Italy Water & Wastewater Pump Market Report: Trends, Growth and Forecast (2026-2032)

By Pump Type (Centrifugal Pumps (End Suction, Split Case, Vertical (Turbine, Axial Pump, Mixed Flow Pump), Submersible Pump), Positive Displacement Pumps (Progressing Cavity, Diaphragm, Gear Pump, Others)), By Application (Water, Wastewater), By End User (Industrial Water & Wastewater, Municipal Water & Wastewater) ... Read more

|

Major Players

|

Italy Water & Wastewater Pump Market Statistics and Insights, 2026

- Market Size Statistics

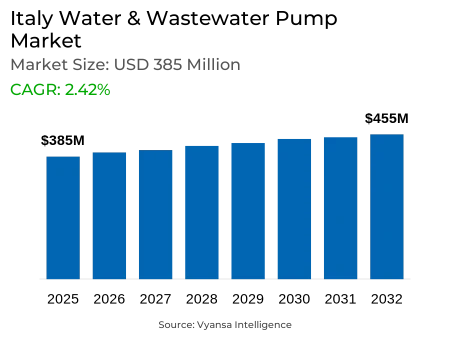

- Water & Wastewater Pump in Italy is estimated at $ 385 Million.

- The market size is expected to grow to $ 455 Million by 2032.

- Market to register a CAGR of around 2.42% during 2026-32.

- Pump Type Segment

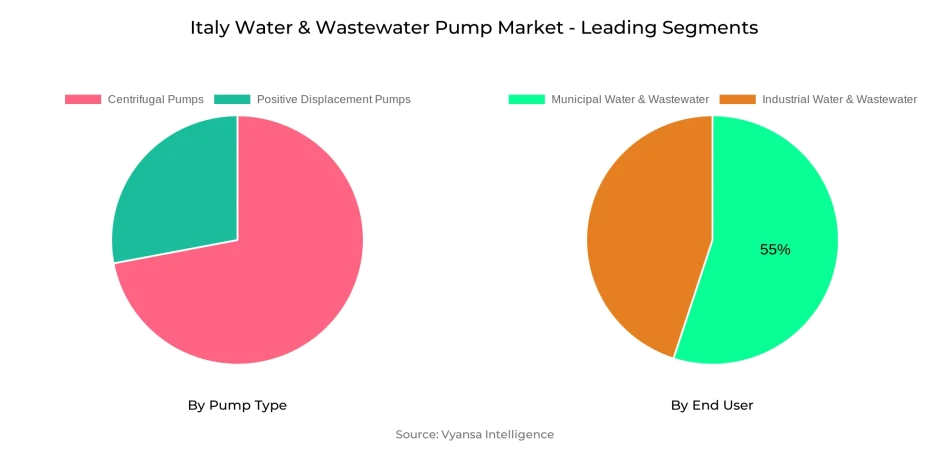

- Centrifugal Pumps continues to dominate the market.

- Competition

- More than 10 companies are actively engaged in producing Water & Wastewater Pump in Italy.

- Top 5 companies acquired the maximum share of the market.

- ITT, IDEX, Dover, Flowserve, Sulzer AG etc., are few of the top companies.

- End User

- Municipal Water & Wastewater grabbed 55% of the market.

Italy Water & Wastewater Pump Market Outlook

Italy presents tremendous growth opportunities for the water and wastewater pump market, supported by tremendous government investment and upgradation initiatives. Worth $385 million in 2025, the market is forecast to grow to $455 million in 2032. The nation also suffers from huge network losses, losing around 42% of its drinking water and nearly 25% of pipes that are more than 50 years old. To cater to this, initiatives like the €2.1 billion PNRR program for leakage saving and €4 billion for building 25,000km of new pipelines have been initiated. With Italy being placed third in Europe in terms of freshwater abstraction per capita at 155 cubic meters per year, effective pumping solutions are necessary to satisfy increased municipal and industrial demand.

