibly sourced. Consequently, the bags segment will maintain its top position during the forecast period.

By Sales Channel

- Retail Offline

- Retail Online

The retail offline segment has the largest share under the sales channel with approximately 80% of the market. Physical stores remain to be a very important factor because people want to be able to evaluate the quality, weight, and functionality of products with their own hands and make a purchase decision. This is especially applicable to more expensive bags and luggage, where the tactile assessment affects the confidence of buyers. The advantages of specialty stores and department stores include edited collections and in-store knowledge, which promote conversion and brand loyalty.

Despite the fact that retail retail online is still significant in terms of price comparison and promotion, it does not substitute offline purchasing but complements it. Retail offline will continue to dominate the market in the next few years, with the help of experiential retail formats and selective integration of omnichannels.

List of Companies Covered in Netherlands Bags and Luggage Market

The companies listed below are highly influential in the Netherlands bags and luggage market, with a significant market share and a strong impact on industry developments.

- Gils Investment Fund NV

- Delsey SA

- Magazijn de Bijenkorf BV

- Samsonite BV

- VF (J) Nederland BV

- Chanel BV

- Tapestry Inc

- Michael Kors (Netherlands) BV

- Castelijn & Beerens BV

- FreSh BV

Competitive Landscape

The Netherlands’ bags and luggage market is competitive, led by established international and domestic brands alongside fast-growing niche players. Samsonite BV retains leadership in luggage through continuous product innovation, strong promotional activity, and a clear tiered brand strategy spanning premium and affordable segments via Samsonite and American Tourister. Dutch brands such as SUITSUIT have strengthened their positions by combining fashion-led design, customisation, and accessible pricing, appealing particularly to younger consumers. At the same time, local and sustainability-focused brands including SoDutch, Smaak Amsterdam, Oh My Bag, and Nortvi are gaining traction by emphasising craftsmanship, ethical sourcing, and durability. Competition is intensifying further through retail e-commerce, with players like Bol.com, Zalando, and new entrants such as Temu using aggressive pricing and promotions to capture value-conscious shoppers.

Frequently Asked Questions

Related Report

1. Market Segmentation

1.1. Research Scope

1.2. Research Methodology

1.3. Definitions and Assumptions

2. Executive Summary

3. Netherlands Bags and Luggage Market Policies, Regulations, and Standards

4. Netherlands Bags and Luggage Market Dynamics

4.1. Growth Factors

4.2. Challenges

4.3. Trends

4.4. Opportunities

5. Netherlands Bags and Luggage Market Statistics, 2022-2032F

5.1. Market Size & Growth Outlook

5.1.1.By Revenues in USD Million

5.1.2.By Units Sold in Thousand Units

5.2. Market Segmentation & Growth Outlook

5.2.1.By Category

5.2.1.1. Bags- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.1. Cross Body Bags- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.2. Bags and Backpacks- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.3. Business Bags- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.4. Duffle Bags- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.5. Clutches- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.6. Others- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2. Luggage- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2.1. Soft Luggage- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2.2. Hard Luggage- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2.3. Wheeled Luggage- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2.4. Non-Wheeled Luggage- Market Insights and Forecast 2022-2032, USD Million

