India Ethnic Wear Market Report: Trends, Growth and Forecast (2026-2032)

By Product Structure (Tops & Tunics, Bottomwear, Dresses, Robes & Draped Garments, Coordinated Sets & Full Outfits, Outerwear & Layering Garments), By End User (Women, Men, Kids), By Fabric Type (Cotton, Silk, Wool, Linen, Synthetic Fabrics, Blended Fabrics, Others), By Price Tier (Economy, Mid-Range, Premium, Luxury), By Product Format (Ready-to-Wear, Customized), By Distribution Channel (Retail Offline, Exclusive Brand Stores, Multi-Brand Stores, Independent/Traditional Retailers, Department Stores, Retail Online, Online Marketplaces, Brand-Owned Online Stores), By Region (North, East, West, South) ... Read more

|

Major Players

|

India Ethnic Wear Market Statistics and Insights, 2026

- Market Size Statistics

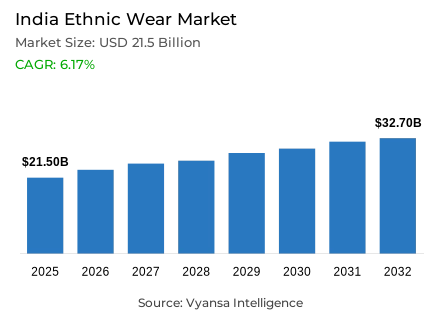

- Ethnic wear market size in India was valued at USD 21.5 billion in 2025 and is estimated at USD 22.8 billion in 2026.

- The market size is expected to grow to USD 32.7 billion by 2032.

- Market to register a CAGR of around 6.17% during 2026-32.

- Product Structure Shares

- Dresses, robes & draped garments grabbed market share of 35%.

- Competition

- More than 10 companies are actively engaged in producing ethnic wear in India.

- Top 5 companies acquired around 35% of the market share.

- Soch, Rangriti, Global Desi, Vedant Fashions, Biba etc., are few of the top companies.

- End User

- Women grabbed 70% of the market.

India Ethnic Wear Market Outlook

The India ethnic wear market was valued at USD 21.5 billion in 2025, establishing a commercially stable and culturally well-rooted foundation within one of the world's most distinctive and enduring traditional apparel ecosystems. Projected to advance from USD 22.8 billion in 2026 to USD 32.7 billion by 2032, the sector registers a compound annual growth rate of 6.17% across the forecast horizon. This steady and structurally supported expansion trajectory reflects the sustained relevance of traditional clothing across everyday household purchasing, festive occasion demand, and special-event wardrobe investment across India's diverse consumer base. Growth is anchored in deeply embedded cultural consumption patterns rather than fashion cycle volatility, giving this market a commercial resilience that sustains consistent category demand independently of broader discretionary spending fluctuations across the forecast period.

The product architecture defining this market's commercial structure is anchored in draped and robe-style garment formats. Dresses, Robes and Draped Garments command approximately 35% of total product category market share, reflecting the consistent and culturally grounded consumer preference for garment formats that combine traditional identity with practical occasion versatility across festive, family, and daily wardrobe contexts. The Ministry of Textiles' documentation that sarees and salwar kameez remain among the most widely demanded products in the domestic market confirms the structural primacy of draped and traditional garment formats in shaping overall ethnic wear category demand. This product concentration creates natural and durable demand advantages for manufacturers and retailers whose collections are built around culturally resonant formats with broad consumer familiarity and consistent repeat purchase motivation.

The end-user architecture reinforces the structural centrality of women as the category's dominant consumer group. Women account for approximately 70% of total market share, reflecting the deep and culturally embedded role of traditional apparel in women's everyday, festive, and occasion-based dressing across India's diverse regional consumer base. The Ministry of Textiles' documentation that women contribute 55.5% of textile purchases in 2024 confirms the foundational commercial significance of female consumer demand in sustaining ethnic wear category volume, collection refresh cycles, and retail investment priorities across the industry's most commercially active product segments. This consumer concentration creates a self-reinforcing demand dynamic where product variety, design refresh frequency, and occasion-linked purchasing motivation collectively sustain high repeat purchase rates across the women's ethnic wear segment.

