Global Modular Data Centers Market Report: Trends, Growth and Forecast (2026-2032)

By Component (Solutions (All-in-One Modular Data Centers, Prefabricated Module Solutions), Services (Consulting & Design Services, Deployment, Integration & Maintenance Services)), By Form Factor (ISO Container-based Modular Data Centers, Enclosure-based Modular Data Centers, Skid-mounted Modular Data Centers), By Build Type (Semi-Prefabricated Modular Data Centers, Fully Prefabricated Modular Data Centers), By Deployment Type (Indoor Modular Data Centers, Outdoor Modular Data Centers), By Organization Size (Large Enterprises, Small & Medium Enterprises), By End User (Cloud Service Providers, Telecom Service Providers, BFSI, Government & Defense, Healthcare, Retail & E-commerce, Manufacturing, Energy & Utilities, Others), By Capacity (Small Capacity Modular Data Centers, Medium Capacity Modular Data Centers, Large Capacity Modular Data Centers), By Region (North America, South America, Europe, Middle East & Africa, Asia Pacific) ... Read more

|

Major Players

|

Global Modular Data Centers Market Statistics and Insights, 2026

- Market Size Statistics

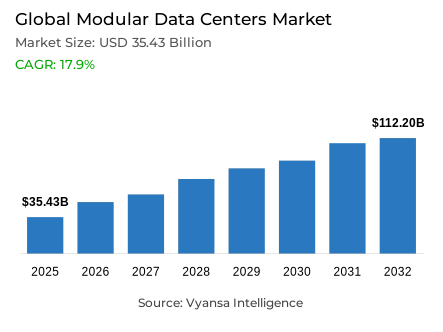

- Modular data centers market size in Global was valued at USD 35.43 billion in 2025 and is estimated at USD 41.79 billion in 2026.

- The market size is expected to grow to USD 112.2 billion by 2032.

- Market to register a CAGR of around 17.9% during 2026-32.

- Component Shares

- Solutions grabbed market share of 80%.

- Competition

- More than 25 companies are actively engaged in producing modular data centers.

- Top 5 companies acquired around 45% of the market share.

- Hewlett Packard Enterprise (HPE), Rittal, IBM, Schneider Electric, Vertiv etc., are few of the top companies.

- End User

- Cloud service providers grabbed 30% of the market.

- Region

- Asia Pacific leads with a 40% share of the global market.

Global Modular Data Centers Market Outlook

The Global modular data centers market was valued at USD 35.43 billion in 2025, establishing a commercially energized and structurally well-supported foundation within the world's most rapidly evolving digital infrastructure investment landscape. Projected to advance from USD 41.79 billion in 2026 to USD 112.20 billion by 2032, the sector registers a compound annual growth rate of 17.9% across the forecast horizon. This near-tripling of market value reflects a structural and irreversible shift in how organizations across every major economy approach digital infrastructure capacity planning one where deployment speed, phased scalability, and operational predictability are systematically displacing conventional long-cycle construction models as the preferred approach to data center buildout across enterprise, cloud, and AI-linked facility development contexts worldwide.

The component architecture defining this market's commercial structure is anchored firmly in integrated deployment offerings. Solutions command approximately 80% of total component market share a dominant position reflecting the consistent and deepening global preference for pre-engineered, standardized infrastructure packages that compress installation timelines, reduce deployment complexity, and deliver reliable operational outcomes across diverse facility environments and geographies. This concentration confirms that buyers worldwide have moved decisively beyond component-level procurement toward outcome-oriented solution investment a behavioral shift whose commercial implications include higher average contract values, stronger provider-operator relationships, and more durable competitive advantages for solution providers with proven deployment track records across multiple market contexts.

The end-user architecture reinforces the structural centrality of cloud infrastructure operators as the category's dominant demand source. Cloud Service Providers command approximately 30% of total end-user market share a leading position that reflects the natural alignment between modular deployment characteristics and the specific infrastructure requirements of cloud operators managing variable, rapidly evolving workload profiles across geographically distributed service networks. ITU's documentation of approximately 6 billion people equivalent to 74% of the world's population using the internet in 2025, alongside mobile broadband traffic reaching an estimated 1.5 zettabytes and fixed broadband traffic advancing to 7.3 zettabytes in the same year, confirms the digital consumption scale that sustains consistent cloud capacity expansion pressure and makes modular deployment formats operationally indispensable to providers seeking agile, cost-controlled infrastructure growth pathways.

