India Leisure & Business Travel Booking Market Report: Trends, Growth and Forecast (2026-2032)

By Travel Sales Type (Leisure Travel, Business Travel), By Booking Channel (Offline Booking, Online Booking), By Booking Method (Travel Intermediaries, Direct Suppliers) ... Read more

|

Major Players

|

India Leisure & Business Travel Booking Market Statistics and Insights, 2026

- Market Size Statistics

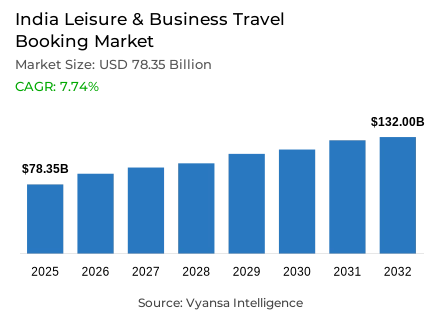

- India Leisure & Business Travel Booking in is estimated at $ 78.35 Billion.

- The market size is expected to grow to $ 132 Billion by 2032.

- Market to register a CAGR of around 7.74% during 2026-32.

- Travel Sales Type Shares

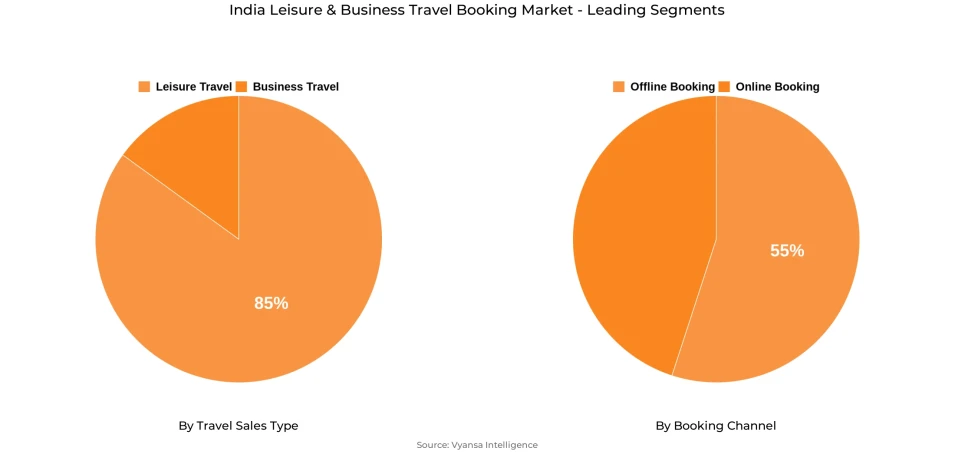

- India Leisure Travel grabbed market share of 85%.

- Competition

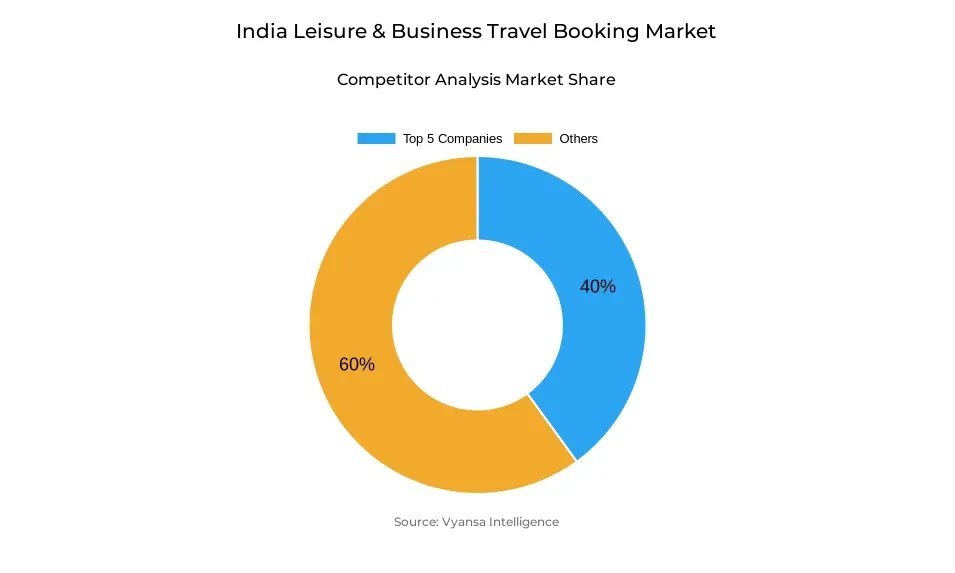

- India Leisure & Business Travel Booking Market is currently being catered to by more than 10 companies.