The forward outlook through 2032 is defined by four converging structural forces whose combined commercial impact creates an ethnic wear market of sustained and well-grounded expansion momentum. India's per capita textile demand reaching INR 6,066 in 2024, documented by the Ministry of Textiles, confirms the household spending foundation that sustains consistent traditional apparel procurement across income levels and geographic markets. Cotton raw material volatility, driven by cotton imports rising from 15.20 lakh bales in 2023-24 to 41.40 lakh bales in 2024-25, creates manufacturing cost management imperatives that shape pricing strategy and fabric sourcing decisions across the industry. The Ministry of Textiles' documentation that reused and retailored textiles account for approximately 58% of the sustainable textile consumption basket in 2024 confirms the growing consumer orientation toward durable, reuse-friendly garment investment that ethnic wear's inherent longevity and cultural value naturally support. India's position as the sixth largest global textile and apparel exporter with a 4.1% world market share in 2024 opens international trade corridors that progressively expand the addressable market for ethnic wear collections beyond domestic boundaries through 2032.

India Ethnic Wear Market Growth Driver

Household Textile Demand Sustains Consistent Traditional Apparel Purchasing

The sustained and institutionally documented strength of household textile spending across India represents the primary structural driver of ethnic wear demand, functioning as a persistent consumer purchasing imperative that sustains consistent category volume across everyday wardrobe replenishment, festive occasion investment, and family event dressing across India's diverse regional and demographic consumer base. This household demand dynamic transcends fashion cycle fluctuations, reflecting a durable cultural consumption pattern whose purchasing volume generation is structurally anchored in the deep integration of traditional clothing into the everyday social, religious, and celebratory fabric of Indian household life across every major geographic and economic segment.

The quantitative evidence validating this household demand dynamic is documented with precision by the Ministry of Textiles. India's per capita demand for textiles reaches INR 6,066 in 2024, confirming a national household textile spending base of sufficient scale and consistency to sustain reliable ethnic wear category procurement independently of cyclical discretionary spending fluctuations. The Ministry's documentation that sarees and salwar kameez remain among the most widely demanded products in the domestic textile market confirms the structural primacy of ethnic apparel formats within India's household textile consumption basket. Women's contribution of 55.5% of textile purchases in 2024 further validates the consumer spending concentration within the demographic segment whose purchasing behavior most directly defines ethnic wear category demand, collection development priorities, and retail investment strategies through 2032.

India Ethnic Wear Market Challenge

Cotton Raw Material Volatility Constrains Manufacturing Cost Management

The structural volatility of cotton raw material availability and pricing represents the most consequential operational challenge confronting India's ethnic wear manufacturers, creating systematic fabric cost management, procurement planning, and retail pricing stability burdens that constrain margin management and collection investment discipline across a competitively price-sensitive traditional apparel market. In a manufacturing environment where cotton fabric costs represent a substantial proportion of total production economics, and where import dependency for raw material supply creates exposure to global commodity pricing and supply chain dynamics beyond domestic policy control, cost management discipline and supply chain diversification capability function as primary determinants of commercial viability for ethnic wear producers competing on both design quality and price accessibility.

The structural depth and policy response specificity of this cotton raw material challenge are documented with precision by the Ministry of Textiles. India's textile industry consumes approximately 94% of the country's cotton production, confirming the depth of the industry's raw material dependency on a single fiber category whose domestic supply variability creates consistent procurement planning complexity. Cotton imports rising from 15.20 lakh bales in 2023-24 to 41.40 lakh bales in 2024-25 confirm the scale of import dependency that the domestic supply shortfall has created across the industry's raw material procurement base. The government's temporary removal of the 11% import duty on cotton in 2025 and the resulting domestic price moderation from approximately INR 57,000 per candy to around INR 52,500 per candy confirm both the severity of the cost pressure and the policy intervention required to manage it. For ethnic wear manufacturers, navigating this volatility demands sustained investment in supply chain diversification and fabric cost hedging capability through 2032.

