India Soil Treatment Market Report: Trends, Growth and Forecast (2026-2032)

By Type (Organic Amendments (Animal Manure, Crop Residue, Compost, Sewage Sludge and Biosolids), pH Adjusters and Soil Conditioners (Aglime, Gypsum, Others), Soil Protection Products (Herbicides, Insecticides, Fungicides, Nematicides)), By Technology (Physicochemical Treatment, Biological Treatment, Thermal Treatment), By Application (Soil Fertility Improvement, Soil Remediation, pH Correction, Weed Management, Pest Management, Soil Structure Improvement), By Crop Type (Grains and Cereals, Fruits and Vegetables, Pulses and Oilseeds, Commercial Crops, Turf and Ornamentals), By Region (North, East, West, South) ... Read more

|

Major Players

|

India Soil Treatment Market Statistics and Insights, 2026

- Market Size Statistics

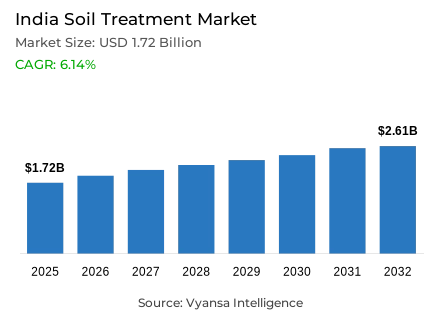

- Soil treatment market size in India was valued at USD 1.72 billion in 2025 and is estimated at USD 1.86 billion in 2026.

- The market size is expected to grow to USD 2.61 billion by 2032.

- Market to register a CAGR of around 6.14% during 2026-32.

- Type Shares

- Organic amendments grabbed market share of 55%.

- Competition

- Soil treatment in India is currently being catered to by more than 10 companies.

- Top 5 companies acquired around 50% of the market share.

- Sumitomo Chemical India Limited, Dhanuka Agritech Limited, Crystal Crop Protection Limited, Coromandel International Limited, UPL Limited etc., are few of the top companies.

- Technology

- Biological treatment grabbed 45% of the market.

India Soil Treatment Market Outlook

The India soil treatment market is valued at USD 1.72 Billion in 2025 and is projected to reach USD 2.61 Billion by 2032, from USD 1.86 Billion in 2026, expanding at a CAGR of 6.14% during 2026-2032. It covers organic amendments, biofertilizers, conditioners, remediation inputs, microbial solutions, and diagnostic-linked nutrient correction for farms, horticulture, cooperatives, and agricultural input distributors. The India soil treatment industry supports yield stability, soil fertility improvement solutions, sustainable agriculture inputs, and measurable soil productivity within the wider crop productivity ecosystem.

Soil health management is gaining procurement priority as nutrient imbalance, low organic carbon, salinity, and pH variability push farmers toward soil testing and nutrient management. Policy-backed Soil Health Card based fertilizer recommendations, organic farming soil inputs, PM-PRANAM soil health initiatives, and integrated nutrient management are shifting demand from generic inputs to targeted treatment packages. This strengthens the India soil treatment market by linking product selection with plot-level diagnostics, crop-specific advisory systems, and regional agronomic correction across major crop clusters and seasons.

Agricultural productivity, input efficiency, and compliance readiness now depend on corrective soil care rather than fertilizer volume alone. The India soil treatment industry benefits as cooperatives, agri-input dealers, and biofertilizer companies position products around micronutrient deficiency correction, soil pH and salinity management, and regenerative agriculture soil health. Stronger demand for organic soil amendments and biofertilizers in India also improves supplier visibility across fragmented rural distribution channels.

The 2026 trajectory points toward broader adoption of sustainable soil treatment solutions, digital soil mapping, and biological inputs. The soil treatment market in India is moving beyond remedial use toward routine fertility planning, supported by state extension networks, testing laboratories, and soil conditioner manufacturers. For suppliers, the India soil treatment industry increasingly rewards field performance, localized formulations, quality certification, and partnerships that convert soil diagnostic data into repeat procurement.

India Soil Treatment Market Growth Driver

Soil Fertility Recovery is Reshaping Input Demand

Soil fertility deterioration is pushing farms and input distributors toward treatment-led nutrient correction rather than blanket fertilizer application. The India soil treatment market gains from this shift as growers seek organic carbon enrichment, microbial inoculants, soil conditioners, and crop-specific amendment programs that improve nutrient uptake efficiency across high-intensity farming belts and commercial horticulture systems. Demand is strongest where intensive cropping has created recurring nutrient gaps, forcing procurement decisions to align with soil diagnostic results and integrated nutrient management.

According to the Ministry of Agriculture and Farmers Welfare, during FY 2025-26 India collected 97.53 lakh soil samples, tested 92.87 lakh samples, and generated 25.79 crore cumulative Soil Health Cards up to February 2026. This scale creates a structured advisory base for soil fertility improvement, allowing the India soil treatment industry to convert diagnostic recommendations at scale into demand for organic amendments, biofertilizers, micronutrient correction products, and field-level treatment services nationwide overall.

