India Modular Data Centers Market Report: Trends, Growth and Forecast (2026-2032)

By Component (Solutions (All-in-One Modular Data Centers, Prefabricated Module Solutions), Services (Consulting & Design Services, Deployment, Integration & Maintenance Services)), By Form Factor (ISO Container-based Modular Data Centers, Enclosure-based Modular Data Centers, Skid-mounted Modular Data Centers), By Build Type (Semi-Prefabricated Modular Data Centers, Fully Prefabricated Modular Data Centers), By Deployment Type (Indoor Modular Data Centers, Outdoor Modular Data Centers), By Organization Size (Large Enterprises, Small & Medium Enterprises), By End User (Cloud Service Providers, Telecom Service Providers, BFSI, Government & Defense, Healthcare, Retail & E-commerce, Manufacturing, Energy & Utilities, Others), By Capacity (Small Capacity Modular Data Centers, Medium Capacity Modular Data Centers, Large Capacity Modular Data Centers), By Region (North, East, West, South) ... Read more

|

Major Players

|

India Modular Data Centers Market Statistics and Insights, 2026

- Market Size Statistics

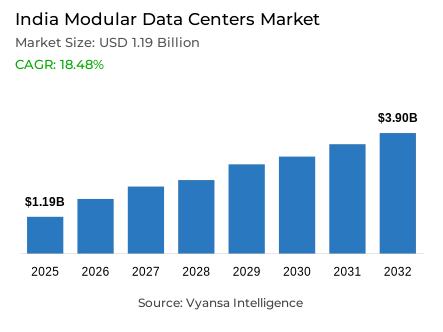

- Modular data centers market size in India was valued at USD 1.19 billion in 2025 and is estimated at USD 1.41 billion in 2026.

- The market size is expected to grow to USD 3.9 billion by 2032.

- Market to register a CAGR of around 18.48% during 2026-32.

- Component Shares

- Solutions grabbed market share of 80%.

- Competition

- More than 10 companies are actively engaged in producing modular data centers in India.

- Top 5 companies acquired around 45% of the market share.

- Delta Electronics, Rittal, Eaton, Schneider Electric, Dell Technologies etc., are few of the top companies.

- End User

- Cloud service providers grabbed 30% of the market.

India Modular Data Centers Market Outlook

The India modular data centerss market was valued at USD 1.19 billion in 2025, establishing a commercially energized and structurally well-supported foundation within one of Asia's most rapidly scaling digital infrastructure ecosystems. Projected to advance from USD 1.41 billion in 2026 to USD 3.90 billion by 2032, the sector registers a compound annual growth rate of 18.48% across the forecast horizon. This near-tripling of market value reflects a structural reorientation in how Indian operators approach digital infrastructure buildout one where speed of deployment, phased scalability, and capital efficiency are systematically displacing conventional long-cycle construction approaches across enterprise, cloud, and AI-linked facility development contexts. Growth is anchored in operational necessity rather than technology novelty, making this one of the most durably positioned expansion categories within India's broader digital infrastructure investment landscape.

The component architecture defining this market's commercial structure is anchored firmly in integrated deployment offerings. Solutions command approximately 80% of total component market share a dominant position reflecting the consistent and growing preference among Indian operators for pre-engineered, standardized infrastructure packages that compress installation timelines, reduce deployment complexity, and support reliable capacity addition across diverse end-use environments. This concentration confirms that buyers are not assembling modular infrastructure from discrete components but investing in complete, outcome-oriented deployment solutions whose practical performance advantages speed, consistency, and operational predictability align directly with the infrastructure planning priorities of India's most digitally active organizations.

The end-user architecture reinforces the primacy of cloud service providers as the category's dominant demand source. Cloud Service Providers command approximately 30% of total end-user market share a leading position reflecting the structural alignment between modular data centers deployment characteristics and the specific infrastructure requirements of cloud operators managing variable, rapidly evolving workload profiles across distributed service networks. India's documented internet subscriber base of 1,002.85 million and broadband subscriber count of 979.71 million as of June 2025 confirmed by TRAI validate the digital consumption scale that is sustaining cloud capacity expansion pressure and making modular deployment formats commercially indispensable to providers seeking agile, cost-controlled infrastructure growth pathways.