The forward outlook through 2032 is defined by four converging structural forces whose combined commercial impact is creating a modular data center market of exceptional and sustained growth velocity. The escalating global data center electricity consumption documented by IEA at approximately 415 terawatt-hours in 2024 and growing at around 12% annually since 2017 creates the infrastructure investment imperative whose execution velocity requirements favor modular deployment formats above all alternatives. The rapid proliferation of AI-linked compute demand evidenced by more than 13% of EU businesses using artificial intelligence in 2024 per Eurostat, up from 8% in 2023 is driving the shift toward higher-density, pre-integrated facility formats that modular solutions are uniquely positioned to deliver. The World Bank's documentation that less than 20% of low- and middle-income countries possess modern data infrastructure creates a globally significant untapped deployment opportunity whose scale and accessibility favor modular modular data centers precisely because of their speed, simplicity, and phased scalability advantages. Asia Pacific's 40% global market share leadership confirms the geographic growth center around which global competitive strategy, product localization investment, and supply chain development are organized.

Global Modular Data Centers Market Growth Driver

Expanding Global Internet Population Sustains Continuous Infrastructure Capacity Pressure

The rapid and institutionally documented expansion of global internet connectivity and digital consumption represents the primary structural driver of modular data center demand functioning as a persistent capacity pressure mechanism that continuously accelerates infrastructure addition requirements across cloud operators, enterprise IT organizations, and digital service providers whose workload growth trajectories demand deployment solutions capable of delivering new capacity faster than conventional construction timelines allow. As more of the world's population transitions from offline to online status and deepens its digital engagement across streaming, e-commerce, financial services, and cloud-based productivity platforms, the volume of compute and storage demand flowing through global data center infrastructure compounds consistently creating structural urgency around deployment speed ad scalability that modular formats are uniquely positioned to address at global scale.

The quantitative momentum of this connectivity-driven demand dynamic is documented with precision by ITU. Approximately 6 billion people equivalent to 74% of the world's population are using the internet in 2025, confirming a massive and continuously expanding digital consumer base whose sustained engagement generates persistent infrastructure utilization pressure across the facilities serving their connectivity and cloud service requirements. Mobile broadband traffic is estimated at 1.5 zettabytes in 2025, while fixed broadband traffic reaches 7.3 zettabytes up from 6.2 zettabytes the previous year confirming the relentless traffic volume intensification that elevates capacity planning urgency and sustains consistent demand for modular deployment formats capable of delivering rapid, scalable infrastructure additions. These connectivity metrics validate a demand expansion dynamic of sufficient global scale and continuity to sustain structural modular data center market growth.

Global Modular Data Centers Market Challenge

Energy Consumption and Sustainability Pressures Tighten Deployment Decisions

The rapidly escalating energy consumption and sustainability compliance obligations surrounding global data center operations represent the most consequential structural challenge confronting modular data center solution providers creating systematic site planning, environmental approval, and operating cost management burdens that moderate deployment velocity and introduce execution complexity into capacity addition timelines even where commercial demand conditions are strongly favorable. In a deployment environment where modular data centers' core value proposition is speed and scalability, the bottleneck created by energy planning requirements, carbon footprint obligations, and water and land resource constraints directly complicates the agility advantages that make modular formats commercially compelling making sustainability engineering capability an increasingly decisive competitive differentiator among global solution providers.

The quantitative scale and structural depth of this energy and sustainability challenge are documented with precision by the IEA and the World Bank. Data centers accounted for approximately 1.5% of the world's electricity consumption in 2024 equivalent to around 415 terawatt-hours with their electricity use growing at approximately 12% annually since 2017, confirming a consumption escalation trajectory whose environmental impact implications are attracting progressively more stringent regulatory and stakeholder scrutiny across major deployment markets. The World Bank further documents that the growing digital sector contributes between 1.5% and 4% of global carbon emissions, while data centers require substantial amounts of water and land that can strain local resource availability creating multi-dimensional sustainability obligations that compound site selection complexity, raise approval timelines, and elevate operating cost management requirements for modular deployment projects. Solution providers that embed sustainability engineering as a core design discipline rather than a compliance afterthought will navigate this challenge with competitive advantage through 2032.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Global Modular Data Centers Market Trend

AI-Ready Infrastructure Demand Reshapes Global Deployment Specification Standards