India Soil Treatment Market Challenge

Testing Infrastructure Gaps are Slowing Precision Adoption

Testing access and service consistency remain bottlenecks for precision soil correction, especially where farmers need timely sample collection, laboratory turnaround, and advisory translation before sowing windows. The soil treatment market in India faces uneven adoption when recommendations are delayed or when retailers cannot convert test results into suitable product packages. This limits repeat demand for advanced conditioners, microbial blends, and remediation inputs despite rising awareness around soil health management, and weakens confidence in premium treatment programs.

As per the Ministry of Agriculture and Farmers Welfare, 8,272 soil testing laboratories had been established by February 2025, including 1,068 static labs, 163 mobile labs, 6,376 mini labs, and 665 village-level labs. The same update notes logistical, technical, and physical infrastructure barriers in remote and hilly areas, which restrict timely diagnostics, slow product selection, and raise participation costs for smaller suppliers, particularly outside well-served districts and plains during peak seasons.

Unlock Market Intelligence

Explore the market potential with our data-driven report

India Soil Treatment Market Trend

Digital Soil Diagnostics are Moving Toward Field-Level Decisions

Digital fertility mapping is changing treatment planning from district-level guidance to site-specific nutrient management. The India soil treatment market is increasingly shaped by geocoded samples, QR-linked test records, and AI-enabled spatial analysis that improve input precision. This trend supports differentiated formulations because suppliers can target low-organic-carbon soils, salinity stress, micronutrient gaps, and pH correction needs with tighter agronomic positioning, stronger retailer training, and more localized demand forecasting regionally.

Data from the Ministry of Agriculture and Farmers Welfare indicates that soil fertility mapping has been undertaken in 6,954 identified model villages, with completion in 2,023 model villages. This strengthens the India soil treatment industry by improving procurement visibility for soil amendments and biological inputs, while enabling extension agencies and distributors to align inventories with village-level nutrient profiles and crop calendars. It also improves demand planning for state-backed advisory programs and private agronomy services and seasonal crop planning priorities nationally.

India Soil Treatment Market Opportunity

Bio-Input Networks Create Scalable Supplier White Space

Bio-input production networks create scalable white space for manufacturers, rural entrepreneurs, and service-led distributors. The soil treatment market in India can capture stronger adoption by linking microbial soil treatment solutions with farmer training, local preparation units, and assured availability during crop cycles. Localized bio-input access also improves pricing discipline, reduces last-mile dependence on distant suppliers, and supports natural farming clusters seeking biological nitrogen fixation and phosphate-solubilizing microbes, especially where organic-input supply remains inconsistent locally.

Recent data reported by the Press Information Bureau shows that the National Mission on Natural Farming targets 10,000 Bio-input Resource Centres and had deployed more than 70,000 trained Krishi Sakhis by July 2025. This gives the India soil treatment industry a distributed delivery pathway for biofertilizers, compost-based products, microbial inoculants, and advisory-linked procurement, strengthening demand capture in underpenetrated farming clusters and improving supplier access to organized community-level buyers reliably at scale across more villages.

Unlock Market Intelligence

Explore the market potential with our data-driven report

India Soil Treatment Market Segmentation Analysis

By Type

- Organic Amendments

- Animal Manure

- Crop Residue

- Compost

- Sewage Sludge and Biosolids

- pH Adjusters and Soil Conditioners

- Aglime

- Gypsum

- Others

- Soil Protection Products

- Herbicides

- Insecticides

- Fungicides

- Nematicides

Organic amendments hold 55% share by type, supported by their fit with soil organic carbon restoration, compost application, farmyard manure, vermicompost, and crop residue recycling. The India soil treatment market benefits from this segment because organic inputs address fertility, moisture retention, microbial activity, and long-term soil structure together. Their compatibility with organic farming, regenerative agriculture, and integrated nutrient management keeps demand anchored across cereals, horticulture, pulses, and high-value crops, while reducing reliance on single-nutrient correction regularly.

Figures published by the Press Information Bureau show that Paramparagat Krishi Vikas Yojana covered around 15 lakh hectares under organic farming, formed 52,289 clusters, and benefitted 25.30 lakh farmers as of February 2025. This policy-backed organic farming base strengthens demand for organic soil amendments, improves supply planning for producers, and supports wider procurement of compost, manure, green inputs, and certification-linked soil fertility products across organized clusters and supplier channels through farm-level input programs.

By Technology

- Physicochemical Treatment

- Biological Treatment

- Thermal Treatment

Biological treatment holds 45% share by technology, reflecting rising adoption of microbial inoculants, biofertilizers, and soil microbiome restoration practices. The soil treatment market in India is increasingly influenced by biological inputs because they support nutrient solubilization, root-zone activity, and chemical fertilizer reduction without requiring heavy infrastructure at farm level. This technology aligns with low-input farming, sustainable soil treatment, and crop-specific nutrient correction, while offering manufacturers scope for differentiated crop formulations and technical advisory services.