Unlock Market Intelligence

Explore the market potential with our data-driven report

India Ethnic Wear Market Trend

Sustainable and Circular Textile Consumption Reshapes Buyer Preferences

The progressive adoption of sustainable textile consumption behaviors across India's consumer base represents the defining structural trend reshaping ethnic wear product development priorities, brand communication strategies, and buyer evaluation criteria within the traditional apparel market. This sustainability trend is moving the purchase decision framework around ethnic wear beyond immediate aesthetic appeal and price accessibility into the domain of fabric durability, garment longevity, repair and alteration friendliness, and responsible consumption alignment, dimensions that are progressively redefining what quality-conscious Indian consumers consider when investing in traditional apparel across everyday and occasion-led purchase contexts.

The institutional documentation and consumer adoption scale of this sustainability trend are confirmed with precision by the Ministry of Textiles. Indian consumers are increasingly adopting sustainable textiles including recycled, reprocessed, reused, and retailored garments, confirming that responsible consumption orientation is advancing beyond urban early-adopter segments into broader mainstream buyer populations. Reused and retailored textiles account for approximately 58% of the sustainable textile consumption basket in 2024, confirming that garment extension, repair, and intergenerational use represent the dominant expressions of sustainable textile behavior among Indian consumers. This consumption pattern aligns naturally with ethnic wear's inherent longevity credentials, cultural value durability, and tradition of intergenerational garment transfer, positioning the category favorably within the emerging sustainability-conscious consumer segment. Brands that proactively align collection design, fabric selection, and brand communication with this evolving consumer value orientation will capture disproportionate loyalty among India's most sustainability-conscious ethnic wear buyers through 2032.

India Ethnic Wear Market Opportunity

Export Trade Corridors Create International Market Expansion Pathways

The expanding international trade access and growing global recognition of Indian textile craftsmanship create a structurally significant and commercially compelling opportunity for ethnic wear brands and manufacturers seeking to extend their addressable market beyond India's domestic consumer base into international diaspora, occasionwear, and premium craft fashion channels. This export opportunity is distinguished from domestic market growth by its geographic breadth, its premium pricing potential for authentic craft-based ethnic collections, and the institutional trade infrastructure whose progressive strengthening is reducing market entry friction and expanding distribution access for Indian ethnic apparel exporters in key international consumer markets.

The quantitative scale and trade access specificity of this international opportunity are documented with precision by the Ministry of Textiles. India is the sixth largest exporter of textiles and apparel globally, with a 4.1% share of world textile trade in calendar year 2024, and the sector contributes 8.63% of India's total merchandise exports in 2024-25. India has signed 15 free trade agreements with partner countries whose combined textile import demand stands at USD 198.9 billion, while the EU alone imports textiles worth USD 268.8 billion, confirming the scale of the international market access that these trade frameworks make commercially accessible to compliant Indian ethnic wear exporters. For ethnic wear brands that invest in export-oriented collection development, international quality certification, and digital commerce infrastructure capable of reaching diaspora and global craft fashion consumer segments, these trade corridors create compelling and progressively more accessible international revenue diversification opportunities through 2032.

Unlock Market Intelligence

Explore the market potential with our data-driven report

India Ethnic Wear Market Segmentation Analysis

By Product Structure

- Tops & Tunics

- Bottomwear

- Dresses, Robes & Draped Garments

- Coordinated Sets & Full Outfits

- Outerwear & Layering Garments

The segment with highest market share under the Product Category is Dresses, Robes and Draped Garments, accounting for approximately 35% of the total market. This commanding position reflects the deep structural alignment between draped garment formats and the specific cultural, aesthetic, and occasion-versatility requirements that define mainstream ethnic wear consumer demand across India's diverse regional markets. With more than one-third of total market value concentrated within a single product category, Dresses, Robes and Draped Garments define the collection development priorities, retail shelf allocation strategies, and brand investment frameworks of the India ethnic wear industry. The Ministry of Textiles' confirmation that sarees and salwar kameez remain among the most widely demanded products in the domestic textile market validates the cultural depth and consumer familiarity that sustain this product category's commercial leadership across multiple consumer segments, geographic regions, and buying occasions simultaneously.