The accelerating global proliferation of artificial intelligence applications across enterprise, government, and hyperscale computing environments represents the defining structural trend reshaping modular data center design priorities, engineering investment, and competitive differentiation worldwide. This AI adoption wave is fundamentally elevating the technical specifications, density requirements, and thermal management engineering standards of modular deployment solutions while simultaneously creating a facility development pipeline of unprecedented scale and urgency whose commissioning velocity demands exactly the pre-engineered, rapidly deployable infrastructure characteristics that advanced modular formats provide. The trend is moving the competitive conversation in the global modular market decisively beyond standard capacity addition deployments into the domain of high-density AI workload infrastructure whose operational requirements are redefining deployment solution specifications at a structural level.

The institutional scale and commercial specificity of this AI-driven infrastructure trend are documented with authority across multiple official sources. The European Commission confirms that 13 AI Factories are already being deployed around Europe's supercomputers in 2025 demonstrating that specialized, high-density compute environments requiring scalable and pre-integrated infrastructure formats have advanced from strategic planning into active deployment across major digital economies. Eurostat further documents that more than 13% of EU businesses used artificial intelligence in 2024, up sharply from 8% in 2023 confirming the enterprise-level AI adoption momentum that is translating directly into data center infrastructure capacity demand across commercial, industrial, and public sector computing environments. As AI workload density requirements intensify and deployment timelines compress, modular data center formats are increasingly recognized as the infrastructure model best aligned with the speed, scalability, and standardization demands of the global AI infrastructure development agenda through 2032.

Global Modular Data Centers Market Opportunity

Underserved Digital Economies Create a Globally Significant Untapped Deployment Frontier

The large and structurally underserved digital infrastructure base across low- and middle-income economies where rising demand for data processing, cloud access, and digital service delivery is confronting a critical shortage of modern data center capacity represents the global modular data centers market's most commercially significant long-term growth opportunity. This emerging market deployment frontier is distinguished from mature market replacement demand by its scale, geographic breadth, and the structural advantage that modular formats hold in exactly the deployment contexts faster installation, lower construction complexity, reduced infrastructure dependency, and phased scalability that characterize infrastructure development in markets where conventional long-cycle data center construction is impractical or commercially unviable.

The quantitative scale and accessibility of this emerging market opportunity are documented with precision by the World Bank. Less than 20% of low- and middle-income countries currently possess modern data infrastructure confirming a structural supply gap of global geographic breadth whose commercial closure requires the rapid deployment, simplified installation, and phased expansion characteristics that modular data center formats deliver as inherent design advantages. The World Bank further documents that low-income countries have zero cloud on-ramps, while cloud resources are progressively moving closer to the edge to improve performance confirming that the infrastructure deficit in these markets extends beyond raw capacity into the connectivity and cloud access architecture that modular edge deployments are specifically positioned to provide. Solution providers that develop modular infrastructure packages engineered specifically for emerging market deployment contexts combining lower infrastructure dependency, simplified installation requirements, and accessible cost structures will capture disproportionate value from this structurally significant and geographically expansive growth opportunity through 2032.

Global Modular Data Centers Market Regional Analysis

By Region

- North America

- South America

- Europe

- Middle East & Africa

- Asia Pacific

The segment with highest market share under the Region is Asia Pacific, accounting for approximately 40% of the total market. This dominant position reflects the convergence of the world's largest and most rapidly expanding digital consumer base, the highest concentration of cloud infrastructure investment momentum, the most advanced 5G deployment trajectory across key economies, and a manufacturing and technology ecosystem that simultaneously drives product innovation velocity and sustains cost competitiveness across all modular deployment price tiers. With two-fifths of total global market value concentrated within a single regional block, Asia Pacific defines the commercial scale, competitive intensity, and growth trajectory parameters of the global modular data centers market making it the organizing geography around which all competitive strategy, supply chain development, and market entry prioritization decisions are structured.