The Ministry of Agriculture and Farmers Welfare reported that ICAR has developed efficient biofertilizer strains for phosphorus solubilization, nitrogen fixation, potassium solubilization, and zinc solubilization, with several commercialized. This expands biological treatment credibility, supports quality-led procurement by agri-input suppliers, and allows manufacturers to differentiate liquid and powdered biofertilizers by crop, soil type, shelf life, and field performance. It also strengthens technology adoption where farmers require measurable nutrient-use efficiency from biological soil fertility improvement across diverse soils.

List of Companies Covered in India Soil Treatment Market

The companies listed below are highly influential in the India soil treatment market, with a significant market share and a strong impact on industry developments.

- Sumitomo Chemical India Limited

- Dhanuka Agritech Limited

- Crystal Crop Protection Limited

- Coromandel International Limited

- UPL Limited

- Bayer CropScience Limited

- Syngenta India Private Limited

- BASF India Limited

- Rallis India Limited

- Godrej Agrovet Limited

Market News & Updates

- Coromandel International Limited, 2026:

Coromandel launched the Gromor Gram initiative across 101 villages in 12 Indian states in March 2026. Each model village provides farmers with soil and leaf testing, crop advisory, demonstration plots, and agri-drone spraying support. The update strengthens diagnostic-linked soil fertility advisory and local agronomy delivery for Indian farmers.

- Rallis India Limited, 2025:

Rallis India launched NuCode in November 2025 as a science-driven soil and plant health brand in India. The platform is built around advanced biological solutions and focuses on biological processes within plants and soil. The update expands Rallis’ soil and plant health portfolio for sustainable, science-led agricultural input programs

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- India Soil Treatment Market Policies, Regulations, and Standards

- India Soil Treatment Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- India Soil Treatment Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Type

- Organic Amendments- Market Insights and Forecast 2022-2032, USD Million

- Animal Manure- Market Insights and Forecast 2022-2032, USD Million

- Crop Residue- Market Insights and Forecast 2022-2032, USD Million

- Compost- Market Insights and Forecast 2022-2032, USD Million

- Sewage Sludge and Biosolids- Market Insights and Forecast 2022-2032, USD Million

- pH Adjusters and Soil Conditioners- Market Insights and Forecast 2022-2032, USD Million

- Aglime- Market Insights and Forecast 2022-2032, USD Million

- Gypsum- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- Soil Protection Products- Market Insights and Forecast 2022-2032, USD Million

- Herbicides- Market Insights and Forecast 2022-2032, USD Million

- Insecticides- Market Insights and Forecast 2022-2032, USD Million

- Fungicides- Market Insights and Forecast 2022-2032, USD Million

- Nematicides- Market Insights and Forecast 2022-2032, USD Million

- Organic Amendments- Market Insights and Forecast 2022-2032, USD Million

- By Technology

- Physicochemical Treatment- Market Insights and Forecast 2022-2032, USD Million

- Biological Treatment- Market Insights and Forecast 2022-2032, USD Million

- Thermal Treatment- Market Insights and Forecast 2022-2032, USD Million

- By Application

- Soil Fertility Improvement- Market Insights and Forecast 2022-2032, USD Million

- Soil Remediation- Market Insights and Forecast 2022-2032, USD Million

- pH Correction- Market Insights and Forecast 2022-2032, USD Million

- Weed Management- Market Insights and Forecast 2022-2032, USD Million

- Pest Management- Market Insights and Forecast 2022-2032, USD Million

- Soil Structure Improvement- Market Insights and Forecast 2022-2032, USD Million

- By Crop Type

- Grains and Cereals- Market Insights and Forecast 2022-2032, USD Million

- Fruits and Vegetables- Market Insights and Forecast 2022-2032, USD Million

- Pulses and Oilseeds- Market Insights and Forecast 2022-2032, USD Million

- Commercial Crops- Market Insights and Forecast 2022-2032, USD Million

- Turf and Ornamentals- Market Insights and Forecast 2022-2032, USD Million

- By Region

- North- Market Insights and Forecast 2022-2032, USD Million

- East- Market Insights and Forecast 2022-2032, USD Million

- West- Market Insights and Forecast 2022-2032, USD Million

- South- Market Insights and Forecast 2022-2032, USD Million

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Type

- Market Size & Growth Outlook

- India Organic Amendments Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Technology- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Crop Type- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- India pH Adjusters and Soil Conditioners Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Technology- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Crop Type- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- India Soil Protection Products Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Technology- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Crop Type- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- Coromandel International Limited

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- UPL Limited

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Bayer CropScience Limited

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Syngenta India Private Limited

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- BASF India Limited

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Sumitomo Chemical India Limited

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Dhanuka Agritech Limited

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Crystal Crop Protection Limited

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Rallis India Limited

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Godrej Agrovet Limited

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Coromandel International Limited

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Type |

|

| By Technology |

|

| By Application |

|

| By Crop Type |

|

| By Region |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.