- Top 5 companies acquired 40% of the market share.

- Le Travenues Technology Ltd, Expedia India (P) Ltd, Booking Holdings Inc, Indian Railway Catering & Tourism Corp Ltd, MakeMyTrip India Pvt Ltd etc., are few of the top companies.

- Booking Channel

- Offline Booking grabbed 55% of the market.

India Leisure & Business Travel Booking Market Outlook

The India leisure and business travel booking market is worth $78.35 billion in 2025 and is expected to reach $132 billion by 2032, driven by the high growth towards online intermediaries and changing end user behavior. Though offline bookings continue to represent 55% of the market, online travel websites are taking share as they improve accessibility, add regional language support, offer convenience, and provide value-added benefits like price lock-ins, pay-later features, and card-based offers. Budget-conscious travellers, driven by rising food inflation, are looking for competitive rates even more, further speeding up the use of online channels.

Offline intermediaries still maintain a significant position, especially for bespoke services, complicated routes, and relationship-based bookings. Their capacity to handle individual end users' requirements, such as customized suggestions, one-to-one interaction, and cash payments, confirms their position, especially among older populations and those with lower digital literacies. All these play a role in maintaining a stable proportion of offline bookings in the market.

Online intermediaries are concentrating on increasing their lodging offerings to tap underpenetrated segments. Although upper-tier hotels already experience considerable online adoption, lower-tier and budget hotels remain dependent on offline channels, hence a white space for expansion. Also, business travels booking for conferences and events are being targeted by online platforms more and more, providing specialized solutions to take a pie in this segment.

The expansion of online travel booking is also underpinned by rising smartphone and internet penetration, digital media impact on itinerary decision-making, and the growing need for experiential and personal travel experiences. Online aggregators' inclusion of AI and bespoke travel tools is likely to augment end-to-end trip planning, covering accommodations, transport, food, and activities, to fuel robust long-term growth in India Leisure & Business Travel Booking Market.

India Leisure & Business Travel Booking Market Growth Driver

Cost-Effectiveness and Price Comparison through Online Intermediaries

India Leisure & Business Travel Booking Market scenario is experiencing greater online channel penetration, with online intermediaries growing at a faster pace than direct providers like airlines and hotels. Online intermediaries are more convenient and accessible with better interfaces in local regional languages, reducing the complexity associated with direct channels. Additional features like a broader range of choices, price fixing, pay later offers, and other card-based offers are inducing more and more customers to move towards online intermediaries, particularly for air and accommodation reservations.

Concurrently, India end users are experiencing increased food inflation, compelling them to opt for cheaper travel arrangements. The belief that improved prices can be obtained by using online intermediaries, as well as the facility of cross-comparison of travel components, is encouraging travellers to increasingly opt for these sites. This is fueling the increasing significance of online intermediaries in leisure and business travel reservations.

India Leisure & Business Travel Booking Market Trend

Increasing Demand for Immersive and Personalised Travel Experience

India online travel intermediaries (OTAs) are experiencing robust growth as increasing end users depend on smartphones, internet connectivity, and online reviews to plan their travel. The convenience of being able to access travel information online is enabling digital channels to take share away from offline channels, with reviews and ratings further contributing to trust and adoption. This trend is transforming the way end users plan and book travel, generating momentum for sustainable growth over the long term through online channels.

Recreation vacation planning, particularly by younger age groups, is increasingly impacted by online media, which translates to increased demand for experiential and immersive travel. Travelers now go beyond hotels and airlines, opting for customized tours like wellness retreats, adventure holidays, and end-to-end packages encompassing all aspects of travel. With increasing consciousness of generative AI and its adoption by global players, the possibility of highly personalised and seamless booking experiences is turning into a trend marker in India Leisure & Business Travel Booking Market.