The structural leadership of this product category is further sustained by its inherent versatility across the full spectrum of ethnic wear consumption occasions, from daily household use through festive celebrations to formal family events, a breadth of application that creates consistent and compounding repeat purchase demand well beyond the seasonal spikes that characterize less versatile apparel categories. As consumer orientation toward sustainable textile consumption deepens and intergenerational garment use becomes more commercially visible, the draped garment category's natural alignment with repair, alteration, and extended service life values positions it favorably within the emerging sustainability-conscious segment of India's ethnic wear buyer population. The segment's structural dominance as the market's primary revenue contributor is expected to consolidate through 2032.

By End User

- Women

- Men

- Kids

The segment with highest market share under the End User is Women, accounting for approximately 70% of the total market. This dominant position reflects the foundational and culturally embedded role of traditional apparel in women's everyday wardrobe decisions, festive occasion purchasing, and family event dressing across India's diverse regional consumer base, where ethnic wear's cultural resonance, style variety, and occasion-linked emotional significance create consistent and high-frequency purchasing motivation across all major demographic segments within the women's consumer population. With seven-tenths of total market value anchored in women's demand, this end-user segment defines the product development priorities, collection design strategies, and retail merchandising frameworks of the India ethnic wear market.

The structural leadership of the Women segment is being actively sustained by the consistent and institutionally documented prominence of female consumers in India's broader textile purchasing activity. The Ministry of Textiles' documentation that women contribute 55.5% of textile purchases in 2024 confirms that female consumer spending authority extends across the full textile category landscape, with ethnic wear benefiting disproportionately from this spending concentration given the category's deep alignment with women's cultural dressing traditions and style preferences. As product variety within the women's ethnic wear segment continues to expand across price points, design aesthetics, and occasion-specific formats, the purchasing frequency, brand engagement depth, and collection loyalty dynamics of this consumer segment are expected to sustain and strengthen the category's commercial growth trajectory through 2032.

List of Companies Covered in India Ethnic Wear Market

The companies listed below are highly influential in the India ethnic wear market, with a significant market share and a strong impact on industry developments.

- Soch

- Rangriti

- Global Desi

- Vedant Fashions

- Biba

- Fabindia

- TCNS Clothing

- Libas

- Indya

- Koskii

Market News & Updates

- Vedant Fashions, 2026:

Vedant Fashions’ February 2026 investor presentation reaffirmed its leadership in Indian wedding and celebration wear, noting 648 EBOs across 241 Indian cities and towns, 16 overseas EBOs, and 9M FY26 retail sales growth of 5.4 percent, while also highlighting its multi-brand portfolio spanning Manyavar, Mohey, Twamev, Mebaz, and Diwas. For the India ethnic wear market, this matters because it shows the country’s most scaled organized player continuing to formalize and widen the category through brand segmentation, deeper city penetration, and sustained retail expansion, which raises competitive pressure on other branded ethnic-wear chains to match both reach and assortment sophistication.

- Libas, 2025:

In August 2025, Libas published official news posts stating that it “eyes 100 stores, Rs 1,000 cr, IPO, & a global ‘Indian Wear’ push” and, just days later in its Press Releases section, that it was set to launch 11 new stores on 15th of August as part of a strong offline push. For the India ethnic wear market, this is one of the clearest verified scale-up moves among the named brands because it signals that digital-native ethnic-wear specialists are rapidly building physical retail networks and preparing for larger capital-market and international ambitions, which strengthens the organized mid-premium segment and accelerates the shift toward omnichannel ethnic fashion retail in India

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- India Ethnic Wear Market Policies, Regulations, and Standards

- India Ethnic Wear Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- India Ethnic Wear Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Product Structure

- Tops & Tunics- Market Insights and Forecast 2022-2032, USD Million

- Bottomwear- Market Insights and Forecast 2022-2032, USD Million

- Dresses, Robes & Draped Garments- Market Insights and Forecast 2022-2032, USD Million

- Coordinated Sets & Full Outfits- Market Insights and Forecast 2022-2032, USD Million