The structural dominance of Asia Pacific is sustained by demand characteristics operating simultaneously across multiple commercial dimensions active large-format hyperscale capacity additions among established cloud operators in China, Japan, South Korea, and Australia; rapid first-time infrastructure development momentum across high-growth emerging geographies including India, Southeast Asia, and South Asia; and a manufacturing ecosystem generating continuous product innovation at progressively accessible deployment cost points. India's documented position as a generator of nearly 20% of the world's data while accounting for just 3% of global data center capacity confirms the structural supply-demand imbalance whose correction requires the rapid, scalable, and cost-efficient deployment characteristics that modular formats uniquely deliver. Asia Pacific's structural leadership as the global market's dominant demand anchor and highest-volume growth contributor is expected to deepen through 2032.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Global Modular Data Centers Market Segmentation Analysis

By Component

- Solutions

- All-in-One Modular Data Centers

- Prefabricated Module Solutions

- Services

- Consulting & Design Services

- Deployment, Integration & Maintenance Services

The segment with highest market share under the Component is Solutions, accounting for approximately 80% of the total market. This commanding position reflects the deep and structurally embedded preference among global data center operators for integrated deployment packages that combine power, cooling, compute, and connectivity infrastructure within a standardized, pre-engineered format that simplifies procurement decisions, accelerates commissioning timelines, and delivers consistent performance outcomes across both large-format hyperscale and distributed edge facility environments worldwide. With four-fifths of total market value concentrated within a single component category, Solutions define the commercial priorities, product development investments, and competitive differentiation frameworks of the global modular data centers market establishing the deployment efficiency benchmarks and operational consistency standards that all market participants must credibly deliver to compete for high-value infrastructure contracts across every major geography.

The structural leadership of Solutions is being actively reinforced by the operational imperatives driving global data center expansion. As AI-linked hyperscale buildouts, cloud capacity additions, and enterprise digital modernization programs converge on shared requirements for faster and more predictable deployment outcomes, the commercial case for integrated solutions over fragmented component procurement strengthens commensurately with the scale and urgency of capacity requirements. The European Commission's documentation of 13 AI Factories being deployed around Europe's supercomputers in 2025 confirms that specialized, high-density compute environments requiring scalable and pre-integrated infrastructure formats are advancing from pilot programs into mainstream deployment activity across major digital economies. The segment's structural dominance as the market's primary revenue contributor and competitive innovation focal point is expected to deepen and consolidate through 2032.

By End User

- Cloud Service Providers

- Telecom Service Providers

- BFSI

- Government & Defense

- Healthcare

- Retail & E-commerce

- Manufacturing

- Energy & Utilities

- Others

The segment with highest market share under the End User is Cloud Service Providers, accounting for approximately 30% of the total market. This leading position reflects the structural alignment between cloud operators' infrastructure requirements characterized by rapid workload growth, phase-based capacity expansion needs, and the imperative for consistent deployment outcomes across geographically distributed service networks and the specific operational advantages that modular data center formats deliver across all three dimensions simultaneously. With nearly one-third of total market value anchored in cloud service provider demand, this end-user segment defines the deployment specification priorities, scalability performance requirements, and speed-of-commissioning expectations that shape product development and commercial strategy across the global modular data centers market.

The structural leadership of Cloud Service Providers is being actively intensified by the sustained escalation of digital consumption across both mature and emerging global markets. ITU's documentation of mobile broadband traffic reaching an estimated 1.5 zettabytes in 2025 and fixed broadband traffic advancing to 7.3 zettabytes up from 6.2 zettabytes the previous year confirms the relentless traffic volume intensification that keeps cloud capacity expansion under continuous operational pressure. As cloud operators respond to this demand trajectory by accelerating infrastructure addition cycles across multiple geographies simultaneously, the modular format's ability to deliver faster commissioning, phased capacity scaling, and cost-controlled deployment economics makes it the structurally preferred buildout approach for providers managing the world's most demanding digital service growth environments. The segment's commercial leadership is expected to strengthen through 2032.

Market Players in Global Modular Data Centers Market

These market players maintain a significant presence in the Global modular data centers market sector and contribute to its ongoing evolution.

- Hewlett Packard Enterprise (HPE)

- Rittal

- IBM

- Schneider Electric

- Vertiv

- Dell Technologies

- Huawei Technologies

- Eaton

- Cannon Technologies

- IE Corp.