The forward outlook through 2032 is defined by four converging structural forces whose combined momentum is creating a modular data centers market of exceptional commercial velocity. India's position as a generator of nearly 20% of the world's data while accounting for just 3% of global data center capacity documented by the Press Information Bureau confirms a structural supply-demand imbalance whose correction requires exactly the rapid, scalable, and cost-efficient deployment characteristics that modular formats deliver. Data center investment announcements of approximately USD 90 billion particularly for AI-linked facilities are creating a facility development pipeline whose commissioning timelines demand deployment flexibility that conventional construction cannot match. The Union Budget 2026-27's proposed tax holiday through 2047 for eligible foreign cloud operators using Indian data center infrastructure further amplifies long-term capacity demand visibility for modular deployment partners positioned within compliant facility ecosystems through 2032.

India Modular Data Centers Market Growth Driver

Expanding Digital Subscriber Base Sustains Continuous Infrastructure Capacity Pressure

The rapid and institutionally documented expansion of India's national digital subscriber base represents the primary structural driver of modular data centers demand functioning as a persistent capacity pressure mechanism that continuously accelerates the infrastructure addition requirements of cloud operators, enterprise IT organizations, and digital service providers whose workload growth trajectories demand deployment solutions capable of delivering new capacity faster than conventional construction timelines allow. As more Indian consumers and enterprises deepen their digital engagement across streaming, e-commerce, financial services, and cloud-based productivity platforms, the volume of compute and storage demand flowing through India's data center infrastructure compounds consistently creating structural urgency around deployment speed and scalability that modular formats are uniquely positioned to address.

The quantitative momentum of this connectivity-driven demand dynamic is documented with precision by TRAI. Total internet subscribers in India reached 1,002.85 million at the end of June 2025, with broadband subscribers standing at 979.71 million establishing a massive and continuously expanding digital consumer base whose sustained engagement generates persistent infrastructure utilization pressure across the facilities serving their connectivity and cloud service requirements. Total wireless data usage reached 65,009 PB during the quarter ended June 2025, while average monthly data consumption per subscriber rose to 24.01 GB confirming the relentless traffic volume intensification that elevates capacity planning urgency and sustains consistent demand for modular deployment formats capable of delivering rapid, scalable infrastructure additions. These connectivity metrics validate a demand expansion dynamic of sufficient scale and continuity to sustain structural modular data centers market growth through 2032.

India Modular Data Centers Market Challenge

Power Availability and Energy Planning Constrain Deployment Velocity

The structural complexity of power availability, energy-intensive scaling requirements, and utility coordination obligations represents the most consequential operational challenge confronting modular data centers deployment across India creating systematic planning, infrastructure readiness, and clean energy access constraints that moderate deployment velocity and introduce execution risk into capacity addition timelines even where commercial demand conditions are favorable. In a deployment environment where modular data centerss' core value proposition is speed and scalability, the bottleneck created by power infrastructure readiness and utility support limitations directly undermines the agility advantages that make modular formats commercially compelling making power planning a defining competitive and operational differentiator among deployment solution providers.

The structural depth and national scale of this power challenge are documented with precision by the Press Information Bureau. India successfully met a peak power demand of 242.49 GW during FY 2025-26 a figure that reflects both the progress of India's power system and the extraordinary scale of the national energy burden within which data center power planning must operate. The Press Information Bureau further documents that India generates nearly 20% of the world's data but accounts for just 3% of global data center capacity a gap whose closure through accelerated deployment will compound power infrastructure demands substantially beyond current utilization levels. The May 2025 NITI Aayog workshop's identification of clean energy access, high-performance computing support, and policy coordination as critical infrastructure development requirements confirms that power-linked planning constraints are recognized at the highest institutional levels as a structural bottleneck requiring coordinated policy and investment responses through 2032.