- Outerwear & Layering Garments- Market Insights and Forecast 2022-2032, USD Million

- By End User

- Women- Market Insights and Forecast 2022-2032, USD Million

- Men- Market Insights and Forecast 2022-2032, USD Million

- Kids- Market Insights and Forecast 2022-2032, USD Million

- By Fabric Type

- Cotton- Market Insights and Forecast 2022-2032, USD Million

- Silk- Market Insights and Forecast 2022-2032, USD Million

- Wool- Market Insights and Forecast 2022-2032, USD Million

- Linen- Market Insights and Forecast 2022-2032, USD Million

- Synthetic Fabrics- Market Insights and Forecast 2022-2032, USD Million

- Blended Fabrics- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By Price Tier

- Economy- Market Insights and Forecast 2022-2032, USD Million

- Mid-Range- Market Insights and Forecast 2022-2032, USD Million

- Premium- Market Insights and Forecast 2022-2032, USD Million

- Luxury- Market Insights and Forecast 2022-2032, USD Million

- By Product Format

- Ready-to-Wear- Market Insights and Forecast 2022-2032, USD Million

- Customized- Market Insights and Forecast 2022-2032, USD Million

- By Distribution Channel

- Retail Offline- Market Insights and Forecast 2022-2032, USD Million

- Exclusive Brand Stores- Market Insights and Forecast 2022-2032, USD Million

- Multi-Brand Stores- Market Insights and Forecast 2022-2032, USD Million

- Independent/Traditional Retailers- Market Insights and Forecast 2022-2032, USD Million

- Department Stores- Market Insights and Forecast 2022-2032, USD Million

- Retail Online- Market Insights and Forecast 2022-2032, USD Million

- Online Marketplaces- Market Insights and Forecast 2022-2032, USD Million

- Brand-Owned Online Stores- Market Insights and Forecast 2022-2032, USD Million

- By Region

- North

- East

- West

- South

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Product Structure

- Market Size & Growth Outlook

- India Tops & Tunics Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By End User- Market Insights and Forecast 2022-2032, USD Million

- By Fabric Type- Market Insights and Forecast 2022-2032, USD Million

- By Price Tier- Market Insights and Forecast 2022-2032, USD Million

- By Product Format- Market Insights and Forecast 2022-2032, USD Million

- By Distribution Channel- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- India Bottomwear Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By End User- Market Insights and Forecast 2022-2032, USD Million

- By Fabric Type- Market Insights and Forecast 2022-2032, USD Million

- By Price Tier- Market Insights and Forecast 2022-2032, USD Million

- By Product Format- Market Insights and Forecast 2022-2032, USD Million

- By Distribution Channel- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- India Dresses, Robes & Draped Garments Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By End User- Market Insights and Forecast 2022-2032, USD Million

- By Fabric Type- Market Insights and Forecast 2022-2032, USD Million

- By Price Tier- Market Insights and Forecast 2022-2032, USD Million

- By Product Format- Market Insights and Forecast 2022-2032, USD Million

- By Distribution Channel- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- India Coordinated Sets & Full Outfits Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By End User- Market Insights and Forecast 2022-2032, USD Million

- By Fabric Type- Market Insights and Forecast 2022-2032, USD Million

- By Price Tier- Market Insights and Forecast 2022-2032, USD Million

- By Product Format- Market Insights and Forecast 2022-2032, USD Million

- By Distribution Channel- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- India Outerwear & Layering Garments Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By End User- Market Insights and Forecast 2022-2032, USD Million

- By Fabric Type- Market Insights and Forecast 2022-2032, USD Million

- By Price Tier- Market Insights and Forecast 2022-2032, USD Million

- By Product Format- Market Insights and Forecast 2022-2032, USD Million

- By Distribution Channel- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- Vedant Fashions

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Biba

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Fabindia

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- TCNS Clothing

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Libas

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Soch

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Rangriti

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Global Desi

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Indya

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Koskii

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Vedant Fashions

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Product Structure |

|

| By End User |

|

| By Fabric Type |

|

| By Price Tier |

|

| By Product Format |

|

| By Distribution Channel |

|

| By Region |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.