- PCX Holding

- Delta Electronics

- Cisco Systems

- STULZ

- BladeRoom Group

Market News & Updates

- Schneider Electric, 2025:

Schneider Electric launched new AI-oriented data center infrastructure that is highly relevant to the modular data centers market, including its Prefabricated Modular EcoStruxure Pod Data Center and new EcoStruxure Rack Solutions; the company said the pod architecture is prefabricated and scalable, supports liquid cooling, power busway, complex cabling, hot-aisle containment, InRow and rear-door heat exchanger cooling architectures, and is designed for high-density deployments of up to 1 MW and beyond. For the global modular data centers market, this is significant because it strengthens Schneider Electric’s position in fully integrated, factory-oriented white-space infrastructure and gives hyperscalers, colocation operators, and enterprise buyers a faster-deploying path to AI-ready modular capacity

- Vertiv, 2025:

Vertiv announced the global availability of Vertiv OneCore, a scalable prefabricated infrastructure platform for AI, HPC, and other high-density 5+ MW data center deployments; the company said the offer integrates power, thermal, and IT infrastructure into a single factory-assembled system and uses prefabricated building blocks, including whitespace fit-outs such as Vertiv SmartRun, within a Vertiv-provided steel shell. This is one of the strongest verified developments in the global modular data centers market because it directly addresses the core buyer needs of the segment—compressed build timelines, reduced on-site complexity, single-point project execution, and scalable deployment across enterprise, colocation, sovereign, and neocloud environments

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- Global Modular Data Centers Market Policies, Regulations, and Standards

- Global Modular Data Centers Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- Global Modular Data Centers Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Component

- Solutions- Market Insights and Forecast 2022-2032, USD Million

- All-in-One Modular Data Centers- Market Insights and Forecast 2022-2032, USD Million

- Prefabricated Module Solutions- Market Insights and Forecast 2022-2032, USD Million

- Services- Market Insights and Forecast 2022-2032, USD Million

- Consulting & Design Services- Market Insights and Forecast 2022-2032, USD Million

- Deployment, Integration & Maintenance Services- Market Insights and Forecast 2022-2032, USD Million

- Solutions- Market Insights and Forecast 2022-2032, USD Million

- By Form Factor

- ISO Container-based Modular Data Centers- Market Insights and Forecast 2022-2032, USD Million

- Enclosure-based Modular Data Centers- Market Insights and Forecast 2022-2032, USD Million

- Skid-mounted Modular Data Centers- Market Insights and Forecast 2022-2032, USD Million

- By Build Type

- Semi-Prefabricated Modular Data Centers- Market Insights and Forecast 2022-2032, USD Million

- Fully Prefabricated Modular Data Centers- Market Insights and Forecast 2022-2032, USD Million

- By Deployment Type

- Indoor Modular Data Centers- Market Insights and Forecast 2022-2032, USD Million

- Outdoor Modular Data Centers- Market Insights and Forecast 2022-2032, USD Million

- By Organization Size

- Large Enterprises- Market Insights and Forecast 2022-2032, USD Million

- Small & Medium Enterprises- Market Insights and Forecast 2022-2032, USD Million

- By End User

- Cloud Service Providers- Market Insights and Forecast 2022-2032, USD Million

- Telecom Service Providers- Market Insights and Forecast 2022-2032, USD Million

- BFSI- Market Insights and Forecast 2022-2032, USD Million

- Government & Defense- Market Insights and Forecast 2022-2032, USD Million

- Healthcare- Market Insights and Forecast 2022-2032, USD Million

- Retail & E-commerce- Market Insights and Forecast 2022-2032, USD Million

- Manufacturing- Market Insights and Forecast 2022-2032, USD Million

- Energy & Utilities- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By Capacity

- Small Capacity Modular Data Centers- Market Insights and Forecast 2022-2032, USD Million

- Medium Capacity Modular Data Centers- Market Insights and Forecast 2022-2032, USD Million

- Large Capacity Modular Data Centers- Market Insights and Forecast 2022-2032, USD Million

- By Region

- North America

- South America

- Europe

- Middle East & Africa

- Asia Pacific

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Component

- Market Size & Growth Outlook

- North America Modular Data Centers Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Component- Market Insights and Forecast 2022-2032, USD Million

- By Form Factor- Market Insights and Forecast 2022-2032, USD Million

- By Build Type- Market Insights and Forecast 2022-2032, USD Million

- By Deployment Type- Market Insights and Forecast 2022-2032, USD Million

- By Organization Size- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- By Capacity- Market Insights and Forecast 2022-2032, USD Million

- By Country

- US

- Canada

- Mexico

- Rest of North America

- US Modular Data Centers Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Component- Market Insights and Forecast 2022-2032, USD Million