Unlock Market Intelligence

Explore the market potential with our data-driven report

India Leisure & Business Travel Booking Market Opportunity

Growth in the Underpenetrated Online Lodging Segment

India online travel agencies are growing at a quicker rate than offline players as they are more selectively developing their accommodation portfolios. Even as luxury and high-end hotels already enjoy a considerable portion of online reservations, budget and unrated hotels still use predominantly offline channels. This disparity offers digital platforms an opportunity to attract more bookings in the accommodation segment by reaching out to these segments.

Conference and event business travel bookings are still dominated by offline intermediaries, but online platforms are now adapting solutions to address this segment. While a large percentage of hotel and alternative stay lodging bookings remain offline, there is substantial white space for online intermediaries to expand. Increased end user demand for highly rated accommodations further validates the potential for digital platforms to reach deeper into this underpenetrated lodging segment.

Unlock Market Intelligence

Explore the market potential with our data-driven report

India Leisure & Business Travel Booking Market Segmentation Analysis

By Travel Sales Type

- Leisure Travel

- Business Travel

The segment with the highest market share under Leisure Travel is Travel Sales with 85% market share. Leisure travel remains the largest in India as end users increasingly use online and offline intermediaries to book their vacation holidays. Internet channels have become significant with the improvement in accessibility, regional language facilitation, and features like price lock-in plans and payment convenience. All these have motivated customers to opt for web-based channels for booking airfares, hotels, and other components of vacation travel.

Meanwhile, offline intermediaries continue to have a role, particularly for those travelers who value customized advice and human contact. Their ability to handle complicated itineraries and serve groups with low digital savvy has made them a continued presence. All combined, these forces bring out the preeminence of leisure travel as the dominant driver of India's booking market, commanding the majority of travel transactions with a blend of online convenience and offline credibility.

By Booking Channel

- Offline Booking

- Online Booking

The segment with the largest market share under the Booking Channel is Offline Booking, which accounted for 55% of the market. Offline travel intermediaries in India still retain a large proportion of value sales in 2024 owing to the high trust and personalisation they offer. With their capacity to engage one-on-one with end users, they can personalise travel suggestions based on individual budgets, preferences, and specific requirements, which makes them particularly pertinent for complicated itineraries.

Also, proximity to domestic travelers makes them more familiar and trustworthy, which boosts the confidence of end users. Offline intermediaries are favored by most older age segments and those with low digital literacy due to the possibility of payment in cash and human advice. All these reasons have kept offline booking in vogue and have made it the leading channel in India's business and leisure travel booking market in the forecast period.

Top Companies in India Leisure & Business Travel Booking Market

The top companies operating in the market include Le Travenues Technology Ltd, Expedia India (P) Ltd, Booking Holdings Inc, Indian Railway Catering & Tourism Corp Ltd, MakeMyTrip India Pvt Ltd, Cleartrip Travel Services Pte Ltd, Yatra Online Pvt Ltd, Easy Trip Planners Ltd, International Travel House Ltd, etc., are the top players operating in the Leisure & Business Travel Booking Market.

Frequently Asked Questions

Related Report

1. Market Segmentation

1.1. Research Scope

1.2. Research Methodology

1.3. Definitions and Assumptions

2. Executive Summary

3. India Leisure & Business Travel Booking Market Policies, Regulations, and Standards

4. India Leisure & Business Travel Booking Market Dynamics

4.1. Growth Factors

4.2. Challenges

4.3. Trends

4.4. Opportunities

5. India Leisure & Business Travel Booking Market Statistics, 2022-2032F

5.1. Market Size & Growth Outlook

5.1.1. By Revenues in US$ Million

5.2. Market Segmentation & Growth Outlook

5.2.1. By Travel Sales Type

5.2.1.1. Leisure Travel- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2. Business Travel- Market Insights and Forecast 2022-2032, USD Million

