France 155mm Artillery Shells Market Report: Trends, Growth and Forecast (2026-2032)

By Shell Type (High-Explosive (HE\HE-FRAG) Shell, Smoke Shell, Illumination Shell, Training/Practice Shell, Other Special-Purpose Shell), By Guidance (Unguided, Precision-Guided), By Range Class (Standard Range, Extended Range, Assisted Range (Base Bleed, Rocket-Assisted (RAP))), By Operational Use (Training Consumption, Routine Peacetime Stockpile Replenishment, Active Conflict Replenishment\Urgent Operational Demand, Strategic Reserve\Surge Inventory Build), By Artillery Platform Type (Towed Howitzers, Self-Propelled Howitzers, Truck-Mounted Howitzers) ... Read more

|

Major Players

|

France 155mm Artillery Shells Market Statistics and Insights, 2026

- Market Size Statistics

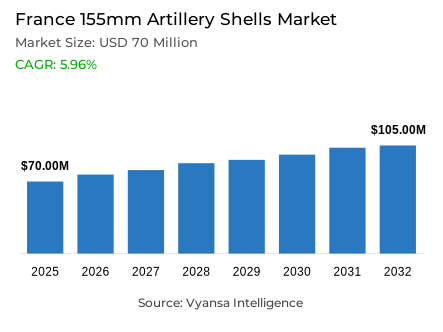

- 155mm artillery shells market size in France was estimated at USD 70 million in 2025.

- The market size is expected to grow to USD 105 million by 2032.

- Market to register a CAGR of around 5.96% during 2026-32.

- Shell Type Shares

- High-explosive (he/he-frag) shell grabbed market share of 65%.

- Competition

- 155mm artillery shells in France is currently being catered to by more than 10 companies.

- Top 5 companies acquired around 70% of the market share.

- Thales, Elbit Systems, General Dynamics Ordnance & Tactical Systems, Nexter (KNDS France), Eurenco etc., are few of the top companies.

- Guidance

- Unguided grabbed 80% of the market.

France 155mm Artillery Shells Market Outlook

The France 155mm Artillery Shells Market is valued at approximately USD 70 million in 2025 and is projected to reach USD 105 million by 2032, registering a CAGR of around 5.96% during 2026-32. This steady growth trajectory is underpinned by a structured scale-up in domestic manufacturing capacity, with monthly shell delivery volumes rising from 1,000 units before February 2023 to 3,000 units by early 2024. EU-level financing through the Act in Support of Ammunition Production (ASAP), which allocated €500 million across 31 projects and mobilised approximately €1.4 billion in combined public and private financing, is reinforcing this momentum and reducing capital risk for French producers.

A critical enabler of sustained growth is the re-shoring of upstream propellant supply. Eurenco's €60 million investment at its Bergerac facility, targeting 1,200 tonnes of large-calibre powder annually and up to 500,000 modular charges, directly addresses the most acute bottleneck constraining output of 155mm artillery shells - energetic material availability. ASAP has directed roughly three-quarters of its funding toward powders and explosives, acknowledging that upstream inputs, not final assembly, are the binding constraint on throughput.

From a segmentation perspective, high-explosive (HE/HE-FRAG) rounds dominate shell type demand with approximately 65% market share, valued for their versatility across suppression, neutralisation, and counter-battery missions. Unguided munitions account for around 80% of the guidance segment, driven by their lower unit cost and suitability for high-rate fire operations.

Looking ahead, the dual-track procurement strategy - sustaining large unguided inventories while selectively building precision stocks such as KNDS's KATANA® guided round - signals a gradual but meaningful evolution in demand composition. Combined with EU joint procurement incentives under EDIRPA's €310 million programme, France is well-positioned as a strategically autonomous and commercially attractive hub for 155mm artillery shell supply through 2032.