- By Form Factor- Market Insights and Forecast 2022-2032, USD Million

- By Build Type- Market Insights and Forecast 2022-2032, USD Million

- By Deployment Type- Market Insights and Forecast 2022-2032, USD Million

- By Organization Size- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- By Capacity- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Canada Modular Data Centers Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Component- Market Insights and Forecast 2022-2032, USD Million

- By Form Factor- Market Insights and Forecast 2022-2032, USD Million

- By Build Type- Market Insights and Forecast 2022-2032, USD Million

- By Deployment Type- Market Insights and Forecast 2022-2032, USD Million

- By Organization Size- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- By Capacity- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Mexico Modular Data Centers Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Component- Market Insights and Forecast 2022-2032, USD Million

- By Form Factor- Market Insights and Forecast 2022-2032, USD Million

- By Build Type- Market Insights and Forecast 2022-2032, USD Million

- By Deployment Type- Market Insights and Forecast 2022-2032, USD Million

- By Organization Size- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- By Capacity- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Market Size & Growth Outlook

- South America Modular Data Centers Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Component- Market Insights and Forecast 2022-2032, USD Million

- By Form Factor- Market Insights and Forecast 2022-2032, USD Million

- By Build Type- Market Insights and Forecast 2022-2032, USD Million

- By Deployment Type- Market Insights and Forecast 2022-2032, USD Million

- By Organization Size- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- By Capacity- Market Insights and Forecast 2022-2032, USD Million

- By Country

- Brazil

- Chile

- Argentina

- Rest of South America

- Brazil Modular Data Centers Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Component- Market Insights and Forecast 2022-2032, USD Million

- By Form Factor- Market Insights and Forecast 2022-2032, USD Million

- By Build Type- Market Insights and Forecast 2022-2032, USD Million

- By Deployment Type- Market Insights and Forecast 2022-2032, USD Million

- By Organization Size- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- By Capacity- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Chile Modular Data Centers Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Component- Market Insights and Forecast 2022-2032, USD Million

- By Form Factor- Market Insights and Forecast 2022-2032, USD Million

- By Build Type- Market Insights and Forecast 2022-2032, USD Million

- By Deployment Type- Market Insights and Forecast 2022-2032, USD Million

- By Organization Size- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- By Capacity- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Argentina Modular Data Centers Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Component- Market Insights and Forecast 2022-2032, USD Million

- By Form Factor- Market Insights and Forecast 2022-2032, USD Million

- By Build Type- Market Insights and Forecast 2022-2032, USD Million

- By Deployment Type- Market Insights and Forecast 2022-2032, USD Million

- By Organization Size- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- By Capacity- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Market Size & Growth Outlook

- Europe Modular Data Centers Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Component- Market Insights and Forecast 2022-2032, USD Million

- By Form Factor- Market Insights and Forecast 2022-2032, USD Million

- By Build Type- Market Insights and Forecast 2022-2032, USD Million

- By Deployment Type- Market Insights and Forecast 2022-2032, USD Million

- By Organization Size- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- By Capacity- Market Insights and Forecast 2022-2032, USD Million

- By Country

- U.K.

- Germany

- France

- Rest of Europe

- U.K. Modular Data Centers Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Component- Market Insights and Forecast 2022-2032, USD Million

- By Form Factor- Market Insights and Forecast 2022-2032, USD Million

- By Build Type- Market Insights and Forecast 2022-2032, USD Million

- By Deployment Type- Market Insights and Forecast 2022-2032, USD Million

- By Organization Size- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- By Capacity- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Germany Modular Data Centers Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Component- Market Insights and Forecast 2022-2032, USD Million

- By Form Factor- Market Insights and Forecast 2022-2032, USD Million

- By Build Type- Market Insights and Forecast 2022-2032, USD Million

- By Deployment Type- Market Insights and Forecast 2022-2032, USD Million

- By Organization Size- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- By Capacity- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- France Modular Data Centers Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Component- Market Insights and Forecast 2022-2032, USD Million

- By Form Factor- Market Insights and Forecast 2022-2032, USD Million

- By Build Type- Market Insights and Forecast 2022-2032, USD Million

- By Deployment Type- Market Insights and Forecast 2022-2032, USD Million

- By Organization Size- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- By Capacity- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Market Size & Growth Outlook

- Middle East & Africa Modular Data Centers Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Component- Market Insights and Forecast 2022-2032, USD Million