5.2.2. By Booking Channel

5.2.2.1. Offline Booking- Market Insights and Forecast 2022-2032, USD Million

5.2.2.2. Online Booking- Market Insights and Forecast 2022-2032, USD Million

5.2.3. By Booking Method

5.2.3.1. Travel Intermediaries- Market Insights and Forecast 2022-2032, USD Million

5.2.3.2. Direct Suppliers- Market Insights and Forecast 2022-2032, USD Million

5.2.4. By Competitors

5.2.4.1. Competition Characteristics

5.2.4.2. Market Share & Analysis

6. India Leisure Travel Booking Market Statistics, 2022-2032F

6.1. Market Size & Growth Outlook

6.1.1. By Revenues in US$ Million

6.2. Market Segmentation & Growth Outlook

6.2.1. By Travel Sales Type- Market Insights and Forecast 2022-2032, USD Million

6.2.1.1. Leisure Air Travel- Market Insights and Forecast 2022-2032, USD Million

6.2.1.2. Leisure Car Rental- Market Insights and Forecast 2022-2032, USD Million

6.2.1.3. Leisure Cruise- Market Insights and Forecast 2022-2032, USD Million

6.2.1.4. Leisure Experiences and Attractions- Market Insights and Forecast 2022-2032, USD Million

6.2.1.5. Leisure Lodging- Market Insights and Forecast 2022-2032, USD Million

6.2.2. By Booking Channel- Market Insights and Forecast 2022-2032, USD Million

6.2.3. By Booking Method- Market Insights and Forecast 2022-2032, USD Million

7. India Business Travel Booking Market Statistics, 2022-2032F

7.1. Market Size & Growth Outlook

7.1.1. By Revenues in US$ Million

7.2. Market Segmentation & Growth Outlook

7.2.1. By Travel Sales Type- Market Insights and Forecast 2022-2032, USD Million

7.2.1.1. Business Air Travel- Market Insights and Forecast 2022-2032, USD Million

7.2.1.2. Business Car Rental- Market Insights and Forecast 2022-2032, USD Million

7.2.1.3. Business Lodging- Market Insights and Forecast 2022-2032, USD Million

7.2.1.4. Others- Market Insights and Forecast 2022-2032, USD Million

7.2.2. By Booking Channel- Market Insights and Forecast 2022-2032, USD Million

7.2.3. By Booking Method- Market Insights and Forecast 2022-2032, USD Million

8. Competitive Outlook

8.1. Company Profiles

8.1.1. Indian Railway Catering & Tourism Corp Ltd

8.1.1.1. Business Description

8.1.1.2. Service Portfolio

8.1.1.3. Collaborations & Alliances

8.1.1.4. Recent Developments

8.1.1.5. Financial Details

8.1.1.6. Others

8.1.2. MakeMyTrip India Pvt Ltd

8.1.2.1. Business Description

8.1.2.2. Service Portfolio

8.1.2.3. Collaborations & Alliances

8.1.2.4. Recent Developments

8.1.2.5. Financial Details

8.1.2.6. Others

8.1.3. Cleartrip Travel Services Pte Ltd

8.1.3.1. Business Description

8.1.3.2. Service Portfolio

8.1.3.3. Collaborations & Alliances

8.1.3.4. Recent Developments

8.1.3.5. Financial Details

8.1.3.6. Others

8.1.4. Yatra Online Pvt Ltd

8.1.4.1. Business Description

8.1.4.2. Service Portfolio

8.1.4.3. Collaborations & Alliances

8.1.4.4. Recent Developments

8.1.4.5. Financial Details

8.1.4.6. Others

8.1.5. Easy Trip Planners Ltd

8.1.5.1. Business Description

8.1.5.2. Service Portfolio

8.1.5.3. Collaborations & Alliances

8.1.5.4. Recent Developments

8.1.5.5. Financial Details

8.1.5.6. Others

8.1.6. Le Travenues Technology Ltd

8.1.6.1. Business Description

8.1.6.2. Service Portfolio

8.1.6.3. Collaborations & Alliances

8.1.6.4. Recent Developments

8.1.6.5. Financial Details

8.1.6.6. Others

8.1.7. Expedia India (P) Ltd

8.1.7.1. Business Description

8.1.7.2. Service Portfolio

8.1.7.3. Collaborations & Alliances

8.1.7.4. Recent Developments

8.1.7.5. Financial Details

8.1.7.6. Others

8.1.8. Booking Holdings Inc

8.1.8.1. Business Description

8.1.8.2. Service Portfolio

8.1.8.3. Collaborations & Alliances

8.1.8.4. Recent Developments

8.1.8.5. Financial Details

8.1.8.6. Others

8.1.9. International Travel House Ltd

8.1.9.1. Business Description

8.1.9.2. Service Portfolio

8.1.9.3. Collaborations & Alliances

8.1.9.4. Recent Developments

8.1.9.5. Financial Details

8.1.9.6. Others

9. Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Travel Sales Type |

|

| By Booking Channel |

|

| By Booking Method |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.