5.2.2.By Sales Channel

5.2.2.1. Retail Offline- Market Insights and Forecast 2022-2032, USD Million

5.2.2.2. Retail Online- Market Insights and Forecast 2022-2032, USD Million

5.2.3.By Material Type

5.2.3.1. Soft Case- Market Insights and Forecast 2022-2032, USD Million

5.2.3.1.1. Nylon- Market Insights and Forecast 2022-2032, USD Million

5.2.3.1.2. Polyester- Market Insights and Forecast 2022-2032, USD Million

5.2.3.1.3. Ballistic Nylon- Market Insights and Forecast 2022-2032, USD Million

5.2.3.2. Hard Case- Market Insights and Forecast 2022-2032, USD Million

5.2.3.2.1. Polycarbonate- Market Insights and Forecast 2022-2032, USD Million

5.2.3.2.2. ABS (Acrylonitrile Butadiene Styrene)- Market Insights and Forecast 2022-2032, USD Million

5.2.3.2.3. Polypropylene- Market Insights and Forecast 2022-2032, USD Million

5.2.4.By Price Category

5.2.4.1. Luxury- Market Insights and Forecast 2022-2032, USD Million

5.2.4.2. Mass/Economy- Market Insights and Forecast 2022-2032, USD Million

5.2.4.3. Premium- Market Insights and Forecast 2022-2032, USD Million

5.2.5.By Application

5.2.5.1. Travel- Market Insights and Forecast 2022-2032, USD Million

5.2.5.2. Business- Market Insights and Forecast 2022-2032, USD Million

5.2.6.By Competitors

5.2.6.1. Competition Characteristics

5.2.6.2. Market Share & Analysis

6. Netherlands Bags Market Statistics, 2022-2032

6.1. Market Size & Growth Outlook

6.1.1.By Revenues in USD Million

6.1.2.By Units Sold in Thousand Units

6.2. Market Segmentation & Growth Outlook

6.2.1.By Category- Market Insights and Forecast 2022-2032, USD Million

6.2.2.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

6.2.3.By Material Type- Market Insights and Forecast 2022-2032, USD Million

6.2.4.By Price Category- Market Insights and Forecast 2022-2032, USD Million

6.2.5.By Application- Market Insights and Forecast 2022-2032, USD Million

7. Netherlands Luggage Market Statistics, 2022-2032

7.1. Market Size & Growth Outlook

7.1.1.By Revenues in USD Million

7.1.2.By Units Sold in Thousand Units

7.2. Market Segmentation & Growth Outlook

7.2.1.By Category- Market Insights and Forecast 2022-2032, USD Million

7.2.2.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

7.2.3.By Material Type- Market Insights and Forecast 2022-2032, USD Million

7.2.4.By Price Category- Market Insights and Forecast 2022-2032, USD Million

7.2.5.By Application- Market Insights and Forecast 2022-2032, USD Million

8. Competitive Outlook

8.1. Company Profiles

8.1.1.Samsonite BV

8.1.1.1. Business Description

8.1.1.2. Product Portfolio

8.1.1.3. Collaborations & Alliances

8.1.1.4. Recent Developments

8.1.1.5. Financial Details

8.1.1.6. Others

8.1.2.VF (J) Nederland BV

8.1.2.1. Business Description

8.1.2.2. Product Portfolio

8.1.2.3. Collaborations & Alliances

8.1.2.4. Recent Developments

8.1.2.5. Financial Details

8.1.2.6. Others

8.1.3.Chanel BV

8.1.3.1. Business Description

8.1.3.2. Product Portfolio

8.1.3.3. Collaborations & Alliances

8.1.3.4. Recent Developments

8.1.3.5. Financial Details

8.1.3.6. Others

8.1.4.Tapestry Inc

8.1.4.1. Business Description

8.1.4.2. Product Portfolio

8.1.4.3. Collaborations & Alliances

8.1.4.4. Recent Developments

8.1.4.5. Financial Details

8.1.4.6. Others

8.1.5.Michael Kors (Netherlands) BV

8.1.5.1. Business Description

8.1.5.2. Product Portfolio

8.1.5.3. Collaborations & Alliances

8.1.5.4. Recent Developments

8.1.5.5. Financial Details

8.1.5.6. Others

8.1.6.Gils Investment Fund NV

8.1.6.1. Business Description

8.1.6.2. Product Portfolio

8.1.6.3. Collaborations & Alliances

8.1.6.4. Recent Developments

8.1.6.5. Financial Details

8.1.6.6. Others

8.1.7.Delsey SA

8.1.7.1. Business Description

8.1.7.2. Product Portfolio

8.1.7.3. Collaborations & Alliances

8.1.7.4. Recent Developments

8.1.7.5. Financial Details

8.1.7.6. Others

8.1.8.Magazijn de Bijenkorf BV

8.1.8.1. Business Description

8.1.8.2. Product Portfolio

8.1.8.3. Collaborations & Alliances

8.1.8.4. Recent Developments

8.1.8.5. Financial Details

8.1.8.6. Others

8.1.9.Castelijn & Beerens BV

8.1.9.1. Business Description

8.1.9.2. Product Portfolio

8.1.9.3. Collaborations & Alliances

8.1.9.4. Recent Developments

8.1.9.5. Financial Details

8.1.9.6. Others

8.1.10. FreSh BV

8.1.10.1. Business Description

8.1.10.2. Product Portfolio

8.1.10.3. Collaborations & Alliances

8.1.10.4. Recent Developments

8.1.10.5. Financial Details

8.1.10.6. Others

9. Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Category |

|

| By Sales Channel |

|

| By Material Type |

|

| By Price Category |

|

| By Application |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.