France 155mm Artillery Shells Market Growth DriverExpansion of Monthly Production Capacity Fuelling Market Growth

The France 155mm artillery shells market is experiencing significant momentum, underpinned by a structured scale-up in domestic manufacturing capacity. In a formal hearing before the National Assembly's Defence Committee in February 2024, the Minister of the Armed Forces confirmed that France's monthly 155mm shell delivery capacity grew from 1,000 units prior to February 2023, to 2,000 units in January 2024, and reached 3,000 units by the date of the hearing. This progressive ramp-up demonstrates the state's firm commitment to restoring strategic ammunition reserves and meeting both domestic and partner support obligations.

Complementing national efforts, EU-level financing has emerged as a powerful enabler for capacity investment across the 155mm value chain. Under the Act in Support of Ammunition Production (ASAP), the European Commission allocated €500 million across 31 projects, mobilising combined public and private financing of approximately €1.4 billion. French producers stand to benefit directly from this co-funding, which supports faster upgrades at existing facilities, reduces the capital intensity of expansion, and aligns output standards with EU interoperability requirements - collectively acting as key growth factors sustaining the France 155mm artillery shells market.

France 155mm Artillery Shells Market ChallengeEnergetic Materials Bottlenecks Constraining Output Scalability

Despite the positive trajectory in shell delivery rates, the France 155mm artillery shells market faces a structural constraint rooted in the upstream supply of energetic materials. Propellants and high explosives represent the most acute production bottleneck, a challenge formally recognised by the European Commission, which directed approximately three-quarters of ASAP funding toward these inputs - allocating €248 million for powder capacity and €124 million for explosives capacity. This funding allocation reflects the degree to which raw material supply limits the rate of final ammunition output.

The challenge is compounded by the inherently slow pace of adding new energetic materials capacity. New production lines necessitate highly specialised equipment, extended safety certification timelines, and a skilled workforce trained for hazardous manufacturing environments. The Commission has noted that ASAP supports projects targeting an increase of more than 10,000 tonnes of powder and 4,300 tonnes of explosives annually - underscoring that inputs, not assembly, are the binding constraint on throughput in the France 155mm artillery shells market. Until these upstream limitations are resolved, downstream output gains will remain partially capped.

Unlock Market Intelligence

Explore the market potential with our data-driven report

France 155mm Artillery Shells Market TrendRe-Localisation of Propellant Manufacturing as a Strategic Imperative

One of the major trends that are redefining the French 155mm artillery shell market is the strategic reshoring of key upstream suppliers, especially large-calibre propellant powder. The Ministry of the Armed Forces has emphasized the fact that Eurenco has decided to transfer the production of large-calibre powder to its plant at Bergerac, with the help of a 60 million investment. This strategic action is clearly positioned as a supply-security action, to decrease the reliance of France on cross-border sourcing of propellants and enhance national control over the quality, safety, and continuity of this essential input.

The Bergerac project will have a production capacity of 1,200 tonnes of large-calibre powder per annum, enough to produce up to 500,000 modular charges per annum. This move is a structural change in the supply architecture of the market- rooting a hitherto fragmented and internationally distributed propellant supply chain squarely on French soil. Simultaneously, the development and introduction of KNDS KATANA(r) 155mm high-precision guided round, after a DGA contract notification in June 2024, is an indicator of an increasing trend towards precision-guided munitions co-existing with high-volume unguided production.

France 155mm Artillery Shells Market OpportunityEU Co-Funding and Re-Shoring Investments Opening New Avenues for Suppliers

The France 155mm artillery shells market presents significant opportunities for domestic and EU-aligned manufacturers, particularly in the context of large-scale public investment and strategic re-industrialisation. The €500 million budget of the ASAP programme, which includes explosives, powder, shells, missiles, and testing, has established a clear pipeline of funded projects to which suppliers can add. To French producers, EU co-financing is a significant mitigation of financial risk of capacity expansion, allowing investment decisions that would otherwise be postponed in a pure market-driven environment.