Regulatory compliance is the key driver influencing market growth. Italy has cut non-compliant areas of wastewater from 41 earlier to four now but remains under EU infringement procedures, since 11% of wastewater is still not treated by EU regulations. The European Court of Justice financial sanctions quicken the process of modernization. With an estimated 18,000 wastewater treatment plants functioning around the country, utilities are pushed to upgrade pumping facilities, improving technical quality and conformity despite being a challenge for smaller operators.

Digitalisation is becoming the hallmark trend. To date, just 17% of Italy's 21 million water meters are digitalised, leaving an €250 million modernisation opportunity on the table. €900 million has been allocated by the government to digital monitoring and smart network programmes under PNRR. IoT-enabled pumps, AI systems, and real-time monitoring are becoming ever more mainstream in new projects. Europe's digital water industry, which spans Italy, is to double by 2033, with SCADA, GIS, and metering equipment accounting for over 75% of growth.

Water and wastewater municipalities lead the market, with 55% of pump demand being required in 2025, owing to Italy's massive public infrastructure covering more than 84% of citizens. Centrifugal pumps remain the market leader because they are tried and tested for reliability and efficiency across massive applications. Concurrently, the industrial water and wastewater segment is the most rapidly growing segment with 3.61% CAGR as manufacturing, energy, and chemical industries embrace sustainable practices. These drivers combined are poised to maintain consistent growth in Italy's pump market until 2032.

Italy Water & Wastewater Pump Market Growth Driver

Aging Infrastructure Demands Urgent Modernization Driving Market Growth

Italy has considerable water infrastructure issues that have strong demand on high-end pump systems. It loses about 42% of its drinking water as network losses, with 25% of the networks distributing water more than 50 years old and 60% over 30 years old. This waste amounts to enough wasted water per year to supply 43 million individuals.

The government retaliates with large-scale investment schemes, such as the €2.1 billion PNRR scheme for the reduction of leakage and €4 billion towards the construction of 25,000km of new water distribution networks. Italy is third in Europe for freshwater abstraction per capita at 155 cubic meters per year, thus emphasizing the imperative importance of efficient pumping infrastructure to cater to this huge water demand from municipal and industrial sectors.

Italy Water & Wastewater Pump Market Challenge

Regulatory Compliance Creates Market Challenges Hindering Market Growth

Italy still has issues with EU wastewater and water treatment standards, generating operational concerns that affect market dynamics. The European Court of Justice levied financial sanctions of €10 million plus €13.7 million for each six-month delay because of insufficient urban wastewater treatment in four agglomerations. Although 41 non-compliant zones improved earlier to only four in 2025, issues with compliance remain in sensitive zones of discharge.

The nation is plagued by consistent EU infringement proceedings, having 11% of wastewater not yet treated as per EU regulations. Italy has around 18,000 wastewater treatment plants that treat 68 million population equivalent, but are plagued by recurring technical quality issues and monitoring problems. These regulatory burdens compel utilities to modernize treatment structures, albeit the intricacy and expense of conformity pose implementation challenges for smaller operators who manage distributed network infrastructure.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Italy Water & Wastewater Pump Market Trend

Digital Water Solutions Drive Market Innovation

Italy is embracing digital water management as a leading market trend, with the adoption of smart technology on the move in the industry. As it stands, just 17% of Italy's 21 million water meters are already digitized, posing an enormous modernization opportunity of €250 million in tender announcements. The government provided €900 million for digitization and network monitoring initiatives, upgrading legacy systems to smart networks under PNRR.

More advanced technologies such as IoT sensors, intelligent meters, and real-time monitoring systems are being made mandatory for new pump installations. The digital water market in Europe, including Italy, is predicted to double from 2025 by 2033, and more than 75% of growth will come from traditional SCADA, GIS, and metering hardware. Italian utilities increasingly integrate cloud and AI solutions for data-driven intelligence, while cybersecurity expenditure expands at good CAGR as regulatory compliance demands tighten for the water sector.