Unlock Market Intelligence

Explore the market potential with our data-driven report

India Modular Data Centers Market Trend

AI-Ready Hyperscale Buildouts Redefine Modular Deployment Requirements

The accelerating development of AI-linked and cloud-oriented data center infrastructure across India represents the defining structural trend reshaping themodular data centerssmarket fundamentally elevating the technical specifications, density requirements, and operational performance expectations of modular deployment solutions while simultaneously creating a facility development pipeline of unprecedented scale whose commissioning velocity demands exactly the pre-engineered, rapidly deployable infrastructure characteristics that advanced modular formats provide. This trend is moving the competitive conversation in India's modular market beyond standard capacity addition deployments into the domain of high-density AI workload infrastructure where thermal management complexity, power delivery engineering, and structural scalability requirements demand modular solutions designed specifically for next-generation compute environments.

The investment scale and policy endorsement of this AI-ready buildout trend are documented with authority by the Press Information Bureau. Investments of approximately USD 70 billion are already underway in India, with data center announcements particularly for AI data centers reaching approximately USD 90 billion and confirming the structural commitment of global technology operators to India as a primary AI infrastructure deployment geography. The Union Budget 2026-27 framework explicitly positions India among the leading global destinations for AI and cloud infrastructure, describing data centers as critical to the infrastructure layer of AI architecture providing institutional endorsement that is accelerating operator confidence and investment commitment across the modular deployment pipeline. As AI-linked workloads expand and facility density requirements intensify, modular data centers formats are increasingly recognized as the deployment model best aligned with the speed, scalability, and flexibility demands of India's AI infrastructure development agenda through 2032.

India Modular Data Centers Market Opportunity

Policy-Backed Cloud Investment Framework Creates Durable Modular Deployment Demand

The comprehensive policy framework being deployed through the Union Budget 2026-27 to attract foreign cloud operator investment into Indian data center infrastructure creates a structurally significant and commercially durable opportunity for modular data centers solution providers delivering a policy-amplified demand expansion dynamic whose investment scale, long-horizon certainty, and domestic infrastructure procurement requirements generate modular deployment contract opportunities of exceptional commercial value and revenue visibility. This policy opportunity is distinguished by its operational specificity: the requirement that eligible foreign operators procure data center services from Indian infrastructure providers creates a direct and structured link between policy incentive uptake and domestic modular capacity addition demand making policy compliance a commercial demand driver rather than merely a regulatory obligation.

The quantitative scale and structural specificity of this policy opportunity are documented with precision by the Press Information Bureau. The Union Budget 2026-27 proposes a tax holiday through 2047 for eligible foreign companies providing cloud services globally using Indian data center infrastructure a 20-year incentive horizon that creates exceptional long-cycle investment visibility for Indian data center operators and their modular solution ecosystem partners. The eligibility framework's requirement that qualifying foreign companies use India-based data center infrastructure for global operations creates a structural procurement commitment that directly sustains domestic modular capacity addition demand across the incentive period. The proposed 15% safe harbour margin on cost for related-entity arrangements further improves modular deployment contract economics and commercial predictability for solution providers positioned within compliant operator supply chains. modular data centers providers that align their deployment capability, solution portfolio, and compliance infrastructure with this policy framework will capture disproportionate value from India's most structurally guaranteed digital infrastructure growth opportunity through 2032.