Furthermore, the European Defence Industry Reinforcement through Common Procurement Act (EDIRPA) work programme, which has a budget of 310 million, presents systematic incentives to joint procurement - expanding tender visibility to qualified ammunition and component end users across member states. This joint procurement model creates repetitive demand signals that are useful to suppliers during long-term capacity planning. The current reshoring program at Bergerac, together with EU-supported production modernizations along the value chain, makes France a stable and strategically independent center of supply of 155mm artillery shells, which offers long-term commercial prospects in the market.

Unlock Market Intelligence

Explore the market potential with our data-driven report

France 155mm Artillery Shells Market Segmentation Analysis

By Shell Type

- High-Explosive (HE\HE-FRAG) Shell

- Smoke Shell

- Illumination Shell

- Training/Practice Shell

- Other Special-Purpose Shell

Within the France 155mm artillery shells market, segmentation by shell type reveals a pronounced concentration in high-explosive (HE/HE-FRAG) Shell, which command approximately 65% of the market share. This dominant position reflects the versatility of HE rounds across a broad spectrum of artillery missions, including area suppression, trench neutralisation, and counter-battery fire. Their multi-mission applicability makes them the default procurement choice for military end users engaged in stock building, routine training, and rapid replenishment to support both domestic operational readiness and partner assistance programmes.

Other shell types - including smoke, illumination, and training rounds - remain operationally essential but occupy a comparatively limited share of overall procurement volumes. These categories are typically procured in smaller lots, as their deployment is event-driven, tied to specific tactical scenarios such as screening operations, target marking, night-time fire support, or scheduled training exercises. Unlike HE rounds, which are consumed continuously whenever firing rates rise, these situational shell types exhibit more predictable and lower-frequency demand cycles - a pattern that simplifies planning for both end users and suppliers in the France 155mm artillery shells market.

By Guidance

- Unguided

- Precision-Guided

The guidance segmentation of the France 155mm artillery shells market is heavily weighted toward unguided munitions, which account for approximately 80% of overall market share. Unguided 155mm shells remain the cornerstone of volume-intensive artillery operations, valued for their lower unit cost, simpler logistics requirements, and suitability for sustained high-rate fire missions. For end users focused on area effects and rapid force-on-force engagements, unguided rounds offer a practical and scalable solution that supports continuous procurement and replenishment at scale without complex handling or targeting infrastructure.

Notwithstanding this dominance, the precision-guided munitions segment is gaining traction as complementary technology to high-volume unguided operations. The DGA's June 2024 contract notification to KNDS for the development of the KATANA® 155mm high-precision guided round represents a concrete step toward industrialising precision options for select high-value targets. This development signals a dual-track procurement strategy, wherein end users sustain large unguided inventories for general engagements while building targeted stocks of guided munitions for precision missions. This trajectory is expected to gradually reshape the guidance segmentation landscape of the France 155mm artillery shells market over the coming years.

List of Companies Covered in France 155mm Artillery Shells Market

The companies listed below are highly influential in the France 155mm artillery shells market, with a significant market share and a strong impact on industry developments.

- Thales

- Elbit Systems

- General Dynamics Ordnance & Tactical Systems

- Nexter (KNDS France)

- Eurenco

- Rheinmetall

- Nammo

- BAE Systems

- MSM Group

- Denel PMP

Market News & Updates

- Nexter (KNDS France), 2025:

KNDS France disclosed a 3-year Long Term Agreement (LTA) with Les Forges de Tarbes to secure hollow 155mm shell bodies in the context of ramping 155mm output under France’s “war-economy” posture, with planned supply of ~60,000 to 150,000 shell bodies over 2026-2028 (and an option to extend), enabling Tarbes’ capacity ramp and locking in a critical domestic bottleneck component for France’s 155mm ammunition industrial base—improving visibility for scaling, investment planning, and sustained production cadence.