- By Form Factor- Market Insights and Forecast 2022-2032, USD Million

- By Build Type- Market Insights and Forecast 2022-2032, USD Million

- By Deployment Type- Market Insights and Forecast 2022-2032, USD Million

- By Organization Size- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- By Capacity- Market Insights and Forecast 2022-2032, USD Million

- By Country

- UAE

- Saudi Arabia

- South Africa

- Rest of Middle East & Africa

- UAE Modular Data Centers Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Component- Market Insights and Forecast 2022-2032, USD Million

- By Form Factor- Market Insights and Forecast 2022-2032, USD Million

- By Build Type- Market Insights and Forecast 2022-2032, USD Million

- By Deployment Type- Market Insights and Forecast 2022-2032, USD Million

- By Organization Size- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- By Capacity- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Saudi Arabia Modular Data Centers Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Component- Market Insights and Forecast 2022-2032, USD Million

- By Form Factor- Market Insights and Forecast 2022-2032, USD Million

- By Build Type- Market Insights and Forecast 2022-2032, USD Million

- By Deployment Type- Market Insights and Forecast 2022-2032, USD Million

- By Organization Size- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- By Capacity- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- South Africa Modular Data Centers Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Component- Market Insights and Forecast 2022-2032, USD Million

- By Form Factor- Market Insights and Forecast 2022-2032, USD Million

- By Build Type- Market Insights and Forecast 2022-2032, USD Million

- By Deployment Type- Market Insights and Forecast 2022-2032, USD Million

- By Organization Size- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- By Capacity- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Market Size & Growth Outlook

- Asia Pacific Modular Data Centers Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Component- Market Insights and Forecast 2022-2032, USD Million

- By Form Factor- Market Insights and Forecast 2022-2032, USD Million

- By Build Type- Market Insights and Forecast 2022-2032, USD Million

- By Deployment Type- Market Insights and Forecast 2022-2032, USD Million

- By Organization Size- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- By Capacity- Market Insights and Forecast 2022-2032, USD Million

- By Country

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- China Modular Data Centers Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Component- Market Insights and Forecast 2022-2032, USD Million

- By Form Factor- Market Insights and Forecast 2022-2032, USD Million

- By Build Type- Market Insights and Forecast 2022-2032, USD Million

- By Deployment Type- Market Insights and Forecast 2022-2032, USD Million

- By Organization Size- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- By Capacity- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Japan Modular Data Centers Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Component- Market Insights and Forecast 2022-2032, USD Million

- By Form Factor- Market Insights and Forecast 2022-2032, USD Million

- By Build Type- Market Insights and Forecast 2022-2032, USD Million

- By Deployment Type- Market Insights and Forecast 2022-2032, USD Million

- By Organization Size- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- By Capacity- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- India Modular Data Centers Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Component- Market Insights and Forecast 2022-2032, USD Million

- By Form Factor- Market Insights and Forecast 2022-2032, USD Million

- By Build Type- Market Insights and Forecast 2022-2032, USD Million

- By Deployment Type- Market Insights and Forecast 2022-2032, USD Million

- By Organization Size- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- By Capacity- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- South Korea Modular Data Centers Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Component- Market Insights and Forecast 2022-2032, USD Million

- By Form Factor- Market Insights and Forecast 2022-2032, USD Million

- By Build Type- Market Insights and Forecast 2022-2032, USD Million

- By Deployment Type- Market Insights and Forecast 2022-2032, USD Million

- By Organization Size- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- By Capacity- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Australia Modular Data Centers Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Component- Market Insights and Forecast 2022-2032, USD Million

- By Form Factor- Market Insights and Forecast 2022-2032, USD Million

- By Build Type- Market Insights and Forecast 2022-2032, USD Million

- By Deployment Type- Market Insights and Forecast 2022-2032, USD Million

- By Organization Size- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- By Capacity- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- Schneider Electric

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Vertiv

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Dell Technologies

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Huawei Technologies

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Eaton

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Hewlett Packard Enterprise (HPE)

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Rittal

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- IBM

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Cannon Technologies

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- IE Corp.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- PCX Holding

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Delta Electronics

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Cisco Systems

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- STULZ

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- BladeRoom Group

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Schneider Electric

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Component |

|

| By Form Factor |

|

| By Build Type |

|

| By Deployment Type |

|

| By Organization Size |

|

| By End User |

|

| By Capacity |

|

| By Region |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.