Unlock Market Intelligence

Explore the market potential with our data-driven report

India Modular Data Centers Market Segmentation Analysis

By Component

- Solutions

- All-in-One Modular Data Centers

- Prefabricated Module Solutions

- Services

- Consulting & Design Services

- Deployment, Integration & Maintenance Services

The segment with highest market share under the Component is Solutions, accounting for approximately 80% of the total market. This commanding position reflects the deep structural preference among Indian data center operators for integrated deployment packages that combine power, cooling, compute, and connectivity infrastructure within a standardized, pre-engineered format that simplifies procurement, accelerates commissioning, and delivers reliable performance outcomes across diverse facility environments. With four-fifths of total market value concentrated within a single component category, Solutions define the commercial priorities, product development investments, and competitive differentiation frameworks of the India modular data centerss market establishing the deployment efficiency benchmarks and operational consistency standards that all market participants must deliver credibly to compete for high-value infrastructure contracts.

The structural leadership of Solutions is further reinforced by the operational imperatives driving India's data center expansion where AI-linked hyperscale buildouts, cloud capacity additions, and enterprise digital infrastructure modernization programs all share a common requirement for faster, more predictable deployment outcomes than conventional component-assembly approaches can reliably provide. As data center investment announcements of approximately USD 90 billion create a facility development pipeline whose execution velocity demands pre-engineered infrastructure readiness, the commercial case for integrated solutions over fragmented component procurement strengthens commensurately. The segment's structural dominance as the market's primary revenue contributor and competitive innovation focal point is expected to deepen and consolidate through 2032.

By End User

- Cloud Service Providers

- Telecom Service Providers

- BFSI

- Government & Defense

- Healthcare

- Retail & E-commerce

- Manufacturing

- Energy & Utilities

- Others

The segment with highest market share under the End User is Cloud Service Providers, accounting for approximately 30% of the total market. This leading position reflects the structural alignment between cloud operators' infrastructure requirements characterized by variable workload growth, phase-based capacity expansion, and the need for rapid commissioning without compromising operational stability and the specific deployment advantages that modular data centers formats deliver across all three dimensions simultaneously. With nearly one-third of total market value anchored in cloud service provider demand, this end-user segment defines the deployment specification priorities, scalability requirements, and performance expectations that shape product development and commercial strategy across the India modular data centerss market.

The structural leadership of Cloud Service Providers is being actively intensified by the sustained expansion of India's digital consumption base. TRAI's documentation of total wireless data usage reaching 65,009 PB in the quarter ended June 2025 with average per-subscriber monthly consumption rising to 24.01 GB confirms the relentless workload growth that keeps cloud capacity expansion under continuous operational pressure. As cloud operators respond to this demand trajectory by accelerating infrastructure addition cycles, the modular format's ability to deliver faster commissioning, phased capacity scaling, and more controlled deployment economics relative to conventional construction makes it the structurally preferred buildout approach for providers managing India's most demanding digital service growth environments. The segment's commercial leadership is expected to strengthen through 2032.

List of Companies Covered in India Modular Data Centers Market

The companies listed below are highly influential in the India modular data centers market, with a significant market share and a strong impact on industry developments.

- Delta Electronics

- Rittal

- Eaton

- Schneider Electric

- Dell Technologies

- Huawei Technologies

- Vertiv

- Hewlett Packard Enterprise (HPE)

- Legrand

- IBM

Market News & Updates

- Vertiv, 2026:

Vertiv announced its role in NxtGen AI’s national-scale sovereign AI factory in India, where it is supplying the full power and thermal infrastructure, including liquid cooling, modular secondary piping skids, UPS systems, and lithium-ion-based energy storage, for a deployment supporting more than 4,000 NVIDIA Blackwell GPUs. For India’s modular data centers market, this is a highly significant verified development because it demonstrates live deployment of high-density, scalable, and energy-efficient infrastructure in the country, while Vertiv’s stated Make in India supply chain and engineering support also reinforce local execution capability for future modular AI and sovereign cloud builds

- Dell Technologies, 2026:

Dell Technologies announced that NxtGen AI had selected Dell AI Factory with NVIDIA solutions to build India’s first and largest dedicated AI factory, with Dell providing core infrastructure through Dell Integrated Rack Scalable Systems and liquid-cooled PowerEdge XE9685L servers to support a cluster of more than 4,000 NVIDIA Blackwell GPUs. This is especially important for the Indian modular data centers market because it validates rack-scale, pre-integrated AI infrastructure as a practical route to faster deployment in India, strengthens demand for high-density liquid-cooled modular builds, and creates a visible benchmark for how enterprise, startup, and government AI capacity can be provisioned through integrated factory-style data center architecture