- Eurenco, 2025:

EURENCO reported signing a major three-year supply contract with a European munitions manufacturer for >200,000 units of 155mm modular charges and base-bleed products manufactured at its Bergerac and Sorgues sites in France, a commercially significant demand signal that supports higher utilization (and expansion economics) for French energetic-materials capacity while de-risking upstream supply for 155mm ammunition assembly programs tied to national and broader European replenishment needs.

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- France 155mm Artillery Shells Market Policies, Regulations, and Standards

- France 155mm Artillery Shells Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- France 155mm Artillery Shells Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Shell Type

- High-Explosive (HE\HE-FRAG) Shell- Market Insights and Forecast 2022-2032, USD Million

- Smoke Shell- Market Insights and Forecast 2022-2032, USD Million

- Illumination Shell- Market Insights and Forecast 2022-2032, USD Million

- Training/Practice Shell- Market Insights and Forecast 2022-2032, USD Million

- Other Special-Purpose Shell- Market Insights and Forecast 2022-2032, USD Million

- By Guidance

- Unguided - Market Insights and Forecast 2022-2032, USD Million

- Precision-Guided - Market Insights and Forecast 2022-2032, USD Million

- By Range Class

- Standard Range - Market Insights and Forecast 2022-2032, USD Million

- Extended Range - Market Insights and Forecast 2022-2032, USD Million

- Assisted Range- Market Insights and Forecast 2022-2032, USD Million

- Base Bleed- Market Insights and Forecast 2022-2032, USD Million

- Rocket-Assisted (RAP)- Market Insights and Forecast 2022-2032, USD Million

- By Operational Use

- Training Consumption- Market Insights and Forecast 2022-2032, USD Million

- Routine Peacetime Stockpile Replenishment- Market Insights and Forecast 2022-2032, USD Million

- Active Conflict Replenishment\Urgent Operational Demand- Market Insights and Forecast 2022-2032, USD Million

- Strategic Reserve\Surge Inventory Build- Market Insights and Forecast 2022-2032, USD Million

- By Artillery Platform Type

- Towed Howitzers- Market Insights and Forecast 2022-2032, USD Million

- Self-Propelled Howitzers- Market Insights and Forecast 2022-2032, USD Million

- Truck-Mounted Howitzers- Market Insights and Forecast 2022-2032, USD Million

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Shell Type

- Market Size & Growth Outlook

- France High-Explosive (HE\HE-FRAG) Shells Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Guidance- Market Insights and Forecast 2022-2032, USD Million

- By Range Class - Market Insights and Forecast 2022-2032, USD Million

- By Operational Use - Market Insights and Forecast 2022-2032, USD Million

- By Artillery Platform Type - Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- France Smoke Shells Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Guidance- Market Insights and Forecast 2022-2032, USD Million

- By Range Class - Market Insights and Forecast 2022-2032, USD Million

- By Operational Use - Market Insights and Forecast 2022-2032, USD Million

- By Artillery Platform Type - Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- France Illumination Shells Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Guidance- Market Insights and Forecast 2022-2032, USD Million

- By Range Class - Market Insights and Forecast 2022-2032, USD Million

- By Operational Use - Market Insights and Forecast 2022-2032, USD Million

- By Artillery Platform Type - Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- France Training/Practice Shells Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Guidance- Market Insights and Forecast 2022-2032, USD Million

- By Range Class - Market Insights and Forecast 2022-2032, USD Million

- By Operational Use - Market Insights and Forecast 2022-2032, USD Million

- By Artillery Platform Type - Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- Nexter (KNDS France)

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Eurenco

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Rheinmetall

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Nammo

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- BAE Systems

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Thales

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Elbit Systems

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- General Dynamics Ordnance & Tactical Systems

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- MSM Group

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Denel PMP

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Nexter (KNDS France)

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Shell Type |

|

| By Guidance |

|

| By Range Class |

|

| By Operational Use |

|

| By Artillery Platform Type |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.