Italy Water & Wastewater Pump Market Opportunity

Infrastructure Investment Creates Growth Opportunities

Italy presents significant opportunities through unprecedented water sector investment programs that directly benefit pump manufacturers and suppliers. The National Recovery and Resilience Plan allocated €4.4 billion for water infrastructure, with €1.4 billion already awarded through tenders and 124 projects totaling €2 billion identified nationwide. The European Investment Bank provided over €4 billion to Italy's water sector in the past decade, more than any other country.

City utilities increasingly co-operate on mass projects, as in Viveracqua's €2 billion investment program covering 3 million citizens through a 30,000km network. The government aim to cut water network losses by 13% by 2026 generates steady demand for cost-effective pumping technology. Furthermore, industrial water treatment demands fuel expansion, with the highest-growing segment growing at 3.61% CAGR as manufacturing, energy, and chemical industries make sustainable methods a priority in response to tight environmental regulation.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Italy Water & Wastewater Pump Market Segmentation Analysis

By Pump Type

- Centrifugal Pumps

- Positive Displacement Pumps

The most dominant segment in the category of Pump Type with respect to market share is Centrifugal Pumps, which retains its position in dominance in the market scenario. Centrifugal pumps retain the top spot because of their efficiency, reliability, and applicability to large-scale municipal water supply and distribution networks typical of Italy's infrastructure requirements.

This predominance is a testimonial to the technology's well-established performance in managing Italy's high-volume, continuous-flow needs crucial for its vast water networks that cater to more than 59 million citizens. The use of centrifugal technology also supports continued digitalization and intelligent infrastructure advancements since these pumps find it easy to integrate with sophisticated monitoring and control systems being installed throughout the nation's upgrading water sector.

By End User

- Industrial Water & Wastewater

- Municipal Water & Wastewater

The most dominant market share under End User is that of Municipal Water & Wastewater, which captured 55% of the market. Such a large share is indicative of Italy's enormous public water infrastructure serving around 84.1% of citizens with water utilities and large municipal networks demanding constant pumping capacity for supply and treatment activities.

Municipal dominance is a result of Italy's centralised strategy to deliver water services and the current €4.4 billion PNRR programme modernising public infrastructure. Yet, the fastest expanding End User segment is Industrial Water & Wastewater, at a CAGR of 3.61%, supported by manufacturing, energy, and chemical industries using enhanced treatment solutions to comply with more rigorous environmental regulations and sustainability needs in a wide range of industrial applications.

Top Companies in Italy Water & Wastewater Pump Market

The top companies operating in the market include ITT, IDEX, Dover, Flowserve, Sulzer AG, KSB, Xylem, Grundfos, Ebara, SPX Flow, etc., are the top players operating in the Italy Water & Wastewater Pump Market.

Frequently Asked Questions

Related Report

1. Market Segmentation

1.1. Research Scope

1.2. Research Methodology

1.3. Definitions and Assumptions

2. Executive Summary

3. Italy Water & Wastewater Pump Market Policies, Regulations, and Standards

4. Italy Water & Wastewater Pump Market Dynamics

4.1. Growth Factors

4.2. Challenges

4.3. Trends

4.4. Opportunities

5. Italy Water & Wastewater Pump Market Statistics, 2022-2032F

5.1. Market Size & Growth Outlook

5.1.1.By Revenues in US$ Million

5.2. Market Segmentation & Growth Outlook

5.2.1.By Pump Type

5.2.1.1. Centrifugal Pumps- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.1. End Suction- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.2. Split Case- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.3. Vertical- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.3.1. Turbine- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.3.2. Axial Pump- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.3.3. Mixed Flow Pump- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.4. Submersible Pump- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2. Positive Displacement Pumps- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2.1. Progressing Cavity- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2.2. Diaphragm- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2.3. Gear Pump- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2.4. Others- Market Insights and Forecast 2022-2032, USD Million