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- India Modular Data Centers Market Policies, Regulations, and Standards

- India Modular Data Centers Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- India Modular Data Centers Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Component

- Solutions- Market Insights and Forecast 2022-2032, USD Million

- All-in-One Modular Data Centers- Market Insights and Forecast 2022-2032, USD Million

- Prefabricated Module Solutions- Market Insights and Forecast 2022-2032, USD Million

- Services- Market Insights and Forecast 2022-2032, USD Million

- Consulting & Design Services- Market Insights and Forecast 2022-2032, USD Million

- Deployment, Integration & Maintenance Services- Market Insights and Forecast 2022-2032, USD Million

- Solutions- Market Insights and Forecast 2022-2032, USD Million

- By Form Factor

- ISO Container-based Modular Data Centers- Market Insights and Forecast 2022-2032, USD Million

- Enclosure-based Modular Data Centers- Market Insights and Forecast 2022-2032, USD Million

- Skid-mounted Modular Data Centers- Market Insights and Forecast 2022-2032, USD Million

- By Build Type

- Semi-Prefabricated Modular Data Centers- Market Insights and Forecast 2022-2032, USD Million

- Fully Prefabricated Modular Data Centers- Market Insights and Forecast 2022-2032, USD Million

- By Deployment Type

- Indoor Modular Data Centers- Market Insights and Forecast 2022-2032, USD Million

- Outdoor Modular Data Centers- Market Insights and Forecast 2022-2032, USD Million

- By Organization Size

- Large Enterprises- Market Insights and Forecast 2022-2032, USD Million

- Small & Medium Enterprises- Market Insights and Forecast 2022-2032, USD Million

- By End User

- Cloud Service Providers- Market Insights and Forecast 2022-2032, USD Million

- Telecom Service Providers- Market Insights and Forecast 2022-2032, USD Million

- BFSI- Market Insights and Forecast 2022-2032, USD Million

- Government & Defense- Market Insights and Forecast 2022-2032, USD Million

- Healthcare- Market Insights and Forecast 2022-2032, USD Million

- Retail & E-commerce- Market Insights and Forecast 2022-2032, USD Million

- Manufacturing- Market Insights and Forecast 2022-2032, USD Million

- Energy & Utilities- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By Capacity

- Small Capacity Modular Data Centers- Market Insights and Forecast 2022-2032, USD Million

- Medium Capacity Modular Data Centers- Market Insights and Forecast 2022-2032, USD Million

- Large Capacity Modular Data Centers- Market Insights and Forecast 2022-2032, USD Million

- By Region

- North

- East

- West

- South

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Component

- Market Size & Growth Outlook

- India Solutions Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Form Factor- Market Insights and Forecast 2022-2032, USD Million

- By Build Type- Market Insights and Forecast 2022-2032, USD Million

- By Deployment Type- Market Insights and Forecast 2022-2032, USD Million

- By Organization Size- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- By Capacity- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- India Services Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Form Factor- Market Insights and Forecast 2022-2032, USD Million

- By Build Type- Market Insights and Forecast 2022-2032, USD Million

- By Deployment Type- Market Insights and Forecast 2022-2032, USD Million

- By Organization Size- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- By Capacity- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- Schneider Electric

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Dell Technologies

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Huawei Technologies

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Vertiv

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Hewlett Packard Enterprise (HPE)

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Delta Electronics

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Rittal

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Eaton

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Legrand

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- IBM

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Schneider Electric

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Component |

|

| By Form Factor |

|

| By Build Type |

|

| By Deployment Type |

|

| By Organization Size |

|

| By End User |

|

| By Capacity |

|

| By Region |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.