5.2.2.By Application

5.2.2.1. Water- Market Insights and Forecast 2022-2032, USD Million

5.2.2.2. Wastewater- Market Insights and Forecast 2022-2032, USD Million

5.2.3.By End User

5.2.3.1. Industrial Water & Wastewater- Market Insights and Forecast 2022-2032, USD Million

5.2.3.2. Municipal Water & Wastewater- Market Insights and Forecast 2022-2032, USD Million

5.2.4.By Competitors

5.2.4.1. Competition Characteristics

5.2.4.2. Market Share & Analysis

6. Italy Centrifugal Water & Wastewater Pump Market Statistics, 2020-2030F

6.1. Market Size & Growth Outlook

6.1.1.By Revenues in US$ Million

6.2. Market Segmentation & Growth Outlook

6.2.1.By Pump Type- Market Insights and Forecast 2022-2032, USD Million

6.2.2.By Application- Market Insights and Forecast 2022-2032, USD Million

6.2.3.By End User- Market Insights and Forecast 2022-2032, USD Million

7. Italy Positive Displacement Water & Wastewater Pump Market Statistics, 2020-2030F

7.1. Market Size & Growth Outlook

7.1.1.By Revenues in US$ Million

7.2. Market Segmentation & Growth Outlook

7.2.1.By Pump Type- Market Insights and Forecast 2022-2032, USD Million

7.2.2.By Application- Market Insights and Forecast 2022-2032, USD Million

7.2.3.By End User- Market Insights and Forecast 2022-2032, USD Million

8. Competitive Outlook

8.1. Company Profiles

8.1.1.Flowserve Corporation

8.1.1.1. Business Description

8.1.1.2. Product Portfolio

8.1.1.3. Collaborations & Alliances

8.1.1.4. Recent Developments

8.1.1.5. Financial Details

8.1.1.6. Others

8.1.2.Ebara Corporation

8.1.2.1. Business Description

8.1.2.2. Product Portfolio

8.1.2.3. Collaborations & Alliances

8.1.2.4. Recent Developments

8.1.2.5. Financial Details

8.1.2.6. Others

8.1.3.WILO SE

8.1.3.1. Business Description

8.1.3.2. Product Portfolio

8.1.3.3. Collaborations & Alliances

8.1.3.4. Recent Developments

8.1.3.5. Financial Details

8.1.3.6. Others

8.1.4.Sulzer Limited

8.1.4.1. Business Description

8.1.4.2. Product Portfolio

8.1.4.3. Collaborations & Alliances

8.1.4.4. Recent Developments

8.1.4.5. Financial Details

8.1.4.6. Others

8.1.5.Grundfos Holding A/S

8.1.5.1. Business Description

8.1.5.2. Product Portfolio

8.1.5.3. Collaborations & Alliances

8.1.5.4. Recent Developments

8.1.5.5. Financial Details

8.1.5.6. Others

8.1.6.Xylem Inc.

8.1.6.1. Business Description

8.1.6.2. Product Portfolio

8.1.6.3. Collaborations & Alliances

8.1.6.4. Recent Developments

8.1.6.5. Financial Details

8.1.6.6. Others

8.1.7.KSB SE & Co. KGaA

8.1.7.1. Business Description

8.1.7.2. Product Portfolio

8.1.7.3. Collaborations & Alliances

8.1.7.4. Recent Developments

8.1.7.5. Financial Details

8.1.7.6. Others

8.1.8.Kirloskar Brothers Limited (KBL)

8.1.8.1. Business Description

8.1.8.2. Product Portfolio

8.1.8.3. Collaborations & Alliances

8.1.8.4. Recent Developments

8.1.8.5. Financial Details

8.1.8.6. Others

8.1.9.Franklin Electric

8.1.9.1. Business Description

8.1.9.2. Product Portfolio

8.1.9.3. Collaborations & Alliances

8.1.9.4. Recent Developments

8.1.9.5. Financial Details

8.1.9.6. Others

8.1.10. Pentair PLC

8.1.10.1. Business Description

8.1.10.2. Product Portfolio

8.1.10.3. Collaborations & Alliances

8.1.10.4. Recent Developments

8.1.10.5. Financial Details

8.1.10.6. Others

9. Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Pump Type |

|

| By Application |

|

| By End User |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.